If You’re Not Long, You’re Wrong

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

This week I visited beautiful Vancouver to attend the CEO Martini Party. The annual event, hosted by Stockhouse, is an opportunity for business leaders representing a number of industries to connect and meet with newsletter writers and potential investors.

It was great to catch up with some old faces and to get to know some new ones. I want to thank Cindy Broad and everyone else at Stockhouse for putting on another successful event!

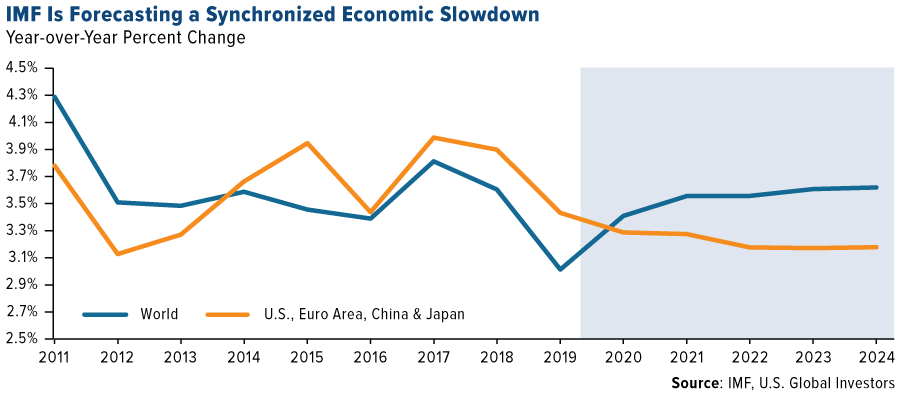

In my keynote address, I explained why I’m bullish going forward despite signs that the world could be facing its worst economic slowdown since the financial crisis. Just this week, the International Monetary Fund (IMF) downgraded its 2019 growth forecast to 3 percent, a significant drop from the past couple of years.

The reason for my bullishness is simple: Bad news is good news. Policymakers and heads of states see the threat of a slowdown and are more likely to enact stimulus measures to prevent a full-blown recession. This is especially the case in nations with upcoming federal elections—the biggest one being the U.S. presidential election.

President Donald Trump is under pressure from a series of House investigations, not to mention an impeachment inquiry that’s near guaranteed to result in official articles of impeachment. Be that as it may, Trump is the only U.S. president that I’m aware of who sees the market as a barometer of his policies’ success. Every morning, after he wakes up and coifs his hair in the mirror, he wonders what his administration can do to drive stocks higher. We’ve already seen aggressive corporate tax cuts and a wave of deregulation, and we may expect to see more as Trump seeks reelection. So even though you may not like the man’s governing style or his Twitter activity, he always has investors’ interests in mind.

Fiscal-Monetary Imbalance Is a Global Growth Headwind

|

The same cannot be said of policymakers in the European Union (EU), where much of the slowdown is currently happening. Germany, the world’s fourth largest economy, is facing a recession. The problem is that there’s a massive imbalance between fiscal and monetary policymaking. Instead of doing as the U.S. has done—cutting taxes, rolling back business-killing regulations—EU strategy has been to keep rates at near-zero or lower. Denmark, for instance, now pays borrowers to take out a mortgage.

This is unsustainable, and there are many market watchers, including Bill Gross, who believe we’ve seen the end of what negative rates can achieve. In his most recent investment outlook, the legendary co-founder of PIMCO says that zero-bound easing may have helped asset markets over the past decade, but it will not be enough to keep the bull market running.

Central bank governors “are becoming wise to the negative effects of rates at zero (or less) that literally rob small savers and larger financial institutions such as banks, insurance companies and pension funds of their ability to earn historically ‘guaranteed’ carry,” Gross writes.

To prepare for “slow economic growth globally,” he has a tried-and-true solution: “High yielding, secure-dividend stocks are what an astute investor should begin to own.”

I agree, and Gross’ advice is in line with what I told listeners at the Stockhouse event this week: If you’re not long, you’re wrong.

Gold Continues to Look Attractive in a Low-Rate Environment

Lower-for-longer rates also favor commodities and gold prices. The last time we saw gold go in a cycle like this, it went from the mid-$200s up to $1,900 an ounce. You can easily get a fivefold increase or more in its price, which is why I believe $10,000 gold could happen the longer supply trails behind money supply.

Speaking of gold… On October 31, I’ll be participating in a webcast on investing opportunities in the gold mining industry. I’m excited to tell you that I’ll be joined by mining legend Pierre Lassonde, who recently said that the yellow metal could hit $25,000 by 2049. To register for the webcast, just email us at [email protected]. Slots are filling up fast!

A Year Since Canada Legalized Recreational Cannabis

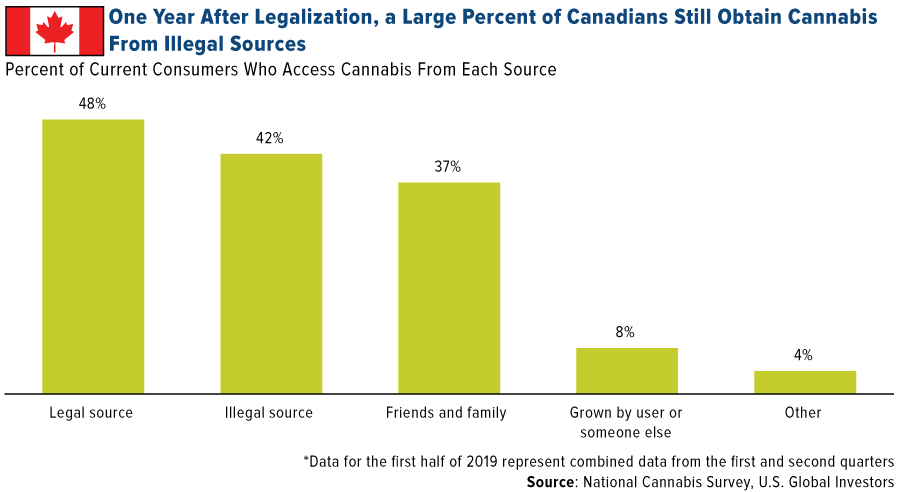

One year ago this week, Canada became the first major country to legalize recreational cannabis for adults. (Uruguay was the very first to do so, in December 2013.) As such, a few other countries—including Luxembourg, Mexico, New Zealand and Russia—are keeping their eyes on Canada to see how things are going.

And with good reason: It’s estimated that the size of Canada’s recreational market will hit $5.2 billion by 2024, up from $569 million in 2018, for an incredible compound annual growth rate (CAGR) of 44.4 percent.

As I told you, I was in Vancouver this week, and the local news spent a lot of time reflecting on this important milestone. I was surprised to learn that, despite legalization, a significant percent of Canadians still get their cannabis from illegal sources. About half of Canadians said they bought supply from a legal source in the first half of 2019, while a whopping 42 percent said they bought it from an illegal source.

The main reason for this is that rollout has been cautiously slow. To date there are only seven official BC Cannabis Store locations in all of British Columbia, none of them in Greater Vancouver.

The same caution is being taken with edibles, which became legal for the first time this past week. (“Edibles” is the catch-all term for THC-infused products such as gummies, cookies, beverages and topical creams.) Even though they’re now legal, they won’t actually be on store shelves for another few weeks as the Canadian government begins accepting applications from companies seeking to produce and sell the products.

It’s a work in progress, but an exciting one nonetheless. For early stage investors in particular, there’s definitely money to be made.

Gold Market

This week spot gold closed at $1,489.85, up $0.75 per ounce, or 0.05 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.03 percent. The S&P/TSX Venture Index came in up just 0.31 percent. The U.S. Trade-Weighted Dollar fell 1.10 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-15 | Germany ZEW Survey Current Situation | -23.6 | -25.3 | -19.9 |

| Oct-15 | Germany ZEW Survey Expectations | -26.4 | -22.8 | -22.5 |

| Oct-16 | Eurozone CPI Core YoY | 1.0% | 1.0% | 1.0% |

| Oct-17 | Housing Starts | 1320k | 1256k | 1386k |

| Oct-17 | Initial Jobless Claims | 215k | 214k | 210k |

| Oct-17 | China Retail Sales | 7.8% | 7.8% | 7.5% |

| Oct-24 | Hong Kong Exports YoY | -7.0% | -- | -6.3% |

| Oct-24 | ECB Main Refinancing Rate | 0.000% | -- | 0.000% |

| Oct-24 | Durable Goods Orders | -0.5% | -- | 0.2% |

| Oct-24 | New Home Sales | 710k | -- | 713k |

Strengths

- The best performing metal this week was palladium, up 3.26 percent as its one-week lease rate reached the highest since January, indicating physical supplies are tight. Gold traders and analysts in the weekly Bloomberg survey were mostly neutral on the metal’s price outlook as the market awaits the upcoming Fed meeting. Gold did advance on Wednesday after an unexpected drop in U.S. retail sales. The metal also got a boost from increased trade war tensions. China threatened “strong countermeasures” if the U.S. enacts legislation supporting Hong Kong protesters.

- U.S. retail sales declined for the first time in seven months, suggesting that consumers are starting to become shaky, reports Bloomberg. The value of overall sales fell 0.3 percent last month, below estimates for a 0.3 percent advance. Slowing retail sales fueled economic worries, which can boost gold’s appeal as an asset class.

- The Dutch National Bank (DNB) released bullish statements on gold this week. “Gold is the perfect piggy bank – it’s the anchor of trust for the financial system. If the system collapses, the gold stock can serve as a basis to build it up again. Gold bolsters confidence in the stability of the central bank’s balance sheet and creates a sense of security,” said the DNB on its website. The Netherlands is the world’s tenth largest holder of gold with approximately 612.5 tonnes in its reserves.

Weaknesses

- The worst performing metal this week was platinum, down 0.66 percent as hedge fund managers cut net bullish positions to a seven-week low. Turkey’s gold reserves fell $181 million from the previous week, according to central bank data. The central bank’s holdings are now worth $25.8 billion, and are still up 44 percent year-over-year.

- China’s slowing growth is now spilling into gold jewelry demand. According to forecasts from Metals Focus, jewelry consumption is set to drop 4 percent in 2019. Investment demand is also forecast for a 20 percent decline. Higher metal prices are also hurting jewelers. Chow Tai Fook Jewellery fell as much as 4.6 percent after it announced it will record an unrealized loss of up to HK$1 billion.

- Jewelry demand has been muted in India too due to higher prices, but higher prices are good for investment demand, which had slowed in recent years. Investments in gold exchange-traded products (ETPs) in India has recovered this year, in part due to rising comfortability in making online purchases. Metals Focus said in its monthly note that recovery is expected to continue, but the size of fresh investment inflows may be limited by the attractiveness of equities. President Maduro of troubled, but gold-rich Venezuela said this week that he has decided “to approve a full functioning gold mine for each governor’s office.”

Opportunities

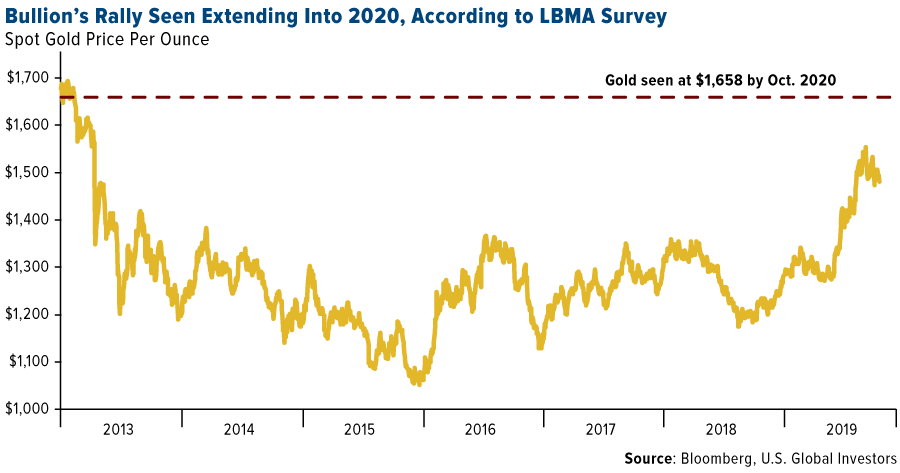

- According to delegates at the London Bullion Market Association (LBMA) annual conference, gold will rise to $1,658 an ounce by October 2020. Last years’ attendees “pretty much nailed” the metal’s rally in 2019, reports Bloomberg. The group also forecasts silver at $23 an ounce next year, rising 11 percent from today’s $17.60 level. Lastly, the attendees predict palladium will reach $1,924 an ounce by this time next year. Palladium is closing in on $1,800 an ounce as a supply deficit persists, according to Australia & New Zealand Banking Group.

- Suki Cooper, precious metals analyst at Standard Chartered Bank, says that the next push in gold prices will come from retail demand. In an interview with Bloomberg, Cooper said that “retail investors almost want confirmation of further rate cuts, some weakness in the equity markets before they move into good. The next leg higher in 2020 is going to be led by the retail side.” Speaking of more rate cuts, the Fed looks almost certain to cut rates for a third time later this month.

- Sprott CEO Peter Grosskopf is bargain hunting for stakes of mining firms that have taken a tumble, reports Bloomberg. Grosskopf said that if big producers don’t buy up their smaller rivals, then “the juniors will consolidate among themselves to create bigger companies.” Iamgold Corp is also bullish that more deals could emerge. “With so many companies chasing so few deposits, there’s certainly an opportunity for further consolidation in the industry,” says Iamgold chief financial officer Carol Banducci.

Threats

- Ray Dalio said that “big unique things are happening” in the global economy and that it’s “in a great sag.” The billionaire investor said impetus from measures such as rate cuts and tax cuts is fading and that a lot of long-term debt maturities are coming such as pensions and health care that are a burden. Dalio says one of the reasons for slower growth is a large wealth gap, which is a disparity that also leads to an education gap.

- In another credit warning, S&P Global Ratings says that the number of weakest links grew to 263 in September from 243 in August and are near a ten-year high. Weakest links are issuers rated B- or lower by S&P Global Ratings with negative outlooks. Twenty percent of the weakest credits are in the consumer products sector which has seen 52 downgrades this year versus only 5 credit upgrades.

- Bloomberg’s Lisa Lee reports that leveraged loan investors are “getting increasingly angsty, and their fear may be a harbinger of more pain coming in credit markets.” Leveraged loans are performing worse than junk bonds, which is surprising since they have been considered a lower-risk way to invest in junk-rated companies. Lee adds that “the loans have grown into a $1.2 trillion market” and that “safeguards and protections for investors have weakened.” While most economists rightly argue you can’t have a recession without a credit blow up, the green brown shoots are beginning to show their color.

Index Summary

- The major market indices finished mostly up this week. The Dow Jones Industrial Average lost 0.17 percent. The S&P 500 Stock Index rose 0.54 percent, while the Nasdaq Composite climbed 0.40 percent. The Russell 2000 small capitalization index gained 1.56 percent this week.

- The Hang Seng Composite gained 1.44 percent this week; while Taiwan was up 2.67 percent and the KOSPI rose 0.79 percent.

- The 10-year Treasury bond yield rose 2 basis points to 1.755 percent.

Domestic Equity Market

Strengths

- Health care was the best performing sector of the week, increasing by 2.03 percent versus an overall increase of 0.69 percent for the S&P 500.

- McKesson Corp. was the best performing stock for the week, increasing 13 percent.

- JPMorgan Chase & Co., which has risen in recent years to be the dominant Wall Street firm, widened its edge on rivals as the biggest banks navigated a tumultuous third quarter, writes Bloomberg News. JPMorgan reported its biggest increase in fixed-income trading revenue in nearly three years and a surprise jump in banking fees. In the process, the bank kept a more than $1 billion lead on its trading competitors and grabbed its biggest advantage over Goldman Sachs Group Inc. in more than a year in the high-stakes investment-banking battle, the article goes on the explain.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 1.71 percent versus an overall increase of 0.69 percent for the S&P 500.

- Cimarex Energy was the worst performing stock for the week, falling 8.80 percent.

- Uber laid off roughly 350 employees in its third round of major job cuts this year, according to TechCrunch.

Opportunities

- Roku Inc. shares rallied after announcing that the Apple TV app would be available on its platform. The agreement “validates Roku’s dominant role as an aggregator” of streaming-video content, wrote Amine Bensaid, an analyst at Bloomberg Intelligence. While it will take some time before the impact of the Apple deal shows up in its results, “the content-agnostic nature of its platform will allow more deals with streaming services.”

- BlackRock beat earnings expectations, reports Business Insider, as technology services drive growth in a “volatile” market. CEO Larry Fink said that clients have entrusted $350 million worth of new assets in the last year to the firm "technology services revenue."

- Google revealed its newest smartphone, the Pixel 4, and a fresh line of products that will rival Amazon and Apple. Google announced the Pixel 4, at its "Made by Google" event on Tuesday alongside several other hardware products, reports Business Insider.

Threats

- Morgan Stanley analysts say that Goldman Sachs could take a $264 million hit on its WeWork stake. Jefferies said in September that it wrote down $146 million related to its WeWork stake, citing uncertainty around timing and pricing of the co-working company's IPO.

- Booking Holdings is the next in line to withdraw from Facebook’s cryptocurrency project known as Libra. The social media giant’s deteriorating relationships with Libra partners, combined with intense scrutiny from lawmakers, leaves the future of the initiative uncertain, Business Insider writes.

- Shares in Wirecard sank more than 20 percent in early trading on Tuesday, writes U.S. News and World Report, after the Financial Times published documents on the company's accounting practices alleging an effort to inflate sales and profits, dealers said.

The Economy and Bond Market

Strengths

- Americans’ sentiment about the buying climate reached an all-time high last week, adding to signs that a strong labor market, income growth and tame inflation will help keep consumers spending and support an economy slowed by trade disputes and manufacturing weakness. Better views of whether it’s a good time to buy lifted the overall Bloomberg Consumer Comfort Index to 63.5 the week ended Oct. 13 from 62.7, data released Thursday showed. The confidence measure stands 1.2 points from an 18-year high reached in late July.

- The number of unemployed workers who applied for jobless benefits in the second week of October rose slightly, but layoffs nationwide remained near a 50-year low and showed no sign of rising. Initial jobless claims, a rough way to measure layoffs, increased by 4,000 to 214,000 in the week of Oct. 6 to Oct. 12, the government said Thursday. Economists polled by MarketWatch had forecast a 215,000 reading.

- U.S. homebuilder confidence in the single-family market jumped three points in October to 71 on the National Association of Home Builders/Wells Fargo Housing Market Index, or HMI. That is the highest level since February 2018 and up from 68 in October of last year. Anything above 50 is considered positive sentiment. “The housing rebound that began in the spring continues, supported by low mortgage rates, solid job growth and a reduction in new home inventory,” said NAHB Chairman Greg Ugalde.

Weaknesses

- U.S. retail sales fell for the first time in seven months in September, raising fears that a slowdown in the American manufacturing sector could be starting to bleed into the consumer side of the economy. The Commerce Department said Wednesday that retail sales dropped 0.3 percent last month as households slashed spending on building materials, online purchases and especially automobiles. The decline was the first since February. Economists polled by Reuters had forecast retail sales would climb 0.3 percent in September.

- A gauge of inflation expectations from the Federal Reserve Bank of New York fell in September to the lowest level in data going back to 2013, the latest sign of weakness that could raise concerns among central bankers already fretting over muted price pressures. The measure of inflation expectations three years from now slipped to 2.4 percent last month from 2.5 percent in August, according to the New York Fed’s monthly survey of consumer expectations published Tuesday. The decline reinforces the message from preliminary results of a monthly University of Michigan survey of consumers published Oct. 11, which suggested expected inflation 5-to-10 years ahead fell to 2.2 percent this month, the lowest level in data going back to 1979.

- Production at U.S. factories fell in September by the most in five months, depressed by an autoworkers’ strike at General Motors Co., sluggish global demand and the trade war. Production at manufacturers declined 0.5 percent last month, weaker than the median forecast in a Bloomberg survey of economists, Federal Reserve data showed Thursday.

Opportunities

- China says it hopes to reach a phased trade pact with the U.S. as early as possible. A phased agreement would help restore market confidence and reduce uncertainty, Gao Feng, spokesman at the ministry, told reporters, adding that both sides were maintaining close communication.

- Illinois Governor J.B. Pritzker said Thursday that he plans to propose legislation before year-end that would consolidate the assets of 649 suburban and downstate pensions into two state funds to seek better returns and savings for the underfunded retirement systems. These funds are under-performing by $1 million a day, according to estimates from Pritzker, who announced the recommendations of a task force that he launched in February to study such a merger.

- Housing figures and durable goods orders will be the main focus next week as investors take pulse of the U.S. economy.

Threats

- The International Monetary Fund (IMF) made a fifth-straight cut to its 2019 global growth forecast, citing a broad deceleration across the world’s largest economies as trade tensions undermine the expansion. The world economy will grow 3 percent this year, down from 3.2 percent seen in July, with the 2020 estimate lowered to 3.4 percent from 3.5 percent, the fund said Tuesday in its latest World Economic Outlook. The forecast for this year would be the weakest since 2009, when the world economy shrank, as the fund chopped projections from the U.S. and Europe to China and India.

- China's economy grew at its slowest rate since the 1990s. China's economy grew at 6 percent between July and September, a rate not seen since 1992.

- China threatened retaliation after the U.S. House of Representatives passed a bill supporting Hong Kong protesters. House lawmakers passed a bill this week which would mean that the U.S. reviews how autonomous Hong Kong is each year, determining its trade policy.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was natural gas, which gained 6.19 percent on expectations that colder weather will grip the Northeastern region. Reversing declines early in the week, crude oil gained on Thursday after a U.S. government report showed large declines in fuel inventories, outweighing negative sentiment around a larger-than-expected increase in stockpiles. The Energy Information Administration said gasoline and distillate supplies shrank by 6.4 million barrels after nearly 17 percent of domestic refining capacity shut down last week. However, concerns remain about demand falling next year.

- Codelco, the world’s largest copper miner, admits that the trade war is hurting prices and demand, and is offering customers better terms to combat it. CEO Roberto Ecclefield said that the company will adjust the terms of contracts to make them more attractive. Bloomberg reports that copper prices have fallen 12 percent in the last 12 months and that Chinese demand for the metal will increase 1.5 percent this year, below forecasts of 2.5 percent. Codelco hopes to sign more three-year contracts in the fourth quarter.

- According to people familiar with the matter and as reported by Bloomberg, advisors working on Saudi Aramco’s massive IPO might spilt a fee pool of as much as $450 million, which would make it one of the biggest IPO payouts globally. More than 20 banks are working on making the oil giant go public and many firms have been working for years investing in Saudi Arabia. On Friday Aramco announced a second delay in its IPO as doubts emerged over its $2 trillion valuation place on the state oil giant by Crown Prince Mohammed bin Salman.

Weaknesses

- The worst performing major commodity for the week was nickel, which fell 7.70 percent. Nickel and iron both had difficult weeks. Iron ore futures fell in Singapore more than 5 percent on Wednesday as supplies rebound and questions build about demand outlooks out of China. Nickel saw its worst week since 2017, also on concerns of falling demand.

- The London Metal Exchange (LME) announced that it will raise fees for the first time in five years by 8 percent in 2020 due to significant investments in infrastructure, compliance functions and market initiatives. The LME is also boosting collateral charges for gold and bonds, and increasing fees for membership subscriptions and market data.

- Tanker rates for shipping oil continue to hit record highs. Last Friday it cost a record $8 per barrel to ship West African crude to Asia, according to Bloomberg, which is four times the average. Rates on the Persian Gulf to China route are almost six times the average, drastically hurting the margins of oil refiners. Higher rates are due to U.S. sanctions on Chinese shipping companies, causing a shortage of ships.

Opportunities

- Russian nuclear producer Rosatom Corp. is in talks with Argentina about building floating power plants and small-capacity facilities. The company is also in talks with Brazil to complete a third reactor at an existing plant, according to Brazilian news source Ria Novosti. The company has been aggressively marketing its floating nuclear technology as a low-carbon energy source for remote locations.

- The U.K. government announced this week plans to allocate up to 1 billion pounds to develop an electric vehicle supply chain, reports Bloomberg. Volvo is also taking big steps to encourage electric vehicle use. The Swedish carmaker said buyers of its 2021 model year hybrids will be able to claim a refund for their electricity costs during the first year of ownership. Volvo will begin producing its first electric vehicle in late 2020.

- Aluminum is winning the race to produce more eco-friendly products such as disposable bottles and cups, as the metal is more eco-friendly than petrochemical. The Aluminum Association estimates that almost 50 percent of cans made from aluminum are recycled, compared with just 29 percent for plastics. Ball Corp is one of the big beneficiaries, with its stock up over 60 percent in the last 12 months, as it rolls out aluminum cups aimed at replacing the classic red solo plastic cups.

Threats

- On Tuesday the U.S. House passed a bill on a voice vote supporting the Hong Kong protestors – potentially worsening already tense U.S.-China relations. China’s Ministry of Foreign Affairs issued a statement in response threatening retaliation if the bill moves forward and President Trump signs it. Last week news broke of a “phase one” trade deal between the countries, but it was soon corrected that more talks are still necessary before any deal is signed. A continued trade war is negative for commodities.

- In continued negative news for the diamond industry, Alrosa reported that third quarter output grew 24 percent while sales fell 23 percent, according to Bloomberg. The producer also said that diamond stockpiles rose 36 percent. Sales could potentially pick back up in the fourth quarter as the holiday shopping season begins. Alrosa has another longer term problem to consider, along with the rest of Russian infrastructure build on permafrost; it melting! Russia’s permafrost area also accounts for 15 percent of its oil and 80 percent of its natural gas operations. Norilsk Nickel’s operation, a major producer of palladium, is also on permafrost and has already seen housing in its area face demolition. Once the soil unfreezes it deforms under the weight of structures not properly anchored to the bedrock.

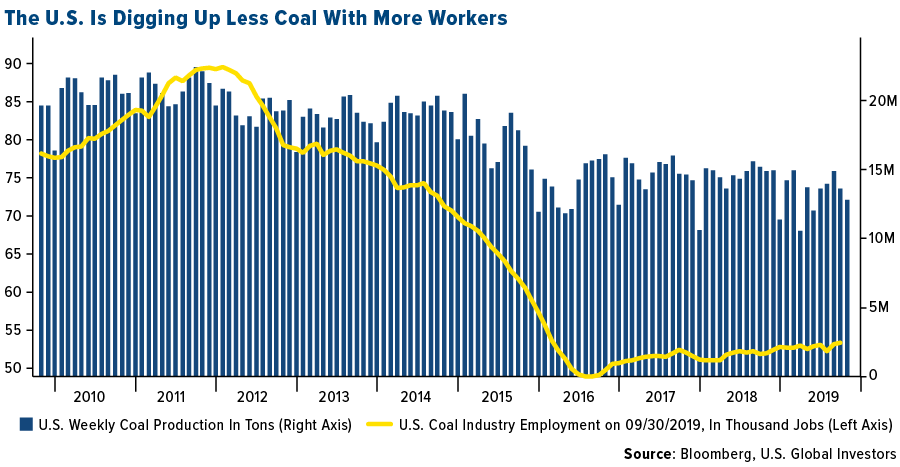

- Bloomberg reports that the amount of coal being produced per U.S. miner is at the lowest level in eight years. Coal productivity has fallen 11 percent so far this year and is expected to fall 10 percent overall for the year. Phil Smith, a spokesman for the United Mine Workers of America Union, says “it’s highly likely there will be more layoffs.” Three domestic producers have already announced plans to close facilities in the past month, including Peabody Energy Corp, Blackhawk Mining LLC and Murray Energy Corp.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 2.9 percent. Banks performed well over the past five days, with Moneta Bank gaining 4.6 percent and Komerci Bank up 5 percent. JPMorgan added Moneta Bank to its Most Preferred stocks in Central Emerging Europe list.

- The Czech koruna was the best performing currency this week, gaining 1.9 percent against the U.S. dollar. The koruna reacted most positively to Thursday’s Brexit agreement between the U.K. and the European Union.

- Health care was the best performing sector among eastern European markets this week. Richter, a Hungarian pharmaceutical company, was the best preforming equity, gaining 8 percent over the past five days.

Weaknesses

- Turkey was the worst performing country this week, losing 60 basis points. Turkey’s attack on Northern Syria sent stocks lower early in the week, and on Friday equites trading on the Istanbul exchange bounced after Thursday’s temporary ceasefire agreement.

- The Russian ruble was the worst relative performing currency in the region this week, gaining just 60 basis points. The central bank may cut its main rate by 50 basis points. The next monetary policy meeting is scheduled for October 25.

- Industrials was the worst performing sector among eastern European markets this week. Tekfen, a Turkish construction company, was the worst preforming equity, losing 6 percent over the past five days.

Opportunities

- The Greek budgetary plan for 2020 was released this week pointing to a primary budget surplus of 3.7 percent for this year and 3.6 percent for 2020. The European Union seems to agree with the figures, but a final decision will be made in November. The expected GDP growth for this year is 2 percent and 2.8 percent for next year.

- According to analysts at BCS Global Markets and Investec, investors are relocating assets from Turkey into Russia, as domestic and international tensions in Turkey are on the rise. Russia stands best-positioned to attract fund reallocations, Investec’s Julian Rimmer said in the e-mail. The VanEck Vector Russia ETF, the main exchange traded fund tracking Russian stocks, posted one-day inflows of $32.2 million on October 16, the most since November.

- Another Russian company announced a dividend increase. Lukoil, an oil and gas producer and distributor, will distribute 100 percent of its free cash flow in dividends, with the buyback program remaining in place. Wood & Company estimates that Lukoil will generate $9 billion in free cash flow, implying a potential three-fold increase in the dividends and a dividend yield of 15 percent.

Threats

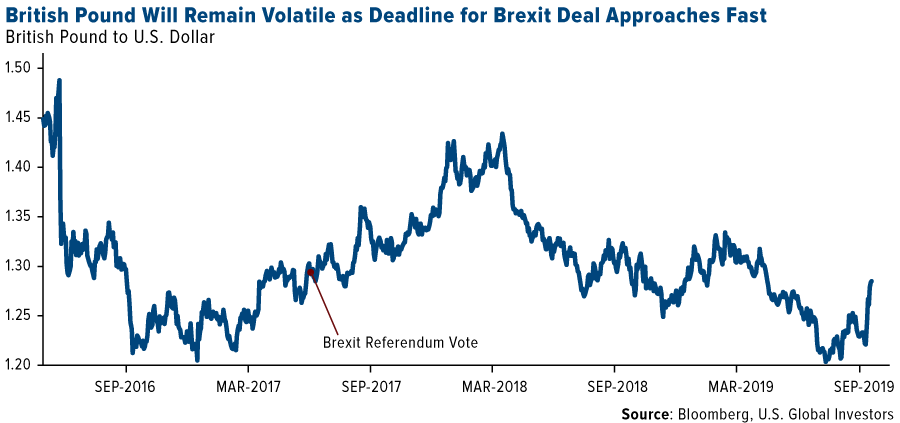

- The British pound had been volatile since June 23, 2016, when Britain has decided to depart from the euro area. The current Brexit deadline is set for October 31, and as negotiations entered the final stage, the currency will follow negative/positive news. In recent days, the pound gained as a deal has been reached between the U.K. and EU. However, it needs to pass through the U.K.’s parliament. The vote is scheduled for this Saturday.

- Geopolitical tension may increase in Turkey as the country’s incursion into Northern Syria faces global criticism. The U.S. imposed sanctions on Turkey, but more severe, financial sanctions might be introduced later. U.S. Republican Senator Lindsey Graham proposed a prohibition on anyone in the U.S. from buying Turkey’s debt. The proposed bill needs to pass the House and the Senate before going to President Trump to be signed into law. On Thursday, the U.S. and Turkey reached an agreement to suspend operations in northern Syria for 120 hours to allow Kurdish forces to withdraw from the safe zone.

- The International Monetary Fund (IMF) said that the U.S.-China trade war will cut 2019 global growth to its lowest pace since the 2008-09 financial crises. The Global GDP growth was revised down from 3.2 percent in July to 3.0 percent. For "Emerging and Developing Europe" (Croatia, Russia, Turkey, Poland, Romania, Ukraine, Hungary, Belarus, Bulgaria and Serbia) the IMF predicts a growth of 1.8 percent in 2019 and 2.5 percent in 2020. The main reason for emerging Europe to grow slower than the global economy is Turkey’s economic stagnation this year, offset by stronger GDP data for Hungary, which is expected to grow at 4.6 percent, followed by Poland and Romania at 4 percent.

China Region

Strengths

- The best performing indices in the region were India’s Nifty and Sensex indices, which jumped 3.26 and 3.09 percent, respectively. Taiwan, which reopened from holidays late last week, climbed 2.67.

- Conglomerates constituted the best performing sector in the Hang Seng Composite Index for the week, rising 2.12 percent.

- While China’s GDP did miss expectations, note that retail sales for the September period did hold steady a 7.8 percent year-over-year, and industrial production actually beat expectations with a 5.8 percent pace of growth, much better than a consensus 4.9 percent.

Weaknesses

- The poorest performing index in the region was the Shanghai Composite, which declined by 1.19 percent. Vietnam joined China in the red for the week; the rest of the region rose.

- Materials and energy were the laggard HSCI sectors this week, falling 1.59 percent.

- China’s third-quarter GDP print clocked in at 6.0 percent even, shy of analyst consensus for a 6.1 percent print, and marking the slowest pace of year-over-year quarterly growth since at least 1992. Imports and exports also missed.

Opportunities

- While last week’s late announcement of the U.S.-China trade talks reaching a “Phase One” stage of deal talks was positive—and while details and a precise timeline still remain a bit murky—there remains a possibility of the two sides advancing talks further, signing an agreed-upon text of some kind at some point in the future (perhaps when Presidents Trump and Xi are both in Chile), and then moving onto thornier issues subsequently and in time (Phases Two and beyond…?). Nothing is yet set in stone, so to speak, and while hiccups may yet remain, hey, in the meantime, the U.S. did not hike tariffs this week, China is reportedly starting up more agriculture purchases, and the markets seem reasonably pleased with the current trajectory for the moment. Larger resolution or any breakthrough remains a potential catalyst.

- Paytm, the current leader in Indian digital payments share, is reportedly close to securing a $2 billion fundraising round at a valuation of some $16 billion from investors including Jack Ma’s Ant Financial and SoftBank, according to Bloomberg News. The article estimates the Indian payments market could potentially reach $1 trillion.

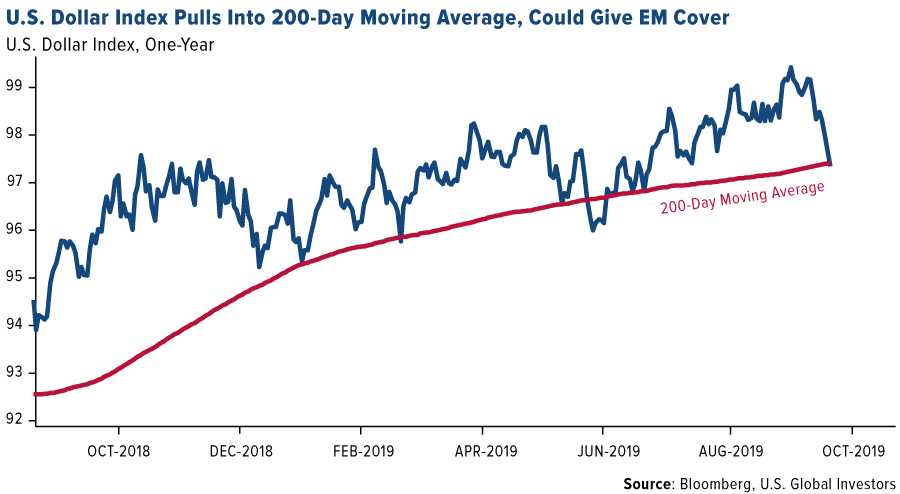

- The U.S. dollar weakened further this week, which may continue to let off pressure on emerging markets.

Threats

- In keeping with this section’s views, we once again reiterate that trade war escalation must remain a threat until it isn’t. Even over the weekend following “Phase One” announcements, President Trump took to Twitter to explain his view of how agricultural purchases should look and how soon they should take place, while President Xi argued the details of the agreement and wording would all take time as well.

- Unrest continues in Hong Kong heading into a twentieth weekend where authorities have already placed at least one major ban on activities originally scheduled for the weekend. (On the bright side, while some data clearly demonstrate deterioration like retail sales, visitor arrivals, etc., unemployment in the Hong Kong SAR remained steady at around 2.9 percent.)

- The United States Congress appears set to move ahead quickly on legislation that will support protestors in Hong Kong despite threats from China. The House voted already on four bills, prompting China’s foreign ministry, according to Bloomberg reports, to issue a warning of “unspecified countermeasures” should they continue to wind its way toward a Senate vote and, perhaps, the president’s desk. Note, however, that the house legislation as it stands stopped short of altering the Hong Kong Policy Act of 1992, which grants the city’s special trading status.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 18 Emirex Token, up 337.57 percent.

- Bank of America has quietly tested out Ripple’s distributed ledger technology, writes CoinDesk, and may be planning to do more with it. Although a Ripple spokesperson would neither confirm nor deny whether the bank was a customer, she did tell CoinDesk, “Bank of America has been part of Ripple’s Global Payment Steering Group since 2016 and we did a pilot with them.” Another signal that the bank could be warming up to the sector? A job posting on its website earlier this month for a product manager who would lead the team for a “Ripple project.”

- Ernst & Young (EY) is using blockchain technology to assist governments in improving transparency and accountability in the management of public funds, writes CoinDesk. EY announced the news on Wednesday, explaining that its new “blockchain-enabled” EY OpsChain Public Finance Manager “will compare government spending programs with the results of the expenditure, even when the money has passed through different layers of government and public service agencies.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 18 was Data Transaction Token, down 85.10 percent.

- The Commodity Futures Trading Commission (CFTC) is charging Nevada-based Circle Society and its operator David Gilbert Saffron with fraudulently soliciting and misappropriating investor funds, as well as registration violations, reports CoinDesk. Saffron offered binary options on forex and cryptocurrency pairs through his firm, and is alleged to have fleeced investors for $11 million in dollars and bitcoin since 2017.

- A U.S. federal grand jury has indicted a South Korean citizen for operating the largest child pornography site by volume, reports CoinDesk, where visitors spent millions of dollars’ worth of bitcoin to pay for the illegal content. According to the Department of Justice, 337 site users from 22 U.S. states and 11 countries around the world were arrested.

Opportunities

- Layer1 co-founder and CEO Alexander Liegl is planning to bring renewable bitcoin mining to the U.S., reports CoinDesk, specifically with the use of wind-powered rigs in West Texas early next year. According to Liegl, the idea of bitcoin crowding out other uses for clean energy reflects a misunderstanding of the market. “We think electricity directed to the bitcoin mining network is certainly a net positive for society,” he commented.

- On Wednesday, the Government of Bermuda announced it will accept payments in USD Coin (USDC) “for taxes, fees and other government services,” reports CoinDesk. In what appears to be a first for a sovereign nation, Bermuda will be supporting USDC as acceptable tax payment for some 60,000 residents.

- Although the SEC denied the latest application for a bitcoin ETF last week, a new product is about to be available in brokerage accounts, reports MarketWatch, giving traditional investors even broader access to the crypto market. The Financial Industry Regulatory Authority gave the crypto asset manager Grayscale the go-ahead to allow shares of an ETF-like product with multiple cryptocurrencies to start trading on public markets, the article explains.

Threats

- Gabriel Soderberg of Sweden’s Riksbank says that cross-border payments are where policy makers need to play catchup, writes CoinDesk. Facebook’s Libra has been that wakeup call for central bankers. “Libra showed there is demand for something that central banks have not yet delivered, which is cheap, efficient cross-border payments,” Soderberg told CoinDesk.

- The executive director of news for Bloomberg Digital, Joe Weisenthal, says that blockchains are essentially inefficient and that “bitcoin is for making transactions The Man is against,” reports CoinTelegraph. In a Bloomberg Markets newsletter, Weisenthal went on to explain that transactions would not be possible without individuals willing to pay fiat money for bitcoin, with blockchains being “inherently inefficient, computationally costly systems.”

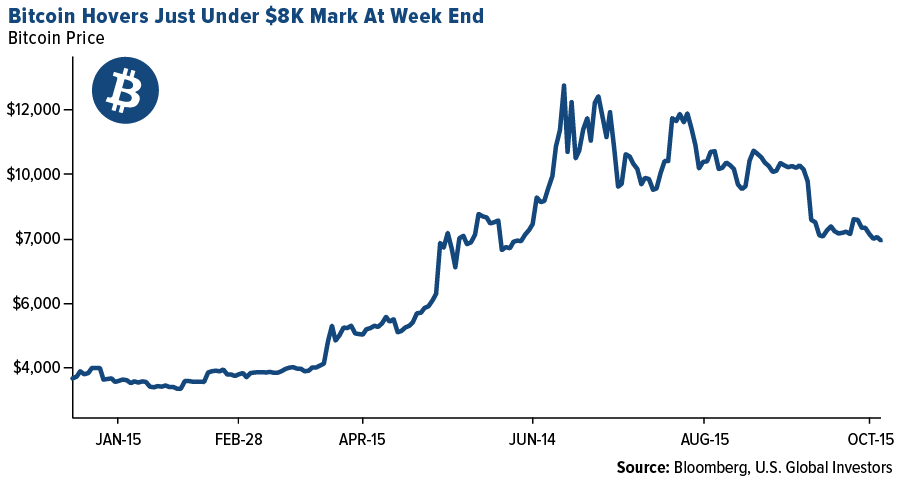

- A popular contrary indicator is “teasing a bearish turn for the first time since March 2018,” writes CoinDesk, meaning bitcoin may be close to bottoming out. Over the next week or so, the 50-day moving average could drop below the 200-day moving average, potentially producing a so-called death cross.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits