Chief Economist Scott Brown discusses current economic conditions.

With U.S. growth anticipated to be moderate this year, little was expected in the way of fiscal policy (taxes, government spending) and monetary policy (short-term interest rates), but life comes at you fast. For the financial markets, tensions in the Middle East came and went in just a few days, but the Wuhan coronavirus has generated considerable uncertainty. The federal funds futures market now shows that a Fed rate cut is in play, while President Trump is expected to soon announce a plan to cut taxes for the middle class.

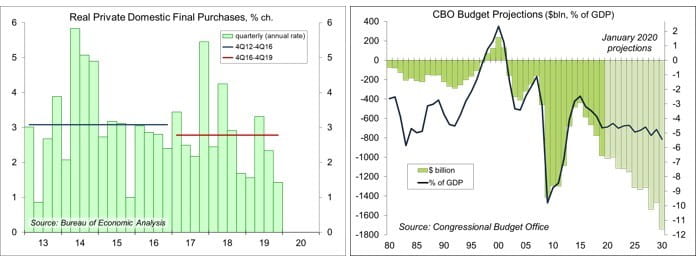

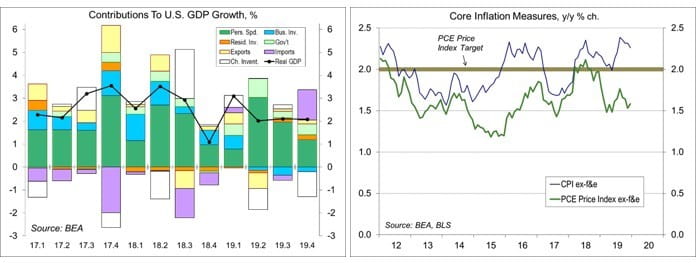

Real GDP rose at 2.1% annual rate in the advance estimate for 4Q19. As expected, consumer spending growth slowed, business fixed investment was weak, and residential fixed investment improved. Inventories slowed more than expected (partly related to the GM strike) subtracting 1.1 percentage points from headline GDP growth. However, the trade deficit narrowed more than expected, added 1.5 percentage points to growth. Imports, which have a negative sign in the GDP calculation, fell at an 8.7% annual rate in the quarter, but that likely reflects a correction from earlier stockpiling (ahead of expected tariffs). Private-Domestic Final Purchases (consumer spending, business fixed investment, and residential fixed investment), a better measure of underlying demand, rose at a 1.4% annual rate – up 2.2% year-over-year, but suggesting a slower trend. The mixed nature of growth (healthy consumer and housing sectors, weak capital spending) appears set to continue in early 2020.

Click here to enlarge

The Trump tax cuts appear to have had a limited, short-term impact on growth, but will have a long-term effect on the federal budget deficit. The latest update from the nonpartisan Congressional Budget Office projects trillion-dollar deficits as far as the eye can see. The government isn’t experiencing any difficulty in borrowing currently, but a much bigger problem lies further out. Beyond the 10-year horizon, entitlement spending is set to surge, lifting the federal debt sharply higher as a percentage of GDP.

Meanwhile, President Trump is expected to propose middle-class tax cuts in his State of the Union speech (February 4). An election year ploy, to be sure, but likely to provide more bang for the buck (although also adding to the federal budget deficit).

In his post-FOMC press conference, Chair Powell repeated that the FOMC believes that “the current stance of monetary policy is appropriate to support economic growth, a strong labor market, and inflation near the Fed’s 2% goal. However, the Fed would respond to “a meaningful reassessment of the economic outlook.” Asked about the Wuhan coronavirus, Powell noted that “the situation is in its early stages and it’s very uncertain how far it will spread and what the macroeconomic effects will be in China and its immediate trading partners and neighbors around the world.” The hope is that the virus will be contained and economic activity will rebound, but restrictions have halted economic activity is a large portion of China. Travel restrictions and voluntary avoidance will have a significant impact. The federal funds futures market reacted to Powell’s comments, and is now pricing in more than a 50% chance of a rate cut by June. Bond yields have fallen, which ought to help keep growth in consumer spending and housing strong. Slower global growth was cited as a key factor restraining business investment in 2019. Global growth was expected to pick up somewhat this year, but the Wuhan virus isn’t going to help.

Data Recap – There were few surprises in the economic data and the Fed left the benchmark rate unchanged. Concerns about the Wuhan coronavirus continued to dominate the financial market action.

By Friday, the Wuhan Coronavirus had infected nearly 10,000 people and killed more than 200. Cases were reported in all provinces and territories of China and in at least 24 other countries (including six the U.S.). The World Health Organization declared it a Public Health Emergency of International Concern. The U.S. quarantined 195 people who were evacuated from Wuhan. Delta and American Airlines suspended all flights between the U.S. and China, as did a number of international carriers.

The Federal Open Market Committee left the federal funds target range unchanged at 1.50-1.75%. In a technical adjustment, the FOMC also raised the Interest on Excess Reserves rate (IOER) and the reverse repo rate by 5 basis points each to better position the effective federal funds rate towards the middle of the target range. As expected, the Fed extended liquidity to the money markets to April.

In his press conference, Fed Chair Powell repeated that the FOMC believes “the current stance of monetary policy is appropriate,” and that “if developments emerge that cause a material reassessment of our outlook, we would respond accordingly.” Asked about the virus, Powell said that “there is likely to be some disruption to activity in China and possibly globally,” but the situation is in its early stages and it’s very uncertain how far it will spread and what the macroeconomic effects will be in China and its immediate trading partners and neighbors around the world.”

In its latest outlook, the Congressional Budget Office projects a $1 trillion budget deficit for FY20 (4.6% of GDP) and sees a $1.3 trillion average over the next 10 years (4.8% of GDP). Debt held by the public is expected to reach $17.9 trillion this fiscal year (81% of GDP), rising to $31.5 trillion in 2030 (98% of GDP).

Real GDP rose at a 2.1% annual rate in the advance estimate for 4Q19, up 2.3% from a year earlier. Private Domestic Final Purchases, a better measure of underlying domestic demand, rose at a 1.4% pace, up 2.2% y/y). Consumer spending rose at a 1.8% pace (following two strong quarters). Business fixed investment fell 1.5%, partly reflecting a further contraction in energy exploration. Residential fixed investment rose 5.9%, the second quarterly gain, following six consecutive declines. Inventory growth slowed sharply, reflecting the GM strike, subtracting 1.1 percentage points from headline GDP growth. Net exports (a narrower trade deficit) added 1.5 percentage points.

Click here to enlarge

Personal Income rose 0.2% in December (+3.9% y/y), held down by a retreat in farm subsidies (figures are reported at an annual rate, exaggerating monthly changes). Ex-farm income, personal income rose 0.3% (+4.9% y/y), in line with expectations. Private-sector wages and salaries rose 0.3% (+5.5% y/y). Personal Spending rose 0.3% (+5.0% y/y), up 0.1% (+3.3% y/y) adjusting for inflation. The PCE Price Index rose 0.3% (+1.6% y/y), up 0.2% (+1.6% y/y) excluding food & energy.

The Employment Cost Index rose 0.7% over the three months ending December, up 2.7% y/y (vs. +2.9% y/y 12 months earlier).

Durable Goods Orders rose 2.4% in December, boosted by a 168.3% rebound in defense aircraft orders (which more than offset a 74.7% decline in civilian aircraft orders). Ex-transportation, orders edged down 0.1%. Orders for nondefense capital goods ex-aircraft fell 0.9%, with a downward revision to November, while shipments fell 0.4% (following a 0.3% decline in November).

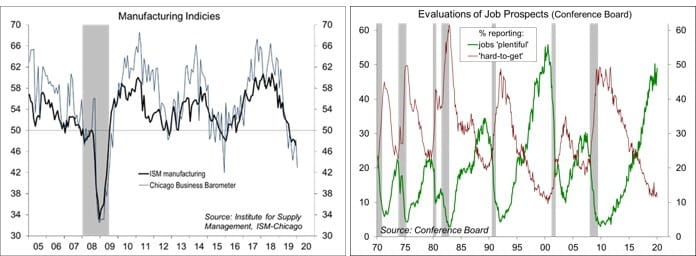

The Chicago Business Barometer fell to 42.9 in January, vs. 48.2 in December and 46.7 in November. It was the seventh month in contraction and the lowest since December 2015.

Click here to enlarge

The Conference Board’s Consumer Confidence Index rose to 131.6 in the initial estimate for January (the cut-off date for the preliminary result was January 15). Most of the increase was due to increased optimism about current and future job availability.

The UM Consumer Sentiment Index rose to 99.8 in January, vs. 99.1 at mid-month and 99.3 in December. The report noted that consumers dismissed concerns about slower economic growth, Mideast tensions, impeachment, and the coronavirus, focusing instead on the job market and personal finances.

New Home Sales slipped 0.4% in December, to a 694,000 seasonally adjusted annual rate (November revised lower). Results were mixed across regions. Unadjusted sales for 4Q19 up 20.7% y/y (Northeast +6.3%, Midwest +6.5%, South +1.1%, West +46.1%).

The Pending Home Sales Index fell 4.9% in December (down 22.2% before seasonal adjustment and +4.6% y/y), lower in all four regions. Monthly figure can be choppy. The average for 4Q19 was up 5.6% y/y (Northeast +2.1%, Midwest +2.7%, South +6.7%. West +10.0%).

Despite slower U.K. growth and Brexit uncertainties, the Bank of England’s Monetary Policy Committee voted 7-2 to maintain the Bank Rate at 0.75%. The statement noted that “policy may need to reinforce the expected recovery in U.K. GDP growth should the more positive signals from recent indicators of global and domestic activity not be sustained or should indicators of domestic prices remain relatively weak.” However, “further ahead, if the economy recovers broadly in line with the MPC’s latest projections, some modest tightening of policy may be needed to maintain inflation sustainably at the target.”

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

More Alternative Investments Topics >