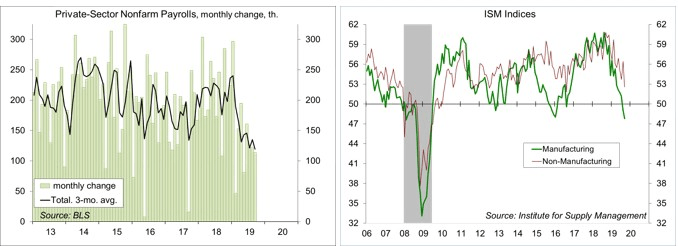

The ISM Manufacturing Index surprised to the downside, falling further into contraction in September and renewing recession fears. The Non-Manufacturing Index also came in lower than anticipated, but remained consistent with an expansion in the overall economy (but at a slower pace). The Employment Report was mixed, but helped to offset concerns that we have entered a downturn. Yet, that was never much in doubt. The worry is that the economy may slip into a recession in 2020. The 2020 outlook revolves around trade policy, changing demographics, and the Fed. We’ll hear from Chair Powell this week.

We’ve often experienced contractions in manufacturing with a downturn in the overall economy. That was the case in 2015-2016, when a correction in energy exploration contributed to declines in industrial production and business fixed investment. Unlike that slowdown, the current weakness is largely self-inflicted. U.S. manufacturers use parts and supplies from around the world. Tariffs, particularly the May 10 escalation, raise costs, invite retaliation, and disrupt supply chains. Firms report a lack of visibility on prices for inputs from abroad. Many don’t know if they will be able to get supplies next year. The uncertainty undermines business fixed investment. While a completed trade deal with China appears unlikely, a truce in trade tensions ought to be viewed favorably. This could include a postponement of the final round of tariffs on Chinese goods, or the rollback of some of the existing tariffs. However, following last week’s WTO ruling, tariffs are set to rise on goods from Europe (again, it is U.S. consumers and businesses that pay the price).

The ISM survey results are diffusion indices and do not measure actual activity. They are more like a sentiment gauge. Small moves in the headline figures are essentially irrelevant. The numbers often bounce around from month to month. However, a trend higher or lower is significant – and the decline in the manufacturing gauge in August and September coincides with other indicators of factory sector weakness.

The ISM Non-Manufacturing Index is more indicative of overall economic growth. The survey results were unexpectedly strong in August, but surprisingly soft in September. Don’t read too much into that. A further decline in October would be unsettling, but we won’t know until we get that report.

Manufacturing and business fixed investment are in a slow patch, to be sure, but consumer spending accounts for 68% of Gross Domestic Product. Strong household fundamentals are expected to support spending growth well into 2020. However, if the economy were to enter a recession, we are most likely to see it in the job market. The unemployment rate is a lagging indicator. Nonfarm payrolls are a coincident indicator, and jobless claims are a leading indicator. Nonfarm payrolls are still growing, indicating that we are not in a recession now, and claims are still trending at a low level, suggesting that we’re not likely to be in a recession anytime soon.

Financial market participants and the financial press focus too much on the monthly payroll figure. There’s a lot of noise in the headline number (the month change in payrolls is reported accurate to ±110,000). With the start of the school year, education jobs rose by 1.45 million before seasonal adjustment, while we shed 1.09 million non-education jobs (reflecting the end of the summer travel season). Are we really going to worry about the nearest 20,000-30,000 in the adjusted number? The three-month average reduces (but does not eliminate) much of the monthly noise in the payroll figure. Private-sector payrolls have averaged a 119,000 monthly gain in 3Q19. The trend has slowed. The question is whether that reflects a slowing in the economy or more binding constraints in the labor market (not enough people to hire). However, demographic changes suggest that we need less than 100,000 jobs per month to absorb new entrants into the workforce. We’ve grown accustomed to thinking that monthly job gains of 200,000 to 300,000 are normal. That’s not going to be the case going forward. Workers are also consumers. Barring an unprecedented pickup in productivity growth (which is even more doubtful as business investment softened), the shift in the labor force outlook implies that overall economic growth will be a lot slower. Trend GDP growth ought to be around 1.5-2.0%.

A slower trend in GDP growth means that recessions are likely to become more common over time. While a 2020 recession does not appear to be the most likely scenario, the odds of entering a downturn within the next 12 months have gone up (currently near 40%). A further escalation in trade tensions would further increase the odds of a recession and it’s unclear whether the Fed can offset the impact. Fed Chairman Powell will speak Tuesday on “Data Dependence in an Evolving Economy.” On Friday, Powell said that “one clear takeaway of the [Fed Listens] sessions so far is the importance of sustaining our historically strong job market.”

Data Recap – The ISM Manufacturing Index fell further into contraction in September, reigniting recession fears. The ISM Non-Manufacturing was also lower than expected, but consistent with expansion in the overall economy (although at a slower pace). Nonfarm payrolls rose a bit less than anticipated in September, but not as bad as feared, offset by an upward revision to July and August. Average hourly earnings were mixed, flat overall, but higher for production workers. The unemployment rate edged down, to the lowest level since 1969.

The September Employment Report was a mixed bag. Nonfarm payrolls rose by 136,000 (median forecast: +145,000, whisper number: +125,000), with a net revision to July and August of +45,000. There was only a 1,000 gain in temporary hiring for the 2020 census (vs. +25,000 in August). Private-sector payrolls rose by 114,000, leaving the three-month average at 119,000 (a +184,000 average over the last eight months).

The ISM Manufacturing Index fell to 47.8 in September, vs. 49.1 in August and 51.2 in July. New orders, production, and employment were below the breakeven level. Order backlogs fell for the fifth consecutive month (not good). Input price pressures were flat. Global trade remained the most significant issue facing supply managers.

The ISM Non-Manufacturing Index fell to 52.6 in September, vs. 56.4 in August and 53.7 in July. Business activity and new orders continued to advance, but more slowly. Employment growth was modest. Input price pressures picked up. Comments from supply managers were mixed, but still showed concerns about tariffs, labor constraints, and the direction of the economy.

Unit Motor Vehicle Sales edged up to a 17.2 million seasonally adjusted annual rate in September, vs. 17.0 million in August and 17.3 million a year ago. The 3Q19 pace was the same as in 2Q19.

The U.S. Trade Deficit widened to $54.9 in August, vs. $54.0 billion in July and a $54.4 billion average for 2Q19. Year‐to‐date, the goods and services deficit increased by $28.3 billion (+7.1%), from the same period in 2018. Exports decreased $3.2 billion (-0.2%), while imports increased

$25.1 billion (+1.2%)

The ADP Estimate of private-sector payrolls rose by 135,000 in the initial estimate for September, while the August gain was revised to +157,000 (from +195,000). The 3Q19 average was +145,000, vs. +214,000 in 3Q18. “Businesses have turned more cautious in their hiring, according to the report, while “small businesses have become especially hesitant.”

The Challenger Job-Cut Report showed that announced layoff intentions totaled 41,557 in September, vs. 53,480 in August and 55,285 a year ago (these data are not seasonally adjusted). The total for the first nine months of 2019 was 27.0% higher than the same period in 2018. These are announced layoff intentions – not actual layoffs – but the recent trend bears watching.

The Chicago Business Barometer fell to 47.1 in September, vs. 50.4 in August ad 44.4 in July (like other regional factory sector surveys, these data tend to be choppy). It was the lowest quarterly average since 3Q09. Production fell 7.6 points to 40.4, the lowest since May 2009. New orders shifted back to contraction (48.5). The employment gauge improved to 45.6, although still below the breakeven level and the lowest quarterly average since 4Q09.

Factory Orders fell 0.1% in August (-1.9% y/y), mixed across industries. Durable goods orders rose 0.2% (-3.0% y/y), with civilian aircraft orders down 17.1 and defense aircraft up 32.6%. Orders for nondefense capital goods ex-aircraft fell 0.4% (revised from -0.2%)

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.