A year ago, the baseline scenario for the economy was moderate growth, but with an elevated level on uncertainty, with risks skewed to the downside. Trade policy uncertainty and slower global growth were dampening factors, but Fed policy was supportive. Investors were willing to look beyond the uncertainty. This year, trade policy is still uncertain, but less so, and the global economy appears poised for improvement. However, there’s a Senate impeachment trial pending, it’s a presidential election year with many unfriendly market themes, and geopolitical tensions have just escalated.

Economic data reports were less market-moving in 2019, as investors focused on the trade policy and the Fed. On a day-to-day basis, stocks tended to rise on news suggesting progress on a trade deal and fell on news of an impasse. The Phase 1 deal with China halts the escalation in trade tensions, prevents the implementation of the final round of tariffs on Chinese goods (mostly consumer goods), and partly unwinds the round of tariffs imposed in September. However, the agreement falls far short of taking us back to where we were. Still, for the financial markets, the absence of bad news is good news.

A year ago, the Fed was expected to raise rates once or twice in 2019. The stock market declined in late 2018, but began to recover at the start of 2019 after Chair Powell said that the Fed was “listening carefully, with sensitivity to the message that the markets are sending and we’ll be taking those downside risks into account as we make policy going forward.” After the FOMC meeting in late January, Powell said that “the case for raising rates has weakened somewhat.” By the middle of last year, the policy outlook had shifted, but rather than signaling the start of a lengthy easing cycle, Powell called it a “mid-cycle adjustment.” The Fed still saw the federal funds target range below the natural rate (that is, below a “normal” level), but felt that it was important to provide insurance against the downside risks from slower global growth and trade policy uncertainty. After lowering short-term interest rates three times, the Fed left rates unchanged in December, believing that “the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation near the symmetric 2% objective”

– and the markets were okay with that. Monetary policy is expected to remain on hold in 2020, but the Fed will respond to a material change in the economic outlook should that occur.

Impeachment? Been there, done that. Stock market participants view the Trump impeachment as similar to the Clinton impeachment, in that there is little chance that two-thirds of the Senate will vote to remove the president from office. House Speaker Pelosi has not submitted charges to the Senate, presumably to let pressure build and possibly accumulate more charges if warranted. The Clinton impeachment came back to bite the Republicans, who lost seats in the midterm elections. Republicans are hoping for a similar blowback in 2020. However, there’s likely more of this drama to play out in the months ahead.

It’s only a few weeks until the Iowa caucus (February 3), then the New Hampshire primary, then the Nevada caucus, and then the South Carolina primary, with a Democratic frontrunner likely emerging by Super Tuesday (March 3, when 14 states will hold primaries). From there, it’s a long slog to the conventions in late August and the November 3 election. The themes for the Democrats are expected to center on universal healthcare, income inequality, monopoly/antitrust regulation, and climate change – things that “will cost money and must be paid for.” Financial markets have shown some sensitivity to discussions (in healthcare, for example), but investors seem to be little concerned overall. That may change depending on the polls.

Of course, there will be some surprises along the way in 2020. According to the old boxing adage, it’s the punch you don’t see that knocks you out. Equity evaluations are rich relative to earnings expectations. That’s not necessarily a problem as long as interest rates remain low (lower rates allow for higher P/E ratios). However, it may leave the market susceptible to shocks.

Department of Defense press release: “At the direction of the President, the U.S. military has taken decisive defensive action to protect U.S. personnel abroad by killing Qasem Soleimani, the head of the Islamic Revolutionary Guard Corps-Quds Force, a U.S.-designated Foreign Terrorist Organization.”

The killing of Soleimani is already an act of war according to many. The key questions are how Iran responds, and it will, and how the U.S. answers Iran’s response. While tensions between the U.S. and Iran were already high, this adds a whole other level of uncertainty to the mix for 2020.

Data Recap – Investor optimism remained strong in the first day of trading of 2020, but news that the U.S. military had assassinated an Iranian general sent share prices lower. The price of oil rose and bond yields fell in response to heightened uncertainty.

The FOMC Minutes from the December 10-11 policy meeting showed (no surprise) that Fed officials viewed the current stance of monetary policy as “appropriate,” although “if developments emerged that led to a material reassessment of the outlook, the stance of policy would need to adjust.” Sentiments expressed suggested a higher hurdle for rate increase in the future.

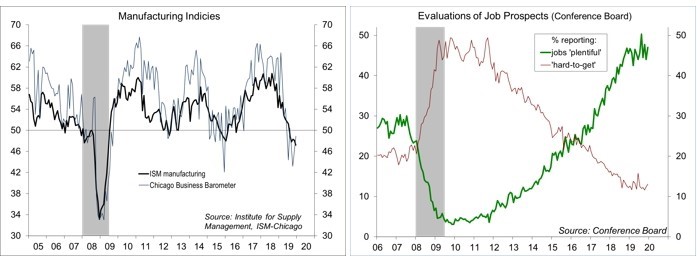

The ISM Manufacturing Index fell to 47.2 in December, vs. 48.1 in November. New orders, production, and employment contracted for the fifth consecutive month. Order backlogs fell for the eight month in a row (not a good sign). “Global trade remains the most significant cross-industry issue, but there are signs that several industry sectors will improve as a result of the phase-one trade agreement between the U.S. and China,” according to the report.

Click here to enlarge

The Conference Board’s Consumer Confidence Index edged down to 126.5 in the initial estimate for December, vs. 126.8 in November (revised from 125.5). Consumers’ assessments of current conditions improved, but their expectations declined, driven by a softening in the outlook regarding jobs and financial prospects. “While the economy hasn’t shown signs of further weakening, there is little to suggest that growth, and in particular consumer spending, will gain momentum in early 2020,” according to the report.

The Advance Economic Indicators report had mixed implications for 4Q19 GDP growth. The merchandise trade measure narrowed unexpectedly to $63.2 billion in November, vs. $66.8 billion in October, mostly on a drop in imports (which have a negative sign in the GDP calculation). Retail inventories fell 0.7% in November, with motor vehicle inventories down 1.6% (likely reflecting the effects of the GM strike). Slower inventory growth will subtract from 4Q19 GDP growth, while net exports are expected to add.

The Pending Home Sales Index rose 1.2% in November (+7.4% y/y). November results were mixed across the four regions, but each was higher than a year ago. Note that the index fell 20.5% before seasonal adjustment.

The Chicago Business Barometer rose to 48.8 in December, vs. 46.3 in November (it was the lowest quarterly average since 2Q09). The production index rose to the highest level since August, but remained in contraction. New orders and employment continued to contract.

Durable Goods Orders fell 2.0% in the advance estimate for November, reflecting a 72.2% plunge in defense aircraft orders (don’t read anything into that, these data are erratic). Ex-transportation, orders were flat, mixed across industries. Orders for nondefense capital goods ex-aircraft edged up 0.1%, while the total for the first 11 months of 2019 were up 0.7% from the same period in 2018.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

More Alternative Investments Topics >