The economy was mixed in 2019. Consumer spending, while uneven, was relatively strong, supported by solid fundamentals. Business fixed investment and manufacturing were weak, but not “recessionary weak.” January data are to be taken with a grain of salt – seasonal adjustment is huge and weather (good or bad) can exaggerate – but figures point to more of the same. Concerns about the coronavirus COVID-19 have replaced trade policy worries.

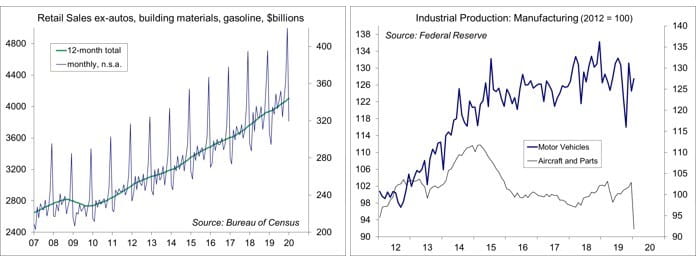

Retail sales plunged 19.4% in January, before seasonal adjustment, reflecting the end of the holiday shopping season. That works out to a 0.3% gain in adjusted sales (±0.4%). Generally mild weather means that more people can go out shopping (general merchandise up 0.5%, eating and drinking establishments up 1.2%), but moderate temperatures can dampen sales of seasonal gear (clothing store sales down 3.1%). The UM Consumer Sentiment Index improved further in mid-February. Consumers rate their current finances and the national economy highly, but we saw a drop in views of the buying climate for durable goods. Strong job growth and wage gains are supportive, but inflation is higher than a year ago, reducing the pace of improvement in purchasing power. Rising shelter and healthcare costs are hitting middle class budgets. On balance, consumer spending growth is likely to trend at a moderate pace, but we can expect some variation from month to month and from quarter to quarter.

Business fixed investment was weak in 2019, reflecting trade policy uncertainty, slower global growth, a decrease in energy exploration, and problems at Boeing. With the Phase 1 trade deal with China, trade policy uncertainty has diminished, but has not been eliminated entirely. Boeing’s halt in production of the 737-MAX reduced the output of aircraft and parts by 10.7% in January. Global growth was widely expected to pick up this year and next, but the coronavirus has dampened that outlook. The softer global outlook has put some downward pressure on oil prices, just as the correction in oil and gas well drilling appear close to having run its course. Taken together, the outlook for business fixed investment remains soft. While the ISM Manufacturing Index edged into expansionary territory in January, factory output softened. Still, as the Fed noted in its Monetary Policy Report to Congress, “mild slowdowns have often occurred during expansionary phases of business cycles -- in contrast, a more pronounced contraction in manufacturing has historically been associated with an economy-wide recession.”

The coronavirus has disrupted supply chains, reducing auto production in Japan and South Korea. Wuhan, a city of 11 million, is effectively a ghost town. Some are able to work from home, but most are not. Voluntary travel restrictions have spread far from Wuhan, reducing global travel. The Mobile World Conference, the world’s largest exhibition for the industry, in Barcelona, was cancelled. Bookings in the cruise industry are down.

Activity will recover once the coronavirus is contained, but it will likely take months instead of weeks. Last week’s adjustment in the reporting criteria raised the estimate of inflations sharply, reduced confidence in Chinese authorities, and added to the uncertainty. There will be an impact on the U.S. economy. However, growth in domestic demand, while mixed, should remain moderate.

Data Recap – The spread of the coronavirus COVID-19 appeared to be slowing, but an adjustment in the criteria for recognizing cases changed, boosting the reported number of infections, increasing anxiety and uncertainty about the economic impact. Fed Chair Powell’s testimony and the mid-month economic reports were about as anticipated.

Fed Chair Powell covered little new ground in his monetary policy testimony. “Fundamentals supporting household spending remain solid and residential investment turned up in the second half,” he reported, “but business investment and exports were weak, largely reflecting sluggish growth abroad and trade developments.” While trade policy uncertainty has diminished somewhat, “we are closely monitoring the emergence of the coronavirus, which could lead to disruptions in China that spill over to the rest of the global economy.” He cautioned that the general low level of interest rates means that there is less scope for monetary policy stimulus during a downturn. Fiscal policy stimulus would likely be needed, Powell said, but we are not currently on a sustainable budget path.

Retail Sales rose 0.3% in the initial estimate for January (+4.4%), with mild downward revisions to November and December. Motor vehicle sales rose 0.2% (+5.7 % y/y). Ex-autos, sales rose 0.3% (+4.0% y/y), also with downward revisions to the previous two months. Gasoline sales fell 0.5% (gasoline prices fell 1.6% in the January CPI report). Sales of building materials and garden supplies rose 2.1% (-1.3% y/y). Core retail sales (which exclude autos, building materials, and gasoline) rose 0.2% (+3.8% y/y) – consistent with a moderate pace of consumer spending growth in the near term.

Business Inventories rose 0.1% in December (+2.2% y/y), while business sales slipped 0.1% (+1.6% y/y). Retail inventories, the only new information in the report, were unchanged (autos -0.1%, non-autos 0.0%), lower than assumed in the advance GDP report.

Industrial Production fell 0.3% in January (-0.8% y/y). The output of utilities fell 4.0%, following a 6.2% decline in December (-6.2% y/y), reflecting mild temperatures. Mining rose 1.2% (+3.1% y/y), with oil and gas well drilling flat (-24.0% y/y). Energy extraction rose 0.9% (+8.4% y/y). Manufacturing output slipped 0.1%, as a 2.4% increase in auto production was more than offset by a 10.7% decline in aircraft and parts. Results were mixed, but generally lackluster otherwise.

The Consumer Price Index rose 0.1% in January (+0.145% before rounding, +2.5% y/y). Food rose 0.2% (+1.8% y/y), mixed over the last year (food at home up 0.7% y/y, food away from home up 3.1% y/y). Gasoline fell 1.6% (-0.8% before seasonal adjustment, and +12.8% y/y). Ex-food & energy, the CPI rose 0.2% (+0.242% before rounding, +2.3% y/y). Note that the Fed uses the PCE Price Index as its official inflation target, which has been trending about 0.7 percentage point below the core CPI y/y in recent months (+1.6% for the 12 months ending in December).

Real Hourly Earnings edged up 0.1% in January (+0.6% y/y). For production workers, real hourly earnings were flat (+0/7% y/y).

Job Openings fell sharply in January (-5.4% m/m, -14.1% y/y), but remained high by historical standards.

The UM Consumer Sentiment Index edged up to 100.9 in mid-February, vs. 99.8 in January. The report noted that evaluations of personal finances and the national economy posted large gains, while views on buying conditions for household durables posted a significant loss.

The Index of Small Business Optimism rose to 104.3 in January, vs. 102.7 in December (it had peaked at 108.8 in August 2018). Hiring intentions and capital spending plans remained moderate.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.