Facing turbulent markets and concern for the health of our clients, colleagues, families, and friends, I’d like to provide you with an update on how we are managing our Asset Allocation portfolios through the current environment.

Summary

-

We believe that COVID-19 need not materially change the fair value of equity markets, although this belief assumes that governments will take appropriate steps to help economies and companies make it through the current period.

-

We continue to follow our long-term, patient, valuation-sensitive process.

-

Equities are meaningfully more attractive than they were at the start of the year, given the large fall in their price.

-

We stand ready to act as liquidity providers to capitalize on market overreactions and dislocations.

-

The opportunity set for dynamic asset allocation today remains one of the best we’ve ever encountered due to the dispersion in valuations globally. COVID-19 does not change that.

-

Assessing Fair Value (Which Has Been Remarkably Stable Historically)

Assessing Fair Value (Which Has Been Remarkably Stable Historically)

We use a long-term, valuation-based perspective to consistently rotate our Asset Allocation portfolios into what we believe are the most attractively priced areas. As with any valuation exercise, the assessment of long-term, fundamental fair value is critical to determining current attractiveness. While there will be a severe short-term economic toll (whether it is officially a recession will depend on the length of the economic shutdown, which is unclear at the moment) resulting from COVID-19, we do not believe it will have an enduring impact on the fair value of global equity capital. The fair value of equity markets has been remarkably stable historically; the only events in our experience to truly impair it have been major wars, the Great Depression, and, for global banks, the 2008-2009 Global Financial Crisis (GFC). Most recessions, even deep ones, do not leave a lasting mark on the economy or the financial markets, nor have previous global pandemics.

Case Study: Spanish Flu Pandemic of 1918-1919

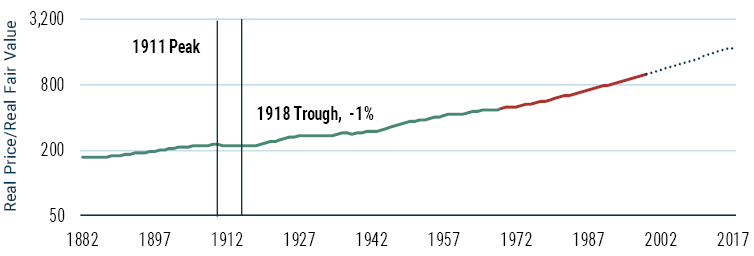

The most severe pandemic that may be in any way comparable to what would be a very bad scenario for COVID-19 was the Spanish Flu pandemic of 1918-1919. Given that it occurred more or less simultaneously to the end of World War I and was followed by a serious depression in 1920-1921, it would be difficult to determine exactly what fair value loss was driven by the pandemic, the war, or the depression. But at some level it doesn’t matter which we blame, as the loss of “clairvoyant” fair value for the S&P 500 from the peak to the trough was 1% from 1911 to 1918, as seen in Exhibit 1.

EXHIBIT 1: S&P 500 CLAIRVOYANT FAIR VALUE

Source: Robert Shiller, GMO. Clairvoyant fair value is based on the next 50 years of dividends and earnings. The red series is an approximation of clairvoyant fair value given a shorter history. The dotted series is our best guess as to what fair value has been over the past 20 years.

This is admittedly an understatement of the impact of the combined war and pandemic, as the trend growth of fair value from 1911-1918 in real terms would have been 8%, making for an aggregate loss of fair value versus expectation of a little over 9%.1 Attributing all of this to the pandemic seems unfair, however, as it implicitly assumes that World War I and the 1921 depression had no impact. For what it is worth, the U.S. stock market seemed to think the war was a bigger deal than the pandemic, as the S&P 500 fell 46% in real terms from the end of 1915 to the end of 1917 (when World War I was certainly an issue, while Spanish Flu had yet to emerge) against 5% from the end of 1917 to the end of 1919 (the period of the Spanish Flu pandemic).

Simply put, it takes an awful lot to change the underlying fair value of the market by more than a few percent. An acute event causing all companies to forgo dividends for a year would reduce fair value by the amount of the expected foregone dividends (2-4% or so at current valuations). Practically, an event has to either change the path of future return on capital for the world or cause a significant dilution event for shareholders. Widespread bankruptcies are a simple way to cause that dilution and the primary way a depression reduces fair value. Historically, we have not found any events that look to have had a long-term impact on return on capital globally.2 However, we have seen an event that caused both dilution and a return on capital fall within a major sector, and it seems instructive to look into that case to see if there are any potential parallels.

Case Study: Banks and the GFC

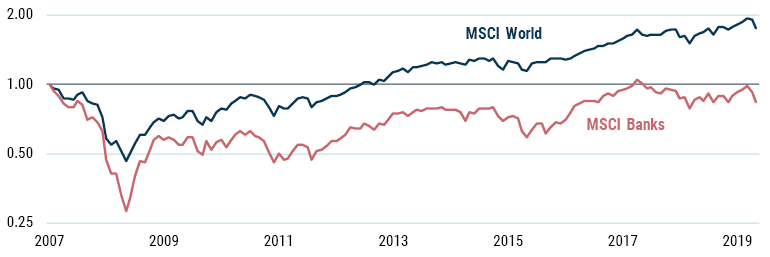

The 2008-2009 GFC constituted a large loss of fair value for the banking sector. First, banks were forced to issue significant numbers of additional shares to recapitalize themselves, and they had to do so at depressed valuations. But even beyond the dilution during the crisis period, increased capital requirements and suppressed net interest margins associated with ultra-low interest rates have impaired their return on capital. We can see the aggregate impact on their returns in Exhibit 2.

EXHIBIT 2: MSCI WORLD AND MSCI BANKS TOTAL RETURN SINCE 2007

Source: MSCI, GMO

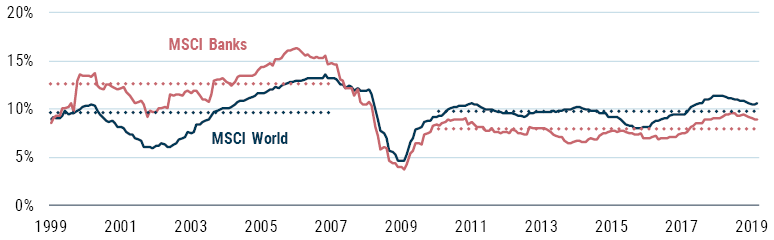

This Exhibit looks at total returns instead of clairvoyant fair value given that we haven’t had anywhere near enough time elapse since the GFC to be able to calculate clairvoyant fair value. But the combination of substantial dilution (16% net issuance by global banks from 2007-2011 versus net buybacks of 2% for the overall market in the same period) and the unique damage to bank business models stemming from regulatory change and monetary policy does give us a template of how fair value can be destroyed. Exhibit 3 shows return on economic book for the MSCI World Index and banks before and after the GFC.

EXHIBIT 3: RETURN ON ECONOMIC BOOK FOR MSCI WORLD VS. MSCI BANKS

Source: MSCI, GMO

For MSCI World, return on capital has been unaffected in the aftermath of the GFC. Return on economic book averaged 9.7% from 2000-2007 and 9.8% from 2011-2019.3 For the banks, however, return on economic book fell from 12.7% to 7.9% for those same periods. The pre-2008 figure for the banks probably owes a fair bit to the excessive leverage we saw in the sector leading up to the GFC, but even if we assume that the “true” profitability of the banking sector was equivalent to that of MSCI World in the years leading up to the GFC, the period after the GFC has seen a deterioration of about 20% in banks’ profitability.

Coordinated Fiscal Stimulus Could Turn Things Around

As we think about the economic effects of COVID-19, it seems unlikely that the world should see something approaching the kind of dilution we saw from the banks in the GFC, and it is even harder to see what kind of long- term effects might be the equivalent of banks’ return on capital challenges since the GFC. With that said, it seems highly likely that efforts to contain the virus will have a severe economic impact. The acute impact in terms of loss of economic activity will be large, larger than in a standard recession, although we can hope it might not be for as long as a normal recession. The saving grace is that since this is a truly exogenous shock, there is little harm in governments stepping in with massive fiscal stimulus to ensure that people can afford food, shelter, and medical care, and that business bankruptcies can be held to a minimum.4 The moral hazard problem associated with saving companies in a downturn simply does not apply, and the calculus on deficit spending should also be suspended in almost all cases. Right now, the focus should be on getting to the other side of this event with as little permanent harm to the population and the economy as can be managed. If that requires trade-offs in future policy flexibility, so be it. Once we get through this period, long-term expected returns on capital seem unlikely to change in a meaningful way, and therefore it is hard to imagine why this should be a material long-term negative for future growth. We have believed for a number of years that a plausibly effective way to cure the world of its addiction to low interest rates would be a meaningful globally synchronized fiscal stimulus. Suddenly, that looks like a much more likely scenario than it has previously seemed, although it is far too soon to see what effect the stimulus might have across the economy.

It may well be that in the short run the financial markets will continue to decline meaningfully before they go up. But without having better information than other investors on the likely path of COVID-19, it is hard for us to want to reduce the forecasted return on our portfolios to speculate on what reactions investors will have to uncertain news flow.

Sticking to Our Time-Tested Process

For that reason, we are holding firm in portfolios and continuing to follow our previously communicated investment process. As of today, that investment process has not led to any drastic changes in overall portfolio positioning, although we have begun to buy equities in multi-asset portfolios as our process dictates. As a reminder, our highest conviction asset classes currently are emerging markets value stocks and liquid alternative strategies, and in neither case do we believe that COVID-19 should have a material impact on medium-term expected returns.5 While U.S. equities are certainly cheaper than they were a couple of months ago, we do not believe they are yet at fair value (as of March 16th). Of course, market conditions have the potential to change rapidly. We are constantly evaluating the markets and stand ready to act as a liquidity provider and take advantage of opportunities if handsomely rewarded; we are likewise prepared to manage risks as necessary.

Each GMO investment team responsible for underlying strategies is conducting independent research and making investment decisions based on its analysis and the parameters of its strategy. Portfolio managers and research analysts across GMO have met multiple times to discuss our views of recent events and the potential future impacts of COVID-19. We are sharing our analyses and portfolio responses across teams and are similarly sharing our analyses of future potential investment opportunities that may arise if economic conditions were to materially worsen. The Asset Allocation portfolios are fortunate to benefit from the experience and research of every investment team at GMO.

As we have referenced since last fall, the opportunity set for dynamic asset allocation today is one of the best we’ve ever encountered, due to the dispersion in valuations globally. COVID-19 does not change that. We believe we are being well compensated to take risk in several areas, and we have positioned the portfolios in assets that we believe are priced to deliver strong returns going forward. The beauty of our approach is that it does not depend on a single call about a market catalyst (such as a projection for the progression of COVID-19). Instead, our approach relies on our 32 years of experience assessing valuations and market conditions and our willingness to bear risk when we are adequately compensated for doing so.

Thank you for your continued confidence in GMO.

Sincerely,

Ben Inker

Head of the GMO Asset Allocation Team

© GMO LLC.

© GMO

Read more commentaries by GMO