Is It Time to Worry about Debt?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWeighing the Week Ahead: Is It Time to Worry about Debt?

The economic calendar is normal with a focus on housing. Some will be parsing the Fed minutes while others watch the impeachment hearings. This week’s topic may not be a media focus for the week ahead, but it gets constant attention. With a government shutdown and the debt ceiling on the agenda, let’s seize the moment and ask:

Is it time to worry about debt?

I suspect that many readers believe it is way past time!

Last Week Recap

In my last installment of WTWA, I took stock of the recent data avalanche and concluded that it was a good time for investors to act. I also noted that this opportunity would not disappear overnight. The key trends are apparent to the watchful, so the opportunity will last. There has been some commentary on my “Great Rotation” themes. I’ll cite some of the examples in WTWA.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring the version from Investing.com. If you visit the original, you will see many interactive features, including the news events indicated on the chart.

The market gained 0.8% for the week, closing on the highs. The trading range was 1.4%. You can monitor volatility, implied volatility, and historical comparisons in my weekly Indicator Snapshot in the Quant Corner below.

Personal Note

Inspired by my travels, I have made a small change. I know that readers like the basic approach of WTWA. I am trying to do a bit more to emphasize important current investment themes and how to take advantage of what is happening. You might not have noticed the shift, but comments are welcome.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. The results remain positive in all time frames. NDD emphasizes that “…other forms of transportation, particularly trucking, have not confirmed the downturn in rail.

The Good

- NFIB Small Business Optimism improved slightly to 102.4 from September’s 101.8. This is off the post-election highs, but still elevated.

- Mortgage applications increased 9.6% for the week of 11/9. The prior week was a decline of 0.1%. We need a chart to put this series in perspective. The Daily Shot version illustrates the seasonality as well as the strength of 2019.

- Retail sales for October increased 0.3%, rebounding from September’s decline of 0.3% and beating expectations of a 0.2% increase. Retail sales ex-auto grew only 0.2% versus expectations of 0.4%, so the overall report was only moderately positive.

- The White House has no intention for a government shutdown. (The Hill, quoting Mnuchin).

- Heavy truck sales were up 3% year-over-year in October. (Calculated Risk).

- Market breadth has been good.

The Bad

-

Consumer prices increased 0.4%, higher than expectations of 0.3% and September’s unchanged reading. Core CPI of 0.2% was in line with expectations.

-

Producer prices for October also increased more than expectations, 0.4% versus 0.3%. September was unchanged.

-

Initial jobless claims increased to 225K, worse than expectations of 214K or last week’s 211K.

-

Industrial production for October declined 0.8%, worse than the expected -0.4% or September’s -0.3% (revised up slightly from -0.4%).

-

Newsletter writers are bullish. This is viewed as a contrarian indicator.

The Ugly

This group features some of the most popular commentators and frequent guests on financial television.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

The economic calendar is normal with an emphasis on housing data—housing starts, building permits, and existing home sales. Michigan sentiment and leading indicators both have a following. And of course, I expect some will be trying to squeeze some extra hints from the Fed minutes.

This news may not provide much competition for the political stories. That’s fine. Investors who pay attention to relevant data that is widely ignored have a solid edge. I am especially interested in building permits.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Despite the important economic news this week, I suspect that political issues will grab the spotlight. Since these matters are not (yet) important for investors, we have a week where we can choose a different topic. Instead of guessing what the punditry will talk about I want to emphasize a subject that is very important, but never quite gets the spotlight. We should be asking:

Is it time to worry about debt?

Many readers have asked about this topic. Most believe it is way past time to take it up. Even though the debt limit will probably be raised, let’s pick this week for a closer look at debt.

Background

Mounting debt is a staple subject for much of the punditry. The typical presentation includes an alarming chart.

The analysis often includes the following elements:

- No consideration of assets, which are a part of any entity’s balance sheet.

- A scale designed to increase the slope and avoid historic comparisons. This means chopping off the bottom part of the scale, shortening the time frame, and avoiding the use of a log scale (which would permit percentage changes at different times).

- The conclusion varies a bit. Some see imminent threats (Zero Hedge, Wolf Street, David Stockman and many featured in this week’s “ugly” section). Others like thought leader John Mauldin (who also has a savvy sense about how to play to investor worries) merely opine that it will all end badly. The Road to Default.

- The proposed solution is often the purchase of gold, annuities, or structured products.

It is an easy sell since it provides confirmation for the conventional wisdom. Why am I always stuck on the other side? (Mrs. OldProf assures me that this is OK. She adds that I am that way about everything. Hmm).

Worldwide Debt

The Visual Capitalist has an informative graphic showing both totals (in the overall size) and the relationship to GDP (via the color).

US Household Debt

Ben Carlson states the problem nicely.

If you want to get people worked up about the financial system the easiest thing to do is mention debt.

It could be U.S. national debt (clocking in at a whopping $23 trillion).

Student loan debt is, of course, another favorite that gets people worked up.

A new entrant into this game is auto loan debt. Just look at how big it’s gotten:

His key point is that those commenting often focus on whatever form of debt makes the case for fear. His entire analysis is great, but I especially like this chart, which puts the various debt types in perspective.

Bear in mind that mortgage debt is supported by collateral. The full posts shows the level of that support and the low rate of foreclosures, topics familiar to WTWA readers.

Corporate Debt

Oops! Those two scary charts are from three years ago. I really need a new research assistant! Let’s look at a current version.

That’s more like it! We now see the real credit cycle peak and potential recession, ignoring the “false peaks” in 2014, 2016, and 2017. This provides some insight into why the NBER waits for a significant pullback before identifying a peak.

There is a concern about high-yield loans and the potential for a run on the market. (Barron’s).

Margin Debt

Barry Ritholtz tweeted about his post from 2015 which did a nice job on bogus indicators. It included this annotated version of Doug Short’s margin debt chart. He accurately concluded that it was a coincident indicator without predictive power. That doesn’t stop it from resurfacing whenever the market makes new highs (which facilitates more margin debt).

A determined writer of the “reliably bearish” persuasion recently wrote that declining margin debt was also a negative indicator. Wow!

Government Debt

Here is the history of federal government debt, and how it would look if current policies continue.

State and local debt show a similar big rise, mostly starting with the Great Recession.

I’ll have some additional observations in today’s Final Thought.

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Long-term technicals have stabilized at neutral. Short-term technical health is a “soft” neutral. Recession risk has declined, but remains in the “watchful” area. There is little confirmation for the risk signals, which we have been monitoring since May. Many observers who reacted to the yield-curve inversion have become less worried.

Some readers have asked how my conclusion can be bullish when technical indicators are weak. The outlook is intended for investors. For them, the technical indicators are mostly useful to guide specific entry and exit pionts. An attractive equity risk premium and modest recession odds are the keys for investors.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis. With all of the recent data updates, it is time for a fresh look at the Big Four measures – those most important for determining recessions.

Guest Sources

Fourth quarter forecasts suggest a continuing slowdown. (James Picerno).

Sober Look (The Daily Shot) highlights the importance of two of our regular indicators.

There is a delay between a Fed rate cut and the impact on borrowers. (My personal observation is that there is no delay after an increase!)

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I try to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades described are certainly not suitable for everyone. The models have returned. We welcome my colleague Todd Hurlbut, Chief Investment Officer at Incline Investment Advisors, LLC. In our most recent post we invited readers to join us in considering whether sentiment was an important factor for traders.

Last week “Trending Todd” and the models joined me in Dallas for the National Association of Active Investment Managers (NAAIM) conference. One feature was the Shark Tank competition, expertly organized by David Moenning, Heritage Capital Research. Congratulations to the winners:

Stock Selection

Bill Davis, Managing Director, Stance Capital. His actively managed quant strategy uses only ESG large caps. He provided evidence on an advantage in both absolute and risk-adjusted returns. Bill is riding a key theme.

Tactical Stock Market Strategy

John Worthington and Jon A. Dauble of Dauble+Worthington Equity Portfolios. John pesented their “aggressive growth focused tactical sector rotation strategy.”

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely

Best of the Week

If I had to recommend a single, must-read article for this week, it would be, once again, Nick Maggiulli. I love his data driven approach. So frequently he explains problems that I am seeing in the popular interpretations of data. This week he writes N=1: On the Persistent Problem of Low Sample Size. He uses terrific examples to show how misinformation creeps into conventional wisdom. Did you know that the iron content of spinach was misstated by an order of magnitude in an early study? This led to Popeye’s wonder food and a 33% increase in spinach consumption. All of this from one study.

He carefully shows how decision making based on a single instance made sense for our ancestors. It is the difference between the statistical errors of Type I and Type II.

He proceeds to a series of anecdotal examples which have power as stories, but little statistical weight.

This all resonates strongly with me, especially after last week’s NAAIM conference. Our famous speaker explained that 7 out of 7 recessions had been preceded by an inverted yield curve. He further observed that the fact that the inversion had changed made no difference. The inverted curve lasted long enough for an accurate forecast of an upcoming recession.

Well! I politely pointed out that he had stated the numbers backwards. Stating that a result was always preceded by another variable is meaningless. My example was saying that all heroin users had smoked pot. In this case, the inverted curve had called for 10 recessions and we got 7. That might seem like a good batting average, but that misses the point. We have a small number of cases. There is a lot of variation among them.

I then asked about the inverted curve reversal. How many times had that happened? “Once” he responded. And on that occasion, there had later been another inversion.

Please think about this. So much of the “evidence” that you see or read is pseudo-statistics based upon inadequate data. I appreciate the fine explanation from Nick and his persuasive argument. It is confirming my thinking of course, but not confirmation bias. It is simply a well-established statistical principle that is often ignored in financial analysis.

Stock Ideas

Chuck Carnevale masterfully combines the role of forecasts and estimates in good decision-making with the example of 3M Company (MMM). Most critics of earnings estimates harp on inaccuracies. Chuck wisely observes:

We must recognize that the only thing certain about the future is uncertainty. Therefore, we must also accept that investing based on our best forecasts is not a game of perfect, nor does it need to be.

What’s with ROKU? Few understand how to analyze the TV streaming world. Perhaps not even knowing the true competitors for each company. Beth Kindig explains Roku is Choppy But Unshakeable Long Term. (Yes, I know her article would have been even more useful if I had not taken last week off. If you are interested, you’ll probably get an entry point. Meanwhile, you should follow Beth. Compare with the current Barron’s analysis of the group.

The housing sector (which I favor) is naturally sensitive to mortgage rates. “Davidson” (via Todd Sullivan) explains that Mortgage Lending Continues to Evolve. He discusses the false signal from the yield curve and recent changes in regulations on first-time homebuyers. His conclusion?

Should first-time home buying begin to accelerate, the positive impact for the US economy would be significant. Existing conditions remain on track for economic expansion as they have been since this cycle began in 2009.

Thinking about Mexico? I am. I love an investment idea that fits an emerging theme. MarketDesk is a new research firm with a great pedigree. They take note of the improving chances for a USMCA (NAFTA 2.0) proposal. (The Hill, quoting Pelosi).Their analysis is that “…passage would provide a significant boost to the Mexican economy in the form of increased business confidence.” This could also lead to more private fixed investment. Their report includes a more complete analysis of the investment and related risks (mostly a strong dollar). The obvious way to play this is the iShares Mexico ETF (EWW).

Barron’s suggests how retirement investors should approach dividend stocks. Lawrence C. Strauss compares total return and income approaches, taking special note of the risks in high-yield assets.

The Great Rotation

The great rotation has barely begun. In this section I will monitor the key shifts:

- To “value” stocks. We must keep in mind that value is defined in many ways.

David Templeton (HORAN) writes, This May Be The Time For Value Investors. His excellent post illustrates the recent move toward value stocks and the possibility of a continuing trend.

- To mid-cap and small-cap stocks.

- To emerging markets.

U.S. Stocks Just Won’t Deliver in the Next Decade, Report Says. It’s Time to Look Overseas.

To stocks benefiting from a cooling of the trade war. This group is often loosely and inaccurately “risk on.”

Watch out for…

Bond funds that misstate their portfolios. “…one or more of the bond mutual funds you own may be riskier than you think.” James Picerno reviews academic research on the topic.

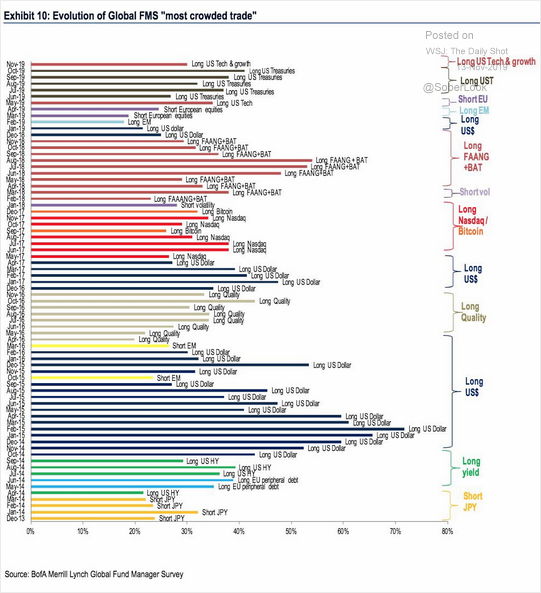

The most crowded trades.

Final Thought

How worried should we be about debt is a very tough question. Here are some partial conclusions:

- For investors, the growth rate of debt is more important than the total amount. (Mark Hulbert).

- Household debt, in total, is well within ability to pay and mostly supported by collateral. Student loans are an important and growing issue.

- Corporate debt is also mostly within the ability to pay or to refinance. The high-yield market is a potential problem.

- Government debt is a problem at all levels. Municipalities are selling or leasing assets. Some states are hopelessly behind on pension obligations. The Federal government is in the grip of powerful political forces: Constituents want more programs and lower taxes. Many incorrectly believe that this dilemma can be solved in a stroke by cutting waste, or foreign aid, or helping immigrants. A real solution requires entitlement reform. That means some bipartisan cooperation.

The implications for us as citizens relate to making our voices heard on taxing and spending at every level of government. Implications for investors are more nuanced. Here are my investment conclusions:

- The current overall debt level is not worrisome when viewed in terms of history and ability to pay. This is especially true for households.

- Investors should beware of high-yield corporate debt. I regard these investments as far less attractive than stocks, but so many are seduced by the coupon. You should also check your corporate bond fund or ETF to verify the holdings. One solution (which we follow) is to buy individual bonds as part of a ladder.

- Municipal debt does not currently offer much of a benefit versus taxable bonds. Be sure to calculate carefully using your own circumstances. State debt is also tricky, although some is supported by tolls or fees.

- Long-term government debt will someday be a problem, but not right now. Most of the bearish arguments made could have been advanced for twenty years. At the moment it is mostly the latest effort to scare you into poor investments and away from value stocks.

Readers might wish to compare my conclusions with the recent Fed assessment of risks.

Some asset values are high, the Fed noted, pointing in particular to commercial real estate values. But “risk appetite” was felt to be in line with “historical norms,” household debt “at a modest level relative to income,” leverage levels low among the largest banks, and the use of potentially volatile short-term funding posing only a modest risk to financial institutions.

But the report highlighted the Fed’s ongoing concern with record high levels of corporate debt, which some Fed officials worry could go bad if business slows and worsen any economic downturn. In addition, the Fed said low global borrowing costs could over time erode bank, insurance company, and pension fund returns, prompting them to take more risks.

Great Rotation Hints of the Week

Each week I will try to provide at least one idea for do-it-yourself investors to take advantage of the Great Rotation. My own approach is to take the four themes, apply criteria which my analytical team has helped me to develop, and purchase individual stocks. This will provide the greatest overall benefit and is not dependent upon any one of the four trends.

Some will not want to do so much work. You can get some of the benefit if you substitute Guggenheim’s S&P 500 Equal Weight ETF (RSP) for your holdings in the cap weighted versions. This is easy and could be very important.

Providing more choices and a great explanation of index issues is Jesse Felder, who writes The Easiest Way To Take Advantage Of The Generational Opportunity In Value.

He carefully describes the difference between fundamental indexes and the traditional passive approaches. There is too much weighting to over-valued equities. Investors are chasing growth and abandoning value. An important technical consideration is that some of the most attractive stocks have high insider ownership and lower float. These should be attractive but are instead underweighted. Read the full post to see several ideas about how to exploit this difference.

Successful investors are aware of important long-term issues, but cognizant of the immediate impacts. Popular “worry” articles are often distractions, not sound advice.

[Investors who are intrigued by the Great Rotation might want to apply for one of our portfolio analysis appointment openings. Just send an email request to info at inclineia dot com].

Some other items on my radar

I’m more worried about:

- Hong Kong protests and Chinese intervention. This is, of course, a possible human rights issue. It could easily become an investment issue if there is trade negotiation impact.

- Continued violence and murder in schools.

I’m less worried about

- Recession risk. Economic indicators have been stable in or a bit below the baseline growth level. If only we could get a little boost from the trade negotiations.

© NewArc Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All