Climbing the ESG Learning Curve in Emerging Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsExecutive Summary

ESG integration is best used as a tool to improve portfolio returns and/or reduce risk. While usually thought of as a company-level concern, material ESG data can be very useful at the country level as well, especially in emerging markets. ESG signals are only as good as the quality of their inputs. Portfolio managers therefore need to determine which ESG inputs are material to their specific investments and not rely blindly on third-party ESG ratings. They also need to establish a process to resolve any conflicts with other fundamental signals, for example, via company engagement. Performance attribution of ESG signals, at least in the short run, requires both qualitative and quantitative analyses.

Over the last couple of years, as we have systematically applied material Environmental, Social, and Governance (ESG) signals into the investment process of our GMO Emerging Domestic Opportunities (EDO) strategy, we have learned several key lessons that reinforce our original research thesis and help us maintain our enthusiasm over having this more robust toolkit moving forward.

Lesson 1: Country ESG Risks Can Be Highly Material

Country allocation can be a very powerful driver of returns. We studied the difference in country performance relative to the MSCI EM index over a typical 3-year period and discovered that if a manager is able to identify and allocate to the 10th best performing country while avoiding the 10th worst country, the resulting spread is an impressive 8% per year in emerging markets.

ESG performance varies widely across emerging countries. Taiwan, for example, scores significantly higher than China. ESG therefore provides us an opportunity to add differentiation along a dimension that can matter quite a bit to returns.

At the country level, our evaluation is based on both long- and short-term models. The long-term models include factors that we believe will impact the prospects and health of an economy in the long run. ESG signals such as the quality of institutions and political capacity are already included as we know these are critical to the long-term attractiveness of a country. After deciding to take a more comprehensive view of ESG, signals related to air pollution, water stress, and national climate policies along with social signals related to health, education, and equality were added to our long-term country evaluation models.

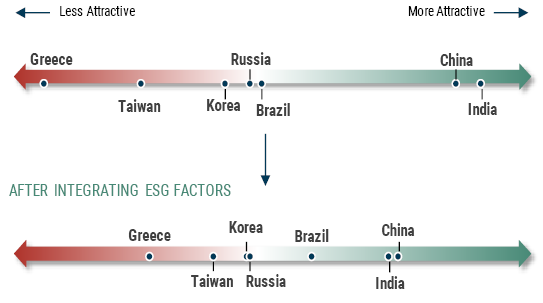

With this in mind, we will compare and contrast what ESG signals tell us about Taiwan and China.

Taiwan scores better than China on ESG signals such as the strength of institutions that constrain leaders, the business climate, and the prevalence of corruption. However, Taiwan is a much smaller domestic growth opportunity given its population of only 25 million and relatively high income of $25,000/capita, which places the average consumer well above the sweet spot of consumption ($3,000 to $10,000/capita).

China, on the other hand, is perfectly poised for increased domestic demand with a population of 1.3 billion and per capita income of $9,000. What this means is that ESG gives Taiwan a boost that brings its long-term attractiveness closer to that of China but not so much of a boost that it can counter the huge edge China enjoys with other aspects of our long-term evaluation framework. Exhibit 1 demonstrates the impact of integrating ESG signals from our proprietary country ESG model on long-term country attractiveness.

EXHIBIT 1: IMPACT OF ESG INTEGRATION ON LONG-TERM COUNTRY ATTRACTIVENESS: SELECT EM COUNTRIES

As of 9/30/19 | Source: Worldbank, WEF, Germanwatch Climate, Factset, GMO

Case Study: Physical Climate Risks – India vs. China

In order to better understand how the country-level ESG risks translate into negative impacts on a company’s fair value, let’s look at the varying level of preparedness of India and China to manage a key country-level ESG risk – Physical Climate Risk. Indian farmers are highly dependent on monsoons and have low crop insurance coverage, which means subpar rains lead to massive rural distress. The government typically responds by waiving loans to small farmers (over USD 25 billion of loans have been waived since 2014). This buys short-term popularity, but carries long-term negatives for the economy as the fiscal slippage leads to lower government spending on infrastructure development (say, for improved irrigation). This practice leaves India vulnerable to future impacts of climate change, and adds the further burden of weakened balance sheets in the banking system, which impacts growth. China, despite having just as large a population as India, has ensured that its economy is more resilient when facing risks related to climate change. It has channeled a lot of its debt toward infrastructure development. For example, China has irrigated the majority of its farming areas by diverting rivers and building canals. This has not only lowered the dependence on the rains, but it has also led to increased productivity, with Chinese crop yields being approximately twice those of India.

Lesson 2: Don’t Rely Blindly on Third-Party ESG Ratings

At the stock level, we estimate the internal rate of return (IRR) for each company using bull, base, and bear case scenarios. ESG signals are factored into each of the three scenarios with, not surprisingly, the bear scenario being the most affected because a majority of ESG signals evaluate the degree of unmanaged risks rather than growth opportunities.

We do not rely blindly on third-party ESG ratings for companies as they tend to be “all things to all people” and, in the process, inevitably include some noise. Moreover, these "desk-based" rating models rely predominantly on data disclosed by companies themselves – some of which may be greenwashing (i.e., "more talk, less action"). Therefore, these agencies are not always able to fully incorporate on-the-ground context into their analysis and ratings, thereby possibly leading to an unwarranted negative view in some cases. Our research also showed that ratings for the same issuer from different agencies have low correlation. In short, whether a company is sustainable or not may depend on which rating agency you refer to.

In order to have the ability to determine materiality of ESG signals and apply them more effectively, we worked to construct our own materiality assessment framework using in-house ESG expertise to identify and weigh material ESG issues, in concert with external frameworks such as the Sustainability Accounting Standards Board’s (SASB) materiality maps. As we explained in detail in our previous white paper,1 issue selection, as well as its relative importance, is a factor of the type of business, its geographical footprint, the degree of financial impact that the ESG issue itself may cause if not sufficiently managed, as well as the likelihood of, and the time horizon over which, the financial impact is expected to occur.

As EM companies have had their fair share of Corporate Governance (CG) related controversies, we have also developed our own CG assessment framework for emerging markets that consists of more than 50 indicators designed to identify red flags related to aspects such as board autonomy, ownership structure, related party transactions, investor relation practices, and executive compensation.

We also utilize our dedicated channel check analysts in India and China and respective country analysts for other countries to verify some of the risks flagged by third-party ESG rating agencies. We then formulate a more robust view about how the company is managing such risks.

In the stock selection process, the analysts adjust their bull, bear, and base case IRRs based on unmanaged material ESG risks that we identify via a combination of third-party data and our in-house analysis. In order to support systematic and efficient ESG integration, we have developed tools like ESG dashboards, which display a company’s current and historical ESG performance coupled with analysis of material risks and strengths provided by our dedicated ESG specialists.

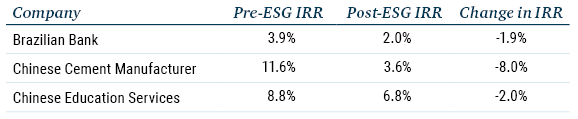

EXHIBIT 2: IMPACT OF ESG INTEGRATION: RELATIVE ATTRACTIVENESS OF CERTAIN COMPANIES HAS DECLINED…

…While for Some Others, It Has Improved.

Source: GMO

Depending on the nature and degree of unmanaged material risk identified by our analysis, the analyst may change his estimates related to margins, compliance-related CAPEX, cost of capital, etc. In most cases, the integration of ESG risk signals leads to a reduction in the base case IRRs and therefore relatively smaller position sizes. Occasionally, it may lead to a decision not to invest as the degree of unmanaged risk is not commensurate with our expected return estimates. However, we have also seen some cases where the company is poised to capitalize on ESG opportunities, leading to a higher base case IRR and therefore a comparatively larger position size in the portfolio.

Lesson 3: Resolving Conflicting Perspectives – It’s Not Always Black or White!

We believe ESG integration is as much an art as it is a science. That is the reason we do not make decisions based on a single score or rating while integrating ESG. This approach allows us to reconcile conflicting pieces of information coming from an analyst's fundamental view and the ESG risk and/or strengths of the company. We take a more holistic approach, which includes having a view on which issues are material, quantifying their potential impact on fair value, and engaging with management in cases where there is not enough clarity on various initiatives that are implemented to sufficiently manage these risks.

Channel checks are an important part of the puzzle: we have found some instances where blindly relying on ESG rating agencies could have led to grossly incorrect position sizing decisions. The 2017 case of Alibaba Group (NYSE: BABA) and its Chinese video hosting subsidiary Youku’s alleged involvement in a data breach that reportedly caused the loss of 100 million users’ login credentials is an interesting example of this framework in action.

Relying primarily on a single news post originating from a little-known website, a prominent ESG ratings agency plunged Alibaba into significant controversy, leading to an extremely negative impact on its overall ESG rating. Our in-house analysis, coupled with on-the-ground research by our Chinese channel check analyst, determined that there was no conclusive evidence supporting the occurrence of such a data breach.

In addition, we did not find evidence of any significant financial and/or reputational impact to Youku that would warrant such a severe penalty to Alibaba’s ESG rating. Based on our findings, we rejected the negative view on the topic of Privacy and Data Security and continued to maintain a large portfolio position in Alibaba through 2017.

Roughly a year later, the agency upgraded Alibaba’s ESG rating, stating that previous data-breach-related concerns at Youku were “unfounded.” Had we relied solely on off-the-shelf third-party ESG ratings/views, we would have missed investing in one of the most rewarding opportunities in emerging markets over the 2017-18 period.

Another example occurred in 2018 when our analyst had a strong "buy" conviction based on his fundamental analysis of a Taiwanese food product company. However, our ESG analysis flagged some risks related to food safety as well as the company’s ability to sustain long-term growth by introducing healthier choices to its product line-up.

We decided to engage directly with the company and learned that management was taking actions to prevent the recurrence of previous ESG issues, including food safety concerns, while also promising to create action plans to manage other areas of concern. We were satisfied with management’s approach and its willingness to tackle some of these unmanaged ESG risks such that we decided to hold the position and continue to monitor the company's progress on these challenges.

Both examples support our view that ESG integration is as much an art as it is a science.

GMO views proxy voting as an integral aspect of security ownership and the function is conducted with the same degree of prudence accorded any fiduciary obligation of an investment manager. Therefore, in addition to direct engagement with select portfolio companies, all of GMO’s proxy voting activities are aligned with Institutional Shareholder Services’ (ISS) Sustainability Policy. We are also participants of the Climate Action 100+, a multi-year collaborative initiative to engage systematically important greenhouse gas emitters and other companies across the global economy that have significant opportunities to drive clean energy transition. Engagement, especially in emerging markets, is an important tool to create awareness regarding the importance of sustainable corporate behavior and also to encourage enhanced disclosure.

Lesson 4: Don’t Look for Short-Term Market Performance to Vindicate the Efficacy of ESG Integration

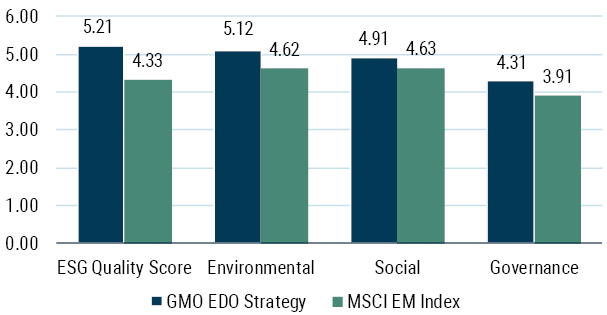

Given ESG is one of the many factors that influence our investment decisions, it is challenging to isolate the impact of ESG integration, especially in a fundamental investing process. One way to confirm whether the ESG integration process is effective or not is to track the portfolio ESG quality score – a weighted average of the underlying holdings’ overall ESG scores. When we started building the ESG analysis and integration process, the EDO Strategy’s ESG quality score was in line with its primary benchmark (i.e., the MSCI EM index). Over time, systematically integrating ESG risks and opportunities has led us to structure the portfolio to have higher weights in companies that demonstrate strong fundamentals in addition to strong ESG risk management.

In our most recent quarterly evaluation, our portfolio (see Exhibit 3) continued to score in the top decile of the Equity Emerging Markets Global peer group with a significantly better (>20%) portfolio ESG quality score when compared to its primary benchmark as per MSCI’s ESG Portfolio Analytics report.

EXHIBIT 3: ESG PERFORMANCE OF GMO’S EDO STRATEGY IS SIGNIFICANTLY BETTER THAN THE MSCI EM INDEX2

As of 6/30/19 | Source: MSCI ESG Research LLC. Reproduced by permission.

However, determining the portfolio performance impact of ESG integration is not entirely straightforward because most of these ESG issues are expected to play out over the long run and not necessarily over each year. As the frequency and magnitude of drawdowns due to mismanagement of ESG risks continue to increase, we expect strategies that ignore ESG signals while taking investment decisions to underperform the ones that integrate them, all other things being equal. Having said that, we have already had instances where appropriately factoring in ESG risks helped us make better investment decisions. Following are examples for both stock selection and country allocation.

Case Study: From Beloved to Bust

Vakrangee Limited (NSE: Vakrangee) provides banking, insurance, e-governance, e-commerce, and logistics services, primarily in rural and semi-urban areas of India. It was one of the leading distributors of the Government of India’s financial inclusion program and a key partner for Amazon’s assisted e-commerce. The company had garnered a relatively strong ESG rating of “A” by a leading ESG ratings agency (as of January 2018) with its corporate governance practices being assessed to be in the top quartile when compared to peers.

Our initial fundamental analysis and channel checks (in mid-2015) uncovered several red flags, including governance and accounting risks such as aggressive revenue booking, an external auditor lacking credibility, and franchisees complaining of delays or non-receipt of dues. At that time, we decided not to invest because of these concerns. Our follow-up channel checks in the first quarter of 2017 showed incremental improvements in some of the risks flagged previously. Therefore, we decided to take a small position. Cognizant of the governance risks identified, we regularly rebalanced the position size as the share price rose exponentially through 2017.

During January 2018, there was a massive drawdown that halved Vakrangee's market capitalization within two weeks. This drawdown was driven by media reports of a regulatory probe for possible share price manipulation, as well as concerns related to an equity investment into an unrelated business. Because of our prudent risk management, unlike some peers, our portfolio was not significantly impacted by this episode.

The China vs. Taiwan case described earlier is a good example of ESG’s impact on country allocation. The policy uncertainty is high in China because power is concentrated in one person. President Xi Jinping's decisions on various issues such as the trade war with the U.S. and deleveraging the Chinese economy determine government policies, and ultimately the environment in which companies operate.

In contrast, Taiwan’s policies fall within a much narrower, more predictable band that is tied to its large tech sector, its reliance on trade, and past government policies. Taiwan outperformed China in 2018, a year in which investors were risk-averse and favored the robust macro conditions in the former over less certain macro conditions in the latter. Therefore, the ESG input into our country allocation decision was beneficial in 2018.

As portfolio managers, we do not look to short-term market performance to consistently vindicate the efficacy of ESG integration. Instead, we do an “attribution” of ESG by clearly understanding the reasons, for example, behind Taiwan’s higher ESG score vs. China’s. We then confirm that the time period in question was one that provided an environment conducive to those reasons. Then, and only then, do we determine how ESG signals have translated into superior performance.

The Learning Continues…

As we reflect on our ESG integration efforts thus far, we are quite satisfied with the value added by integration of both country-level and stock-level ESG signals into our investment process. The success is not only reflected by our portfolio’s strong ESG scores compared to both peers and the benchmark, but also via numerous examples wherein ESG signals have been useful in making better investment decisions. As ESG risks and opportunities continue to evolve, it is natural to think about how we could strengthen our approach in the future.

A key topic that we are increasingly delving deeper to assess is the direct and indirect impacts of climate change on our portfolio. Owing to a significantly lower carbon footprint and intensity compared to peers as well as the benchmark, our portfolio has limited carbon transition risks. However, certain companies remain exposed to physical climate risks due to asset impairment (say, in the Real Estate sector) and/or operational disruptions due to extreme weather events. Given our exposure to countries such as India, China, and South Africa, which are exposed to a high degree of water stress, we recently assessed identified companies in our universe that are highly vulnerable to water stress using data from the World Resources Institute’s Aqueduct tool as well as corporate disclosures on water risk management. This analysis will also be useful in engaging further with these companies. Moreover, we are testing the resilience of our portfolio under various climate scenarios as this will help us better identify and manage climate risks within certain highly-exposed country-sector sets.

Another aspect that some of our clients are increasingly interested in is attribution of ESG at the portfolio level. Given ESG is one of the many factors that influence our investment decisions, it is challenging to isolate the impact of ESG integration, especially in a fundamental investing process. The other difficulty lies in the horizon mismatch between the impact of ESG signals and portfolio performance analysis. We are thinking about ways in which we can better define and report the impact of ESG on the overall portfolio’s performance. Stay tuned!

1 Binu George and Hardik Shah, “ESG Improving Your Risk-Adjusted Returns in Emerging Markets,” March 20, 2018. This GMO white paper is available at www.gmo.com.

2 Although GMO’s information providers, including without limitation, MSCI ESG Research LLC and its affiliates (the “ESG Parties”), obtain information from sources they consider reliable, none of the ESG Parties warrants or guarantees the originality, accuracy, and/or completeness of any data herein. None of the ESG Parties makes any express or implied warranties of any kind, and the ESG Parties hereby expressly disclaim all warranties of merchantability and fitness for a particular purpose, with respect to any data herein. None of the ESG Parties shall have any liability for any errors or omissions in connection with any data herein. Further, without limiting any of the foregoing, in no event shall any of the ESG Parties have any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of the possibility of such damages.

Disclaimer: As of June 30, 2019, Alibaba was held with the Emerging Domestic Opportunities Strategy and is considered by GMO to be a “hold” recommendation. The information presented on this security or any others discussed in this paper is not definitive investment advice, should not be relied on as such, and should not be viewed as a recommendation by GMO generally as of the date indicated. It is presented solely to illustrate GMO’s investment process and its analysis and views of the security presented as of the date indicated. The security presented is not representative of all the securities purchased, sold or held for advisory clients, and it should not be assumed that the investment in the security identified was or will be profitable. GMO’s views of, recommendations with respect to, and investment decisions regarding, the security presented may vary across GMO’s strategies. Such recommendation is subject to change continually and without notice of any kind and may no longer be true after the date indicated.

The views expressed are the views of Amit Bhartia, Binu George, and Hardik Shah through the period ending October 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2019 by GMO LLC. All rights reserved.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits