“The markets appear to be emerging from a psychotic break from reality. The ugly process of repricing risk has begun. The market's reaction to Uber and Lyft was the Monday morning sunrise ending a young Robert Downey Jr. Miami weekend binge. The shelving of the We and Endeavor IPOs was the market preemptively taking keys away, arresting the bender before it starts.”

Scott Galloway – Professor of Marketing, NYU Stern School of Business

Listen... do you hear that? A bubble is popping. No, we aren’t talking about the stock market... well, at least not the stock market you’re probably thinking about1. Generally, public companies have the economics to back up their lofty valuations, even if those valuations are, well, lofty.2 It is the market for private companies, specifically those backed by venture capital (VC), that looks truly bubblelicious.

Recent years have seen the rise of the well-documented phenomenon of “unicorns” – private companies valued at over one billion dollars, often coming from Silicon Valley. To borrow the terminology of financial commentator Matt Levine, these “unicorns” have grown up and now that they are emerging from the “enchanted forest” of private markets via an IPO, they are discovering that the real world can be a dark and scary place. To name a few examples, Uber, Lyft, Peloton and SmileDirectClub are down 20, 40, 15, and 30 percent respectively since their IPOs this year. If these declines were the cracks in the walls3, then perhaps the failed IPO of WeWork was the VC dam finally breaking.

But first, how did we get here? Consider Steve Jobs. Steve Jobs was a phenomenon. He revolutionized companies and industries – multiple times. His vision was so strong, his presence so over-powering, that he created what some people called a “reality distortion field” where the impossible became possible, and he was able to get his comrades to follow an impossible dream and turn it into a reality. After he built Apple into a global powerhouse (for the second time), he passed away and a slew of books were written about him that lionized his achievements, but also revealed that he was kind of a jerk. Naturally, people wanted to emulate his successes. Millions of people read these books, saw these things, and learned the wrong lesson. The lesson some learned was: to be a visionary leader, you have to be a jerk. That may have worked for Steve Jobs, but it is not good advice for the average leader. The average person does not have a reality distortion field and instead needs to charm others to get cooperation. The average person is better off, will accomplish more, will be a better leader, by not being a jerk.

The same sort of thing happened with Amazon: people learned the wrong lesson. For years, Amazon grew extremely fast but earned no, or negative, profits along the way. Many people doubted this business strategy would ever be successful. But when Amazon ended up being incredibly valuable, and eventually, profitable, this perception began to change (even though this result was achieved in large part by discovering and succeeding in a different business: cloud computing). The wrong lesson learned was this: it is a great strategy to grow really fast and not care at all about profitability. We disagree: this is not a great strategy for every business, or even most. Most companies are not Amazon. Most companies are not going after the gargantuan market opportunity that Amazon was. It was, and is, clear that online shopping was, and is, going to become more popular; furthermore, the scale is huge, so years of unprofitability could be worth it to get such a prize. But, in another sense, one could argue that Amazon got somewhat lucky with this strategy. It was fortunate to have one of the best CEOs in America. He was willing to try new things, and thus they experimented with Amazon Web Services (AWS) which was a fantastic smash hit. AWS is an amazing business (no ongoing losses there) that currently earns more than half of total company pretax profits.

It is truly amazing how many companies have embraced the Amazon inspired, grow-fast-and-worry-about-profits-later strategy. There are so many VCfunded, loss-making companies that some have talked of a VC-subsidized lifestyle. Let us explain: ever ridden in an Uber or a Lyft? Despite all the ink spilled on how these companies barely pay their drivers, according to the data we’ve seen, Uber and Lyft lose money on each individual ride. The fee you paid didn’t cover the cost of that individual ride (let alone the cost of headquarters, etc). Who made up the difference? Venture capital; their dollars covered the costs that the fee you paid didn’t. What if you order food through Postmates4? Or ride a Lime scooter5? Or work at a WeWork or even live in a WeLive? All of these services are provided below cost by money-losing enterprises backed by venture capital dollars. If this was your day, then you’re living that VC-subsidized life.

Because so many people learned the wrong lesson from Amazon, this grow fast-lose-money strategy is seen as desirable and has practically become gospel. This approach can work until you finally “make it” to enough scale and are profitable, like Amazon did. But there is another way this strategy can “work”. Growing quickly and racking up losses is a viable strategy... if everyone believes in it. Today’s believers are the venture capitalists6. If the VCs feel like it, they can keep funding your loss-making ventures. Indeed, if they too believe in the Amazon strategy, they will be excited by the fast revenue growth and untroubled by losses. Each round of fund-raising takes place at a higher and higher valuation. Investors see the gains of early entrants and allocate more money into the space. Early investors are cashed out by the later investors. Everyone is winning. This... is what a bubble looks like.

The above described dynamic works... until it doesn’t. When investors lose faith in this strategy, it stops working. At all. And this is what’s happening now. Or at least so it appears to us.

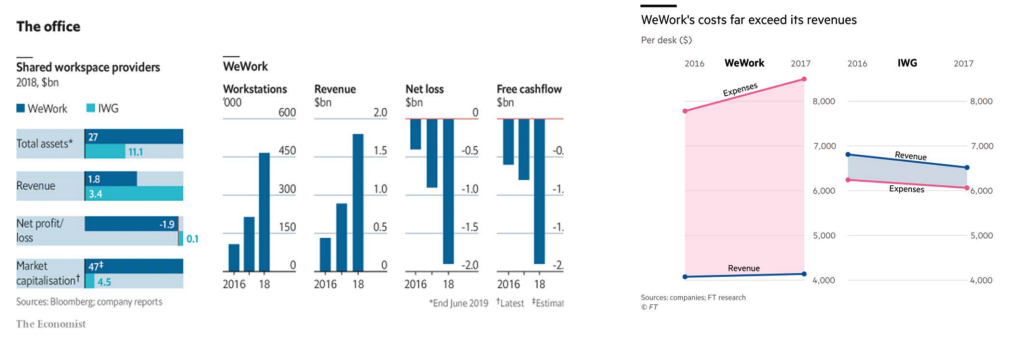

Though there are many others, WeWork is the quintessential example of this strategy... and how the perception around it is potentially changing. WeWork is of course the venture-backed office outsourcing business: they rent space by-the-building and then sublease it by-the desk. It had been growing at warp speed. Accordingly, its primary backer, SoftBank, kept pushing its value higher, funding round after funding round. The most recent iteration valued the company at $47 billion, on its way to an IPO. Wall Street, trying to win that IPO business, played along and issued reports stating that an IPO could value the company at $100 billion. And the way things have been for the last five years… that crazy IPO could have happened. But then something changed. Investors actually read the company’s prospectus and balked at all the corrupt self-dealing and terrible economics. Fast forward to today, the CEO is out, the IPO is off, employees are being laid off, and amid a cash crunch, WeWork has just been rescued (again by Softbank)... at a valuation of just $8 billion.

Investors have figured out that WeWork is a terrible business. The greater the revenue, the bigger the losses and cash burn. It’s not even a novel business model. IWG plc is another office space provider with basically the same business model. It is publicly traded and mildly profitable (though it went bust in the last recession). IWG’s 2018 revenue was nearly double that of WeWork, yet WeWork’s last fundraising valuation stood at more than ten times that of IWG. What accounts for the ridiculous difference in valuation?7 WeWork used the word “tech” 123 times in their IPO prospectus.

NYU Professor, Scott Galloway, says it best8: “Find the hottest sector, and if you don't have the insight, IP, genius, capital, code, skills, human capital, or a clue, then just borrow the words. SAAS9 firms trade at a multiple of revenues (yay), vs. real estate firms, which trade at a multiple of EBITDA (boo). So, We[Work] isn't a real estate firm renting desks, it's a Space as a Service (SAAS) firm. I know, use the word "technology" over and over, despite having little R&D and computers and stuff, and voilà … we're Salesforce.”

There are other examples of this phenomenon of faith-based, profitless growth. WeWork is simply the one which has taken up the most space in the collective consciousness. The WeWork situation was so big, so wellcovered, so egregious, and so disastrous, it may have triggered an inflection point in the profitless growth mentality... or at least in how these enterprises are valued. The VCs and their investments may now be caught in a cascading waterfall. The disastrous IPOs named in this letter’s opening quote burned public shareholders and, perhaps as a result, other late stage ventures (like WeWork and now Postmates and Endeavor) can’t go public at all. This could be the start of a vicious cascade which would go something like this:

- Highly valued private companies have IPOs where their stocks tank (Uber, Lyft)

- Public investors are more skeptical of IPOs of loss-making companies (Postmates)

- Private companies are forced to stay private (WeWork)

- These companies are forced to raise money in private markets again (remember, they are not self-funding)

- This next round of fund raising in the private markets comes with a lower valuation, i.e. a “down round”

- The “down round” causes paper losses to show on VC funds. Investors start allocating less money to venture capital

- With less VC money to go around, the next fund can’t get raised. More down rounds happen

- VC companies can’t get funding AT ALL

- VC companies stop spending like crazy

- VC companies lay people off

- Start of... the next recession?

What generally causes a recession? Supposedly, economic expansions don’t die of old age. One of two specific types of events is required. The first is an external cost shock, with the classic example being the 1970s oil embargo, when the all-important price of oil shot through the roof10. The second and more common cause is a misallocation of capital. Examples of this are S&Ls in the 1980s, dotcom companies in the 1990s and housing in the 2000s. When the misallocation is realized by society, the bubble pops, people in the bubble industry (construction workers/mortgage brokers/bankers) lose their jobs and unemployment rises. Investors who lost money investing in the bubble pull back on investment. Financial institutions, worried about getting stuck with defaults, pull back on financing. Financing-sensitive activities, like factory expansions or car purchases, get hit. How bad these three factors are determines how bad the recession is. If private market investors no longer wish to continue financing loss-making companies at such scale, that means the VC bubble has popped, and going forward there will be investment losses, employment losses and knock-on effects.

What will a venture capital downturn look like? Bubbles in the stock market pop fast whereas the housing bubble deflation took a few years. A VC bubble would likely be somewhere in between. In terms of size, the “bubble” in VC is likely closer to the dotcom bubble than the massive housing bubble and less connected to the financial system than the housing bubble and S&L crisis, thus any effect on the broad economy from a bubble popping would likely be relatively mild.

Any popping of a VC bubble would also happen somewhat out of public view. That said we are already getting (unconfirmed) reports of large blocks of private stock in well-publicized unicorns being offered at 50% discounts to the last announced round. If this is true, it will doubtlessly result in large economic adjustments.

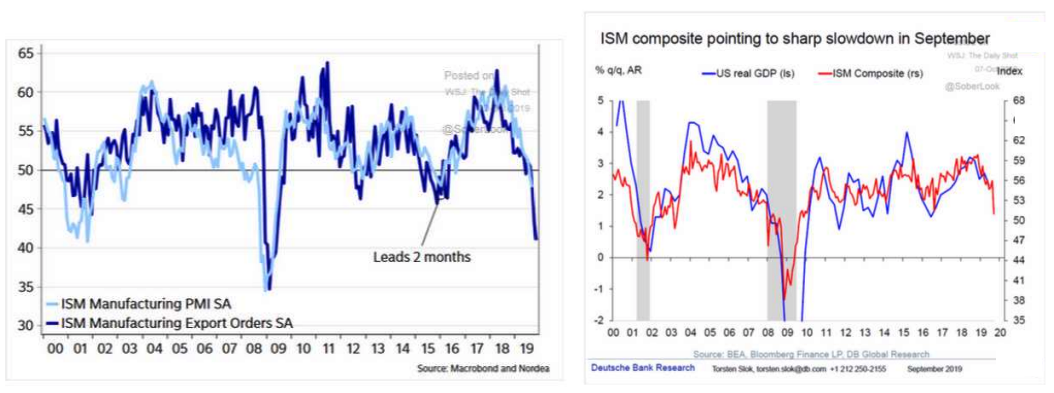

Turning now from the tribulations of venture capital, to the regular economy at large, the update is the same as last time: economic stormclouds are still gathering but haven’t really broken just yet. The ISM manufacturing Purchasing Manager Index (PMI) is now firmly negative. New export orders (dark line in left graph) are especially poor. Remember that PMIs are one of the best leading indicators of the economy, as shown in the graph at right. It seems the trade war is finally hitting home... though don’t forget that future tariff escalations are still scheduled for December.

During the quarter, another ominous sign appeared in the bond market. For the first time since the financial crisis, the yield on 10-year Treasury bonds dropped below that of 2-year Treasuries during August11. This is the big inversion everyone feared, that we discussed in our Q4 2018 letter12. We hope we are wrong, but we continue to be on recession watch.

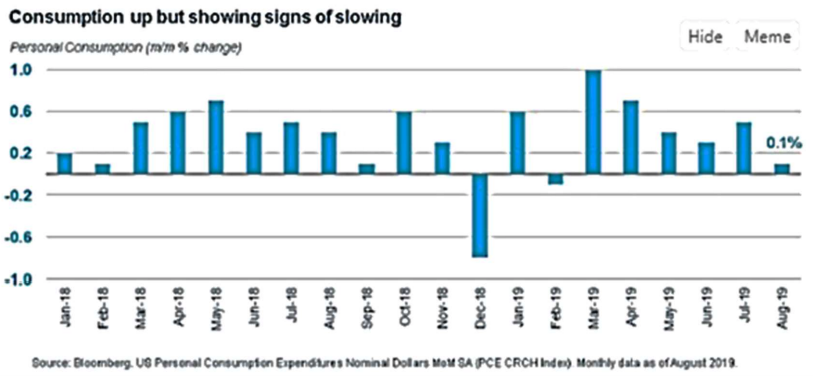

For now, the economy remains in decent shape. That’s because consumer spending makes up nearly 70% of GDP. Aside from the large decline in December 2018 (a month in which the stock market plunged), consumer spending has consistently increased, albeit at a diminishing rate of late.

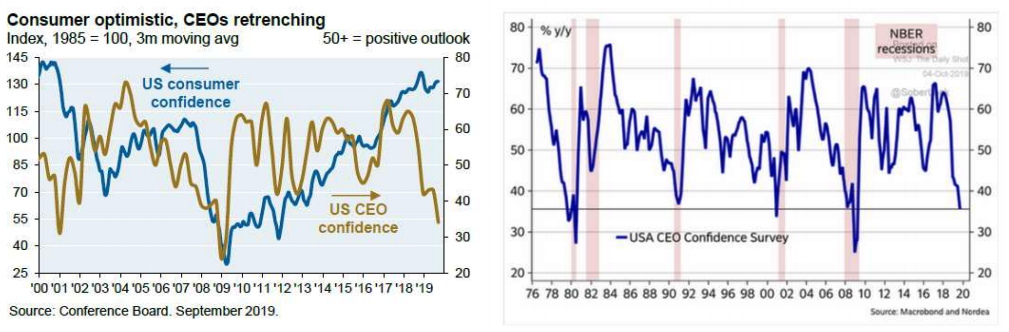

It’s no surprise consumers are spending given the level of US consumer confidence. But consumer confidence is a measure of how things are, not necessarily where they’re going. CEOs, unfortunately, have a much more negative outlook and tend to have a better idea about what is coming next.

Lately, what has ended up being the most important factor in the daily fluctuations of the market has been the trade war. The Dow swings hundreds of points (billions in value) based on whether Trump’s tweets are conciliatory or hostile. But we wonder if the skirmish will end up mattering in the end. Will a trade truce necessarily result in a skyrocketing market? In the run up to the 2016 election the market was terrified of Trump. Every time he rose in the polls, the market fell; this pattern was repeated on a daily basis. Good news for Trump was bad news for the market. Good news for Hillary was good news for the market. This pattern was clearly established across hundreds of discrete market events. And then what happened? Trump won and the market took off, completely invalidating the previously established relationship. This is to say: sometimes even the market itself focuses on the wrong thing or gets it wrong.

It is our job to worry about all these issues and we will remain vigilant. As always, we are invested alongside you, knowing the markets will reward us over time regardless of where, inevitably, recessions may periodically fall.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 Though small parts of the stock market are perhaps in a bubble. Momentum and growth stocks are more expensive than value stocks on a price/earnings basis to a degree not seen since the dotcom tech bubble in the late 1990s.

2 As we’ve discussed previously, given how low interest rates are, equity valuations ought to be lofty compared to historical valuations. Perhaps they are too high, but even then, we wouldn’t call it a “bubble”.

3 A further sign is the downward trend in appreciation by tech IPOs: up 94% in 2017, up 13% in 2018 and up only 5% this year.

4 Which just postponed its IPO

5 Which just lost $300 million on revenue of $420 million

6 We use this term a little loosely since much funding for late stage private companies has come from mutual funds as well.

7 WeWork’s $47 billion valuation was 20 times 2018 revenue. IWG trades at 1.6 times 2018 revenue.

8 For those interested in this subject, we highly recommend you search online for “Galloway” and “WeWork” to read more about what he has to say. Sometimes bombastic, Galloway is insightful, extremely readable, and so far has been spot on regarding this topic. Good examples: http://nymag.com/intelligencer/2019/10/marketing-expert-scott-galloway-onwework-and-adam-neumann.html https://www.businessinsider.com/nyu-professor-calls-wework-wewtf-and-slamsbankers-2019-8

9 SAAS stands for “Software as a Service”; the hottest segment of the stock market this year... though having its own troubles of late.

10 Could the recent tariffs qualify as such a shock? They do represent a cost shock, but one which is much smaller in magnitude (at least in direct terms) than the 70s oil crisis. US exports represent roughly 12% and imports 15% of GDP.

11 The 10yr-3m and 10yr-2yr yield curve spreads are now back in positive territory (i.e. they un-inverted). Un-inversion is not uncommon on the road to recession.

12 As a reminder, we warned in our Q1 2019 letter that the inversion of the 10yr3m curve, which had just occurred, might portend a peaking stock market in September, with a recession following in January… though this is only based on an average of past cycles and is not meant as a pinpoint estimate.

© Knightsbridge Asset Management, LLC

More Fixed Income Topics >