Market Update: Is Panic the Primary Pandemic?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEquity markets have bounced around rather dramatically in recent weeks (up and down) as investors are trying to get a grasp of the impacts of Covid-19 (aka Coronavirus). While there will clearly be economic softening from Covid-19, the base case is that it will be transitory. A key question remains, when will fiscal and monetary policies assist a turn-up in economic activity? This also begs the question: Is our biggest pandemic actually a public panic?

The markets are now also digesting the impact of an impasse between OPEC and Russia to curb oil production in an effort to stabilize prices. This is the primary driver of the market’s reactions on Monday, March 9th. Oil prices were sliding on expectations of global softening due to Covid-19.

Before we address oil, let’s review Covid-19. Please also reference our posts on February 25th and March 3rd, as well as the recording of our February 28th conference call for related information on the virus and how diversification and portfolio construction can help weather these times. Within this update, we also discuss what issues could help change the narrative.

We should also wish those impacted by Covid-19 our sincerest thoughts and prayers.

Watching the Outbreak (Update)

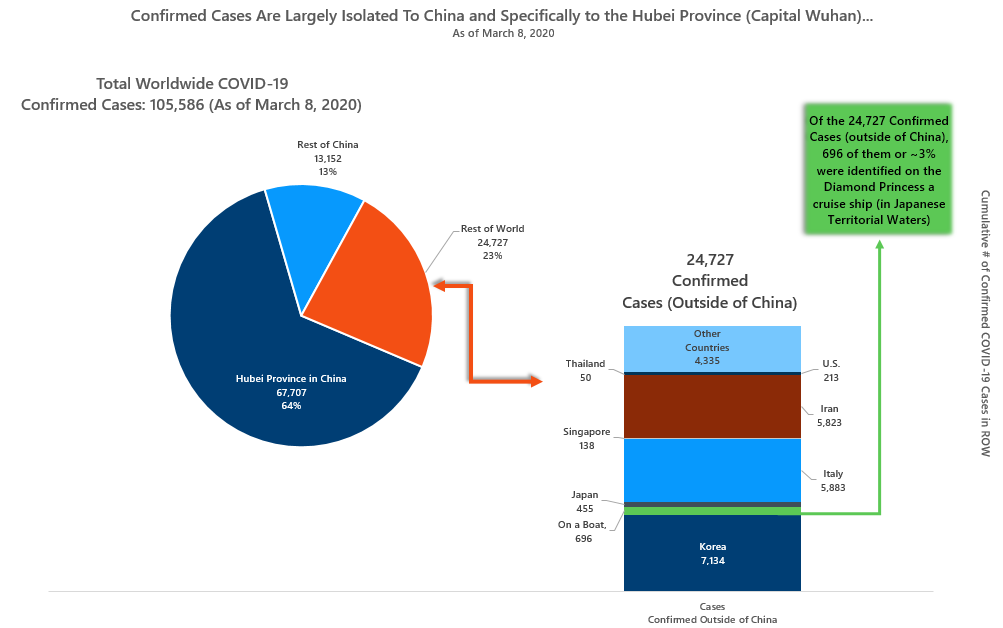

While the following chart shows that China still represents the vast majority of cases, it is important to note that the daily cases inside of China have dropped dramatically (according to the World Health Organization “WHO”). Korea was one of the countries outside of China to be hit with escalating cases. The number of new cases reported daily in Korea have also declined. Korea has reportedly been very aggressive in testing and appears to have curbed the momentum.

The focus is now elsewhere, particularly on Iran and the European region.

Exhibit 1: Tracking Recorded Cases – Shift in Focus to Outside China

Source: World Health Organization. As of March 8, 2020.

Revisiting Virus Outbreaks

While the total number of outbreaks continues to rise. It is helpful to revisit other epidemics and pandemics.

Comparing COVID-19 to Severe Acute Respiratory Syndrome (SARS)

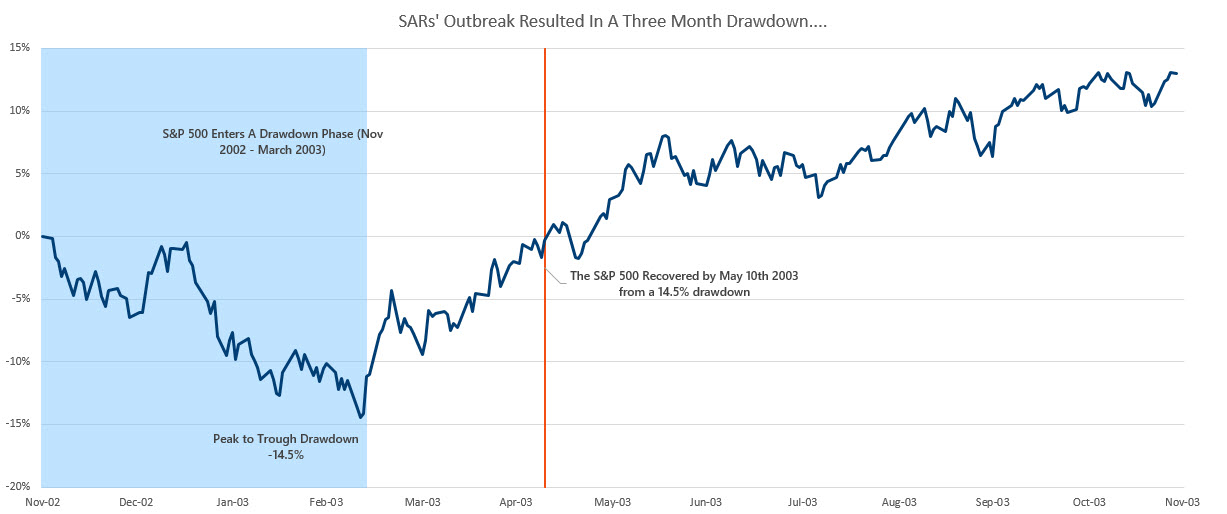

The comparison of Covid-19 to SARS has drawn the most attention. According to the World Health Organization (WHO) as of March 8th, Covid-19 has climbed to over 100,000 cases, more than estimates for SARS in 2002-03 of approximately 8,000. There were an estimated 774 deaths globally and an approximate 10% mortality rate. Here in the U.S., SARS only impacted 8 people with no reported deaths. While many issues impact the equity and bond markets, the S&P 500 did drift down approximately 14.5% during the SARS outbreak. As of March 9th, the S&P 500 was down approximately 15% year-to-date and 19% from its high on February 19th.

Exhibit 2: S&P 500 Performance During SARS Outbreak

Source: Calamos Wealth Management, Bloomberg; Past performance is no guarantee of future results.

Comparing COVID-19 to Swine Flu

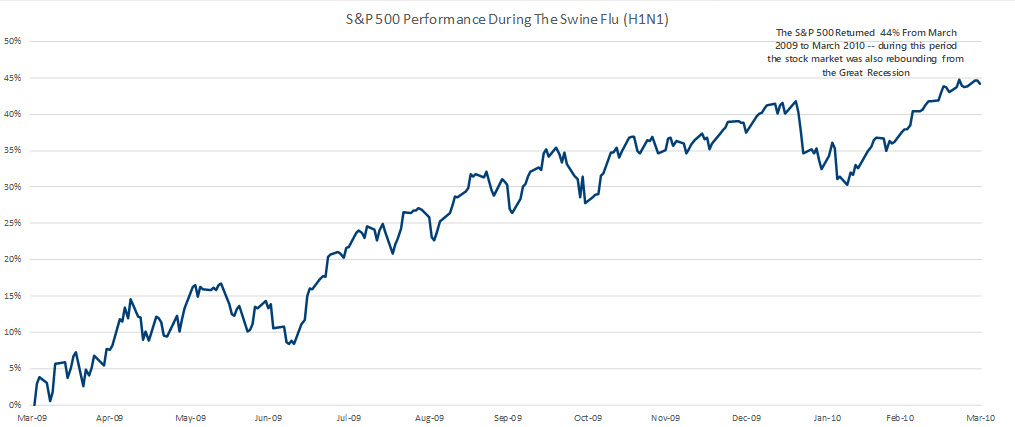

As Covid-19 is now spreading much further than SARS and we prepare for potential closing of schools along with travel and work restrictions, comparisons to the Swine Flu of 2009 is taking on more relevance. Estimates are that the Swine Flu impacted 11% to 21% of the world’s total population. In the U.S. approximately 60.8 million people were infected with 12,469 attributed deaths. Ironically, the stock market was rebounding from the Great Recession and did not encounter any meaningful decline. The market was certainly benefiting from cheap valuations and monetary and fiscal stimulus.

Exhibit 3: S&P 500 Performance during the Swine Flu Outbreak

Source: Calamos Wealth Management, Bloomberg; Past performance is no guarantee of future result.

Comparing COVID-19 to Seasonal Flu

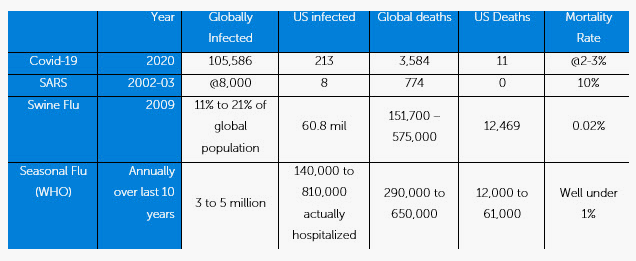

As the following table illustrates, the World Health Organization estimates that over the last 10 years, the seasonal flu has impacted 3 to 5 million people globally with nearly 290,000 to 650,000 deaths. In the U.S., estimates are that 140,000 to 810,000 have actually been hospitalized, while deaths have ranged from 12,000 to 61,000 annually over the last decade.

Table 1

Source: World Health Organization, CDC, Northern Trust. (As of March 8th 2020)

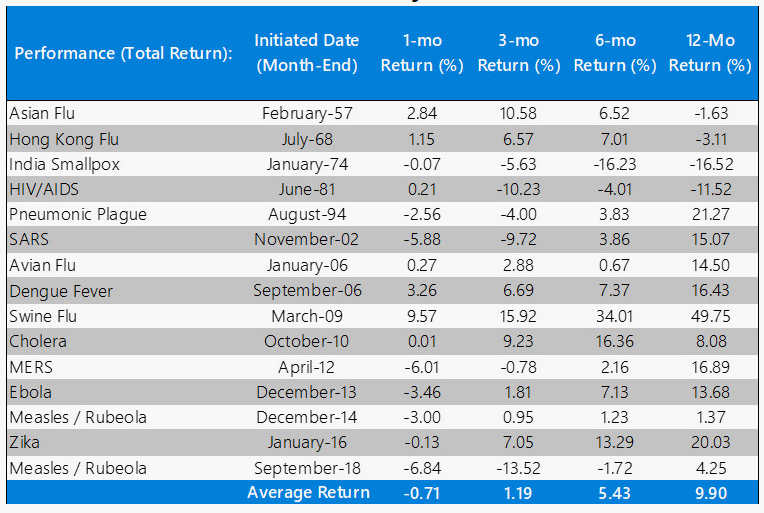

The following table shows a fuller set of epidemics and pandemics since the 1950s. As can be seen markets have generally responded favorably over the long-term as markets get back to fundamentals.

Table 2

The S&P 500 Index Tends to Historically Look Past Outbreaks

Epidemics and Pandemic episodes sourced by MarketWatch and Strategas to capture a fuller dataset. Returns calculated from month-end of publicly available outbreak dates. Sources: Bloomberg. Past performance is no guarantee of future results; Initial outbreak dates source: Asian Flu: Encyclopedia Britannica; Hong Hong Flu: Encyclopedia Britannica; India Smallpox: World Health Organization; HIV/AIDS: CDC; Pneumonic Plague: CDC; SARS: Wikipedia; Avian Flu: Wikipedia; Denigue Fever: NDTV; Swine Flue: CDC; Cholera: Foreign Policy, MERS; CDC; Ebola: New England Journal of Medicine; Measles/Rubeola: CDC; Zika: NPR; Measles/Rubeola: Discover.

The Impact of Oil Disruptions

It wasn’t long ago that the world was worried about military airstrikes between the U.S. and Iran. The concern then was that oil supplies could be disrupted, which could propel energy prices higher. Higher energy prices could essentially serve as a tax on consumers as they would have less money to spend after paying more for gas at the pumps. In our publication, Air Strikes and Oil Disruptions, we believed that we were more immune to this in the U.S. due to our energy independence.

Now the cards have changed. The primary news arresting markets on Monday, March 9th, was that Russia disagreed to a cut in production with other OPEC nations. Saudi Arabia responded over the weekend by stating they will increase production in April. While oil was already drifting down due to demand concerns on economic impacts from Covid-19, oil was down over 20% (WTI and Brent Crude Oil) on Monday. More supply on lower expected demands equates to lower prices. While this will have negative impact on countries dependent on oil exports for their budgets, it will also impact domestic shale producers. At the end of the day, this posturing between Russia and Saudi Arabia will have to be revisited as oil at $20 to $30 per barrel is not sustainable for oil exporting countries, nor shale oil producers in the U.S.

The silver lining in the short-term is that gas prices will be lower allowing for consumers to spend on other goods and services. However, this brings us back to the Covid-19 dent in consumption due to quarantines and change in life patterns.

Economic Reports May Bring More Concern

We fully expect economic news out of China to be down dramatically for the first quarter, as the government shut down businesses and quarantined regions. According to ISI, they are now expecting a potential -20% quarterly (year-over-year) decline in GDP. As China is now the second largest economy in the world, this will impact supply chains and other economies and markets. On the positive side, Chinese employees are being sent back to work and the government is stepping up with stimulus, albeit patiently. And, as many European countries were growing much more slowly, a technical recession is clearly possible.

However, central banks are intent on using monetary policy, while politicians are intent on stepping up fiscal policies.

Monetary Policy

The talk of more central bank cuts continues. This is driving down 10-year U.S. Treasury rates. Such declines in these rates suggests two motivations. First, the market believes a recession is imminent. Second, a flight to safe-haven assets is driving rates lower. The market is also naturally repricing bonds with the expectations that the Fed is going lower and could even take Fed Funds rates to 0%. We expect that central bank balance sheets will grow as quantitative easing picks back up. In the meantime, global short rates are lower.

Fiscal Policy

According to ISI, G7 finance ministers said they are ready to take actions. In recent days, Italy announced a $4 billion injection into its economy. The World Bank announced $12 billion in aid for virus support. South Korea announced a $9.8 billion stimulus to fight coronavirus. Hong Kong has announced a variety of stimulus measures including a HK$10,000 cash handout for adult permanent residents - ISI believes these measures could boost the economy by 1%. The Trump administration is now working with Congress on a variety of support measures.

U.S. Economic News

While we expect some soft economic news, economic news of the last few days has been positive. We received a very strong employment report last Friday (March 6, 2020). According to the Bureau of Labor Statistics change in non-farm payrolls increased to 273K (versus expectations of 175k). Also, the unemployment rate dropped from 3.6% to 3.5% with average hourly earnings clocked in at 3% year-over-year growth.

What’s next?

Naturally, markets are trying to look to the future. As of now the question remains as to when countries outside of China see a topping out in virus outbreaks and when government-induced economic slowing reverses. Other questions remain as to when will the markets see a transitory move to a future pick-up in economic activity after the flow-through of damage takes the U.S. economy to flat or negative growth in the second quarter? And, what additional fiscal policies are on the horizon that could help bridge tough terrain?

China may be a leading economic indicator on this front. The International Monetary Fund (IMF) suggests China is now running at 60% capacity and could be at 90% in weeks. The Chinese stock market (as measured by the MSCI China Index) is one of the best-performing stock markets year-to-date.

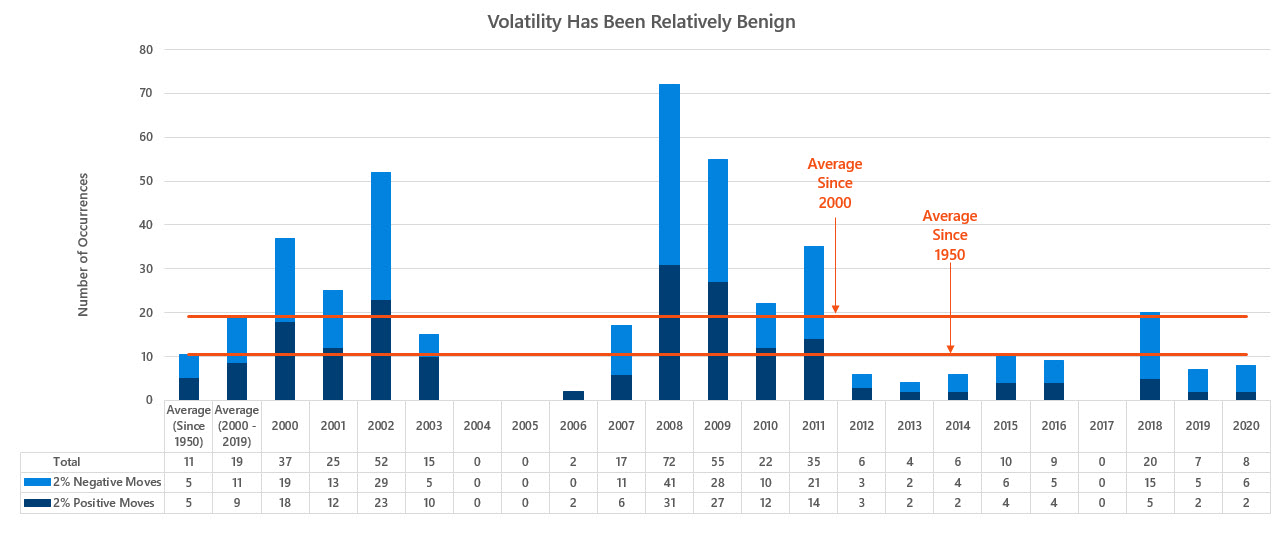

VOLATILITY & BUILDING A BASE

As we have discussed previously, we have been immune to volatility in recent years. The following exhibit shows the total number of 2% moves (up or down) by year.

Exhibit 4: Volatility Has Been Relatively Benign (2% Daily Moves)

Source: Calamos Wealth Management, Bloomberg; Past performance is no guarantee of future results.

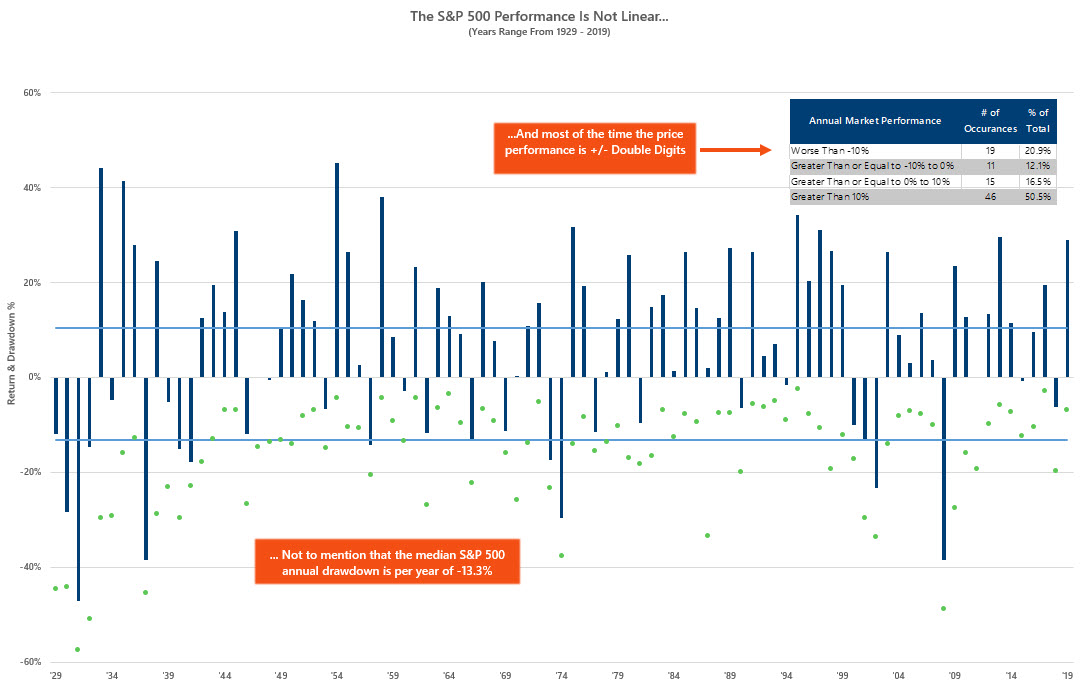

The following chart shows the S&P 500’s calendar year returns along with each year’s maximum drawdown during that year. This study shows that the average annual drawdown since 1929 has been 13.3%. Drawdowns (the percentage change of the market peak, relative to the market trough for a given year) happen during positive and negative returning calendar years.

Exhibit 5: S&P 500 Calendar Year Performance & Drawdowns

Source: Calamos Wealth Management, Bloomberg; Past performance is no guarantee of future results.

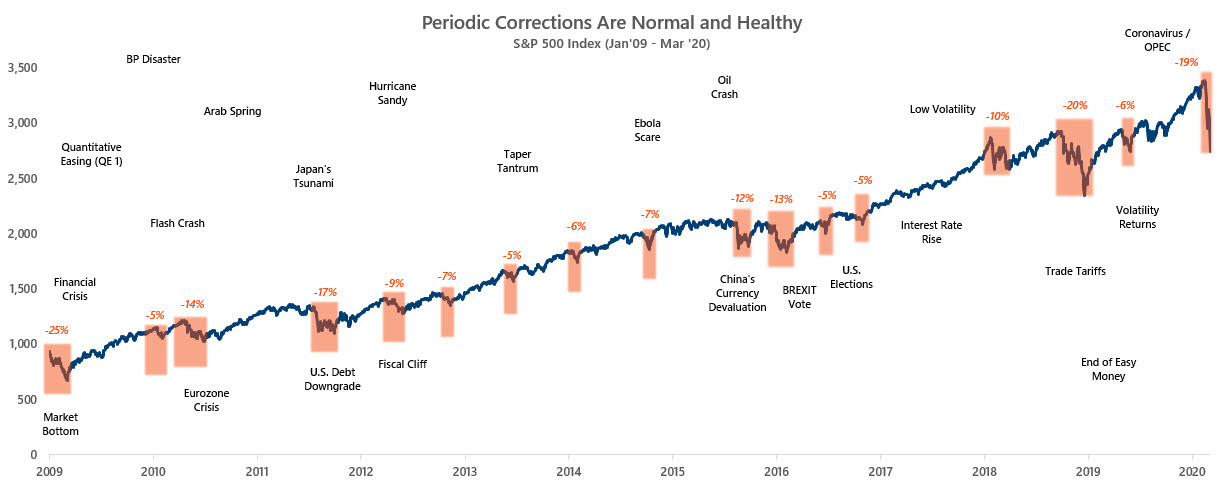

The following exhibit shows that markets have continued to climb despite set-backs. As populations grow, economies grow and captial markets grow with them over the long-term.

Exhibit 6: Periodic Corrections Are Normal and Healthy

Source: Calamos Wealth Management, Bloomberg; Past performance is no guarantee of future results. As of March 9th, 2020.

We continue to believe that the market will bounce around while countries adjust to the Covid-19 outbreak, just as China did. Markets will also adjust and eventually look through bad economic news and possible technical corporate earnings and/or economic recessions. This means that we may continue to test equity market lows until we build a base case that rationalizes a move to higher markets.

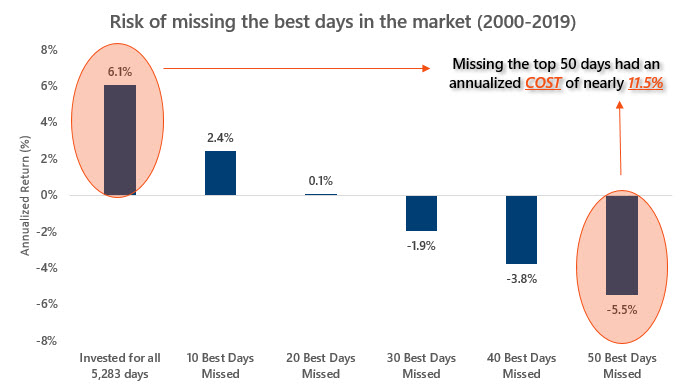

In the meantime, we recommend that investors remain with their long-term strategic plans. The following exhibit demonstrates the damage of missed opportunities when the markets decide to trade higher as they are likely to do as we bounce around up and down on a daily basis.

Exhibit 7: Risk of Missing the Best Days

Source: Calamos Wealth Management, Bloomberg; Past performance is no guarantee of future results.

RECENT LONGER-TERM PERSPECTIVE

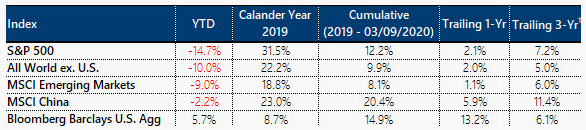

While we are not sure when this panic in the markets will subside, it is important to remember that the S&P 500 was up over 30% in 2019 and with its decline year-to-date of approximately 15% through March 9th, the S&P 500 is still up 12.2% since January 1, 2019. Similarly, the Bloomberg Barclays Aggregate bond index was up 8.7% in 2019, is up 5.7% year-to-date through March 9th, and up 14.9% since January 1, 2019.

Exhibit 8: Primary Market Returns Still Positive Over Longer Recent Periods

Bloomberg. As of March 9th 2020; Past performance is not indicative of future results S&P 500 is represented by the S&P 500 Index, All World ex U.S. is represented by the MSCI All World ex U.S. Index, MSCI Emerging Markets is represented by the MSCI Emerging Markets Index, MSCI China is represented by the MSCI China Index, Bloomberg Barclays U.S. Agg is represented by the Bloomberg Barclays U.S. Aggregate index.

We often use other asset classes and vehicles in client portfolios that not only did well in 2019, but have also done well year-to-date. This demonstrates the importance of diversification and professional, active management in constructing and managing portfolios.

The Importance of Diversification

While equity markets are down, the 10-year U.S. Treasury yield drifted down to an all-time historical low of 0.54% on March 9th from 1.92% at the beginning of the year. This means bonds should serve portfolios well as bond prices go up when interest rates go down.

Here are a few other portfolio construction reminders that should be helpful for broadly diversified, balanced investors.

- International Equities – As we discussed in our recent paper, Why International?, we believe active management is important when allocating to international equities.

- Domestic Equities - Many of our clients have defensive allocations within their domestic equity allocations.

- Global Infrastructure - This asset class also has defensive properties that we highlighted in a recent topic paper titled, Global Infrastructure Investments.

- Bonds - Bonds, specifically treasuries, serve as a “safe haven” asset during choppy markets.

- Convertibles - Provide a good diversifier and risk-adjusted profile. When volatility rises, the relative performance of convertibles tends to improve historically.

- Market-Neutral Strategies - These strategies tend to have historically lower correlations to both stocks and bonds, potentially providing good diversification with downside risk mitigation.

What to do?

Covid-19 is another exogenous reminder that market corrections occur and that balanced and diversified portfolios help investors achieve their long-term strategic plans.

While we do not yet know the full reach and impact of Covid-19 and new longer-term dynamics around oil, we do know that emotional reactions at this point would be based on unknowns and speculation. While the S&P 500 may drift lower amid this period, it is also important to note that U.S. economic fundamentals are good. There are numerous items that should eventually change the narrative for markets, possibly including continued fiscal support from central banks, more fiscal stimulus announcements from politicians (including the U.S.), Covid-19 running its course, and possible drug treatments, among others.

We will continue to monitor this situation and provide more context as events warrant.

Please remember that past performance may not be indicative of future results. Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. The information contained therein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Calamos Wealth Management LLC), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Calamos Wealth Management LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Calamos Wealth Management LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Calamos Wealth Management LLC client, please remember to contact Calamos Wealth Management LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Calamos Wealth Management LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

Diversification and asset allocation does not guarantee a profit or protect against a loss.

Quantitative Easing “QE”: Quantitative easing (QE), also known as large-scale asset purchases, is a monetary policy whereby a central bank buys predetermined amounts of government bonds or other financial assets in order to inject liquidity directly into the economy. An unconventional form of monetary policy, it is usually used when inflation is very low or negative, and standard expansionary monetary policy has become ineffective. A central bank implements quantitative easing by buying specified amounts of financial assets from commercial banks and other financial institutions, thus raising the prices of those financial assets and lowering their yield, while simultaneously increasing the money supply. This differs from the more usual policy of buying or selling short-term government bonds to keep interbank interest rates at a specified target value.

Bloomberg Barclays Aggregate Bond Index: covers the U.S. denominated, investment grade, fixed-rate, taxable bond market of SEC registered securities.

S&P 500 Index: measures the market performance of 500 large companies on the stock exchanges of the US

MSCI ACWI ex U.S. The Morgan Stanley Capital International All Country World Index Ex-U.S. (MSCI ACWI Ex-U.S.) is a market-capitalization-weighted index maintained by Morgan Stanley Capital International (MSCI). It is designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI ACWI Ex-U.S. includes both developed and emerging markets.

MSCI Emerging Markets: Index is an index used to measure equity market performance in global emerging markets.

MSCI China: China Index captures large and mid cap representation across China H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs). With 710 constituents, the index covers about 85% of this China equity universe. Currently, the index also includes Large Cap A shares represented at 15% of their free float adjusted market capitalization.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits