The coronavirus is a looming economic problem.

The cognitive dissonance in the credit market is stunning. I recently have had the feeling that I’m living peaceably in Britain during the 1930s while on the continent the Germans were building weapons, expanding their army and navy, and opportunistically grabbing land. I know this comparison may seem excessive, yet market participants seem to be indulging in a cognitive dissonance akin to when British Prime Minister Neville Chamberlain in 1938 confidently assured not just Britain but the world that there would be “peace for our time.” He told them to ignore all the red flags and assured them that two decades after the end of the Great War there would be no repeat of the global carnage. Two years later the Nazis were bombing Britain.

In the markets today, yields are low, spreads are tight, and risk assets are priced to perfection, but everywhere you look there are red flags.

The latest red flag is the coronavirus. I would think that the correct way to measure the mortality rate of the coronavirus is similar to how you would evaluate the fail rate of an exam—the number of people who fail divided by the total number of people who have completed the exam, both passed and failed. Picture a four-hour exam that is administered every half hour from 8:00 a.m. to 12 noon. The fail rate for the 8:00 a.m. cohort is the number of 8:00 a.m. people who failed divided by the number of 8:00 a.m. test-takers, not the number of 8:00 a.m. people who failed divided by the sum of all the people who are taking the test at each interval from 8:00 a.m. through 12:00 noon.

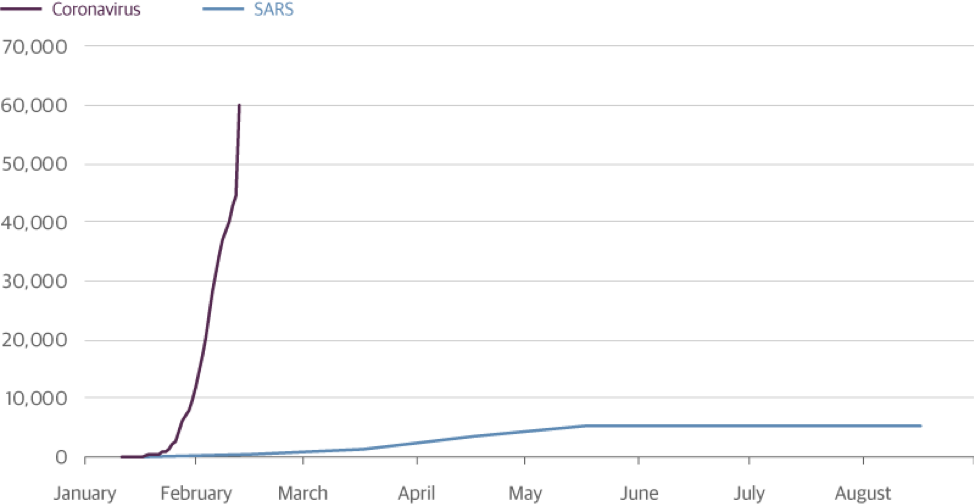

Unbelievably, this is how the popular press is reporting the coronavirus “fail rate,” which is the mortality rate. At this moment, the coronavirus death toll stands at 1,370, and the number of confirmed active cases is 60,408. The press will take those two numbers and suggest that the death rate is 2.3 percent, and therefore lower than the 9.6 percent death rate of the SARS episode. But in order to calculate death rates, the denominator needs to be the sum of deaths plus cures, i.e., those who have completed the test. According to Worldometer, the number of cases with outcomes total 7,641 (1,370 deaths plus 6,271 recoveries/discharges), which suggests a much higher death rate of 18 percent.

The coronavirus was first widely reported in early January, and the total number of deaths already exceeds the total from SARS, which went on for about nine months. Coronavirus is much more deadly than SARS and if not contained threatens to become a global pandemic. For perspective, the last pandemic, the Spanish influenza of 1918, killed 50 million people around the world, or 3 percent of the global population.

The Coronavirus Spread Much Faster Than SARS in China

Number of Confirmed Cases

Source: Guggenheim Investments, China National Health Commission, Wind. Data as of 2.12.2020.

Even if there were a vaccine for coronavirus today, production would have to get to a scale to meet demand. We don’t just need the vaccines for the 60 thousand active cases already diagnosed, we would need enough for the expected exponential rise in the number of cases, which on the current trajectory soon will reach hundreds of thousands if not millions.

The already-terrible human impact of coronavirus clearly has the potential to become tragic, but the economic impact will be significant even if its progress can be impeded. Our estimate is that China’s Gross Domestic Product (GDP) growth for the first quarter could be slashed to -6 percent annualized from an already slow 6 percent in the fourth quarter. That could shave about 200 basis points off of global growth relative to its recent trend.

At the same time that China is being forced to shut down factories and quarantine workers, interruptions to the supply chain in the United States and Europe have yet to be felt. By most estimates, if the Chinese extend the lunar new year by two weeks it would not meaningfully impact the global supply chain, but if it went beyond two weeks then we would start to see problems for materials and consumer goods outside of China. Even if the virus does not turn into a pandemic, to think it isn’t going to impact what’s going on in the world is irrational.

The impact of all this on corporate profits and free cash flow will be dramatic. The effect on oil and energy prices could be even more extreme. Right now, excess oil production in the world is an estimated one million barrels per day, so as demand dries up from repercussions, oil could plunge to $25 a barrel unless OPEC or other producers decide to cut production.

Also, we cannot forget that the published numbers related to the coronavirus may be understated. Many experts are confident that as bad as the numbers are, the Chinese are underreporting.

Yet as a major economic problem looms on the horizon, the cognitive disconnect between current asset prices and reality feels like the market equivalent of “peace for our time.” The average BBB bond yields just 2.9 percent. A recent 10-year BB-rated healthcare bond came to market at 3.5 percent and subsequently was increased in size from $1 billion to $1.7 billion due to excess demand.

For those investors who perceive the disconnect between risk assets which are priced for a rosy outcome and the reality of the looming risks to growth and earnings, any attempt to reduce risk leads to underperformance. It is a mind-numbing exercise for investors who see the cognitive dissonance. The frantic race to accumulate securities has cast price discovery to the side. In the world of corporate bonds and asset-backed securities, issuers are launching deals and then tightening spreads to Treasurys by 25 basis points or more relative to where the last similar new issue was priced just a day before. They are also upsizing deals, as it has become common to see new issue bond underwritings ten times oversubscribed. The giant flood of liquidity is driven by virtually every central bank in the world injecting reserves into the system. And many investors today don’t even buy individual bonds, they purchase a basket of bonds that can be traded versus an exchange-traded fund (ETF). The quality of the bond doesn’t matter; no one is actually negotiating a rate or a price. In the ETF market, prices are set by pricing services that frequently use stale data when no price discovery has occurred. The result is a non-market price determining where a security is trading and there is no additional price discovery, meaning nobody is negotiating individual bond prices. If it is in the index, buy it! This is what price discovery has become.

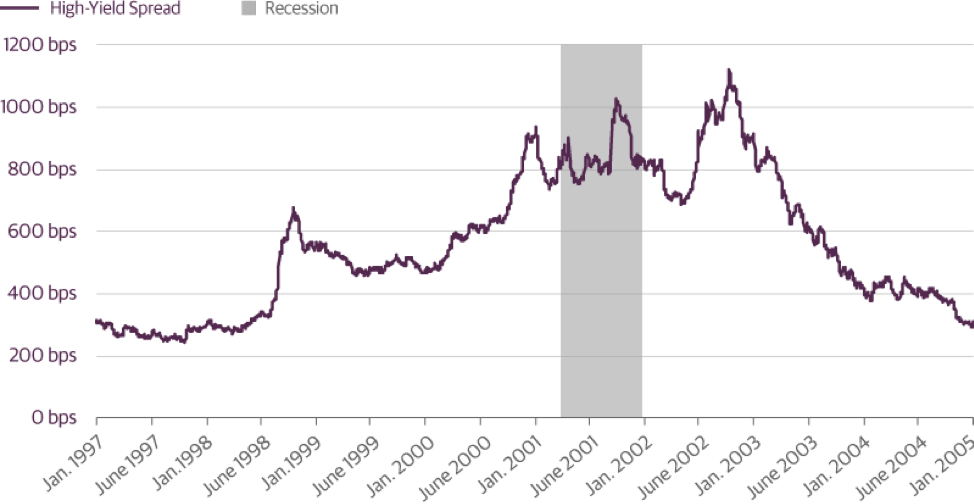

This will eventually end badly. I have never in my career seen anything as crazy as what’s going on right now. It was crazy in 2006 when I was pounding the table saying we were going to have a financial crisis of biblical proportions. And it was crazy in 1997, when high yield spreads got as tight as 239 basis points over Treasurys in October of that year, and then zigzagged their way higher for five years, until they peaked at 1,036 basis points in October 2002.

High-Yield Spreads Widened for Five Years After 1997 Tights

Source: Guggenheim Investments, Bloomberg. Data as of 2.10.2020.

The coronavirus is just one example of exogenous events that could prick the bubble. Just as Britain experienced in 1938, the ultimate calamity would not occur for another year or more.

So what is an investor to do in an era of cognitive dissonance? Buy the highest-quality securities possible that reach some target threshold return. I accept the fact that we may be investing money at levels that don’t make sense, but we invest for the long-term and to preserve capital, and as the cash flows in it must be spent.

We are either moving into a completely new paradigm, or the speculative energy in the market is incredibly out of control. I think it is the latter. I have said before that we have entered the silly season, but I stand corrected. We are in the ludicrous season.

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

One basis point is equal to 0.01 percent.

Investing involves risk, including the possible loss of principal. Investments in fixed-income instruments are subject to the possibility that interest rates could rise, causing their values to decline. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

©2020, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.

© Guggenheim Investments

More Alternative Investments Topics >