Recession risks have diminished, and we are more confident in our baseline forecast of a moderate recovery in global growth this year against a backdrop of benign inflation.

But monetary policymakers have less space left to guard against future recessions, and the possibility of disruptions due to trade conflicts, political tensions, or unforeseen events such as the emergence of the new coronavirus loom over the outlook.

As discussed in our Cyclical Outlook, “Seven Macro Themes for 2020,” investors should watch the interplay of forces such as global growth, inflation, and potential disruptors for clues on how to adjust their portfolios in the year ahead.

The world leads, the U.S. lags

Just as the U.S. cycle lagged behind the global cycle during 2018 and 2019 with the U.S. economy slowing later and by less than the rest of the world, we expect global growth to trough out and rebound earlier than U.S. growth this year.

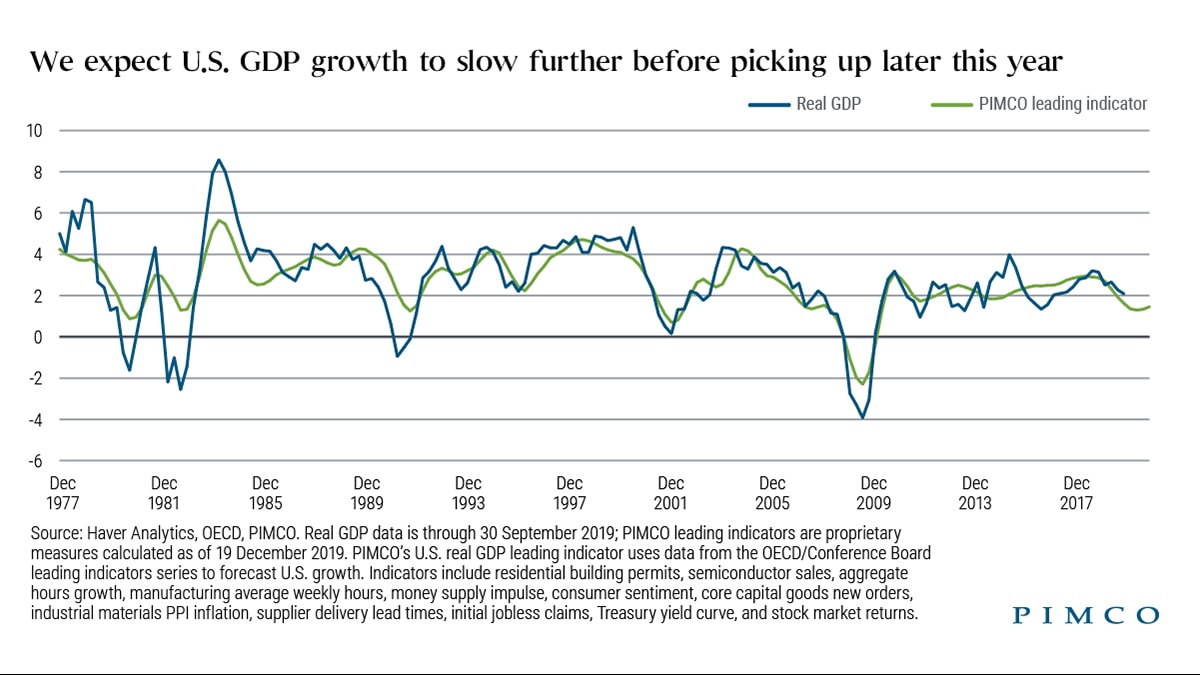

Signs of a rebound already started to show up late last year in the global purchasing managers’ indices (PMIs), particularly in emerging markets, and in other business surveys that are sensitive to global trade and manufacturing, such as the German Ifo survey. Meanwhile, in the U.S. our leading indicators suggest that GDP growth could slow further to around 1% annualized in the first half of this year before picking up again (see chart).

Moreover, temporary production cuts in the U.S. airline industry could shave off another 0.5 percentage points from first-quarter annualized GDP growth, though this would likely be largely recovered assuming production resumes in the second quarter as is widely expected.

Image Pop Up

Image Pop Up

Another factor that could hold back U.S. animal spirits and growth this year would be a possible increase in political uncertainty ahead of the U.S. elections, particularly if progressive high-tax, high-regulation Democratic candidates gain more support during the primaries. This would most likely weigh on business sentiment and investment spending and could lead to a tightening of financial conditions via lower expected equity returns.

Taken together, U.S. growth momentum may lag global growth momentum at least for some time during the first half of 2020.

Inflation: the devil they prefer

While our baseline forecast is for benign inflation in the advanced economies over our cyclical horizon, we believe medium-term upside risks outweigh downside risks, especially given how little inflation is priced into markets.

One reason is that labor markets have continued to tighten, and wage pressures, though still very moderate given the low level of unemployment, have been picking up recently. If unemployment falls further as economic growth recovers this year, wage pressures are likely to intensify over time, and firms will find it easier to pass on cost increases as demand improves.

Also, with fiscal policy likely to become more expansionary over time, in line with our view that “fiscal is the new monetary,” nominal demand should be better supported, especially if central banks play ball and don’t aim to offset fiscal easing with monetary tightening as the Fed did in 2018.

Last but not least, after many years of missing their inflation targets on the downside, virtually all major central banks seem to prefer inflation (the devil they know) over deflation (the devil they don’t know). While any changes resulting from the Fed’s ongoing and the European Central Bank (ECB)’s upcoming strategic review are likely to be evolutionary rather than revolutionary, we expect a nod toward average inflation targeting in the U.S., and a more symmetric 2% inflation target or target band centered around 2% in the euro area, implying a higher tolerance by two major central banks for potential inflation overshoots.

Against this backdrop, and despite the expected global growth recovery this year, we see the major central banks largely on hold and expect the bar for tighter policy to be generally higher than the bar for further easing. While discomfort with negative interest rates in Europe is rising given the unpleasant side effects, the ECB is very unlikely to exit until well beyond our cyclical horizon.

Dealing with disruption

While our baseline economic outlook of a moderate pickup in global growth amid supportive monetary and fiscal policy is relatively benign, we remain cognizant of the potential for significant bouts of volatility caused by geopolitics and national politics around the world.

Despite the Phase 1 trade deal between China and the U.S., relations between the established power U.S. and the rising power China remain fragile and tensions could easily erupt again during this year.

Another area of focus this year will be the U.S. elections in November. Risk markets will pay close attention as the field of Democratic candidates for the presidency narrows during the primaries.

Moreover, the recent wave of protests against the political establishment across many emerging market economies may spread further, especially as potential growth in many of these economies has downshifted, which increases the dissatisfaction with governments and sharpens the focus on income and wealth inequality.

The recent coronavirus outbreak adds to the uncertainty. Thus, as we pointed out in our 2019 Secular Outlook, investors will have to get used to “dealing with disruption” and position their portfolios accordingly.

Read PIMCO’s latest Cyclical Outlook, “Seven Macro Themes for 2020,” for further insights into the 2020 outlook for the U.S. and global economy along with takeaways for investors.

Joachim Fels is PIMCO’s global economic advisor and a regular contributor to the PIMCO Blog.

DISCLOSURES

All investments contain risk and may lose value. Investors should consult their investment professional prior to making an investment decision.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. There is no guarantee that results will be achieved.

© PIMCO

© PIMCO

More Alternative Investments Topics >

Image Pop Up

Image Pop Up