Weighing the Week Ahead: All Eyes on Black Friday

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is loaded with data and we have a holiday-shortened week. In some circumstances the many economic reports and the Washington stories would dominate. This week the market and economic context suggests a different theme:

Will Black Friday results confirm consumer strength? Can this spark the typical Santa Claus rally, or should we expect (like last year) a big lump of coal?

Since there is no easy answer, the investment community will be watching closely for hints.

Last Week Recap

In my last installment of WTWA, I took advantage of a quiet calendar to ask whether we should be worrying about debt. I did not expect this to be a media favorite, but it never is. We must occasionally take up matters that are important beyond today’s trading! Readers seemed to enjoy the discussion and the format.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring the version from Investing.com. If you visit the original, you will see many interactive features, including the news events indicated on the chart.

The market lost 0.3% for the week. The trading range was only 1.2%. You can monitor volatility, implied volatility, and historical comparisons in my weekly Indicator Snapshot in the Quant Corner below.

Personal Note

Mrs. OldProf and I will be traveling over the next two weekends. I’ll try to do a weekly update if something dramatic is happening. We will be staying at the hotel where I was on the 16th floor during an earthquake. I had no idea what was happening. There was no alarm. It felt like a huge dog was bouncing on my bed. I did what any modern person would do: Sign into Twitter. I had my answer instantly – better than any news show.

I might try to dig up my presentation for the Money Show that year. It was well-received, but I wonder how many people cashed in on the ideas. Do-it-yourself investors are not natural contrarians. The process of reading and learning exposes them to an excessive level of good-sounding bad analysis.

Noteworthy

Great investors think ahead. If they own the right businesses, they worry little about the current opinion of Mr. Market. And yet, everyone worries about being “too early.” The Top 10 Emerging Technologies of 2019 provides some ideas that are more than just a dream, but still in the future. These are all fascinating developments.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. The results remain positive in all time frames. NDD also describes what to watch for. Currently this is the possible spread of weakness in manufacturing to the rest of the economy.

This analysis is in sharp contrast to those who look at the same list and select one choice to prove their point.

The Good

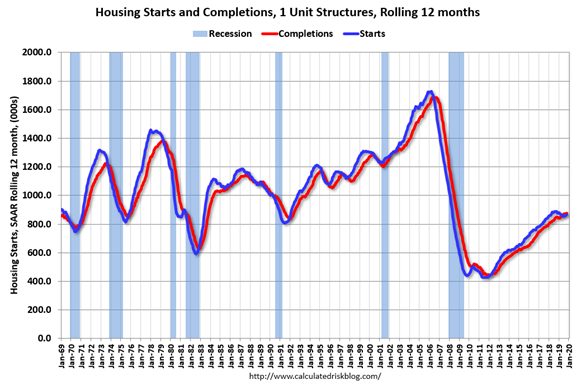

- Housing starts for October reached 1314K (SAAR) beating estimates of 1300K and September’s upwardly revised 1266K. Calculated Risk accurately predicted a “wide bottom” in the post-recession years. That has played out. Despite recent gains, there is plenty of room for more growth in housing.

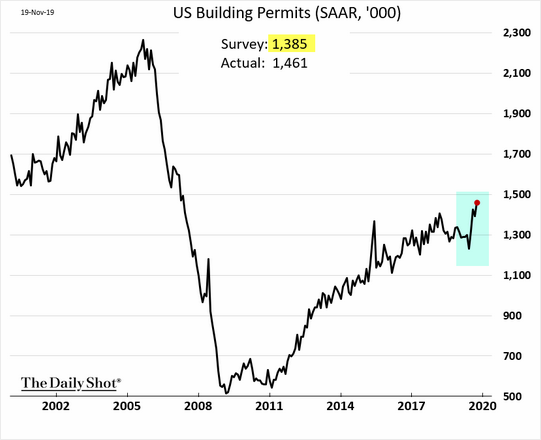

- Building permits for October were 1461K (SAAR) beating expectations of 1365K and September’s 1391K.

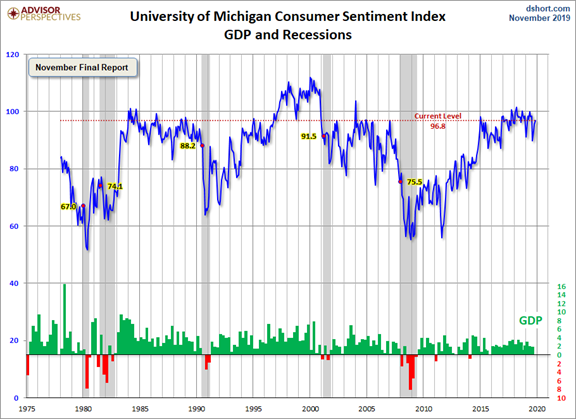

- Michigan sentiment for November recorded 96.8 beating expectations of 94.9 and October’s 95.5. Jill Mislinski has my favorite chart of this series. As always, she combines several key variables into one look.

The Bad

-

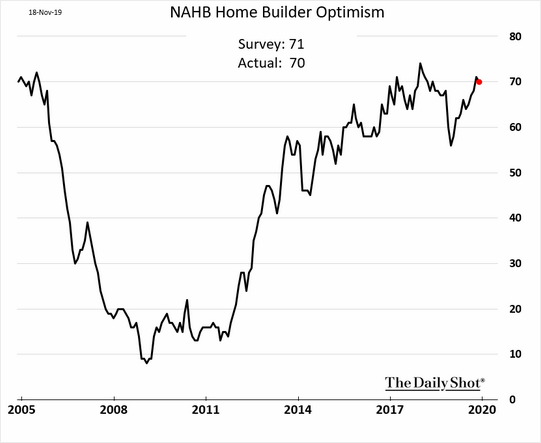

Homebuilder confidence down ticked to 70 missing both expectations and October’s reading of 71.

-

Mortgage applications declined 2.2% on the week after a prior week gain of 9.6%.

-

The USMCA deal hit a snag. It is less likely that an agreement will be reached before the end of the year. An incentive remains for both the White House (a signature accomplishment when one is needed) and the Democrats (proof that they can govern while pursuing impeachment). (Bloomberg)

-

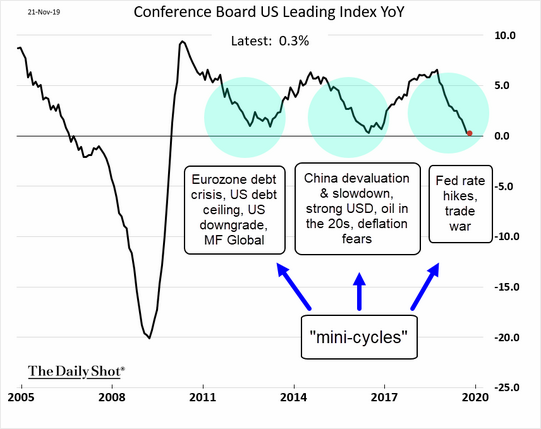

Conference Board leading indicators met expectations of a 0.1 decline, but it sustains a weak picture. The Daily Shot looks at the data in terms of three past “mini-cycles” and asks whether a fourth may be upon us.

-

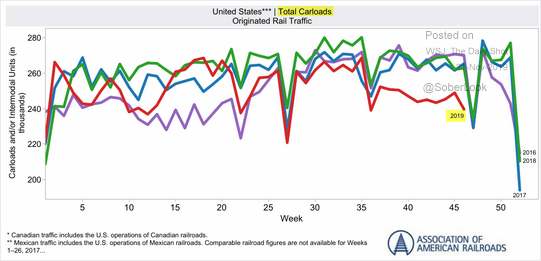

The rail decline continues, especially in the “economically intuitive sectors” closely monitored by Steven Hansen (GEI). Check out the full analysis to consider the data using multiple techniques. For comparison, The Daily Shot does a comparison of traffic by week for the last four years.

-

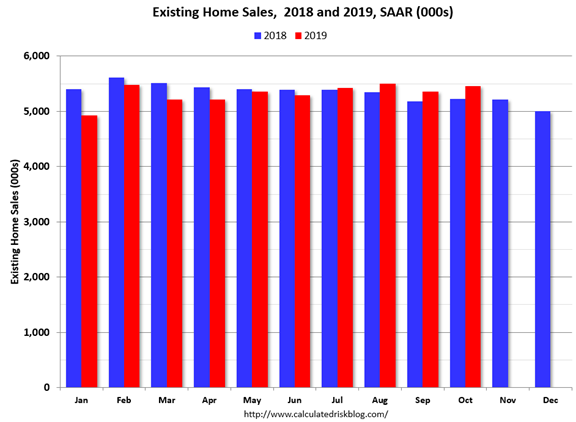

Existing home sales for October were 5.46M, slightly missing expectations of 5.5M but better than September’s 5.36M. I am scoring this as “bad” because of the slight miss in expectations. Calculated Risk is more upbeat, observing that sales were up 4.6% year-over-year, the fourth consecutive increase after 16 consecutive months of declines. Bill believes that easier comparisons will allow 2019 to beat 2018.

The Ugly

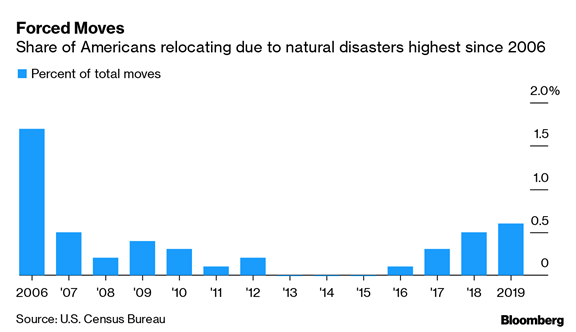

Forced relocations from natural disasters in the US. The level is at the highest pace since 2006 (Katrina).

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

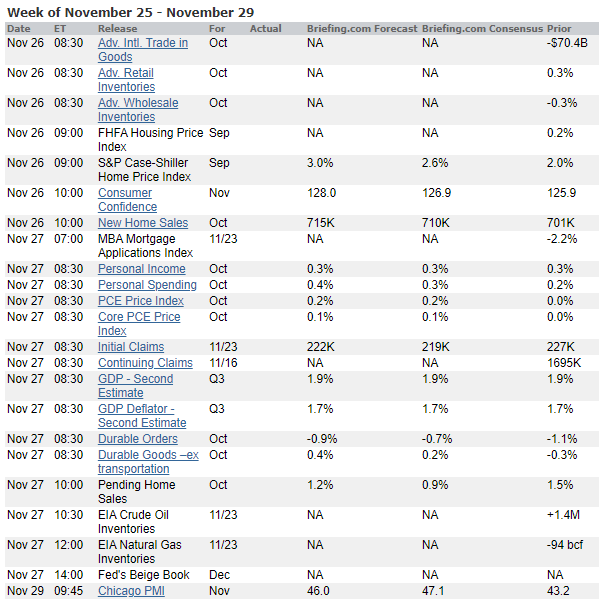

The Calendar

The economic calendar is huge and crammed into a holiday-shortened week. So much data, so little time. And I am not even counting the continuing stream of non-financial news.

Consumer confidence, new home sales, personal income and spending, the PCE price index, the update of the GDP estimate, and even the Beige book are all important. The Chicago PMI will catch some interest, although I expect market participants to go shopping soon after that Friday morning release.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Despite the many important economic reports, I expect a focus on Black Friday. Consumers are so important to the economy; all will be watching for hard data about current behavior. As usual with important data, many will exaggerate the result.

Will Black Friday results confirm consumer strength? Can this spark the typical Santa Claus rally, or should we expect (like last year) a big lump of coal?

Background

With the recent weakness in manufacturing data, remaining economic strength is consumer-based. Many wonder whether the weakness will spread to consumption, or the consumer strength will stimulate business investment. There is no good economic theory for such a question.

What to watch

The elements of consumption are like a murder mystery –means, motive and opportunity.

- The means is mostly a matter of personal income and spending.

And we mustn’t forget debt. From Dollars&Sense.

- Motive is fueled by a natural desire for consumer goods, but that is related to confidence. It might be confidence about the current economic conditions, but job prospects are also important. The confidence surveys do not usually show a great correlation with stocks. Will it be different when consumers are so important?

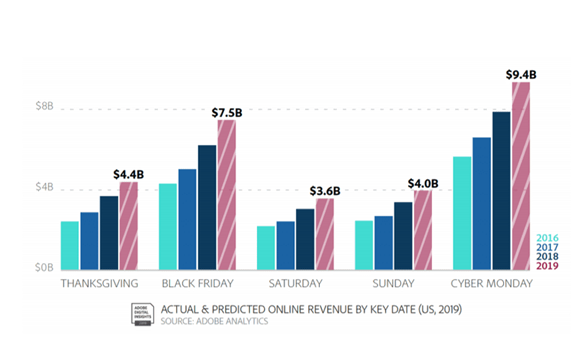

- Opportunity to buy things is always there, of course. Black Friday makes it more attractive (low prices) and easier (especially online). The AppInstitute has a good analysis of the data, including some great graphics and tips for sellers. For investors, here is the key chart:

What will be the market reaction to a good sales weekend? Investing.com considers the pluses and minuses. Most of the negatives from last year are missing, but there are other new worries.

I’ll have some additional observations in today’s Final Thought.

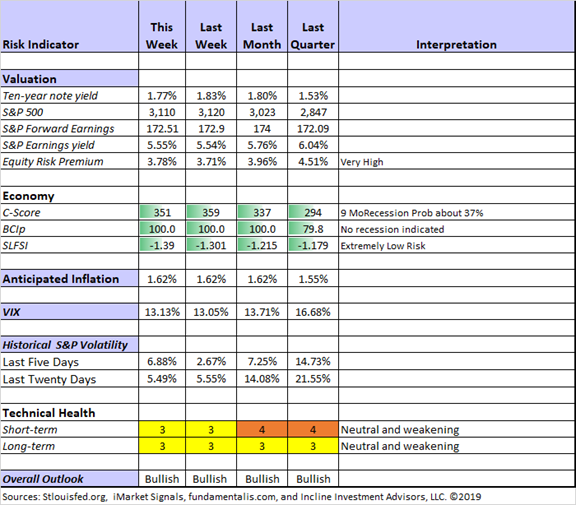

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Both long-term and short-term technical indicators remain neutral, but are weakening. I use this information to assist in entries and exits planned for other reasons.

Recession risk has declined, but remains in the “watchful” area. There is little confirmation for the risk signals, which we have been monitoring since May. Many observers who reacted to the yield-curve inversion have become less worried.

Some readers have asked how my conclusion can be bullish when technical indicators are weak. The outlook is intended for investors. For them, the technical indicators are mostly useful to guide specific entry and exit pionts. An attractive equity risk premium and modest recession odds are the keys for investors.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Guest Sources

Here is a great post explaining an important concept: Likely plus likely equals very likely. Please read this excellent summary and synthesis of how people consider probability.

Specifically, if people are confronted with two assessments of an event expressed as numerical probabilities (e.g. 50% and 60%), then they aggregate this information by averaging the probabilities (i.e. they conclude that the probability of the event is 55%). This works for probabilities above and below 50%, and independent of how the probabilities are conveyed (simultaneously or one after the other). In short, people deal with numerical probabilities as if they were generated independently and average them out.

But if the same probabilities are presented as words instead of numbers, something different happens. If people meet two experts (e.g. financial advisers) who both tell them that an event is “likely”, they afterward conclude that the event must be “very likely”. Instead of averaging between the two expert opinions, they add them up and get more confident in a certain outcome. This effect leads people to make more extreme forecasts and become overconfident in those forecasts.

[Jeff – It might be even worse. When the NY Fed’s recession probability model reached 30%, Art Cashin reported that those on the NYSE floor inferred a much higher estimate. Why? Whenever it had hit 30 in the past, there had eventually been a recession!]

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I try to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades described are certainly not suitable for everyone. We welcome my colleague Todd Hurlbut, Chief Investment Officer at Incline Investment Advisors, LLC. In our most recent post we examined the popular problem of losing money on a trade that was theoretically sound. As usual, we include some ideas from the trading models, using several different styles.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely

Best of the Week

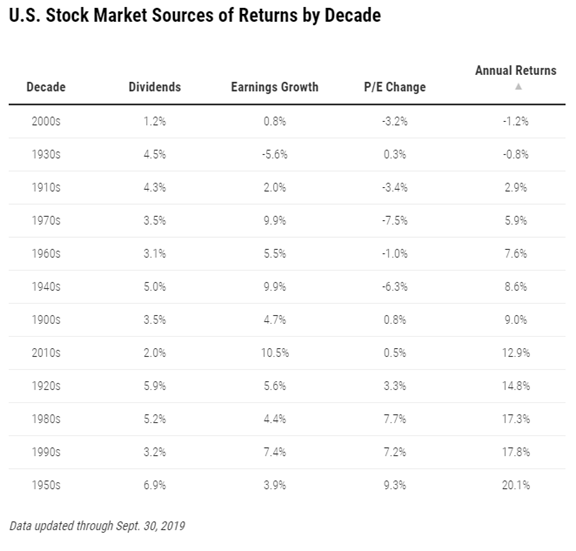

If I had to recommend a single, must-read article for this week, it would be Ben Carlson’s explanation of why the last decade has been so good for stocks. Here is his key theme:

…we’ll likely see a decade where stocks were up 9 out of 10 years, for a total gain well in excess of 200%.

But the naysayers are quick to point out this stock market rally is a house of cards, built on the back of money printing by the Fed, stock buybacks from corporations, low-interest rates, and multiple expansion. Many have pointed to the idea that the stock market has gotten ahead of the underlying fundamentals of American business.

When you look at the data, however, this decade’s performance is being almost exclusively driven by the fundamentals, much to the chagrin of perma-bears who blame everything that’s happened on the Fed.

He cites a simple formula from the late Jack Bogle: Market Returns = Dividend Yield + Earnings Growth +/- Changes in the P/E Ratio.

Here’s how the formula looks over several decades.

His conclusions from the table?

Shockingly, a vast majority of the gains over the past decade can be explained almost exclusively by improving fundamentals. Earnings growth and dividends explain nearly 97% of the annual returns for the 2010s. So the change in valuations have played a minor role in explaining the gains during this cycle.

[Jeff – I don’t find it shocking at all. Now I really do need to find some charts from my 2014 presentation. The emphasis on the Fed has been driven by those who have been completely wrong about the economy and market valuations. They needed some explanation, and blaming the Fed resonates.]

Stock Ideas

Barron’s analyzes the new, growth-oriented approach for Pfizer (PFE).

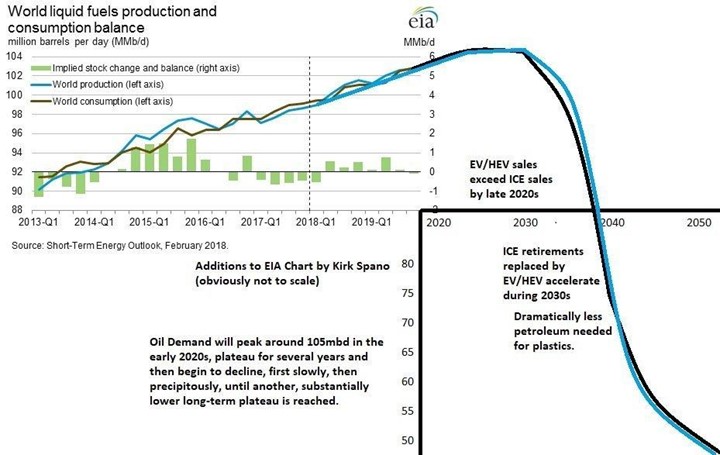

Energy Stocks? There are several good takes this week.

Kirk Spano warns that “peak oil” may finally be on the schedule. He does some tweaking of the EIA chart to illustrate what he expects. Read the entire well-sourced article for background on the sector.

Chevron: 4% Dividend Yield And New Projects Fueling Long-Term Growth

Check out the argument about the company’s growth prospects.

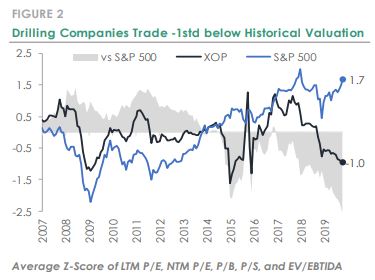

Market Desk’s Friday Strategist report takes a shorter time frame, expecting a closer match in supply and demand. Their conclusion? Look to the capital-intensive oil drilling sector (not gas). The report also notes the effect of improved pipeline capacity. And of course, their solid work also analyzes key risks.

Investors that prefer to buy single name stocks rather than ETFs should use XOP as a starting point. In our view, oil is more attractive than natural gas because gas is experiencing excess supply capacity that’s pressuring prices. From a regional perspective, the Permian Basin continues to be the top performing U.S. shale region.

Want Yield?

The Stanford Chemist updates his analysis of the Closed End Fund universe, citing those with the highest discounts and best coverage.

Double Dividend Stocks highlights two choices with yield in the 7-8% range and also insider buying.

The Great Rotation

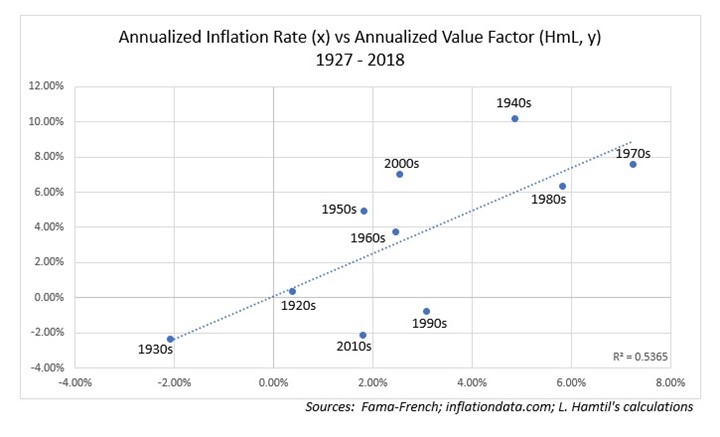

How Inflation Makes the ‘Value’ Factor a Sector Bet

(HT Eddy)

The complete analysis is well worth reading and you will enjoy the other charts. Here is a key point in the reasoning.

Now, the question remains, of course: why would inflation help value stocks? For William Bernstein, the explanation lay in inflation’s impact on growth stocks’ earnings. Earnings for growth stocks are typically forecast well out into the future, and rarely if ever catch up to those of more mature ‘value’ companies. Inflationary pressures compound this problem, as the future earnings streams on which the growth investor counts are eaten away. Inflation impacts the earnings forecast of value stocks, too, but the impact is much higher for growth stocks, as their valuations are much more reliant on future earnings.

James Picerno observes, US Small-Cap Stocks Continue To Trail Large Caps In 2019.

Watch out for…

Exxon Mobil (XOM). Don’t Chase the Wrong Yield, opines Stone Fox Capital.

Bond risk. Barron’s points out that a 50 bp increase in the ten-year Treasury note implies a 4% decline in price.

Final Thought

I will join in watching the Black Friday reports. I have no special insight on the consumer, but my research leads me to two themes that I have mentioned in past WTWA editions.

- I continue to love homebuilding stocks – mortgage rates, demographic trends, inventory, and changing behavior by the builders.

- Consumer cyclical stocks play nicely into my Great Rotation theme.

Market Outlook

From Eddy Elfenbein, his typically clear focus on a key issue:

“The whole problem with the world is that fools and fanatics are always so certain of themselves, and wiser people so full of doubts.” – Bertrand Russell

So true, Berty. Consider this scenario: If someone told you that come November, there would be impeachment hearings in Congress, and violent street demonstrations in Chile, Iran and Hong Kong, what would the stock market be doing?

But many individual investors are missing out persuaded by Bearish Forecasts Still Not Backed By Actual Data. “Davidson” (via Todd Sullivan) explains the problem: market psychology drives prices after economic trends, events and corporate earnings become media headlines. Market psychology lags existing conditions only once they become known. Psychology does not forecast.

My own theory about the year-end rallies relates to the switch in focus to next year’s earnings. This analyst tendency makes no sense, but we see it every year. It is better to always look twelve months ahead if you want a yearly time frame. Why be driven by the calendar. Since next year’s expectations have been falling a bit (Brian Gilmartin is all over this story), we might not see the normal reaction.

With weakness in technical indicators as well, I am patiently deploying new funds into my Great Rotation themes.

Great Rotation Hint of the Week

Each week I will try to provide at least one idea for do-it-yourself investors to take advantage of the Great Rotation. My own approach is to take the four themes, apply criteria which my analytical team has helped me to develop, and purchase individual stocks. This will provide the greatest overall benefit and is not dependent upon any one of the four trends.

This week’s suggestion is that you look for stocks that fit more than one of the themes. You might find an ETF that supposedly fits a theme. You might also look at the top holdings of some “value” investors.

Successful investors look ahead, finding emerging trends. What worked last year is old news and usually a contrary indicator.

[Investors who are interested in housing stocks might want to request my free spotlight paper on this topic. Those intrigued by the Great Rotation might want to apply for one of our portfolio analysis appointment openings. Just send an email request to info at inclineia dot com].

Some other items on my radar

I’m more worried about:

- Hong Kong protests and Chinese intervention. And now, a controversy over a US role. This could easily become an investment issue if there is trade negotiation impact.

- The USMCA negotiations.

- Brexit.

I’m less worried about

- Impeachment news. The story is not getting much traction with the electorate and even less with the market. This is what I predicted months ago.

- US/China trade progress. There is a new meaningless story every day and the DJIA moves 100 points. It is just normal posturing.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All