KEY HIGHLIGHTS

• Volatility has been the story of 2019. The markets have dealt with uncertainty around global trade restrictions, recession fears and the possibility of impeachment of President Donald Trump.

• We project these headwinds will cause global economic growth to remain relatively weak for the remainder of the year.

• We believe the likelihood of a near-term recession is unlikely and tentative signs of economic stabilization could develop in the next few months.

U.S. CONTINUES TO POWER THE GLOBAL ECONOMY

Despite a tepid 2.3% gross domestic product (GDP) growth rate through the first half of the year, the U.S. economy continues to be the engine that drives the global economy. However, we continue to have concerns about the negative impacts from the current status of global trade.

We were disappointed by the Trump administration’s decision to enact a 15% tariff effective Sept. 1 on certain consumer goods. These latest tariffs could hamper consumer spending, which consistently is the key driver of the U.S. economy. In addition, the U.S. plans to raise tariffs on the original $250 billion in Chinese goods by 5 percentage points to 30% in December and apply a 15% tariff on the remaining consumer goods that had been left alone. We are hopeful the weaker trajectory in economic growth, coupled with possible weaker poll numbers, will encourage Trump to consider pausing the trade war with China and refraining from additional tariffs until after the 2020 elections.

Our projections don’t take into account the impeachment inquiry now underway in the House of Representatives. While we believe it’s too early to gauge the impact of these proceedings, we do not believe the Senate would produce the necessary 67 votes to convict Trump in the event the House returns articles of impeachment.

On a related note, if the impeachment process reduces Vice President Joe Biden’s chance to be the Democrat’s nominee in the 2020 presidential election because of questions about his family’s dealings in Ukraine, we think it improves the odds that Sen. Elizabeth Warren wins the party’s nomination. We believe a Warren nomination would be viewed unfavorably by the markets due to her positions on taxes and regulation.

After two consecutive quarterly interest rate cuts by the Federal Reserve (Fed), the federal funds target range currently is 1.75–2.0%. We believe one more rate cut is likely by year’s end. In September, the overnight interest rates on repurchase agreements spiked, spooking the markets. We think the upward pressure on rates is a sign banks do not have as many excess reserves as the Fed originally thought, and there is a shortage of dollars as a result. We believe the Fed will soon allow its balance sheet to grow once again, which should inject the necessary liquidity into the banking system.

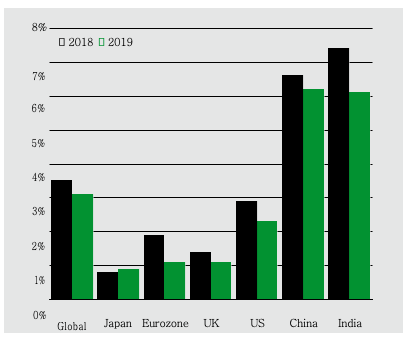

GLOBAL GROWTH CONTINUES AT A SLUGGISH PACE

Source: Ivy Investments. Chart shows 2018, 2019 forecasts of annual gross domestic product (GDP) growth, all based on purchasing power parity. Past performance is not a guarantee of future results. The GDP growth forecasts are current through Oct. 31, 2019, and are subject to change at any time based on market and other conditions. No forecasts can be guaranteed.

WEAKNESS IN THE EUROZONE

The pace of economic growth in Europe has weakened to below 1% on an annualized basis, mainly due to the drag of global trade and Brexit uncertainty. Related to this performance, Germany posted negative growth in the second quarter, and, in our estimation, could show a technical recession when third-quarter numbers are released. We anticipate eurozone growth will remain weak through the rest of the year, but could see some stabilization sometime in the fourth quarter.

The European Central Bank (ECB) introduced a broad stimulus package in September, including lower rates, a reboot of quantitative easing (QE) and a commitment to maintain these initiatives until inflation moves towards its target of just below 2%. With core inflation currently around 1%, we expect these policies to be in place for at least the next year or two.

Brexit fears continue to weigh on the U.K. economy. Since taking office in July, Prime Minister Boris Johnson has created chaos with continued threats to take the U.K. out of the European Union at the Oct. 31 deadline without a deal in place. In response, the U.K. Parliament passed a law requiring the nation to seek an extension to the Brexit deadline. Johnson is attempting to do everything he can to prevent that from occurring.

SIGNS OF REFORM AND STIMULUS IN EMERGING MARKETS

The Chinese economy continues to slow. While official GDP data slowed to 6.2% in the second quarter –down slightly from 6.4% from the previous period – monthly data through August pointed to further weakness in the third quarter. While policymakers continue to indicate a loosening of fiscal and monetary policy is needed, actual stimulus has been disappointing up to this point. For the second time this year, the People’s Bank of China cut its reserve requirements in September. However, credit growth continues to be lackluster. The benefits from various tax cuts that occurred over the past year are starting to wane. Infrastructure spending has been weak, despite a rebound in the most recent monthly period.

All of this indicates authorities are not yet overly concerned about the effects of the trade war or the impact from tightening on credit growth and property. We believe additional stimulus will be necessary to prevent further weakness and rising unemployment, although not at the previous levels that triggered a dramatic boost in China’s economy.

Stress around non-bank financial institutions have tightened financial conditions in India, which has resulted in the weakest GDP growth in six years. This prompted the Reserve Bank of India to slash interest rates by 135 basis points this year. In addition, Prime Minister Narendra Modi announced a reduction in corporate tax rates. These moves should be supportive of economic growth.

An interesting takeaway from India’s tax cuts was a new provision that allows lower tax rates for manufacturing companies that establish bases of production in the country. This is clearly an effort to attract companies looking to diversify supply chains away from China. While India has the scale in terms of population, the country needs to continue to improve its infrastructure and introduce further reforms. If Modi were to move in this direction, it could be quite positive for the future of the country.

Brazil’s economy is beginning to show signs of life after several difficult years. Pension reform was approved by the lower house of Brazil’s National Congress, and appears likely to sail through senate approval early in the fourth quarter. We believe Brazil’s economy will gradually improve from here on the back of lower interest rates and positive sentiment around the progress of fiscal reform.

Past performance is not a guarantee of future results. Risk factors: Investment return and principal value will fluctuate, and it is possible to lose money by investing. International investing involves additional risks, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Fixed income securities are subject to interest rate risk and, as such, the net asset value of a fixed income security may fall as interest rates rise.

The opinions expressed are those of Ivy Investment Management Company and are not meant as investment advice or to predict or project the future performance of any investment product. The opinions are current through October 2019, are subject to change at any time based on market and other current conditions, and no forecasts can be guaranteed. This commentary is being provided as a general source of information and is not intended as a recommendation to purchase, sell, or hold any specific security or to engage in any investment strategy. Investment decisions should always be made based on an investor’s specific objectives, financial needs, risk tolerance and time horizon.

NOT FDIC/NCUA INSURED | MAY LOSE VALUE | NO BANK GUARANTEE | NOT A DEPOSIT | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY IVY DISTRIBUTORS, INC. IVY-DEREK-Q4/43688 (10/19)

© Ivy Investments

Read more commentaries by Ivy Investments