The Fed’s policy statement, the revised dot plot, and Chair Powell’s press conference reaffirmed expectations that monetary policy will remain on hold for the foreseeable future. That doesn’t mean that rates won’t be changed. The Fed stands ready to provide further accommodation if conditions warrant. However, the hurdle for a rate increase appears to be relatively high.

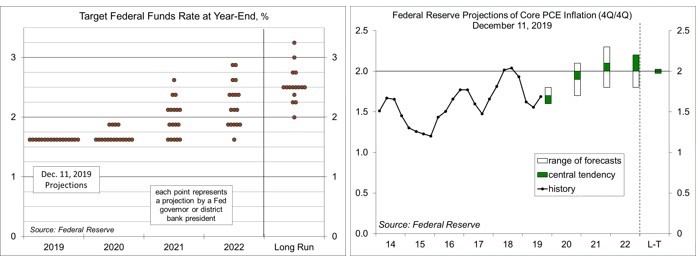

At every other Fed policy meeting (four times per year), senior Fed officials (the governors and 12 district bank presidents) submit projections of growth, unemployment, and inflation. Officials generally expect GDP growth to be in the 2.0-2.2% range for 2020 (4Q/4Q), with a median forecast of 2%. That seems a little optimistic, but is not out of the question. Labor market constraints are likely to become more binding and labor force growth should be slow (to about 0.5% per year given the demographics and limitations on legal immigration). Of course, the central bank would be the first to admit that there could be a lot more slack in the labor market. Fed officials misjudged the tightness in labor market conditions as they raised rates in 2018 (although by most accounts, monetary policy remained accommodative even after the December 2018 hike). In normal circumstances, the unemployment rate understates the strength of the labor market when conditions are strong (as those on the sidelines, not officially counted as “unemployed,” are drawn back into the labor force) and understates the weakness when conditions are weak (as individuals drop out of the workforce and are no longer considered “unemployed”). The unemployment rate has come to be viewed as a less reliable measure of labor market slack. One can get around the participation issue by looking at the employment/population ratio, which for the 25-54 year cohort is currently back to where it was before the recession.

While wage pressures have picked up, they remain generally moderate. That could change, but until it does, there is likely to be limited upward pressure on inflation. While Chair Powell spoke against the Fed adopting a make-up policy for inflation, he appeared reluctant to raise short-term rates until the Fed reaches its 2% goal. This is a change, as the Fed has long believed that if the Fed waited for higher inflation to show up, it would be too late to prevent it from rising further. In other words, the policy of preemptive tightening ahead of inflation appears to be out the window.

Click here to enlarge

While the Fed appears to be somewhat optimistic about the prospects for growth in 2020, the central bank still sees downside risks. Slower global growth and trade policy uncertainty dampened growth in 2019 and inflation pressures were unexpectedly muted. The truce in trade tensions is welcome, helping to reduce the downside risks to growth in 2020, but a lot of damage may have already been done. Import and export decisions do not turn on a dime, and more work needs to be done. Trade policy has generally been “one step forward, two steps back,” but the focus should be on reducing impediments to growth in an election year.

We ought to see the global economy pick up in 2020. Brexit may generate some turmoil, but simply removing the uncertainty would be a plus. Emerging economies should be helped by the Fed’s three rate cuts.

The Fed can be patient in deciding its next move, but we’re unlikely to see any changes through the first half of 2020.

Data Recap – There were no surprises in the Fed’s policy decision, statement, or projections. The long-awaited trade truce materialized ahead of the tariff increase that had been set for December 15. The house headed toward impeaching the president, but few see any chance that the Senate will vote to remove Trump from office. On the data front, consumer price figures were largely in line with expectations, but retail sales results for November were mildly disappointing.

As anticipated, the U.S. and China reached a Phase 1 Trade Deal, effectively a trade truce. Tariffs on $160 billion in Chinese goods, set for December, will not be levied. China agreed to buy more U.S. farm products (back to levels before the trade dispute), but U.S. tariffs on the bulk of Chinese goods were not rolled back. The 25% tariffs on $250 billion in Chinese goods remains (contrary to earlier press reports).

Along party lines, the House Judiciary Committee approved two articles of Impeachment on President Trump.

The Federal Open Market Committee left short-term interest rates unchanged. The wording of the policy statement was nearly identical from the one from October 30. The FOMC indicated that “the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee's symmetric 2 percent objective.”

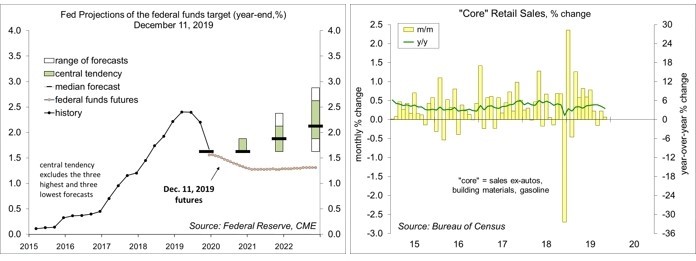

In its Summary of Economic Projections, forecasts of growth, unemployment, and inflation were about the same as those made in September. In the revised dot plot, 13 of the 17 senior Fed officials expect no change in rate in 2020.

In his post-FOMC press conference, Fed Chair Powell said that “our outlook remains a favorable one despite global developments and ongoing risks.” Over the last year, “the economy faced some important challenges from weaker global growth and trade developments.” In addition, “inflation pressures were unexpectedly muted, strengthening the case for a more supportive stance of policy.”

Click here to enlarge

Retail Sales rose 0.2% in the initial estimate for November (+3.3% y/y), with mixed revisions to September (lower) and October (higher). Motor vehicle sales rose 0.5% (+4.9% y/y). Ex-autos, sales edged up 0.1% (+3.0% y/y), also with mixed revisions. Gasoline sales rose 0.7% (+0.5% y/ y), reflecting an uptick in prices (+1.1% m/m, -1.2% y/y). Sales of building materials were flat (-9.1% before seasonal adjustment, +0.4% y/y). Ex-autos, building materials, and gasoline, sales edged up 0.1% (+3.5% y/y). Department store sales fell 0.6% (-7.2% y/y), while non-store retail sales (including internet shopping) rose 0.8% (+11.5% y/y). Sales at restaurants and bars fell 0.3% (+5.1% y/y). Note that the seasonal adjustment accounts for the late Thanksgiving, but it’s difficult to get that right)

Business Inventories rose 0.2% in October (+3.1% y/y), about as expected. Business sales slipped 0.1% (-0.1% y/y).

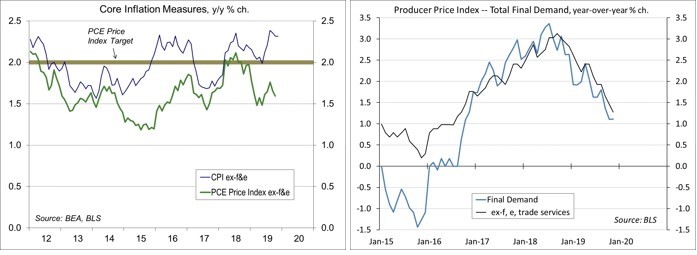

The Consumer Price Index rose 0.3% in November (+2.1% y/y). Food rose 0.1% (+2.0% y/y), mixed over the last year (food at home up 1.0% y/ y, food away from home up 3.2% y/y). Gasoline (4.0% of the overall CPI) rose 1.1% (-1.1% before seasonal adjustment, and -1.2% y/y). Ex-food & energy, the CPI rose 0.2% (+2.3% y/y). Note that the year-over-year increase in the core PCE Price Index has been trending 0.6-0.7 percentage point below the CPI y/y in the last couple of months. Ex-food & energy, prices of consumer goods were flat (+0.1% y/y). Non-energy services rose 0.3% (+3.0% y/y).

Real Hourly Earnings were flat for the third consecutive month in November (+1.1%). For production workers, real hourly earnings edged up 0.1%, following a 0.1% decline in October (+1.7% y/y). The slower trend (which is not the only factor in consumer spending) implies more sluggish growth in purchasing power in the near term.

Click here to enlarge

The Producer Price Index was unchanged in November (+1.1% y/y). Food rose 1.1% (following a 1.3% rise in October), reflecting gains in eggs (+76.6%), beef (+5.4%) and pork (also +5.4%). Wholesale gasoline prices rose 2.3% (-1.9% before seasonal adjustment, -3.7% y/y). Trade services (which measure changes in margins received by wholesalers and retailers) fell 0.6% (+1.4% y/y). Transportation and warehousing services fell 0.3% (-0.4% y/y). Ex-food, energy, and trade services, the PPI was flat (+1.3% y/y).

Import Prices rose 0.2% in November (-1.3% y/y), boosted by a 38.2% jump in natural gas prices (which account for just 0.4% of the headline index). Ex-food & fuels, import prices fell 0.1% (-1.3% y/y). These figures do not include import duties (tariffs). Ex-fuels, prices of imported supplies and materials were flat (-2.5% y/y), reflecting softness in global demand. Import prices for finished goods (capital equipment, motor vehicles, and consumer goods) showed no inflation pressure (but again, these figures don’t include tariffs).

Jobless Claims jumped to 252,000 in the first week of December, following a low 203,000 in the Thanksgiving week. This is just noise. Seasonal adjustment is difficult from November through February and the unadjusted figures appear to be in line with year ago data (accounting for the late Thanksgiving).

Nonfarm Productivity fell at a 0.2% annual rate in the revised estimate for 3Q19 (vs. -0.3% in the preliminary estimate, +1.5% y/y). Unit Labor Costs rose at a 2.5% pace (vs. +3.6% in the initial estimate, +2.2% y/y). Manufacturing productivity edged down at a -0.1% annual rate, with unit labor costs at a +3.0% pace (+4.4% y/y). For the nonfinancial corporate sector, productivity rose at a 3.0% annual rate (+1.7% y/y), with unit labor costs at a -0.6% pace (+1.7% y/y).

The Index of Small Business Optimism rose to 104.7 in November, vs. 102.4 in October. The general business outlook edged up (with an average of 12 in 2019, well below the 38 average reading from Dec-16 to Oct-18). The earnings trend poked above zero for the first time since August 2018. Hiring plans were moderate. Capital spending plans remained moderately strong.

As expected, the European Central Bank’s Governing Council left short-term interest rates unchanged. In her first meeting as ECB President, Christine Lagarde cited “continued muted inflation pressures and weak euro area growth dynamics,” although with “some initial signs of stabilization in the growth slowdown and of a mild increase in underlying inflation.”

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James