2019

2019 was a very unusual year. Domestic growth whipsawed from strong (over 3%) to concerning (just over 1%). This volatility was compounded by both domestic and global headline factors: a very public trade dispute and very weak global growth. Policy was also in play. The Fed rotated from tightening, to neutral, to easing in the first 3-quarters of the year. Nominal rates moved up a little at the start of the year, but then dramatically declined for the first three quarters with the 10-year falling from 2.69% to 1.46% by the start of September. This low in intermediates coincided with a very modest 5 basis point (bps) inversion in the bellwether 2-year to 10-year yield curve measure. Around the same time, a significant repo market disruption occurred that the Fed countered with QE-like intervention. By year-end, the bulk of the economic growth scare had dissipated, the yield curve was more normalized, rates across the curve were lower by 80- 100 bps and risk markets had logged in some of the best returns over the past 10-years.

ECONOMY

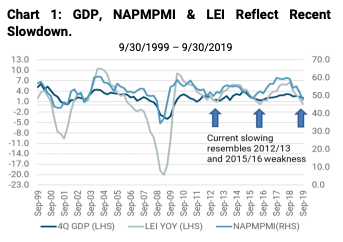

Chart 1 shows three measure of economic activity: Last twelve months (LTM) of quarterly Gross Domestic Product (GDP), the National Association of Purchasing Managers Purchasing Managers Index (NAPMPMI) and the Conference Board’s Leading Economic Index (LEI). The former tracks trailing domestic growth. The latter two indicators are more forward looking.

All three indicators reflected a slowing domestic economy. The material message from the PMI and LEI, however, is that while decelerating over the bulk of 2019, both indicators suggest that the domestic economy is no longer weakening. Indeed, the current readings are very similar to those we experienced at the bottom of the 2012/13 and 2015/16 growth slump periods. The biggest difference between 2019 and those previous periods is the focus and magnitude of weakness in the industrial and manufacturing sectors, recently amplified by the decline in the Purchasing Managers Index to a “Contracting” 47.2 reading on January 3rd. Comparing the current conditions to the previous two recessions supports our view that the current situation is slowdown, but not evidence of a lead up to recession. In both those cases, the LEI continued to weaken all the way through the point where GDP went negative. This is not the trend we are seeing today. Our view is that the Fed’s forecast of 2% growth in 2020 is potentially a little high in the nearterm, but broadly consistent with our assessment of approximately 2% growth for 2020. Any strength above that number will likely develop in the second half of 2020.

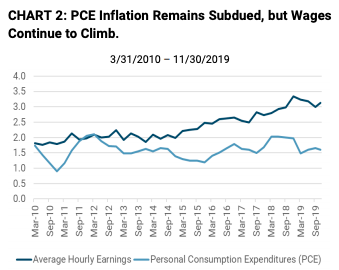

Chart 2 displays two important inflation measures over the past 10-years: Personal Consumption Expenditures (PCE) and Average Hourly Wages (AHW). Since consumer behavior represents roughly 2/3 of GDP in the US, the Fed is especially conscious of trends in personal consumption. This measure remains relatively well behaved under the Fed’s 2% inflation target. Wages, as represented here in AHW are a cause for concern.

Our view is that wage pressure will ultimately put upward pressure on prices, but that its effect will continue to be muted by productivity, global and technological substitution. As such, we regard inflation as a potential problem, but one that will more likely become evident in the face of synchronized global growth and reflation. As we witnessed in 2019, the market will undoubtedly extrapolate any surprises on the inflation side insofar as it might foreshadow a change in Fed behavior.

FEDERAL RESERVE

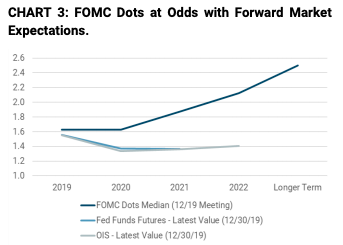

Chart 3 presents the median outlook by Federal Open Market Committee (FOMC) voting members for the Fed Funds target rate from the most recent FOMC meeting (Dot projections as of 12/11/19), Fed Funds Futures and the Overnight Indexed Swap rate. There are two observations about this chart that inform our view. First, the FOMC members expectations imply a relatively neutral Fed over the course of 2020. The second is that the Futures markets believe this neutral stance could include a modest rate cut in 2020. As of the end of December 2019, the market was discounting more than a 56% probability that Fed would cut rates.

Our view is that the Fed and the market expects a very modest amount of policy activity in 2020 and we think there is reason to be relatively cautious on this outlook. Accounting for all the factors that influence this view (e.g., growth, inflation, unemployment, etc.), we think there is a good chance that “not much happening” is probably unlikely. It’s instructive to remember that in December 2018, the market (as opposed to the Fed’s dot projections) was forecasting little change in overnight lending rates. The outcome was a 125 bps decline in overnight rates. Unless something exogenous develops, we view rates as vulnerable to a resumption in growth, especially from global activity and building labor related price pressures. We were surprised by magnitude of rate moves in the 2019. The current market is forecasting modest declines in the Fed Funds rate. We see both sides of the coin: higher rates due to a resumption in growth or lower rates due to an exogenous drag. We lean toward an expectation of higher rates, but we also think the prudent approach is to maintain a near benchmark duration in 2020, especially in the first six months of the year.

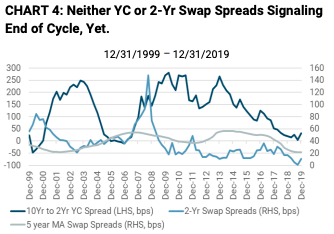

Chart 4 presents two indicators we view as end-of-cycle or recession tripwires: The 2-year to 10-year US Treasury yield curve (YC) slope and the spread between fixed and floating rate 2-year swaps. We have discussed both indicators in previous research pieces. Although this yield curve spread measure briefly inverted in September, it was neither material in magnitude nor persistent in duration as we have seen in previous periods in which the measure predicted a recession. In the case of swap spreads, this measure continues to show no stress in the financial system.

Taken together, we see these indicators as confirming our view that eminent contraction is not the horizon and that the current cycle will continue through 2020 (and possibly into 2021).

LENDING/CREDIT CHANNEL

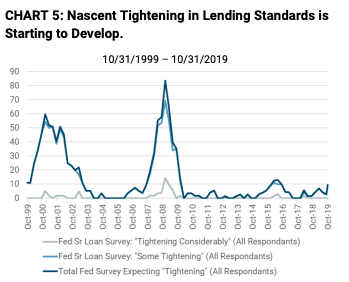

Some economic commentators have discussed the possibility of tightening lending standards as a cause for concern in the current market. At this point in the previous two expansions, that would be an appropriate expectation. However, the fundamentals of the current cycle are somewhat different from the last two cycles. Namely, the Dodd-Frank reforms implemented in the aftermath of the Global Financial Crisis have eliminated much of the fragility of the financial system that existed in those prior periods. Whether it is bank balance sheets and/or lending practices, the current financial system much more conservatively positioned compared with the previous periods. Chart 5 presents a portion of the Fed’s Senior Loan Officer Survey, specifically the percentage of firms reporting some level (Some Tightening or Tightening Considerably) of credit standard tightening. Like the two previous slowdowns in the current cycle (2012/13 and 2015/16), we are seeing a pick-up in “Some Tightening”, but at this juncture it remains relatively modest and consistent with normal ebbs and flows of credit creation. Our view is that much of the current credit tightening activity is targeted at sectors that have undergone significant upheaval (Energy, Retail) or are related to specific initiatives (ESG-related issues) or litigation (Opioid litigation).

DEFAULTS

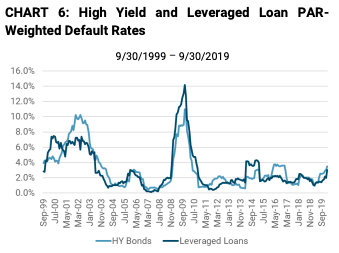

Chart 6 shows Par-weighted default rates for high yield bonds and leveraged loans. Over the past 20 years, the Par-weighted default rate for both asset classes averaged just over 3.0%. As of December 2019, bonds and loans have experienced last 12-month Parweighted default rates of 2.6% and 1.6%, respectively. The biggest contributor to the recent rise in default rates have been mainly Energy related bankruptcies or restructurings (40% of all defaults/recaps in 2019). Telecommunications (9.1%), Metals/Mining (8.4%) and Diversified Media (6.8%) round out the top four sectors impacted by defaults in 2019. The individual sector level default rates are especially meaningful. For example, the sector level default rate for the Energy sector was 12% in 2019, up from a little over 3% in 2018 but still below the peak of over 14% in 2015.

Our view is that slow, but still clearly positive economic growth will make broad default rates muted somewhere at or slightly above current levels in 2020. We think leveraged loan default rates probably have more room to move upward in 2020 compared to bonds. Of the problem sectors that are undergoing the most creative destruction (Energy, Retail, Fixed-line telephony), we view the first half of 2020 as the most trying period, especially for a few large Energy issuers that could end up filing in this year. There are also a few sectors that are especially vulnerable to litigation (Pharma) or access to lending (ESG-related), that could find challenges in 2020 as they try to refinance their debt.

SUPPLY, DEMAND AND THE SUPPLY DEFICIT/SURPLUS

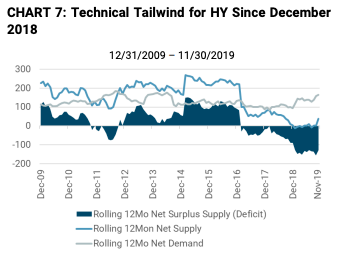

Chart 7 portrays the flows into and out of the high yield market that dimension the technical posture of the marketplace. Total Net Supply considers gross issuance, calls, tenders, maturities and fallen angles to arrive at a net amount of new high yield paper that enters the market during any month. Total Demand includes rising stars, coupon reinvestment and mutual fund flows on the same monthly basis. A Supply Surplus describes a condition where observable supply estimates exceed observable demand estimates. A Supply Deficit describes the opposite.

What is interesting to observe from Chart 7 is that the high yield market has been experiencing a protracted period of Supply Deficit over 2018. This is a somewhat unusual case across the ten-year horizon on the chart. In classical economic terms this period of excess demand would be expected to produce a tailwind for valuations in the sector.

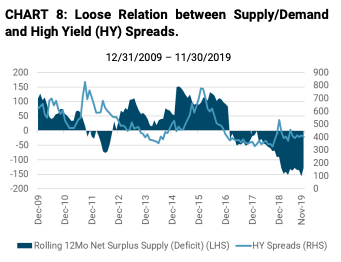

Chart 8 compares the rolling 12-month Supply Surplus or Deficit against spreads over government high yield bonds for the broad high yield market to evaluate the linkage between this technical estimate of a supply/ demand imbalance and a typical valuation metric.

At best, we find only a loose relationship between our measure of supply/demand and spreads. What we conclude is that this technical picture of the market is only a partial view of the overall high yield market. In the early days of high yield when outside investors were few and access was highly specialized both in execution and vehicle availability, this closed system supply-demand estimate would have had more veracity. Today, with a broad array of potential investors, enhanced transparency for price discovery and the array of access vehicles (some not included in our demand estimates), we think the supply-demand estimates available are only helpful insofar as they describe shifts in flows and stimulate questions regarding what factors could be accounting for the observed breakdown in classic supply demand conclusions.

The current market is a case-in-point. Given the persistently large supply deficit since 2018, we would have expected spreads to tighten dramatically. The reality is that 93% of gross supply in the high yield market was used to facilitate some form of refinancing and much of the new paper that funded the refi was done so in another leveraged debt format (bank debt). Moreover, our demand estimate has its own issues.

Our rising star estimate, for example, intends to accommodate those issuers that have been re-rated higher and moved out of the high yield market.

Over 37% of our LTM demand estimate is derived from rising stars. Practically speaking, rising stars are rarely instantaneously sold upon upgrade. Our conclusion is that this technical consideration is rarely a first order influence on high yield. It is always trumped by fundamental economic conditions and a more precise assessment will only be available after more work is done (future quarterly). That said, we will revisit this issue later in this piece as it relates to an especially persistent feature in 2019 high yield conditions. As for our outlook regarding technicals in the high yield market, we think 2020 will continue to exhibit Supply Deficit conditions with strong refinancing activity absorbed by loan market activity. We regard this as a modestly positive tailwind for high yield in 2020.

VALUATIONS

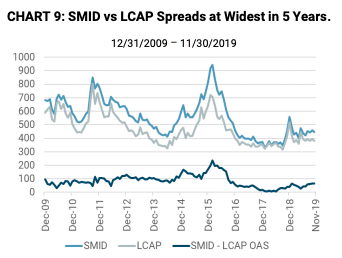

Chart 9 shows absolute spreads and the spread between Small- and Mid-cap (SMID) and Large-cap (LCAP) high yield bonds over the last 10 years. There are a couple of interesting observations. Not surprising given the weak performance of SMID compared with LCAP in 2019, spreads between the two have widened to the highest levels in five years. The more important observation given the importance of SMID to our investment strategy at Hotchkis & Wiley is that SMID spreads continued to weaken over 2019. Some of this is concentration related insofar as Energy and other hard-hit sectors have disproportionately high representation in the SMID universe underlying this chart. Given our expectations for possibility of crystallization of more carnage in these hard-hit sectors in the first half of 2020, we expect SMID spreads to remain vulnerable across some or most of the year.

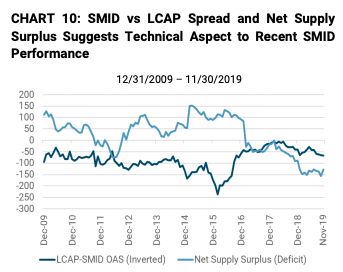

Chart 10 intends to underscore the idiosyncratic nature of SMID spreads over the period of its recent underperformance. The chart effectively maps the inverse of the SMID-LCAP spread against the Supply Surplus/Deficit measure discussed above. What we see is that since late 2017, when the supply deficit really started to expand, the LCAP-SMID spread has moved in near lockstep. It was only in the second half of 2019 that this strong correlation began to erode. We believe that there are two issues at play that might explain the parallel behavior. First, we know that this period coincided with an expansion of SMID bank debt issuance. This would partially explain why SMID bonds might weaken as the broader market remains relatively stable because of a negative survivorship bias in residual SMID universe. For example, the good SMID issuers refinanced into SMID bank loans, leaving the less able or more challenged names to compose the SMID market. Second, we also know that a significant buying force that evolved over that period was the higher quality and liquidity-demanding cross-over buyer. Only a modest percentage of the SMID market would meet this dual quality/liquidity criteria.

Although we need to continue to analyze this relatively new aspect of the SMID market, we believe the forces that have put pressure on SMID spreads over the recent several quarters could continue at least into the first half of 2020. At the same time, we think this represents an opportunity for SMID credits with solid fundamental execution and prospects. Our perspective is that we are cautiously optimistic for the SMID cohort because both bank loan market cannibalization and crossover demand are potentially transitory influences. We intend to use more discrete position sizing and diversity to map our SMID exposure as we move into 2020.

OUTLOOK

Late cycle conditions with moderate growth, relatively contained inflation and constructive policy regime. This implies a baseline strategy that favors carry but does so while attempting to avoid downside volatility by focusing on core credit themes of seniority, asset coverage and flat-to-improving debt metrics. Upside variations include a faster-than- expected domestic growth, spurred in part by global reflation, which will push credit spreads tighter but could also force the Fed to reengage its tightening posture. Spread tightening would probably be offset by higher US Treasury yields and produce baseline returns in the mid-single digit area for 2020.

Downside scenarios are primarily tied to policy away from the Fed. Trade policy and the US Presidential election loom large as unknowns. Recent polling suggests Trump’s re-election prospects have improved, and that has ironically helped improve the tenor of the talks with the Chinese. Modulating a spiraling trade war is positive for the domestic economy and credit markets in general. The election will be expensive and provide economic stimulus. However, the real consequence will be in the outcome and to what degree does Congressional composition change. A sweep on either side will have material implications. Broadly speaking, we see a range of return scenarios for high yield ranging from very low single digits to upper single digits.

Duration. We will target a near benchmark duration stance for our accounts. Although we expect rates to rise modestly in 2020, we believe the economic data will continue to reflect a modest growth environment into the first part of 2020. Combine modest growth with a fragile international environment and an election year that could result in very different outcomes, we believe neutral is a prudent posture.

Quality. Some of the same factors that have made SMID look cheap, have made BB-rated bonds look rich to single Bs and CCCs. We will focus our attention on mid- and higher-quality single-B names as we believe that credit quality represents the base risk-reward trade-off. We also believe seniority is attractive and intend to focus on senior paper, either first or send lien. We will pursue this in bonds and bank debt.

Capitalization. We will maintain our overweight to SMID names, but we will actively diversify and manage position size lower with an average position size near 50 bps in an attempt to modulate the volatility of our SMID holdings in 2020.

All investments contain risk and may lose value. Investing in high yield securities is subject to certain risks, including market, credit, liquidity, issuer, interest-rate, inflation, and derivatives risks. Lower-rated and non-rated securities involve greater risk than higher-rated securities. High yield bonds and other asset classes have different risk-return profiles and market cycles, which should be considered when investing.

Data sources (most current data available): Charts 1-5: Bloomberg, FOMC, HWCM; Charts 6-8: JPMorgan, HWCM; Chart 9: ICE BofAML, HWCM; Chart 10: ICE BofAML, JPMorgan, HWCM.

©2020 Hotchkis & Wiley. All rights reserved. Any unauthorized use, disclosure or distribution is prohibited. This material is for general information only and does not have regard to the specific investment objectives, financial situation and particular needs of any specific person. It is not intended to be investment advice. This material contains the opinions of the authors and not necessarily those of Hotchkis & Wiley Capital Management, LLC (H&W). The opinions stated in this document include some estimated and/or forecasted views, which are believed to be based on reasonable assumptions within the bounds of current and historical information. However, there is no guarantee that any estimates, forecasts or views will be realized. Certain information presented is based on proprietary or third-party estimates, which are subject to change and cannot be guaranteed. Any discussion or view on a particular company, asset class, segment industry/sector and/or investment type are not investment recommendations, should not be assumed to be profitable, and are subject to change. H&W has no obligation to provide revised opinions in the event of changed circumstances. Information obtained from independent sources is considered reliable, but H&W cannot guarantee its accuracy or completeness. For Investment Advisory Clients.

Past performance is not a guarantee or a reliable indicator of future results.

© Hotchkis & Wiley

Read more commentaries by Hotchkis & Wiley