Executive Summary

The conventional 60/40 portfolio of today is not going to generate the kind of returns that investors say they need. Investors must seek to embrace the terrifying concept of being different. As the ghosts of many great investors past have amply demonstrated, being different is the path to investment success. However, such advice falls into the simple but not easy category, to borrow Warren Buffett’s expression.

Both human nature and the institutional imperative are serious impediments to the budding contrarian. There are few quicker ways to lose one’s job than being alone and “wrong.” But the appalling forward-looking returns to a standard 60/40 portfolio leave no choice. Owning U.S. equities today virtually ensures low long-run returns. Instead, investors should own as much international and, in particular, emerging market equities as they can.

Emerging markets are trading on a Shiller P/E of 13x. This is the level of valuation that generally gets me excited. We have not experienced permanent impairment of capital from this level outside of markets that have shut down due to war. This doesn’t guarantee short-term returns or that we have reached a bottom: cheap stocks can always get cheaper. But it does provide a compellingly attractive entry point for those with a long horizon.

Even better are the value stocks within emerging markets, which trade on single-digit Shiller P/Es. So, embrace career risk, dare to be different, and recall the motto of the Special Air Service: Who Dares Wins.

60/40 Won’t Cut the Mustard

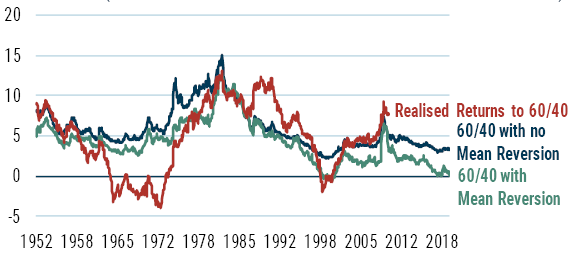

The biggest single challenge facing investors today, in my humble or otherwise opinion, is that the returns to a conventional 60/40 portfolio look set to be somewhere between very low and zero. For example, Exhibit 1 shows the expected (and realised returns) to a 60% S&P 500/40% 10-year U.S. Government Bond portfolio. If you assume mean reversion in equity market1 valuations, the return in real terms (after inflation) is on track to be around 0% p.a. for the next decade. Even if you assume valuations stay where they are in equity space, you are only looking at around a 3% return from a 60/40 portfolio.

EXHIBIT 1: EXPECTED AND REALISED RETURNS TO A 60/40 PORTFOLIO (10-YEAR ROLLING RETURNS AND FORECASTS)

As of 12/31/19 | Source: GMO

Deploying capital in a 60/40 portfolio today falls short of Ben Graham’s definition that “An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.” By investing in a 60/40 portfolio today, you are taking on risk with little to no hope of a return. Of course, as Exhibit 1 also shows, this portfolio has done remarkably well over the last decade, which makes the advice I am about to offer even more unpalatable than usual. But the past is not prologue, and few things in life are as dangerous as driving while focused on the rearview mirror.

Sadly, doing what is right is often not easy. This is as true in investing as it is in many other aspects of life. If you were to seek advice on investing from some of the great luminaries of the past, one of the common themes would surely be to take a contrarian stance. To wit, Sir John Templeton noted, “It is impossible to produce superior performance unless you do something different from the majority. If you buy the same securities everyone else is buying, you will have the same results as everyone else.” John Maynard Keynes opined, “The central principle of investment is to go contrary to the general opinion on the grounds that if everyone agrees about its merits, the investment is inevitably too dear and therefore unattractive.” In short, the ghosts of investing past would urge you to dare to be different.

Human Nature

However, such advice whilst simple is not easy (to purloin a famous modern-day contrarian, Warren Buffett’s, turn of phrase). Both human nature and the institutional imperative force us to want to behave like others. Let’s start with human behaviour. Human beings are (generally at least) a social species. Like many social species we implicitly recognise that it is warmer and safer in the middle of the herd.

It transpires that herding animals (such as zebras) don’t actually provide an accurate depiction of our species. In his wonderful book, Why Zebras Don’t Get Ulcers, Robert Sapolsky points out that although zebras may have apparently stressful lives (after all, that sound of long grass swaying might be the wind or a hungry lioness on the hunt for dinner), they have been well-honed by evolution to deal with the environmental stresses they face.

Sapolsky suggests that we humans are much more akin to baboons. He has been studying one troop of baboons for a long time, a group fortunate enough not to have to devote very much time to finding food. Regrettably, this leaves them with a significant amount of time on their hands to be unpleasant to one another, something that it turns out baboons excel at. These primates have a complex social structure and have strict social pecking orders. Sapolsky has observed that the baboons at the nadir of the social hierarchy (the socially excluded) undergo rapid weight loss, loss of hair, and even physiological changes in brain structure. It isn’t a big stretch to see similarities with humans under social pressure.

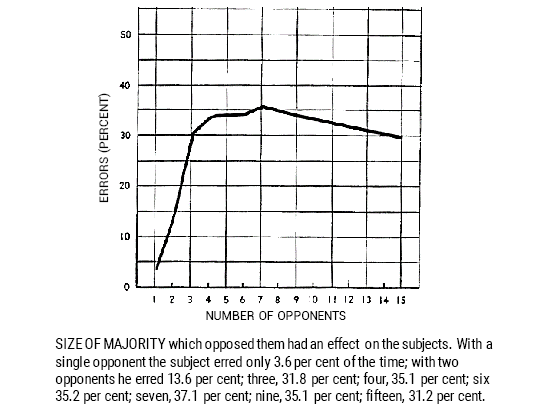

Social psychologists have studied the tendency for conformity in humans as well, represented by the classic work done by Solomon Asch in the 1950s. He set up an experiment in which a participant was asked to select which of three lines was closer to another line being shown (as per Exhibit 2). Now, this may not seem to be a hard task, but Asch had one study participant sit in a room with a number of other people who gave their answers before this lone subject did. Unbeknownst to this person, the other people in the room worked for Asch and were briefed to answer incorrectly on a number of occasions during the study.

EXHIBIT 2: THE SOLOMON ASCH EXPERIMENT

Source: Asch (1950)

Exhibit 3 shows the results from the Asch experiment. When faced with any number greater than 3 people in the room, there was a roughly 30-35% probability that the genuine study participant would go along with the clearly incorrect answer that the group was reporting. Such is the pressure to conform and be a part of the crowd.

EXHIBIT 3: CONFORMITY IN ASCH’S EXPERIMENT

Source: Asch (1950)

Just in case you were wondering about the relevance today of psychological studies done in the 1950s, it turns out that modern versions of Asch’s experiment produce very similar results.2 This is only to be expected. After all, our brains are shaped by the glacial process known as evolution and a mere 70 years is nothing on such a scale.

Other studies in the field of psychology have explored the opposite side of the equation: How does it feel when we are left out, socially excluded, and on our own? Eisenberger, Lieberman, and Williams3 designed an experiment in which the participant controlled one avatar who was playing a game of catch with two other avatars. At some point during the game, the other two ‘players’ stop passing the ball to the subject. The researchers tracked where the reaction to this behaviour was located in the brain. It happened that this social exclusion was registered in exactly the same places as real physical pain (measured by having people keep their hands submerged in buckets of ice water for long periods of time).

Effectively, the human brain has both push (the pain of doing something different) and pull (the desire to belong) factors moving it towards conformity. Taking the contrarian path is potentially akin to having your arm broken on a regular basis.

Institutional Imperative

As if these innate human tendencies were not enough, we live in a world that seems to be governed by Keynes’ edict (aka career risk):

It is the long-term investor – he who most promotes the public interest – who will in practice come under the greatest criticism whenever investment funds are managed by committees or boards or banks. For it is the essence of his behavior that he should appear eccentric, unconventional and rash in the eyes of average opinion. If he is successful, that will only confirm his rashness; and if in the short run he is unsuccessful, which is very likely, he will not receive much mercy. Worldly wisdom teaches that it is better for one’s reputation to fail conventionally than to succeed unconventionally.

Not only is doing something different likely to lead you to feel something close to physical pain, it is also very likely to get you fired. No wonder so few dare to be different.

Being Different Today

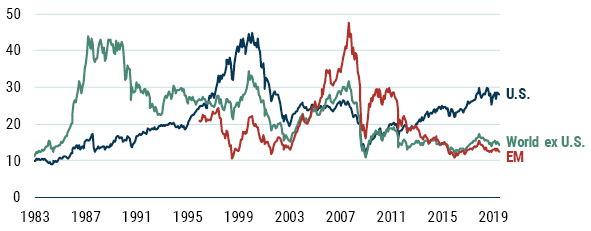

Even a cursory glance at Exhibit 4 makes obvious the valuation spread that has resulted from the massive outperformance of U.S. equities relative to the rest of the world. The U.S. stands on a Shiller P/E of nearly 30x, whilst the rest of the developed markets trade on a Shiller P/E of around 16x, with emerging markets at an even more attractive 13x.

EXHIBIT 4: SHILLER P/ES AROUND THE WORLD

As of 1/1/20 | Source: GMO

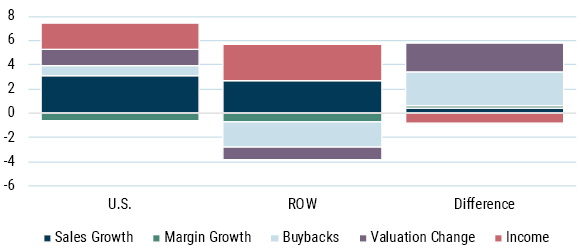

How did we end up here? Well, it turns out that almost all the U.S. outperformance can be attributed to either relative valuation expansion or relative buybacks and not to fundamentals (see Exhibit 5). I’ve written before (on multiple occasions) about the unsustainability of valuations and buybacks as sources of outperformance so I will skip a further discussion here, and instead refer those interested to previous papers.4 Although I will note that the dates of my prior pieces attest to the difficulty of timing. And, as we all know, in the short term being early is indistinguishable from being wrong.

EXHIBIT 5: THE SOURCES OF U.S. EXCEPTIONALISM RETURN DECOMPOSITION

Source: GMO

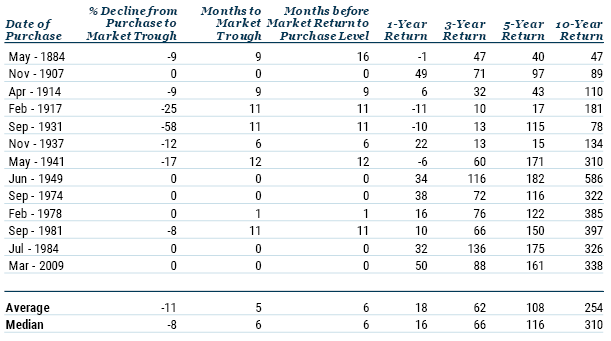

From a valuation perspective, the path to being different is clear: own non-U.S. equities and, in particular, own emerging market (EM) equities, which are very close to the levels of valuation where I get giddy. I generally regard a Shiller P/E of 13x as very attractive. The last time I was excited about anything outside of EM was over Europe in late 2011. At our client conference in October of that year I pointed out that Europe was cheap. I used Table 1 to illustrate the point, noting that the U.S. market had not witnessed a permanent impairment of capital when bought at 13x. I’m delighted to report that Europe has not provided an exception to this evidence, returning around 108% since October 2011, or just over 9.5% p.a.

TABLE 1: BUYING THE U.S. MARKET AT 13X

Source: GMO

When I was discussing the attractiveness of non-U.S. (and EM in particular) equities and the juxtaposition provided by the nosebleed-inducing valuation of U.S. equities with a colleague, he made the argument that this was a widely held view (indeed I recall him actually saying the ‘c’ word – consensus, guaranteed to make my flesh crawl). And perhaps it is a commonly expressed position, but it is certainly not reflected in prices and valuations as we saw above. Talk is cheap, and actions speak far louder than words.

You Can Do Even Better

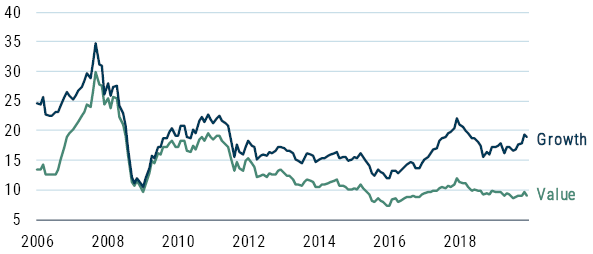

For those willing and able to truly embrace pain and career risk, the bifurcation within EM should be noted. EM value equities have dramatically underperformed EM growth equities in recent years (see Exhibit 6).

EXHIBIT 6: EM VALUE VS. EM GROWTH TOTAL RETURN (1997=1)

As of 12/31/19 | Source: GMO

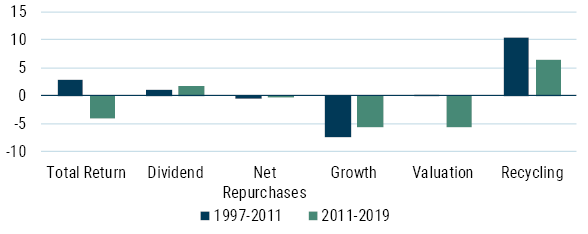

Using a framework that my colleagues Simon Harris and John Pease created,5 we can explore the sources of the value underperformance since 2012. Specifically, we are interested to see if anything ‘fundamental’ can account for the poor performance of value. The good news is that the decomposition shown in Exhibit 7 reveals that relative growth has actually been a little better (of course, value undergrows growth, but it has undergrown by slightly less than history), which suggests that the fundamentals are not driving the performance.

EXHIBIT 7: EM VALUE VS. EM GROWTH RETURN DECOMPOSITION

Source: GMO

In fact, two (inter-related) factors can be clearly seen as the source of underperformance. First, the value group has become significantly cheaper since 2012 (more on this in a minute), and second, the recycling (or migration if you prefer, which is really just value stocks working [i.e. rising in price] then exiting the value group by moving up and out of the value universe) has become lower than history. The reason that these factors are inter-related lies in the relationship between the valuation spread separating value and growth stocks. When this spread is wide, it takes a lot for a value stock to leave the value universe, hence reducing the recycling effect. Both the value of the value group and the spread between value and growth can be clearly seen in Exhibit 8.

EXHIBIT 8: EM VALUE VS. EM GROWTH SHILLER

As of 1/31/20 | Source: MSCI, GMO

Without question, the level of value offered by EM value stocks on a Shiller P/E of 9x is exceedingly attractive. Does this mean that value stocks can’t go down? Of course not. As Table 1 showed, buying when cheap is no guarantee of immediately higher returns. But it does bode well for good long-term returns. As Seth Klarman observed:

While is it always tempting to try to time the market and wait for the bottom to be reached (as if it would be obvious when it arrived), such a strategy has proven over the years to be deeply flawed. Historically, little volume transacts at the bottom or on the way back up and competition from other buyers will be much greater when the markets settle down and the economy begins to recover. Moreover, the price recovery from the bottom can be very swift. Therefore, an investor should put money to work amidst the throes of a bear market, appreciating that things will likely get worse before they get better.

To conclude, both human nature and our institutional set-up drive us to look and behave like everyone else. However, the key to good long-term investment returns lies in overcoming these hurdles and daring to be different. Today that means running as little U.S. exposure as you can and as much EM value as you can stomach. Remember the motto of the Special Air Service: Who Dares Wins.

1 I have assumed the Shiller P/E returns to be 17.5x over a decade, and that fixed income returns are not mean reverting.

2 See for instance Berns et al. (2005), “Neurobiological correlates of social conformity and independence during mental rotation,” Biological Psychiatry, 58(3): 245-253.

3 N.I. Eisenberger, M.D. Lieberman, and K.D. Williams (2003), “Does rejection hurt? An FMRI study of social exclusion,” Science, 302(5643): 290-2.

Disclaimer: The views expressed are the views of James Montier through the period ending March 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2020 by GMO LLC. All rights reserved.

© GMO

More Alternative Investments Topics >