Want to read more by Guggenheim Investments? Visit their Featured Firm page here

Is this turning out as badly as you thought it would?

First, the economic data seem worse than I had expected. The economic drawdown is going to be bigger than I originally thought, and we are currently estimating an economic contraction of well over 10 percent this year. Second, the Federal Reserve’s (Fed) response has been really good. They’ve managed to stem the liquidity crisis in the market pretty quickly with programs that intervene directly to stabilize markets. Third, the response out of Congress and the White House has been disappointing. The programs that have been put in place likely will not be anywhere near sufficient and, in some cases, they are somewhat misguided. Extending and increasing unemployment benefits is very good but sending out $1,200 checks to lower- and middle-class families is not going to have the kind of impact that we need to keep the economy going.

Probably the most surprising thing to me at this point is how well the markets are holding up. Given the economic data, and given the fact that large portions of the capital markets are still virtually closed for business, I would have expected stock prices to be lower at this point.

How are you allocating capital as the pandemic progresses?

Coming in to this period we were very conservative. We were concerned about valuations being too high and thought that interest rates could sink lower. We believe that this has left the portfolios we manage for clients in a terrific position to take advantage of opportunities that are being uncovered. At this point, we are opportunistically trying to move from some of our more conservative investments to securities that, in our view, look attractive. We are looking at investment-grade corporate bonds and municipal bonds, and select securities in structured credit and high-yield, where prices have dropped and spreads have widened significantly, look interesting. As this situation continues to play out, we will slowly increase our risk tolerance and watch for more buying opportunities.

As I have said before, we are in the value ZIP Code, and bonds are historically cheap, so it would be foolish to remain underweight. It’s time to start nibbling, not gorging on these values. At the very least it is probably best to get to neutral versus the benchmark, which is the position to which we have moved.

How cheap are corporate bonds and asset-backed securities right now? Looking at the historical spread relationships to U.S. Treasurys for domestic debt markets, virtually every sector is at or near extreme wides. But we still expect spreads could spike wider from here, and these kinds of spikes in the past have not always been short-lived. This is why we are still cautious.

Current Sector Valuations Are More Attractive, But the Selloff Is Not Over

Fixed Income Spread Percentiles (% of Time Spent at or Below Current Spreads Historically)

Source: Guggenheim Investments, Credit Suisse, BAML, Bloomberg Barclays. Data as of 4.2.2020. Index Legend: Credit Suisse Leveraged Loan Index, Credit Suisse High-Yield Corporate Bond Index, Bloomberg Barclays Investment-Grade Corporate Bond Index, Bloomberg Barclays US Aggregate Index (Agency Bond subset), Historical CLO spreads provided by Bank of America Merrill Lynch Research, current CLO spreads based on JP Morgan CLOIE Index, Non-agency CMBS spreads provided by JP Morgan Research.

What aren’t you buying?

It is difficult to try to buy what has really been hammered. Some of the hospitality stocks and airline stocks, for example, could be a death trap—some of them may never come back. One place to look for opportunity is in companies that will perform in what I expect to be a resurgence in the United States in manufacturing.

But one thing I would caution is that if earnings continue to fall as I expect them to, S&P earnings could get as low as $100 this year. Given the traditional market multiple of about 15 times earnings, that would put the S&P at about 1,500, still about a thousand points lower than we are today. Certainly, we are down from the recent peak of 3,386, so we’ve made a big move, but we still have a pretty good move to make. Investors should probably focus their activity on bonds at this point.

We need to see the other shoe drop. When the markets start to see some of the data on unemployment rising and economic growth and corporate earnings contracting, there will be another level of panic in the market. The most likely indicators that will coincide with a buy signal would be a sharp rise in the unemployment rate and a continued fall in the ISM Manufacturing Index.

How do you see the energy business?

Again, some companies are never going to come back. Many of the exploration and production companies will likely be gone if they can’t consolidate, get a bailout, or recapitalize. Companies like Exxon and the major integrated energy companies look interesting, but it’s still a dicey call and I would hold off. Our models show oil prices continuing to drop, with prices possibly getting into single digits. There are some scenarios we’re running where oil prices could go negative. That may sound crazy, but oversupply could get so bad that there is a point where producers would actually be willing to pay to have oil taken off their hands rather than to store it. I’m not predicting a negative price of oil, but it’s easy to see how oil could get in a range between $5 and $10 a barrel. Oil got to $10 a barrel during the Asian crisis in 1998, so I don’t see any reason why it couldn’t happen again.

The large integrated companies will be able to weather the storm, but for smaller producers it will likely be the end of the road unless there is some government intervention to save them, beyond a deal between the Saudis and the Russians. The demand side of the equation has fallen off so dramatically, that even if we can get a deal between major producers, we would still probably have about 5 million barrels per day (MMbbl/d) of excess production for the full year. And that’s a lot higher excess production than we had back in 2015-2016 when we saw oil plummet from $107 down to $26. So, we’re far from out of the woods on the oil crisis.

The nearby chart shows three scenarios for our oil supply model. Each case keeps the demand assumption constant—we assume that demand falls compared to last year by about 20 MMbbl/d on average over April and May, and gradually recovers to pre-coronavirus levels by mid-2021—and then we adjust our supply assumptions for OPEC and the rest of the world. Case 2, which models an OPEC deal and moderate cuts from other global producers, shows the average excess supply production over the rest of 2020 is 5.1 MMbbl/d. This excess supply will put enormous pressure on global storage capacity, which will likely push prices even lower.

Possible Paths for Global Excess Oil Supply

MMbbl/d, Quarterly Average

Source: Guggenheim Investments, IHSMarkit. Actual data as of 12.31.2020 and estimates through 3.31.2020.

Are there any areas of the market that are particularly concerning to you?

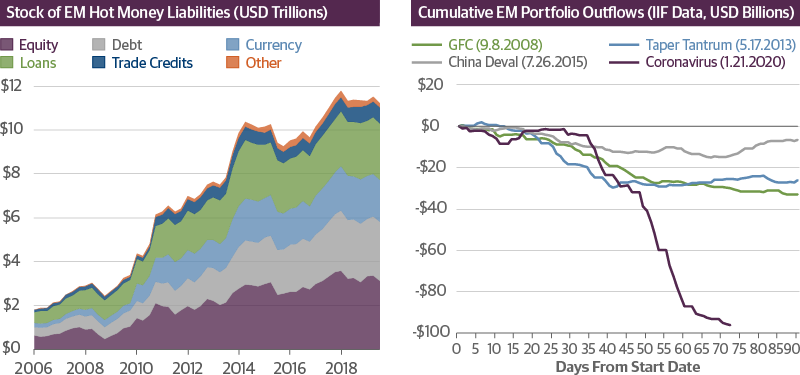

Emerging markets could be the next domino to fall, and we are keeping an extremely close eye there. As a percentage of gross domestic product (GDP), the emerging markets have significantly more debt today—over 180 percent—than they did back at the time of the Asian crisis—approximately 110 percent.

Emerging Markets Are Highly Vulnerable in This Environment

Emerging Market Debt to GDP (Corporate + Government)

Source: Guggenheim Investments, IIF. Data as of 9.30.2019.

The big difference now is most of the sovereign debt is denominated in their local currency, whereas in the Asian crisis it was denominated in dollars. But the other side of the coin is that we now have record amounts of dollar-denominated corporate debt issued by emerging markets companies. If a country has a dollar shortage, the Fed and the International Monetary Fund are there to work with them and help stall out the problem. But there never has been a testing of the collapse of private sector debt out of the emerging markets since the 1930s, and that instability could easily arise there. We will also see higher domestic interest rates in emerging markets as government deficits in those countries are swelling and there is more and more pressure on their central banks to help accommodate the supply of government debt. All of this puts downward pressure on the local currency, and that puts more pressure on the corporate sector.

We have also seen that the amount of “hot money” capital—equity, debt, currency, loans, trade credits—going into emerging markets has exploded over the last decade. Those inflows will turn to outflows during a crisis, which also spells trouble. So, all in all, not a pretty picture in emerging markets.

An Emerging Markets Crisis Could be the Next Shoe to Drop

Source: Guggenheim Investments, Haver, IIF. Data as of 9.30.2019 (LHS) and 4.1.2020 (RHS).

What is your longer-term view on rates?

As John Maynard-Keynes once said, “In the long run we are all dead,” but I still like to get perspective on the long run. Having said that, after such a large dose of fiscal and monetary stimulus with these high levels of debt in the United States and around the world, it’s likely that at some point the scale will tip from deflation to an inflationary spiral. When that happens, we will start to enter the bear market in bonds. But this won’t happen for a number of years.

To put this all into perspective, the stock market crash of 1929 was the beginning of an era of extremely low interest rates. That era of low rates ended 22 years later, in 1951 with the Fed-Treasury Accord, when policymakers essentially decided they were no longer going to try to hold down rates to keep the economy expanding. Here we are now, 12 years after the beginning of the financial crisis, and policymakers were essentially doing the same thing before the pandemic hit.

At this point, policy is primarily focused on driving long-term rates as low as possible and keeping them there. We likely will succeed in the near term.

But someday the pandemic will end. In terms of output, it will take about four years to get U.S. GDP back to where it was at the end of the fourth quarter of 2019. Using the timescale above, it will be four years from now, and then another eight years, before policymakers contemplate the idea of raising interest rates significantly. For the near term, we don’t need to worry about rates rising, and I encourage investors to buy high-quality, long-duration bonds as a way to keep income up during this long period of very, very low interest rates. Ultimately, we will get through this, but if interest rates go as low as we think, there’s little risk in owning long-duration fixed-income assets.

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Investing involves risk, including the possible loss of principal. Investments in fixed-income instruments are subject to the possibility that interest rates could rise, causing their values to decline. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

©2020, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.