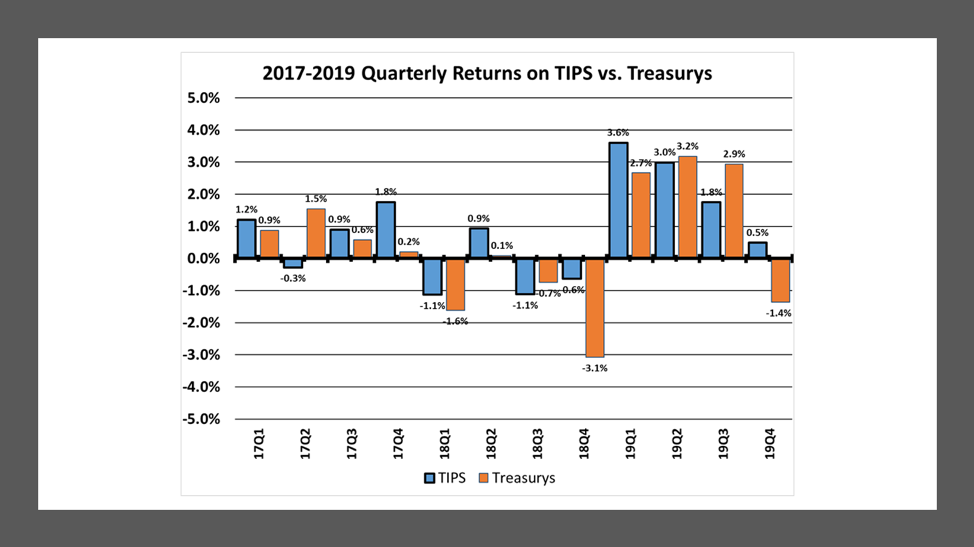

After underperforming for two consecutive quarters, TIPS posted a small gain of 0.5% in the 2019 fourth quarter, significantly outperforming comparable maturity straight Treasurys, which posted a decline of 1.4%.

That performance mirrored the trend in the equity markets, which bounced back first on the rumors and then on the news of a Phase 1 trade deal with China. Equity markets had essentially traded sideways with two modest corrections from the beginning of May to the end of September; but they took off in October on rumors of a pending trade deal.

At the same time, Treasury markets rallied and inflation expectations eased during the middle two quarters of the year, as investors worried about a weakening economic outlook. As those fears began to subside in the fourth quarter, investors sold straight Treasurys but continued to buy TIPS, driving Treasury yields up and TIPS yields down.

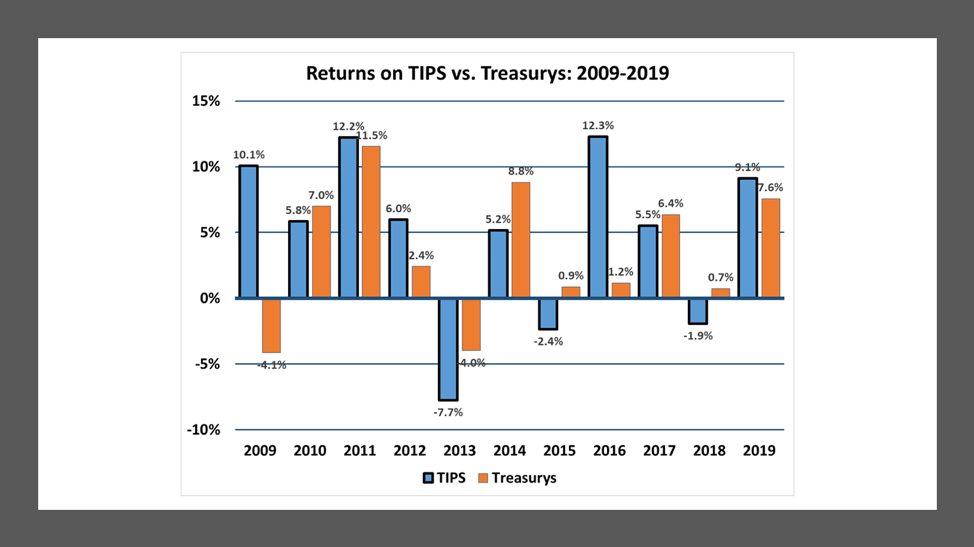

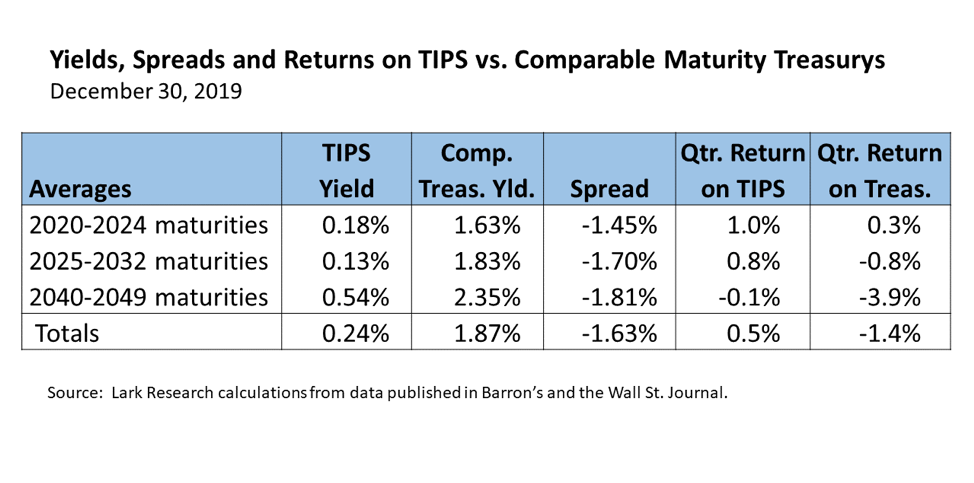

In 2019. TIPS outperformed Treasurys in the first and fourth quarters; while Treasurys outperformed TIPS in the second and third quarters. For all of 2019, TIPS earned a total return of 9.1%, which was 1.5 percentage points or 150 basis points (bps) better than the 7.6% total return on comparable maturity straight Treasurys. By my estimates, the 9.1% total return for TIPS included a yield of 1.3%, price appreciation of roughly 6.0% and an inflation adjustment of 1.8%. With the 6% of price appreciation, the average yield on TIPS, which is equivalent to the real rate of interest (i.e. excluding inflation) was just 0.24% at the end of 2019, down from 1.34% at the end of 2018.

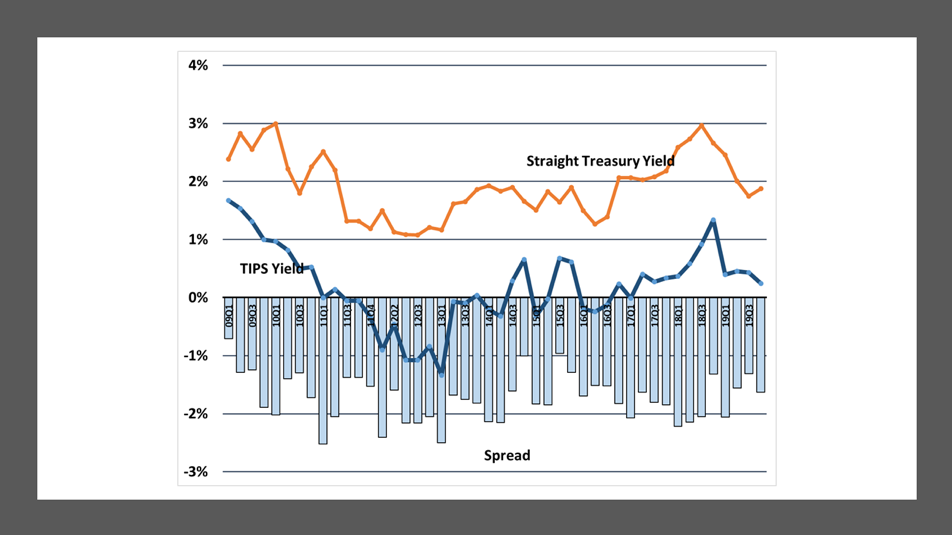

During the 2019 fourth quarter, the average TIPS yield declined 19 basis points (bps) from 0.43% to 0.24%; while the average yield on comparable maturity straight Treasurys increased 13 bp from 1.74% to 1.87%. With the change in yield, the average breakeven spread increased by 32 bp from 131 bp to 163 bp.

Since 2009, the breakeven spread has averaged 173 bp, according to my estimates, with a minimum of 71 bp and maximum of 252 bp. The minimum occurred during the height of the financial crisis in 2009 as TIPS yields surged higher, apparently because of forced selling by hedge funds. The maximum occurred in the 2011 first quarter, due to abnormally high demand for short-term TIPS, presumably in response to an expected pick-up in inflation. That buying drove short-term TIPS yields sharply negative.

The decline in the breakeven spread to 131 bp in the 2019 third quarter, well below the longer-term average of 171 bp, signaled that TIPS were cheap relative to comparable maturity straight Treasurys. When economic sentiment turned positive on the trade deal rumors, investors continued to buy TIPS even as they were selling straight Treasurys. This pushed the spread back up to 163 bp at the end of the year, which is still below the longer-term average.

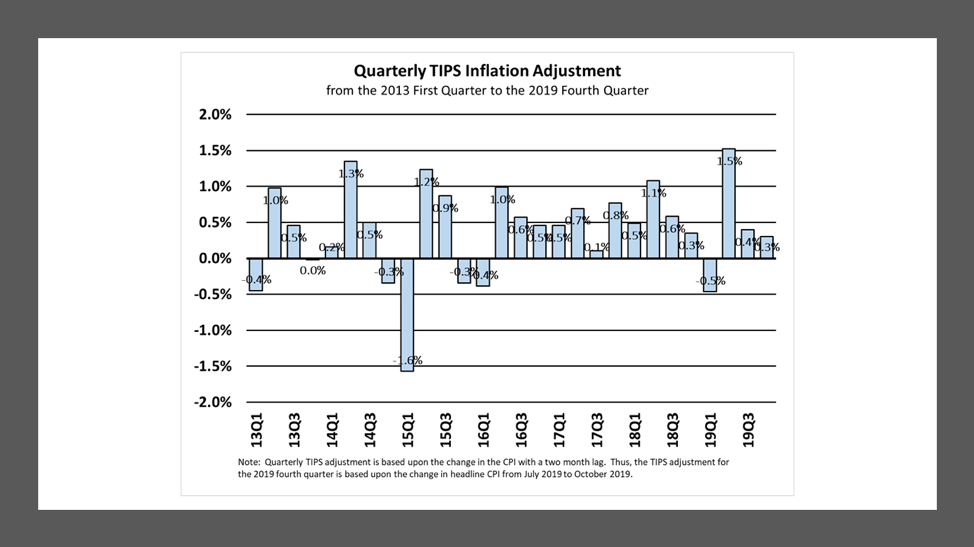

The 19Q4 returns on TIPS were bolstered by an average 30 bp kick from the inflation adjustment, equivalent to the year-over-year change in the headline Consumer Price Index (CPI) from July to October. Excluding the inflation adjustment, TIPS earned a total return (income plus price appreciation) of 0.2%. For the full year, the CPI-based inflation adjustment was 1.76%.

Performance varied across TIPS and Treasury maturities, as shown in the TIPS vs. Comparable Maturity Treasurys table above. Both short- and intermediate-term TIPS generated solid returns of 1.0% and 0.8%, respectively, in the 2019 fourth quarter. In contrast, straight Treasurys posted losses in the intermediate- and long-term maturities of 0.8% and 3.9%, respectively. Long-term TIPS and short-term Treasurys delivered essentially breakeven results in the quarter.

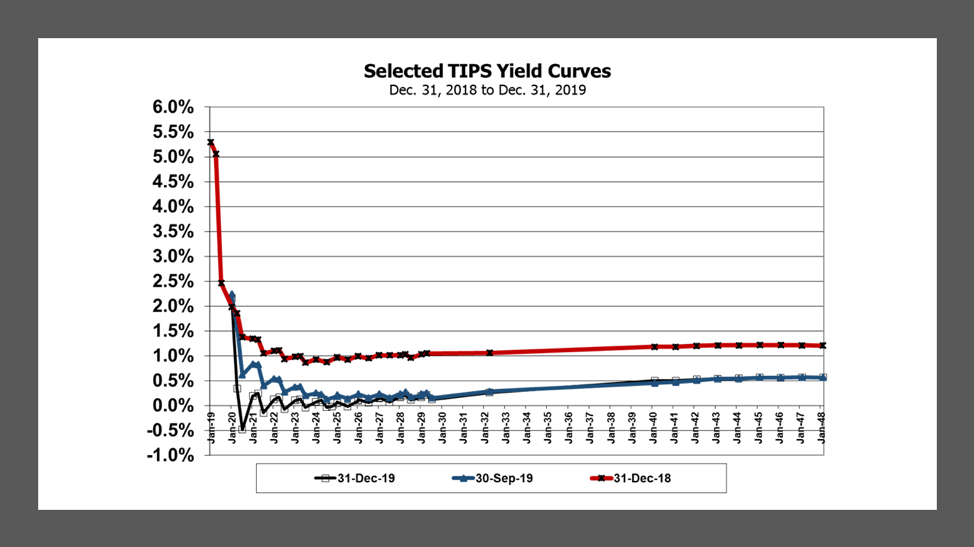

From the 2019 third quarter to the fourth quarter the TIPS yield curve shifted across the shorter maturities, which is suggestive of higher near-term inflation expectations. (Investors are willing to accept a lower yield on short-term securities presumably because they believe that they will obtain a greater inflation adjustment.) Yields across the intermediate- and long-term maturities were essentially unchanged.

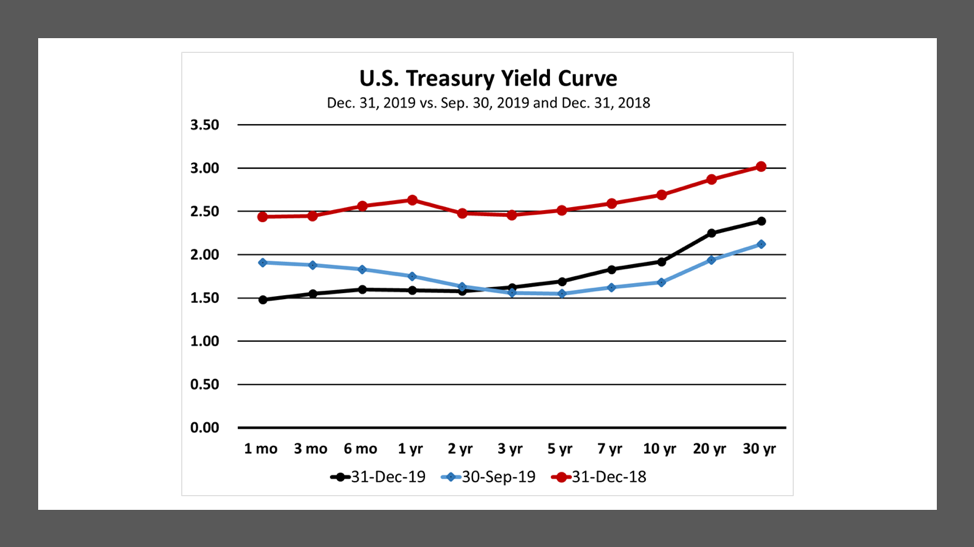

A similar shift is evident in the U.S. Treasury yield curve (as shown in the chart on the next page). The yield curve at Sept. 30, 2019 was inverted across the one-year to 10-year maturities, which reflected concerns about a coming economic slowdown, perhaps even a recession. As with the TIPS yield curve, the Treasury curve in the 2019 fourth quarter shifted down across the shortest maturities, mostly from one-month to one-year; but it also shifted up across the intermediate- and long-term maturities. Thus, the yield curve became upward sloping again in the fourth quarter as concerns about the economic outlook eased; but this shift across the long-end of the curve produced negative returns and was the primary cause of TIPS underperforming straight Treasurys during the quarter.

Relative strength in TIPS has accelerated into the New Year. The Financial Times reported yesterday that U.S. investors are seeking protection against inflation as the Federal Reserve considers letting consumer price inflation run above target for a period (so called “inflation averaging”) to escape the low growth, deflationary fates of Europe and Japan. That sentiment caused prices of intermediate-term TIPS to jump between two-thirds and a full point and long-term TIPS to surge roughly two-and-one-half points over the first three trading sessions of 2020. (Yesterday (Jan. 7), however, TIPS gave back about one-third of those gains in the stock market sell-off, which was precipitated by a U.S. drone strike that killed a top Iranian military commander.)

Several major fund managers say that they see TIPS as attractive because their breakeven spreads are below historical averages. For example, the average breakeven TIPS spread at the end of 2019 was 163 bp, according to my calculations, below the long-term historical average breakeven spread of 173 bp from 2009 to 2019. Long-term TIPS breakevens were 181 bp at the end of 2019, below their historical average of 203 bp. If inflation picks up, TIPS at these prices could be a solid investment, especially vs. straight Treasurys.

On an absolute basis, however, the average TIPS yield (i.e. the real rate of interest) of 24 bp at the end of 2019 suggests that TIPS are expensive. The low real interest rate leaves little room for interest rate volatility, which could cause real interest rates to rise. By comparison, TIPS yields averaged 200 basis points in the seven years preceding the 2009 financial crisis and 50 basis points since 2011.

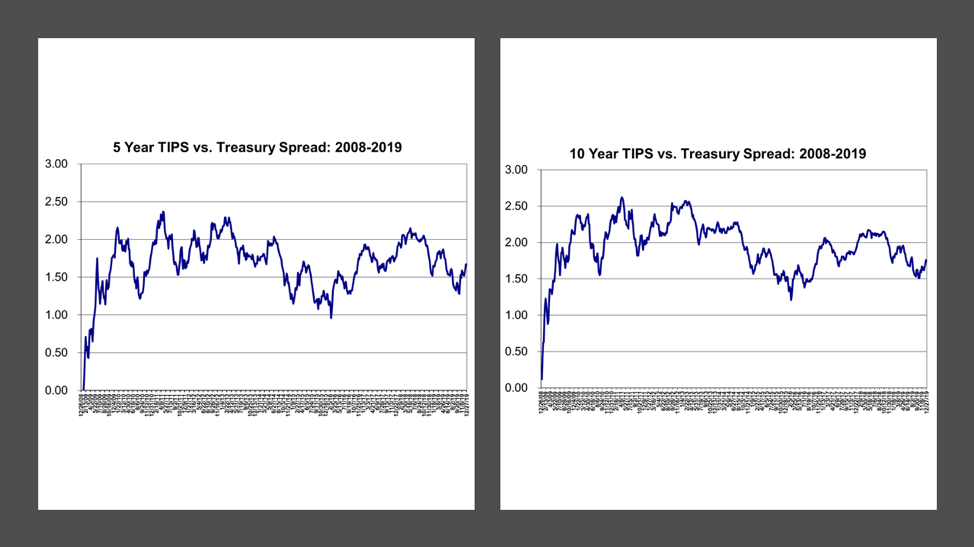

With real interest rates at such low levels, it is hard to imagine that TIPS can achieve the same level of price appreciation in 2020 as they achieved in 2019. In order for that to happen, the yield on TIPS, equal to the real rate of interest, would have to turn negative, as they did for a short stretch of time from 2011 to 2013 (shown in the table above).

From my perspective, real rates can turn negative for a sustained period of time under two scenarios (or perhaps a combination of these two scenarios): either inflation picks up above the Fed’s target range of 2% while yields on straight Treasurys remain essentially unchanged or inflation holds constant and straight Treasury yields move lower. The first scenario could occur under the Fed’s contemplated “inflation averaging” strategy, where it allows inflation to move its current 2% target range for some period of time in order to avoid a slowdown in the economy. The second scenario could occur if there is an economic slowdown and confidence in the long-term outlook for the U.S. economy and financial system is maintained. Of course, it is possible that inflation could rise and Treasury yields could fall at the same time, which would drive real yields even lower. President Trump has advocated a negative interest rate strategy for the U.S. in his Twitter commentaries on Federal Reserve policy.

Absent such a shift in real interest rates, TIPS look expensive, but they can still play a role in investor portfolios as a potential hedge against certain risks. Whether such anticipated hedges work as intended depends upon the trend in real interest rates. A long position in TIPS, especially in the longer maturity issues, is essentially a bet that real interest rates will not rise and inflation will exceed the current breakeven rate of 1.63% (average for all TIPS) or 1.81% (for long maturity TIPS).

January 8, 2020

Stephen P. Percoco

Lark Research

839 Dewitt Street

Linden, New Jersey 07036

(908) 448-2246

[email protected]

www.larkresearch.com

© Lark Research

Read more commentaries by Lark Research