Theoretically, there is no single variable more important to the economy than productivity, or output per worker. Productivity growth is how we get improved living standards over time. Faster productivity helps to offset the impact of wage growth, supporting gains in corporate profits. However, in practice, the productivity estimate is among the most troublesome of economic statistics. Productivity growth has slowed over the last week, in the U.S. and worldwide. Efforts to boost productivity growth should be a priority, as improvement would help to counter slower growth in the workforce.

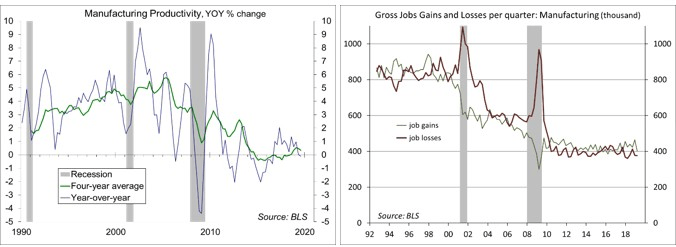

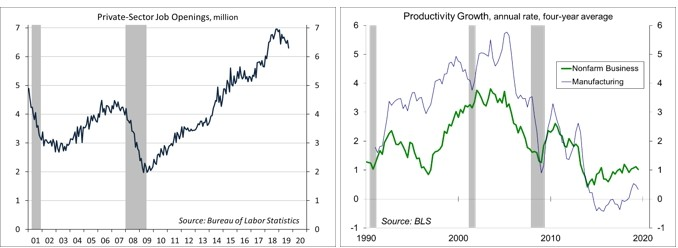

Productivity weakened in the preliminary estimate for 3Q19, down at a 0.3% annual rate (+1.4% y/y). Quarterly figures are quirky and subject to large revisions. However, the underlying trend remains low (a 1.0% annual rate over the last four years). The slowdown in productivity growth is also seen outside of the U.S. and is believed to be associated with a weaker trend in capital spending (also seen outside the U.S.). The slowdown in productivity growth is more pronounced in manufacturing (-0.1% y/y and a +0.3% average over the last four years). This is in contrast to previous decades, when gains in the manufacturing sector outpaced overall productivity growth by a wide margin.

Click here to enlarge

In the 1980s, the rule of thumb was that we would lose one out of ten manufacturing jobs each year, but that job would be replaced by a new job. The U.S. shed low-productivity jobs in areas like textiles and apparel, and grew jobs in higher-end industries, like technology. In the late 1990s, production of new technologies (cell phones, networking equipment, and the internet) boosted overall output per worker. By the early 2000s, these new technologies led to efficiency gains. Firms could produce more with fewer workers. Following the 2001 recession, we didn’t just have a jobless recovery – we had a job loss recovery (we didn’t begin to add jobs until nearly two years after the recession had ended).

Increased trade with China had a significant impact on manufacturing jobs since the turn of the century. However, technology also played a part. The turnover in manufacturing jobs is now about half of what it was in the 1990s. Looking ahead, advances in robotics and artificial intelligence should limit job growth in manufacturing (although there will always be some degree of flux – creation and destruction – over time).

So, how do we boost productivity growth? Efforts to lift capital investment should be a priority. Academic research indicates that cuts in the corporate tax rate are more likely to show up as share buybacks and dividend increases than higher business investment – and that was reinforced by what we saw over the last year. Lowering the corporate tax rate means that the after-tax cost of business investment is greater. Government can help boost productivity growth over the long term by providing greater support for research and development, but that’s not happening.

The tight labor market ought to lead to shifts in labor allocation over time. Workers will tend to move to more productive (higher-paying) endeavors over time. However, that transition is not going to be smooth and will likely be difficult for regions that are far from major population centers. The U.S. economy has always been in a state of flux, but our great success has been our ability to reinvent ourselves over time. If we fail to make needed transformations, that will be our own fault.

Data Recap – Once again, economic data reports were dominated by shifting perceptions in trade policy. However, this time things were flipped. It was the Chinese indicating a possible roll back of tariffs on both sides, sending the stock market higher. However, that was refuted by the White House the next day.

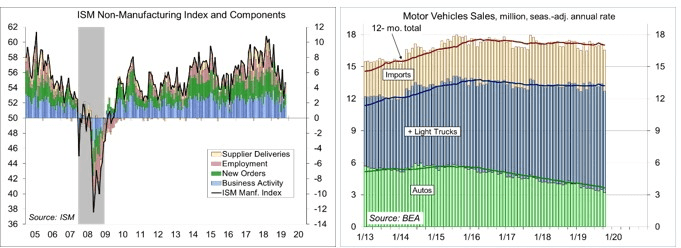

The ISM Non-Manufacturing Index rose to 54.7 in October, vs. 52.6 in September and 56.4 in August. Growth in business activity, new orders, and employment improved following a “soft” September report. Input price pressures were moderate. Comments from supply managers were mixed, but mostly upbeat.

Click here to enlarge

Unit Motor Vehicle Sales fell to a 16.5 million seasonally adjusted annual rate in October, down from 17.1 million in September.

The JOLTS (Job Opening and Labor Turnover Survey) data for September showed a further decline in job openings (trending lower since October 2018), although the level remained very high by historical standards. Hiring and quit rates were little changed from a year ago.

Click here to enlarge

Nonfarm Productivity fell at a 0.3% annual rate in the preliminary estimate for 3Q19, up 1.4% y/y. Unit Labor Costs, the key measure of inflation pressure from labor, rose at a 3.6% pace, +3.1% y/y. In manufacturing, productivity fell at a 0.1% annual rate, down 0.1% y/y, while unit labor costs rose at a 3.6% pace, up 4.9% y/y.

The University of Michigan’s Consumer Sentiment Index was little changed at 95.7 in the mid-November reading, vs. 95.5 in October and 93.2 in September. Consumers remain optimistic about the job market and the impact of the impeachment inquiry is “virtually nonexistent” according to the report.

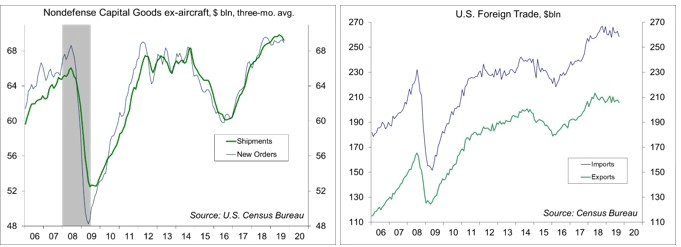

Factory Orders fell 0.6% in September (-3.5% y/y). Orders for durable goods fell 1.2% (revised from -1.1%), down 5.5% from a year ago, reflecting lower orders for civilian aircraft (-11.8% m/m, -42.2% y/y). Orders for nondefense capital goods ex-aircraft, a rough proxy for business fixed investment, fell 0.6%, following a 0.8% drop in August (-1.0% y/y). Shipments for this category fell 0.7% (+0.3% y/y), while unfilled orders fell 0.2% (-2.1%, not a good sign). (M19-2818101)

Click here to enlarge

The U.S. Trade Deficit narrowed to $52.5 billion in the initial estimate for September, about what was assumed in the advance GDP report. Monthly figures can be choppy. Merchandise exports were down 1.4% y/y in 3Q19, while imports fell 2.2% (petroleum -22.3%, non-petroleum -0.1%).

The Bank of England’s Monetary Policy Committee voted 7-2 to leave the Bank Rate unchanged at 0.75%. The statement noted that “Monetary policy could respond in either direction to changes in the economic outlook in order to ensure a sustainable return of inflation to the 2% target.” However, “if global growth fails to stabilise or if Brexit uncertainties remain entrenched, monetary policy may need to reinforce the expected recovery in UK GDP growth and inflation.” Looking ahead, “provided these risks do not materialise and the economy recovers broadly in line with the MPC’s latest projections, some modest tightening of policy, at a gradual pace and to a limited extent, may be needed to maintain inflation sustainably at the target.”

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James