In January, we highlighted signs of green shoots in economic data—learn how recent developments affect our outlook.

Executive Summary

As a result of the current economic backdrop and accommodative central bank policy, we expect a short-lived contraction as we believe near-term economic data will be weak, but ultimately rebound later in the year.

While the magnitude of the recent market selloff is certainly nerve-wracking, it is important to note that this market cycle has survived several periods of significant uncertainty and market volatility.

While risk is generally skewed to the downside, we are also beginning to see pockets of opportunity—this is particularly true in the IG credit and high yield markets where, similar to the fear-based sell off of December 2018, we are finding select opportunities to purchase oversold credits with robust fundamentals.

Global Markets: The Impact to Date

The rout in equity and credit markets as a result of the new cases of COVID-19 (Coronavirus) accelerating globally has caused significant selling pressure across virtually all risk-related asset markets. The data from Johns Hopkins University’s Center for Systems Science and Engineering paint a picture of stabilization in terms of new cases of the virus reported in China. However, new cases outside of China are accelerating, which in turn has caused a widespread selloff across global risk assets.

The initial selloff started in emerging markets. However, as the virus spread to other countries, U.S. markets have quickly followed suit. In just ten days, the S&P 500 went from a record high to a correction of over -10%. Corporate credit markets have also experienced meaningful volatility and yields for the 30-year and 10-year Treasury reached all-time lows.

How Does the Virus Affect Our 2020 Outlook?

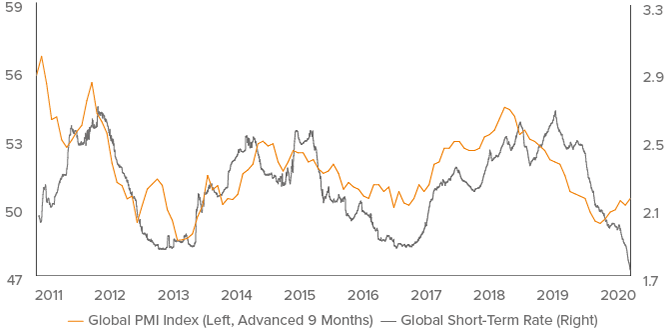

In January, we published our investment themes for 2020, highlighting signs of green shoots in the economic data arresting the slowdown that began in 2018. Our outlook focused on the monetary policy response that unfolded in 2019. A look at the decline in global short-term interest rates prior to the COVID-19 outbreak was an important source of steam that was in the pipeline, and remains so today, in our view (Figure 1).

Liquidity aggregates have been improving. Some of our longterm fundamental indicators turned positive in early February for the first time since May 2018 and inventories were declining. As of today, we see COVID-19 as a shock to the economy. If the COVID-19 morphs into a global pandemic, we believe the signs of emerging positive trends in the global economy will evaporate. If the virus can be contained, then global growth can recover after recessionary readings for the first quarter. In our view it’s the next two to three weeks that the narrative will unfold.

Figure 1. Global Central Bank Policy Remains Supportive of Growth

Source: Cornerstone Macro. As of 1/31/20.

What We Are Monitoring

Credit spreads and U.S. corporate financing conditions are part of the indicators we are watching closely. Economic data will be impacted significantly for the next few months.

In China, one measure we will be watching closely is the number of extended closures. This number seems to have peaked in early February with companies like Starbucks recently announcing that it was reopening hundreds of stores it had closed in response to the virus. So far, the Chinese government is injecting targeted stimulus to help curb the economic impact of the coronavirus. In February, the Chinese government rolled out a series of policy measures to support areas heavily affected by the virus, most notably the manufacturing sector.

What We Expect: Growth is Delayed, Not Derailed

While the magnitude of the recent market selloff is certainly nervewracking, it is important to note that this market cycle has survived several periods of significant uncertainty and market volatility. For example, while the U.S.-China trade war may seem like ancient history, it was only a few months ago when the market experienced large swings in response to the ongoing negotiations between the two countries.

Based on available information and our forward-looking indicators (which incorporate some of the recent market stress), we believe the outlook we outlined in January remains largely intact. As a result of the current economic backdrop and accommodative central bank policy, we expect a short-lived contraction as we believe near-term economic data will be weak, but ultimately rebound later in the year.

However, the situation is very fluid and we are (as always) incorporating our models and indicators into our investment views. The path of U.S. monetary policy is skewed towards lower rates and additional liquidity injections may be needed, but the intra-meeting speeches from Federal Reserve officials indicate they are taking the risks to the near-term path of financial stability and economic growth into their forecasts. In the meantime, we will closely monitor the situation for confirming or contradictory evidence, and we will continue to publish updates to keep you informed about new developments that materially affect our outlook.

Disclaimer

Voya Investment Management has prepared this commentary for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.