Should Investors Heed the Message of the Markets?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe have a big economic calendar featuring employment news and the latest ISM survey. In normal times, observers would be parsing the data to adjust their economic and earnings expectations. Next week few will care. The market ignored last week’s reports and there is no reason to expect a change to “old news.” Instead, the punditry will be asking:

Should investors heed the message of the markets?

And expect plenty of variation in just what that message might be!

Last Week Recap

My last installment of WTWA, I expected attention to the wisdom of Mr. Buffett, highlighting his annual letter to investors. That prediction was accurate (barely) until markets opened Monday morning. The coronavirus spread beyond China, mentioned in last week’s “worry” list, became the most important story and lasted all week. We might remember, however, that Mr. B does not pay attention to the (hypothetical) market message.

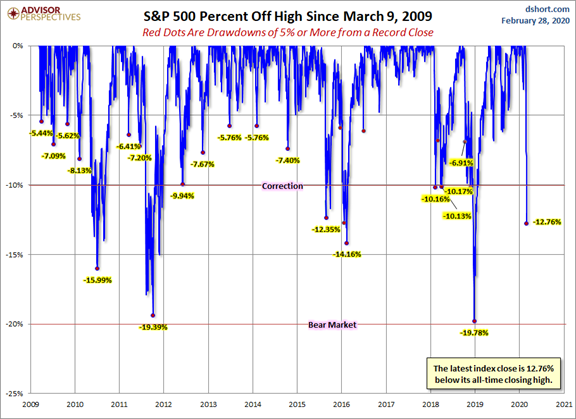

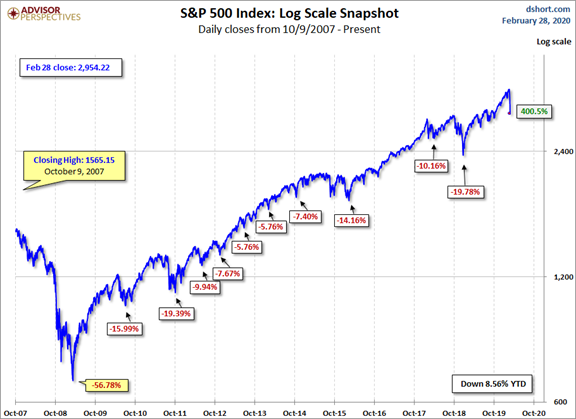

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, an excellent combination of key variables.

Let’s take a look at where this stands in the history of drawdowns in the current market rally.

And where we stand in the long-term.

The market lost 11.5% for the week, much of it during overnight activity. The trading range during market hours was 14.1% and 16.9% if measured from the prior weekly close. Many observers were surprised by the late rebound on Friday. In times of worldwide risks, traders often are cautious in front of the weekend. You can monitor volatility, implied volatility, and historical comparisons in my weekly Indicator Snapshot in the Quant Corner below.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. This report is fact-based and consistent with the choice of indicators. Consideration of three different time frames helps to clarify economic changes. This week shows an unusual pattern: positive long and short-term indicators, but a slightly improved, neutral “nowcast.” NDD observes that coronavirus impacts are not yet evident, but points to Redbook consumer spending, shipping, and rail as the best early indicators.

The Good

- Mortgage applications increased 1.5% versus the prior week decrease of 6.4%. Affordability has been helped by lower interest rates.

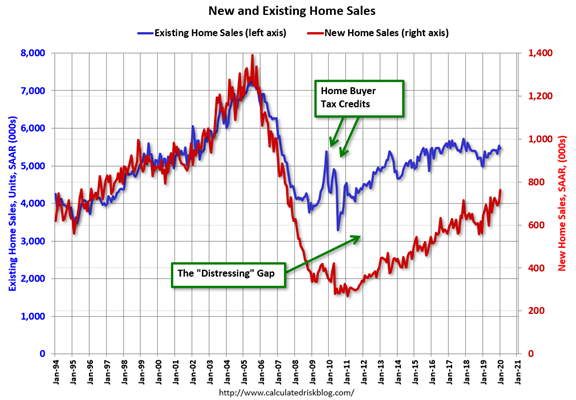

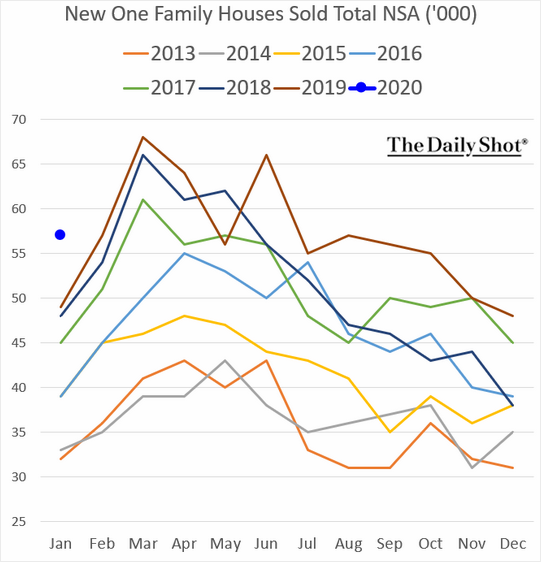

- New home sales for January were 764K (SAAR) versus the upwardly revised 708K for December and beating expectations of 720K. Calculated Risk observes that it was the highest sales rate since July 2007. He also shows the continued closing of the “distressing gap” created by distressed sales after the housing bubble. Homebuilders are further adapting to buyer needs. Foreclosures and forced sales are down.

I also like this chart from The Daily Shot, which compares January 2020 with each of seven prior years.

- Durable goods orders for January declined 0.2% much worse than the prior upwardly revised gain of 2.9%, but better than expectations of a 1.6% decline. The ex-transportation result, a gain of 0.9% was better than December’s small decline and expectations of 0.2%. This is a noisy series. It is often difficult to interpret, but I am scoring it as a small positive.

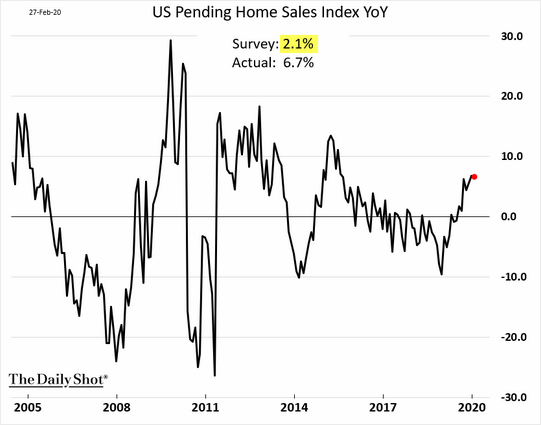

- Pending home sales for January increased 5.2%, beating expectations of 2.0% and December’s upwardly revised decrease of 4.3%.

- PCE Prices increased 0.1% on both the headline and core measures. This is slightly below expectations of 0.2% and below the Fed’s 2% annual target. I treat low values in this series as attractive, since the lack of inflation makes interest rate increases less likely.

- Personal income for January registered an increase of 0.6%, beating expectations of 0.4% and December’s downwardly revised 0.1%.

- Chicago PMI for February, which sometimes gets extra attention when the national PMI is in the following week, rebounded to 49.0. Many observers were alarmed by the prior reading of 42.9.

- Michigan sentiment for February was 101.0 slightly better than expectations of 100.8 and January’s 100.9.

The Bad

-

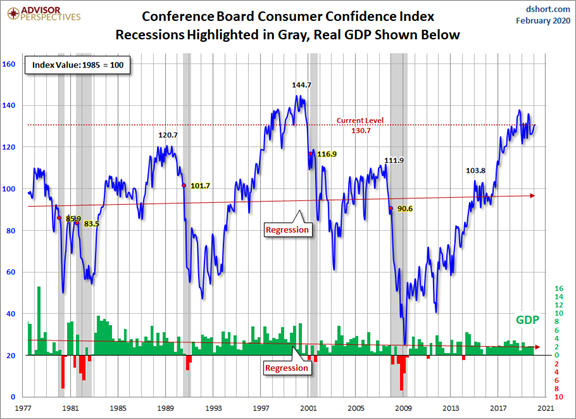

Consumer confidence for February Jill Mislinski reports

“Consumer confidence improved slightly in February, following an increase in January,” said Lynn Franco, Senior Director of Economic Indicators. “Despite the decline in the Present Situation Index, consumers continue to view current conditions quite favorably. Consumers’ short-term expectations improved, and when coupled with solid employment growth, should be enough to continue to support spending and economic growth in the near term.”

- Initial jobless claims edged higher to 219K versus last week’s 211K and expectations of 212K. The series remains in a historically attractive range.

-

Hotel occupancy declined Calculated Risk

“The obvious question is whether a dip in demand in airport hotels was directly connected to the coronavirus outbreak,” said Jan Freitag, STR’s senior VP of lodging insights. “However, one week of data is not sufficient for STR to make that correlation, especially considering last week was rather weak around the country in general—possibly due to extended vacations after Presidents’ Day.

“We’ve maintained that we do expect to see a coronavirus impact in U.S. hotel performance data, especially in gateway cities that have historically seen a large number of Chinese arrivals. We’ll continue to monitor the data each week. The next few weeks will be especially interesting considering the news to come out of the CDC on Tuesday.”

- Personal spending for January increased 0.2%, below expectations of 0.3% and December’s upwardly revised 0.4%.

An Important Comment on Data Interpretation

Regular reporting of data releases makes it easy to forget that the “news” is often weeks old. When events are breaking fast and markets responding to headlines, this is important to keep in mind. Here are two examples from last week, comparing two popular measures of individual sentiment.

Consumer Confidence from the Conference Board reflects the results of a mail survey from the early portion of the month.

The CCS mailing is scheduled so that the questionnaires reach sample households on or about the first of each month. Returns flow in throughout the collection period, with the sample close-out for preliminary estimates occurring around the eighteenth of the month. Any returns received after then are used to produce the final estimates for the month, which are published with the release of the following month’s data.

Michigan sentiment is drawn from a telephone survey including results from the final week of the month. Richard Curtin, chief economist for the survey, wrote this comment.

Consumer sentiment rose to 101.0 in February, nearly matching the expansion peak of 101.4 set in March 2018. The coronavirus was mentioned by 8% of all consumers in February when describing the reasons for their economic expectations. However, on Monday and Tuesday of this week, the last days of the February survey, 20% mentioned the coronavirus due to the steep drop in equity prices as well as the CDC warnings about the potential domestic threat of the virus. While too few cases were conducted to attach any statistical significance to the findings, it is nonetheless true that the domestic spread of the virus could have a significant impact on consumer spending. Importantly, the early indications suggested only a very modest impact as the Sentiment Index among consumers who mentioned the coronavirus was still quite high (just over 90.0). If the virus spreads into U.S. communities, consumers are likely to limit their exposure to stores, theaters, restaurants, sporting events, air travel, and the like. There is likely to be some advance buying and increased online shopping, but much of the discretionary spending may not occur. To be sure, there is no reason to anticipate that consumers will engage in such extreme measures at this time. It is a fine line that needs to be drawn to encourage people to take normal steps of preventive hygiene but not to engage in panic reactions. Panic is best avoided by a strong sense of confidence in the government’s responses that aim to control the potential spread of the virus and limit any resulting damage to the economic welfare of consumers. The most effective fiscal and monetary policies include proposed reactions to the virus that are transparent, well understood, and act to maintain confidence in government economic policies close to its nearly two-decade high.

And keep in mind that this Friday’s Employment Situation report is based upon data from the week of Feb 10-14, missing the last two weeks of coronavirus news.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

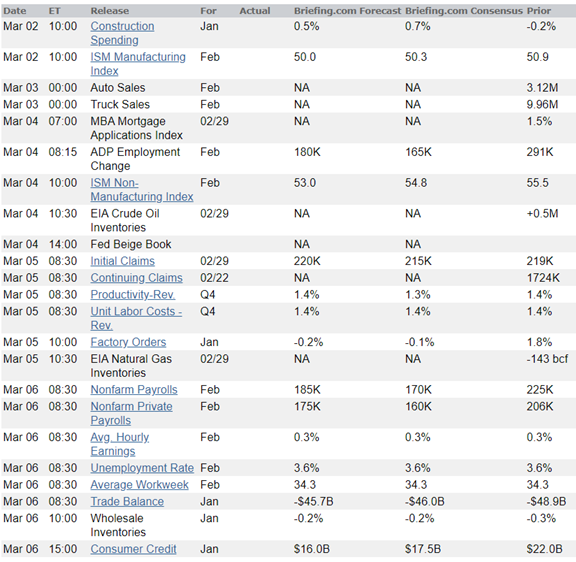

The economic calendar is a big one including several important reports and featuring employment. The Super Tuesday primary results will attract attention, but probably will not be market moving. Information about the coronavirus spread will not follow a calendar but will command attention all week.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Despite the important economic data to be released in the week ahead, news about the current economy will not be the theme. The speed of last week’s market decline has drawn attention from everyone, including those who are not regular followers of financial news. I expect the punditry to be asking:

Should investors heed the message of the markets?

Pundits love this sort of question. They need not deal with any actual data. They can weave stories using anecdotes. And anyone can sound very smart by describing what just happened and telling you “the message.”

Background

The first problem in answering this week’s question is figuring out what the message really is? This speculation will be undertaken by historians pretending to be economists, economists who claim expertise in epidemiology, and technical analysts who know not only what people are currently thinking, but what they will think next week. There is plenty of information, but it is a disorganized mess of unsound opinions, myths, along with solid research. It is not very helpful to the average investor.

My objective is to organize and report the best of what I read last week, placing emphasis on the problems of the individual investor. A logical framework is a great starting point. I’ll separate discussion into several important topics including:

- Facts

- Problems with data

- Potential for a “solution”

- Leadership needs

- Economic effects

- Earnings

- Wildcards

- Investment implications

- What to watch

I am placing more emphasis on thinking clearly about the investment challenges and less on specific investment ideas.

Events and facts

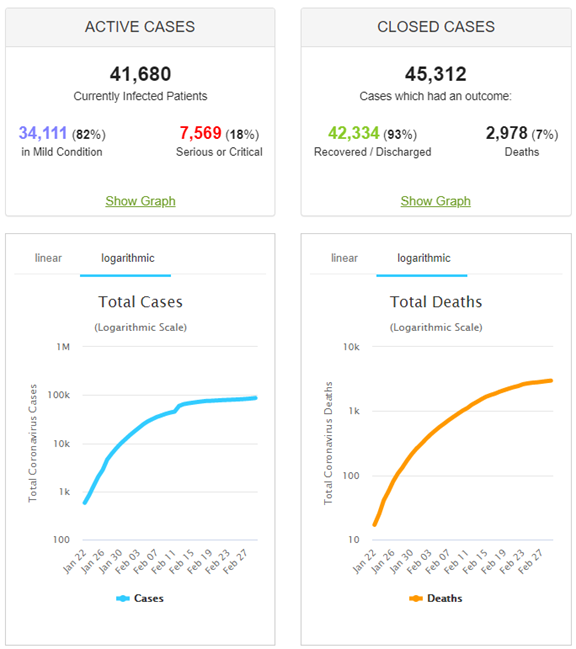

The spread to more countries has grown more extensive. I use worldometers.info as a monitoring source. It classifies the cases, regularly updates breaking news, and has useful charts. Here is their summary at my time of writing (just before midnight, EST).

Community spread is also showing up. These are cases where the patient does not have a travel or contact history that suggests exposure. (WSJ) The first US death occurred today. (AP)

A shortage of test kits and a fault in one of the tests hampered early testing. (Reuters).

Barely more than a handful of public health departments across the country are able to test for the novel virus, which began in China and has spread to at least 44 countries. The federal government has less than 10% of the protective masks required to protect healthcare workers and the public. And Washington still does not have adequate funding in place to support health departments’ efforts, though more money is on the way.

Conflicting messaging from the White House and top U.S. officials regarding the severity of the threat has only added to the uncertainty.

As CDC warns of US COVID-19 spread, labs frustrated over lack of tests

“Ultimately we will see community spread in the US; not a question of if, but when, and of how many people in this country will have severe illnesses,” said Nancy Messonnier, MD, director of the CDC’s National Center for Immunization and Respiratory Diseases, in a press conference.

But there was a swift policy response to the testing issue. (FDA news release). Local laboratories can now use tests they have developed and validated. More test kits are also being provided. (NPR)

Expert scientific analysis is difficult because of problems with the data. Most observers question the accuracy of the Chinese data, although their scientists have been helpful in work on a vaccine or antidote. Since victims can be asymptomatic for an extended period, we do not really know how many have been affected, the transmission rate, or the fatality rate.

Market action is widely believed to carry a message. Is that always true? What if the “message” changes very rapidly? What if it seems inconsistent? The extreme moves of last week did not really correspond to changes in the facts, despite the daily media effort to create an explanatory narrative. A more plausible interpretation is that some tail wagging is going on. Here is the pattern:

- Fresh news hits the tape.

- Algorithms, trained on recent reactions to similar news, react immediately.

- Traders, noting the current change in market direction, pile on.

- Technical traders carefully watch support and resistance levels from their charts. Violations bring them into action as well.

- The modern trading vehicle is the ETF. This is the reason for the huge spike in ETF volume last week. If there is no buyer, then the ETF managers can liquidate units by selling the underlying stocks.

- Financial news puts up splashy warning pages and a parade of experts who “explain” what just happened.

The result of this pattern is that moves that begin as relatively modest are quickly exaggerated. News that is relevant for only certain companies and sectors affects everything in the ETF. It is not the result of thoughtful investor or fund manager analysis. Fund outflows from stocks to bonds can occur even if most investors are doing nothing!

David Templeton (HORAN) sees a Market Decline Driven By A Panic Narrative. He provides a more balanced look at the market data, while warning that the “negativity can feed on itself.” There is also interesting data on the volume of stocks and ETFs.

Economic effects

The economic data is still OK, and the traditional recession indicators are little changed. The general perception has changed dramatically. There is plenty of attention to worst case outcomes.

The mechanisms for economic effects are easy to list, but difficult to quantify. By the Numbers: How the Coronavirus Epidemic Is Hitting Businesses Around the World, for example, provides estimates of some specific impacts. That is still far from an estimate of total effects.

- Lost purchases and commerce. Sometimes this is a one-time hit and other times a permanent loss.

- Store closings. Can result from public safety measures, quarantines, or simply lack of traffic.

- Supply chain. This can be an overall lack of goods or a single critical part. An example: Out of Stock: Coronavirus in China Threatens Amazon Sellers

- Nesting. People avoid public places. Planned travel and recreation are canceled. Eat at home or order in instead of going to a restaurant.

- Business meetings and travel. Much can be done by teleconference if really necessary. Hotels, restaurants, and airlines are affected.

- Business investments delayed. This is the typical result of uncertainty. It is easy for leadership to say, “Let’s just postpone our expansion plans. We can decide better when we have more certainty.”

These are all legitimate concerns and easy to imagine. They are also candidate for what I call “light switch thinking,” perhaps the biggest error of the amateur economist. Such effects happen at the margins, with a distribution of outcomes. The imagination quickly takes us to a worst case.

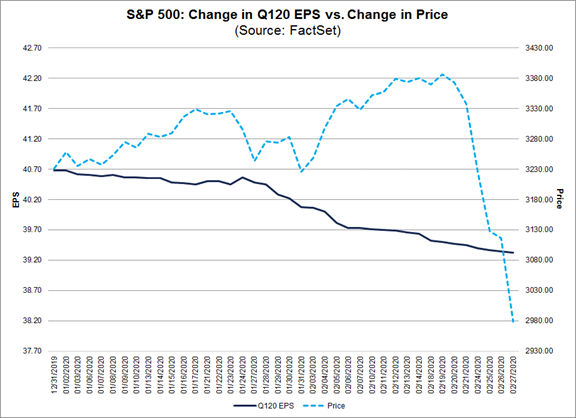

Earnings reductions

The economic effects influence stock prices through changes in earnings estimates. One “top-down” market strategist has gone to zero earnings growth in 2020. The “bottoms-up” analysts have not made large changes so far. John Butters suggests that these analysts are either not as pessimistic or are waiting for more complete company guidance. Meanwhile, some warnings from major companies have gotten plenty of coverage.

Wildcard Factors

If panic is a problem, effective leadership can be a solution. Instead, the issue has been overly politicized. The Trump Administration message has been inconsistent and not reassuring to many. This was partly a partisan reaction (CNN), but GOP Representatives also voiced frustration.

Acting White House chief of staff Mick Mulvaney accused the media of covering the story because it “will bring down the president, that’s what this is all about.” This should be a time to recognize issues and pull together. This has been typical in past crises, but the intense partisan dynamic may be crippling the ability of leaders to respond effectively.

Some worry about election effects on stocks. If there is perceived Trump weakness and Sanders strength, this is the most worrisome combination for markets.

Those on my list of “reliably bearish commentators” always forget that they are fighting powerful policymakers. There will be a policy response. Even if it is not perfect, it will have an effect. Some are looking to the Fed, because so many see their policy as underpinning the rally in financial markets. There has been some Fed response, but as usual, their viewpoint is not as pessimistic as that of traders. They want to see more data. The market wants and expects rate cuts – and plenty of them. Tim Duy has his usual excellent analysis criticizing the Fed message so far.

There might actually be some fiscal stimulus. Expect the traditional battle of tax cuts and targeted spending.

Thoughtful Expert Conclusions

Dr. Ed Yardeni summarizes the scientific data and then considers the economics. He writes:

More fearsome than the virus itself is the global contagion of fear it could spawn as governments continue to react with extreme measures and the media continues to hype the threat up. Governments’ responses have been drastic, as discussed in a 2/24 WSJ article; they include China’s quarantine of 60 million people in Hubei province, halting economic activity, and the US’ travel warnings and ban on entry of any non-American who has been to China in the past 14 days. As noted above, just yesterday, the CDC warned Americans to prepare for a severe disruption to everyday life in the US in the event of an outbreak here.

What Actions Might Investors Consider

I must start by underscoring that I provide investment advice to clients. I provide information to readers – information that I hope will be helpful in making their own decisions. With clients I can determine their personal situations and needs and discuss issues with them when needed. My readers cover a very wide range of circumstances. My challenge is to be helpful in my posts without crossing the line into advice.

With that in mind, I’ll begin with my own decisions and actions last week. On Monday morning, right after the opening, I reduced positions in our fundamental stock programs by 20-25%. This meant that the stock allocation in portfolios was lower than it would normally be. I was not trying to time the market. I did not know what would happen over the rest of the week. I did know that risk was greater, changing significantly after I published last weekend.

The size of my selling was a first reaction to the increased risk. If my risk assessment gets greater, I will make further reductions. This was not an across-the-board reduction in every position. I targeted holdings that I expect to participate least in a rebound (energy, big banks, chip stocks). If risk lessens, I will add to positions. If I were a Fed member, I could say that I am “data dependent.”

As some general advice, here is what investors of various stripes might do:

-

If you are a long-term investor, just sit tight. Unless you can do a sophisticated evaluation of all of the information, it is best not to attempt market timing.

- If you have a shorter time frame, you should have both short- and long-term components. For the short-term portion, you should take your own temperature on risk tolerance. Markets rebound from declines like this, but not always right away. Michael Batnick has an excellent series of charts showing “a bang,” a “rally and retest,” and a “fizzle.” “There are no rules,” he writes. Here is an example of the first but be sure to look at the others as well.

What Investors Should Not Do

-

Go all in or all out. That is a mug’s game where you must constantly ask when to get back in the market. If you must do some selling, analyze first and be selective.

- Try to time the crisis end. Markets can turn slowly or quickly. There can be false starts.

End Game Hints

I repeat that we cannot successfully time the market turn. I do see some things that might happen. These would all help to put a bid in the market.

- Reduction in the rate of the spread. Resulting news items might send the algorithm process into reverse.

- Fed action? The substantive effects can be debated, but the psychological market effect is significant.

- Strong fiscal stimulus. This seems unlikely right now, but it is on the watch list.

- Scientific progress. This does not need to be a total solution or miracle cure. Strong evidence that the progress of the virus can be contained would be greeted warmly with recession worries moving from the worst case. New drugs will not be following the same testing protocols. Some are already in tests in China and others may be used under the Right to Try Act. These could both provide test results much more quickly than usual. The sample sizes will not be as large, but preliminary decisions will be reached.

As usual, I’ll describe more of my own conclusions in today’s Final Thought.

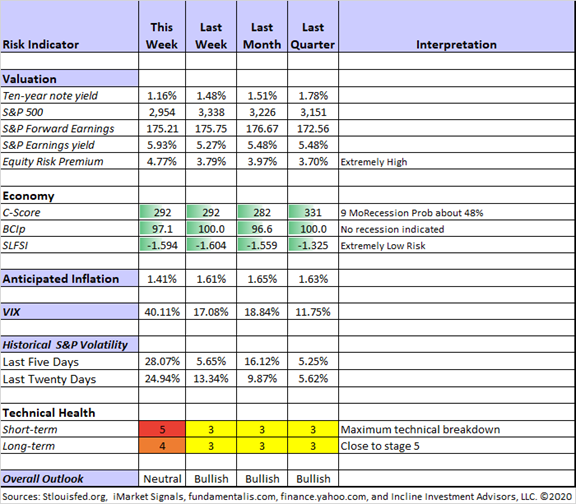

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Both long-term and short-term technical indicators collapsed this week. The C-Score remained the same, but I am boosting the recession odds to 48% since the indicators are capturing only some of the current factors. The St. Louis Financial Stress Index is published on Thursday, using data from the prior Friday. We can expect a higher reading next week.

I have moved to “Neutral” in the overall outlook despite attractive valuations. It reflects the increased risk and the need for patience in either buying or selling.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. Brian has a great highlight of the top ten stocks in the S&P 500. Welcome Procter & Gamble (PG) and Visa (V). This reinforces one of my own frequent points. When you buy an index ETF you are loading up on the current top cap stocks, not the ones that will move in. The leadership changes much more than most would think.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

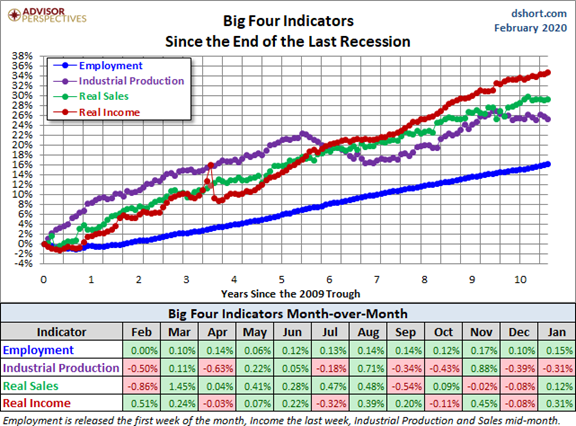

Doug Short and Jill Mislinski: Regular updating of an array of indicators. With the January data completely reported, it is time to check out the Big Four.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely. The drawback this week is that there is a lot of uncertainty surrounding when and how current worries will be resolved.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Aswath Damodaran’s A Viral Market Meltdown: Fear or Fundamentals?. As always, I admire the balanced and evidence-based work. As a Finance Professor and valuation expert, Prof. Damodaran does not exaggerate his credentials. While he takes note of the facts about the virus, he recognizes that his model for judging the effects will change with the evidence.

In short, there is a lot more that we do not know about COVID-19, than we do, at least at the moment. While it has not been labeled a pandemic yet, it seems to have the potential to become one, and we do not yet have a clear idea of how quickly it will spread, how many people will be affected and what will push it into dormancy. It is also clear that much of this uncertainty will get resolved by real-time developments, not by collecting data or by listening to experts to tell us what will happen.

He considers the long-term market move, writing “Since the first casualty of a crisis is perspective, it may be worth stepping back and looking at the market through a wider lens.”

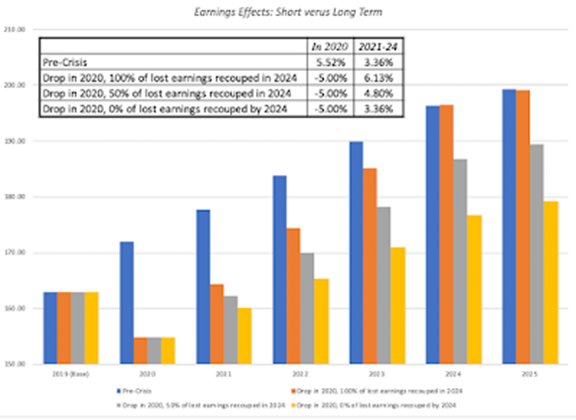

He then considers the various impacts – changed earnings growth for 2020 and possibly for longer.

In previous crises, where consumers and workers stayed home, either for health reasons or because of fear, the business that was lost as a result of the peril was made up for, when it passed. If consumption is just deferred or delayed, the growth in subsequent quarters will be higher, to compensate for the lost business in the crisis quarter. If consumption is lost, the drop in earnings in the crisis quarter will never be made up.

Here are the earnings effects under three different assumptions.

And finally, he modestly provides his model and again emphasizes the need to adjust in real time. A model like this helps you focus on the important factors and know what to watch for.

I am not an expert on infectious diseases, and the health and economic impacts of this virus are likely to play out as developments in real time, requiring that I revisit this framework frequently. Based upon my estimates of how this virus will affect the numbers, the value that I get for the index is 3003, about 4.14% less than the index level of 3128.21 at the close of trading on February 25, 2020, which, in turn, represents a significant drop from the level of the index a week ago. To the question of whether a virus can cause this much damage to the markets, the answer is yes, though whether it is an overreaction or not will depend on how it plays out in the numbers. For the moment, though, if you are tempted to buy on what looks like a dip, I would suggest caution just as I would argue for slowing down to someone who wants to do the opposite and sell.

Stock Ideas

Back next week. Right now, it is more important to focus on overall strategy and portfolio management.

The Great Rotation

The tension grows tighter, as the spreads we are monitoring grow wider. The coronavirus effect has nudged people along a path that has been recently successful, not one that will be ultimately successful. I am having patience in building this position, and you should as well.

Watch out for

- Attempting to hedge positions using VIX.

Coronavirus Sends VIX Into Backwardation—Here’s What That Means

Final Thought

Policy responses are important at a time of crisis, but the correct balance is a challenge. Even intelligent people (perhaps especially intelligent people) are likely to be trapped by their general knowledge and reading. Dr. Amitha Kalaichandran relates a story about a conversation with an intellectual friend “who doesn’t easily head into panic mode.” She was trying to purchase a mask, which you do not really need for protection.

It immediately struck me that, despite being trained in both epidemiology and medicine, I wasn’t entirely sure what to advise Ann at the time: the messages I had received, and articles I had read, were no more consistent. There was still much uncertainty around the coronavirus in terms of how serious it was projected to be and what ordinary citizens could do to minimize risk. We all make decisions every day despite uncertainty, and when emotions come into play it can make things trickier.

But when it comes to public health, where the risks of sending the “wrong” message can have devasting consequences—unnecessary anxiety on the one hand (which can take an immense psychological toll) and thousands of unnecessary deaths on the other. To me, one thing is clear: the messaging around coronavirus thus far has been far from ideal, which suggests that uncertainty in a public health emergency is a wrench that can have devastating consequences if it isn’t harnessed appropriately.

And this conclusion.

Similarly, public health stakeholders should communicate what is and isn’t known, coordinate messages to help ensure consistency, and perhaps most importantly, acknowledge that their views (and thus their messaging) may change quickly; thankfully more recently media organizations are choosing to express this uncertainty and a recent op-ed in the New York Times underscores many of these principles, as “people react more rationally and show greater resilience to a full-blown crisis if they are prepared intellectually and emotionally for it.” The authors also urge that we consider using the term “pandemic” (though the WHO is not yet comfortable with this).

Specific investment moves, as I noted above, vary widely according to each investor’s situation. There are a few things that apply to everyone. I can offer these recommendations to all investors who want to think clearly and unemotionally. The businesses you own are not worth 12% less than they were a week ago. No one is forcing you to accept less than the appropriate value if you sell one of your businesses. Instead, try the following:

- Quit watching your account balance and financial media. It is not providing useful information and is irrelevant unless you sell.

- Turn off the TV. This is not burying your head in the sand. It is avoiding the temptation to do something seriously wrong.

- Practice risk control, not timing. If your investments feel too risky, cut back. Don’t worry about taxes or selling at a loss. Getting the risk level right is more important.

- When you have the risk control right, just sit back. You may not “enjoy the flight” but you’ll have a more successful landing.

To summarize a long and difficult analysis, perhaps the most challenging I have ever undertaken:

The market reflects varied opinions and emotions, all of which change quickly. The market message reflects these emotions. Do not fall into the trap of believing that there is some great knowledge you must understand. The knowledge you need is what your stocks are really worth!

[I’m getting many reader questions about the Great Rotation. I have described the themes for several months, but there are always some new readers. I am using this approach in a few client accounts as well as my own personal account. I am excited about it. It is not yet an official program for my firm. Hint: Compliance and marketing.

Until we have more materials, readers can opt-in to an email list which describes our progress with the design of the program, provides detail on the themes, and analyzes a specific stock we have already purchased. There is no charge and no obligation for participants, and we will not use your email for any other purpose. You can opt-out whenever you wish, but I hope you don’t! Comments and reactions are an important part of my investment process. I welcome your participation. Just write to info at inclineia dot com. There has been a lot of interest. If we have missed you, please write again].

I’m more worried about

- More panic. Most experts expect to see more US cases and more deaths. It is not clear how much of this is already reflected in current market prices.

I’m less worried about

- Finding inexpensive stocks. Those waiting for a dip or needing to rebalance are getting such an opportunity.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits