Weighing the Week Ahead: Earnings Season Opportunity?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is a modest one featuring home sales and Michigan sentiment. With the Q3 earnings reporting season in full swing, that news rates to be more important than the economic reports. Despite the likely drumbeat of political news, investors should be asking:

Does earnings season represent a special opportunity?

Last Week Recap

In my last installment of WTWA, I focused on the US/China trade announcement. I identified it as a defining moment for financial markets, but one that would not be immediately recognized. I was correct about the second part! The skeptics were out in force on Monday, and additional stories dribbled out during the week. Only David Templeton (HORAN) considered the improved backdrop from the trade deal. My friend Paul Schatz led the skeptics.

Since I expect the process of recognition to take time, this is exactly what I predicted last week. Today’s installment continues our effort to take advantage of our strong contrarian position.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring the Investing.com version.

The market gained 0.5% for the week with a narrow trading range of 1.5%. The DJIA looks more dramatic, but more than 80% of the decline represented specific events at Boeing and Johnson and Johnson. The low was on Monday coinciding with the expected round of skepticism on the US/China trade announcement. You can monitor volatility, implied volatility, and historical comparisons in my weekly Indicator Snapshot in the Quant Corner.

Noteworthy

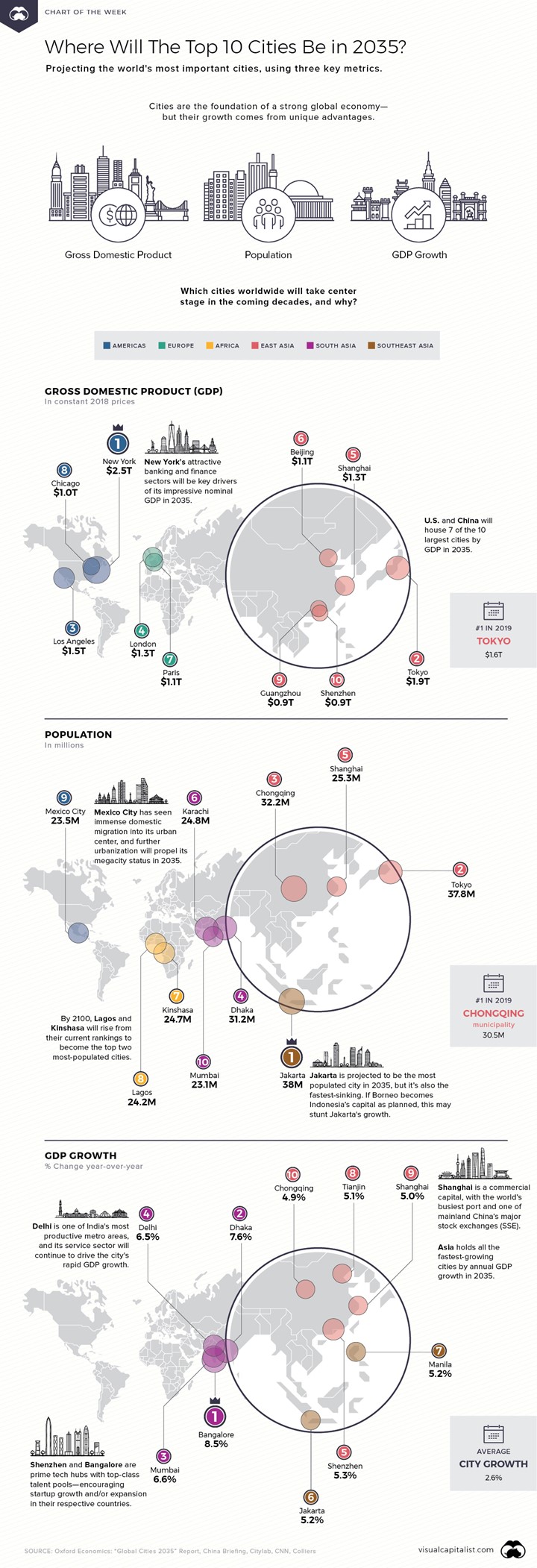

The Visual Capitalist analyzes the top 10 cities in 2035 based upon population, GDP, and GDP increase. This is a great way to get a sense of key trends and not so far in the future.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. The results remain positive in all three of the time frames. The short-term indicators are volatile and the weakest, mostly reflecting the emphasis on manufacturing. NDD sees a lower risk of recession despite economic weakness, especially in manufacturing.

The Good

- The NAHB Housing Market Index improved to 71 in October from September’s 68. (Calculated Risk).

- Building permits for September were 1387K (SAAR). While lower than August’s 1425K, the gain beat expectations of 1350K.

- Mortgage applications increased 0.5%. This was lower than the prior week’s 5.4% gain but remains strong.

The Bad

-

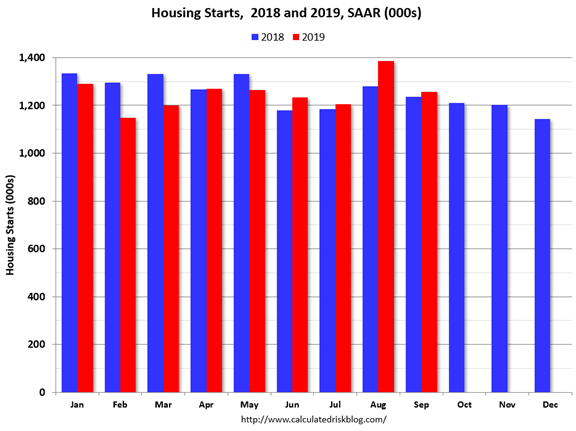

Housing starts for September were only 1256K (SAAR) versus expectations of 1306K and August’s (upwardly revised) 1386K. Calculated Risk puts the report in context, calling it a “decent” report. Bill now expects starts for 2019 to exceed those in 2018.

-

Industrial production for September declined 0.4%, slightly more than the expected 0.3% and much worse than August’s 0.8% gain (revised up from 0.6%).

-

LA area Port Traffic is lower. Calculated Risk mentions the Panama Canal expansion, a topic I and readers have occasionally raised. The expansion was completed in 2016, so we might expect the data to retain some value for our purposes.

-

Leading indicators for September declined 0.1% versus expectations of unchanged. August was revised from unchanged to a loss of 0.2%.

-

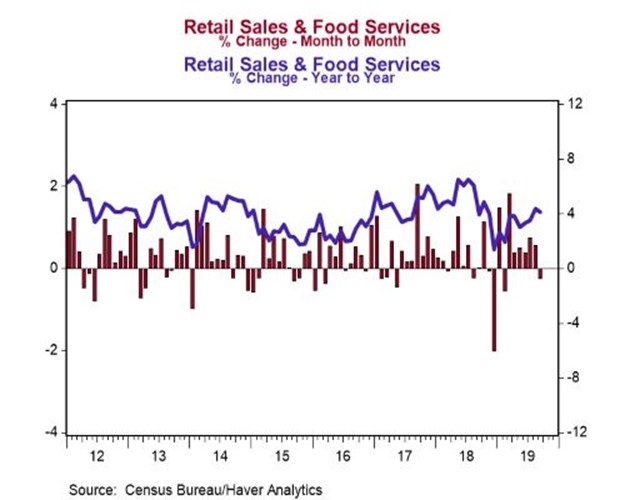

Retail sales for September disappointed with a surprising decline of 0.3%. Expectations were for a gain of 0.3%. August was revised up from a gain of 0.4% to 0.6%. Brian Wesbury notes the 4.1% year-over-year increase, opining that another rate cut is not necessary.

The Ugly

Continued political polarization.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

The economic calendar is a modest one featuring home sales data and Michigan sentiment. It is a big week for corporate earnings reports, which will be 40% complete by the end of this week.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The week ahead is light on economic data, but heavy on earnings reports. The cacophony of political news has hijacked much of the financial programming. This seems to generate higher ratings than the focus on corporate reports, unless they generate big moves in popular stocks.

The pundits may be distracted by Washington, but serious investors should have a different focus, asking:

Where are the opportunities revealed by earnings reports?

Background

I will begin with some basic information about earnings season – concepts that we might always use. From that, I will turn to what is special. In today’s Final Thought I will try to be a bit more specific about how I am sniffing out opportunities.

Anecdotal Evidence is Often Misleading

The biggest stories during earnings season are the gigantic moves, especially when a well-known company is involved. Traders typically look for similar companies or those affected by the same key factors. This gives the illusion of supporting evidence, when it is actually a mere echo of the original story.

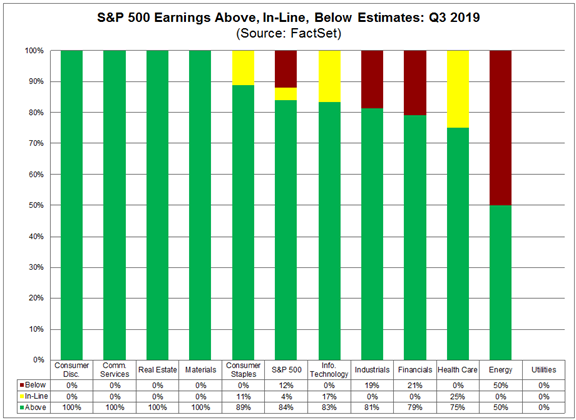

The most important earnings story is the aggregate interpretation of the many reports. I cover this weekly, but it is difficult to find on TV. Here is an example from this earnings season, drawing upon one of our go-to sources, FactSet.

Forward Earnings Tell the Real Story

Few people buy stocks because of valuations based upon earnings reports from past years. I never hear a CAPE ratio story about an individual stock. Investors and traders alike are forward-looking. They want to know what will happen next. Stocks often report a “beat” on the top and bottom lines and still decline because of earnings guidance. In other cases, a poor report is overlooked because of future prospects.

Despite these facts, a portion of the punditry emphasizes past earnings. In the typical case of a company that is improving performance, the trailing earnings reflect a higher P/E multiple. This is eagerly embraced by those on my Twitter list of reliably bearish commentators.

Earnings guru Brian Gilmartin consistently updates the twelve-month forward earnings and the related ratios. This approach is far superior to the commonplace summary based upon calendar year earnings.

Growth Stocks Face a Double Danger

A growth stock often carries a high multiple. If earnings growth is at 30%, then a P/E multiple of 40 or 50 (or even higher) is not unusual. If the earnings growth continues apace, all is well. But what if there is an earnings miss?

An earnings report that does not maintain the growth rate has a dual effect:

- The earnings base for the ratio is lowered.

- The multiple is reduced to match the new growth rate.

Because of this risk, growth stocks face special scrutiny.

The Paradox of Expectations

There are two widely held conclusions about corporate earnings:

- Analysts are overly optimistic, so expected earnings are always too high.

- At the time of corporate reports, the high “beat rate” is because expectations are too low.

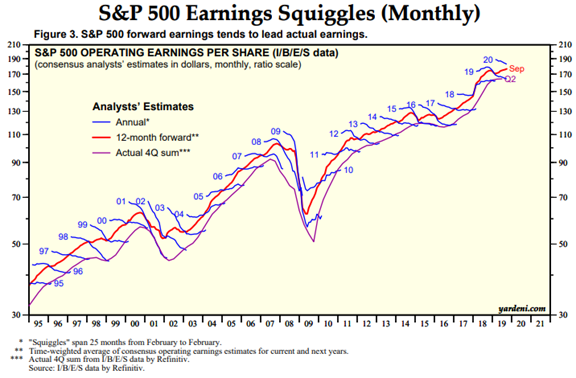

The apparent contraction is universally ignored as the punditry shamelessly cites whatever conclusion fits the occasion. The claim is often supported by a “squiggle chart” showing the change over time. Here is an example from Dr. Ed Yardeni.

The chart shows that forward earnings estimates are pretty reliable in leading actual results. If you look at an individual squiggle, you can see the 25-month history of the consensus estimate for that quarter. These often, but not always, start out too high. After the report, the estimate is (of course) on target. For estimates to be too optimistic at the start and too pessimistic at the end, there must be a crossover point – a time when the estimate is accurate. My research shows this to be about nine months before the actual report. You can decide yourself by finding the 16-month point on each squiggle.

The Importance of Outlook

Most companies discuss their outlook in a conference call after the report. These calls combine company-specific information with macro events. This often includes specific factors for the current quarter, along with commentary on whether this impact will continue. Typical factors might include currency effects, the trade war, the overall economy, and regulatory effects.

It is a challenge to disentangle the two type of effects. To summarize the problem, a company with global exposure may provide an accurate account of how these factors affected the current quarter. When it comes to predicting economic trends, however, their information is no better than anyone else’s. Despite this, markets tend to credit executives with special knowledge on these factors.

I’ll have some additional observations in today’s Final Thought.

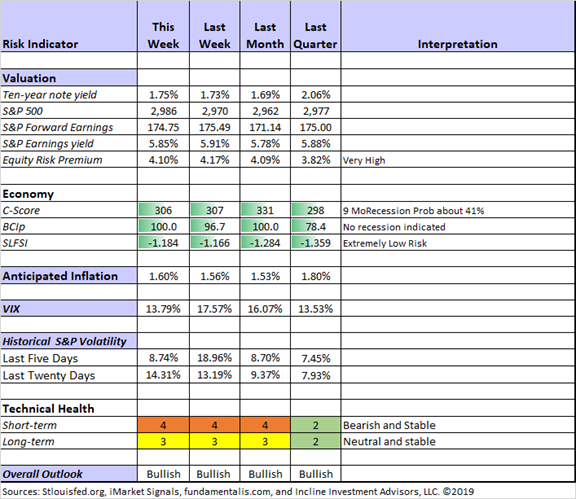

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term technicals stabilized a bit, but remain in bearish territory. Long-term technicals remain neutral. Recession risk is still in the “watchful” area. We are seeing little confirmation for the risk signals, which we have been monitoring since May.

Considering all factors, my overall outlook for investors remains bullish.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Guest Sources

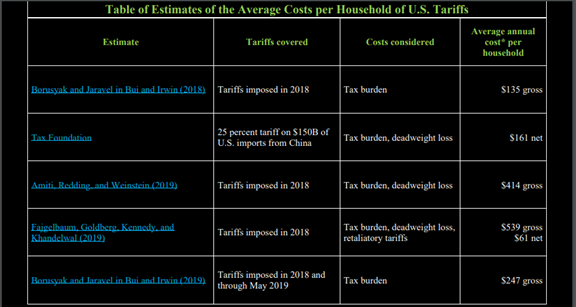

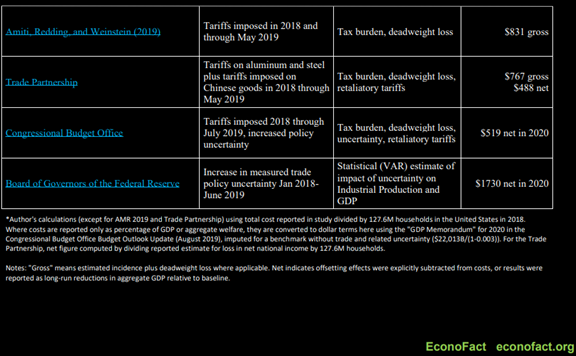

EconoFact has an excellent summary of various sources and their estimates of the household impact of tariffs. Read the full article for detailed explanations.

Prof. Steve Hanke has an excellent and accessible explanation of why a negative external trade balance is not a “problem.” Here is a key quote about what I have called a real-time economics lesson:

The level of economic illiteracy that surrounds the strange world of international trade policy is stunning. Now we have irrefutable arguments and evidence to explain why a country’s external balance is determined domestically, not by foreigners. As the history of trade policy shows, it’s difficult to change false beliefs with facts. But, now we have even more damning evidence to refute the false beliefs than ever before.

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I try to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades described are certainly not suitable for everyone. Last week we had a company conclave at mission control in Incline, Nevada. The views are beautiful, but the air is thin.

The models will resume their appearance soon with some new participation among the characters and the editorial team.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Ashby Daniels’ When Its Smart to Pay Capital Gains Taxes. (HT Abnormal Returns Personal Finance). His basic argument is a reply to those who are worried about paying “too much in taxes” so they want to wait and see.

There are only three possible outcomes that can accompany this “wait and see” approach:

The stock price doesn’t move so they are no better or worse off theoretically (ignoring opportunity cost).

The stock price rises and exacerbates the capital gains issue they are seeking to avoid.

The stock price falls reducing the gain and the taxes that go along with it.

What exactly is the investor hoping will happen? Wasn’t the whole point of investing to make money? If they’re at the doorstep of achieving their retirement goals, why keep playing the game?! Are they hoping the stock falls in value so they could pay 15-24 cents less for each dollar they lost? Crazy, no?

He also notes some exceptions, but the principal analysis addresses a common investor error.

Stock Ideas

Chuck Carnevale has an excellent two-part series on the importance of forecasting future business results as part of your stock selection. His thorough analysis includes several points I am emphasizing for the current earnings season. In Part 1 he writes,

Furthermore, I want to restate and acknowledge that I believe that investors cannot escape the obligation to forecast – our results depend upon it. However, we should not just guess nor should we merely play hunches. Forecasting should be approached as analytically and even as scientifically as possible.

Part 2 considers various forecasting approaches. Taken together, these articles help us become better consumers of this information.

ConocoPhillips Stock Looks Cheap After a Selloff. Andrew Bary describes how the company is generating free cash flow and returning it to shareholders.

Andrew Hecht sees support for gold, largely based upon international concerns.

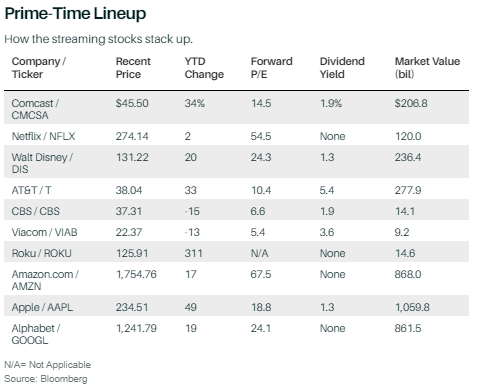

The Streaming TV Revolution Will Have Winners and Losers. How to Play the Stocks.

Jack Hough explains the opportunities and risks for the leading candidates.

Bernstein Research has some new picks developed by combining fundamental and quantitative analysis. It is an interesting collection.

Personal Finance

Abnormal Returns is the go-to source for anyone serious about the investment business. The Wednesday edition has a special focus on personal finance, with plenty of ideas for the individual investor. As always there are many good links. I especially liked Sarah Newcomb’s A Simple Plan for Financial Independence. She cleverly examines personal finance using economics as the prism.

Watch out for…

Changes to Medigap Plan F, the “first-dollar coverage” plan. This is important for retirees who may face restrictions on changing plans in the near future. (Barron’s)

China risk for Apple (AAPL). (Stone Fox Capital).

Final Thought

Earnings season typically centers on finding stocks where you expect superior performance. This season provides some special opportunities, centered on the “defining moment” I discussed last week. The ideal investment would include the following:

- Sound business model and balance sheet;

- A “poor report” based upon trade, currency, or global economic weakness;

- A bargain price, judged by a normalized PE multiple.

I am still using the various indicators and screens I mentioned last week to identify attractive sectors – a work in progress. This week’s Barron’s includes a top analyst who has reached conclusions similar to my own, Buy Home Builder and Tech Stocks, a Top Strategist Says. I always enjoy reading the viewpoints of buy-side analysts like Denise Chisholm, “a specialist in seeing patterns that others miss.” Here are a couple of key quotes:

The first is that, given the drop in Treasury yields, real interest rates in the U.S. are now negative. They’ve been negative a couple of times in this cycle, and it happened a few times in the 1970s and the 1980s. That is predictive of an overall equity market advance and a cyclical rotation away from defensive sectors.

And later..

With the PMI being below 50, 60% of the time it’s actually not a recessionary indicator. It can provide an opportunity to extend your time horizon over the next year to capture double-digit returns. It has also been predictive, even at these levels, of high odds of a cyclical rotation, where economically sensitive sectors, like consumer discretionary, technology, industrials, and financials, outperform those defensive groups that we’ve seen sort of outperform, year to date, like utilities, consumer staples, and, to a lesser extent, health care, which hasn’t kept up this time. Defensive is expensive. Risk is cheap.

This confluence of rare signals, of low-quartile manufacturing indexes, coupled with global central-bank easing, has led to 16% to 24% average returns over the next 12 months, versus the average of 8%. Historically, at least, it has been a time to extend your time horizon to take advantage of double or potentially triple the market’s average historical return.

And finally…

Consumer staples, utilities, and health care are the most expensive they’ve been since 1970, in the top percentile. That data point has been not just informative, but also predictive in history. It’s a rare signal that has only really occurred five times. You see a 1,000-basis-point rotation back to the economically sensitive sectors and an average underperformance of the defensive sectors.

Some other items on my radar

I’m more worried about:

- Escalation in Hong Kong. The temptation for US involvement is growing.

- Brexit – delayed again with provisions uncertain. (MarketWatch)

- Government debt. What Every American Should Know About the Debt & Deficit

I’m less worried about

- Recession risk. Coincident indicators remain near the base case, slower growth levels. That is not great, but it is good enough for now.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits