Executive Summary

As Covid-19 continues to dominate headlines around the world, we have been working to develop a methodology that will help us position our portfolios as we deal with the current and coming shocks to Emerging Market economies. We believe assessing the unique risk factors that the virus brings along with understanding a country’s ability to mitigate those risks is key to determining how well that country will navigate the current crisis. This paper introduces the framework we have developed to further help us make the best decisions for positioning our portfolios.

We thought long and hard before adding to the reams of Covid-19 related reading material our clients likely have littering their virtual desks. Yet, the lack of a coherent framework to address the vulnerability of the Emerging Market (EM) equities asset class during this crisis compelled us to write. It is well understood that Covid-19 will impact economic activity, but there has been far less focus on the capital market fallout of the pandemic, which will be particularly acute in emerging markets. Of course, not all EM countries will be affected similarly given these nations vary in their resilience and ability to respond and bounce back. As investors, it is critical to understand the factors that both contribute to and detract from a country’s efforts to move forward once the imminent danger of this pandemic has receded.

In our 2013 paper, “Health is Wealth,”1 we argued that resilient domestic consumption is a function of effective public spending on health care, and we have been using this premise over the years as a key input in our top-down ESG models. In this paper, we present observations from our proprietary “Covid-19 Risk Assessment” framework, which identifies where EM countries fall on the vulnerability scale. We then couple these findings with information gleaned from our “Ability to Respond” framework, which uses several factors to determine the strength of a country’s ability to combat and recover from the virus. Using this methodology, we are able to identify the “clusters” of countries that we believe will be more resilient as this crisis and its aftermath unfold.

Key Takeaways

The headline results regarding EM vulnerability/ability to respond to Covid-19 derived from this new methodology, which is described more fully in the sections that follow, are:

- About 60% of the MSCI EM index comprises countries that rest in what we define as a “safe cluster.”

- Countries falling in the “high risk cluster” represent 14% of the index.

- There is significant variability among countries in their ability to respond to a crisis.

- It is very difficult for EM countries to implement measures like “social distancing” when per capita incomes are one-sixth those of Developed Markets (DM); a “daily” wage sustains 20% of the ex-China EM working population.

- Unlike previous crises, when index composition was poor, we now think EM countries are better-equipped to manage severe drawdowns. (Recall that drawdowns were 60% during both the 1997 Asian Financial Crisis and the 1998 Russian Financial Crisis.)

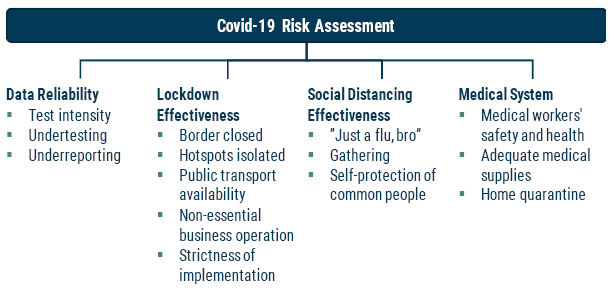

Covid-19 Risk Assessment Framework

Our framework distributes 15 factors across 4 broad categories: data reliability, lockdown effectiveness, social distancing effectiveness, and medical system (see Exhibit 1). For each factor, we assign a score of 0 to 10, with 0 being the best and 10 being the worst. Our scoring methodology incorporates inputs from individual country analysts, local social media analysis, and Google mobility data.

EXHIBIT 1: COVID-19 RISK ASSESSMENT FRAMEWORK

Source: GMO

The inputs for each of the factors grouped into categories in the framework are briefly described as follows:

- For data reliability, we look at test intensity (measured by positive results as a percent of total tests administered) and signs of underreporting/undertesting. For example, in Korea each citizen is entitled to a set of three tests free of charge. As of early April, approximately 1 of every 100 in a population of 51 million has been tested. Taiwan is also noteworthy, and we recommend reading a recent article by Wang, et al.2

- We place significant emphasis on countries that impose lockdowns given the fragile medical systems in many of these regions.

- Social distancing is a luxury in a number of countries. India and Indonesia, respectively, have 24% and 15% of their labor force constituted by casual workers who effectively depend on daily wages, making extended lockdowns extremely difficult. We also take into account that heads of government in several countries continue to exhibit a very cavalier attitude toward virus mitigation recommendations.

- Lastly, we look at the medical system from the perspective of the protection of medical workers, quality and quantity of medical supplies, and, most importantly, whether or not home quarantine is practiced when infection is confirmed.

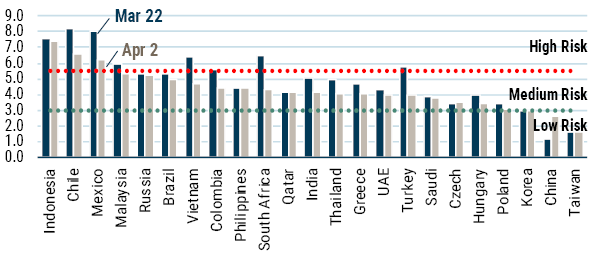

Experience in DM has taught us that once the early window for virus detection is missed, it might be too late. We took this into consideration after we developed a methodology for arriving at a Covid-19 risk score. This ranks each country by how many cases of Covid-19 exist per million within that country’s population. DM experience once again shows that once this number rises above 100 infections, the spread of the virus is difficult to contain. Exhibit 2 shows the risk scores of EM countries at two points in time: March 22 and April 2. Though this data is very fluid, it is clear to see which countries face the greatest challenges and which countries have been able to better reduce risk.

EXHIBIT 2: COVID-19 RISK SCORE

Source: GMO

Note: Below 3 = Low Risk; 3-5.5 = Medium Risk; Above 5.5 = High Risk

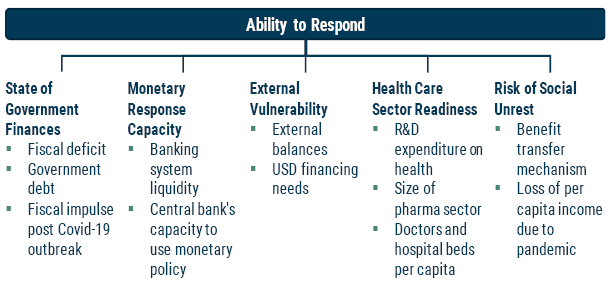

Ability to Respond Framework

Output from the Risk Assessment framework is just one piece of our analysis. We have also built a framework to assess the ability of different EM economies to respond to Covid-19. In this framework, we employ a total of 12 factors across five categories: state of government finances; monetary response capacity; external vulnerability; health care sector readiness; and risk of social unrest (see Exhibit 3).

EXHIBIT 3: ABILITY TO RESPOND FRAMEWORK

Source: GMO

Similar to the Covid-19 risk score, the ability to respond score ranges from 0 to 10, with 0 being the best and 10 being the worst. The state of government finances and central bank balance sheets will determine the quantum of stimulus countries can undertake to address macro challenges. External vulnerability helps in assessing the level of capital outflows as demand for U.S. dollars (considered the “safe haven” currency) rises in times of crisis. Health care sector readiness shows us how well-equipped the existing medical infrastructure is to fight the pandemic. We also assess the likelihood of social unrest in EM economies due to prolonged lockdowns. These factors will play a crucial role in a country’s ability to fight the pandemic and mitigate a significant economic fallout.

The economic stimulus packages announced by EM countries post the Covid-19 outbreak range from as low as 0.3% of GDP to as high as 17% of GDP. We looked beneath the headline numbers and found that the size of the fiscal measures is actually relatively small. Support measures from the banks and other non-financial government-linked companies in the form of loan guarantees, debt moratoriums, soft loans, etc., are far larger. We argue that these relief measures are essential, but do not necessarily stimulate spending. For example, Malaysia has so far announced fiscal packages amounting to 17% of GDP. However, if we look into the details, its actual fiscal deficit will rise by only 0.6% of GDP in 2020.3

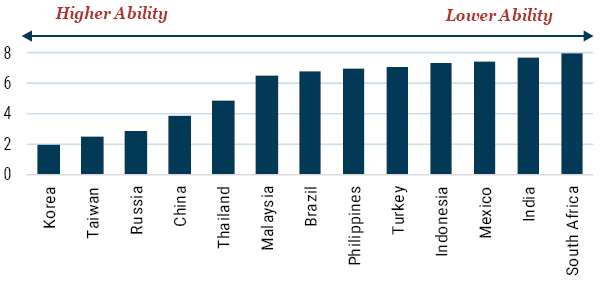

Assessing these factors together, we find South Africa, India, Mexico, and Indonesia with the least ability to respond. Korea, Taiwan, Russia, and China score the best (see Exhibit 4).

EXHIBIT 4: ABILITY TO RESPOND SCORE

Source: GMO

Combining Covid-19 Vulnerability along with Ability to Respond to Identify Safe and Risky Country Clusters

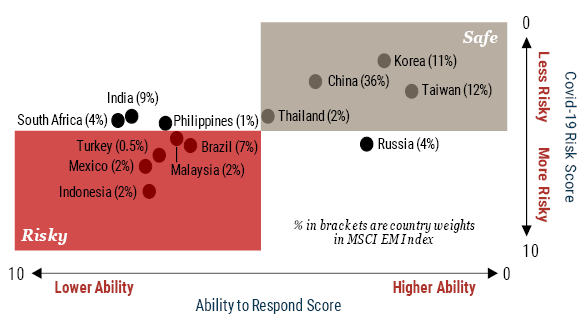

Exhibit 5 plots the Covid-19 risk score and the ability to respond score together. The result of combining the two scores gives us a clearer understanding of a country’s ability to mitigate the risks presented by the pandemic. Our data indicates that China, Taiwan, and South Korea, which together account for 60% of the MSCI EM Index, are relatively safer countries. Indonesia, Mexico, Turkey, Malaysia, and Brazil, with a combined 14% weight in the index, are the higher-risk countries.

EXHIBIT 5: COMBINING COVID-19 VULNERABILITY ALONG WITH ABILITY TO RESPOND

Significant Divergence among EM Countries' Ability to Recover from Covid-19

Source: GMO

Note: While Turkey had improved its Covid-19 risk score from March 22 to April 2, its cases per million reached 221 as of April 2. DM experience shows once this number rises above 100, the virus is fairly difficult to contain. Therefore, we still categorize Turkey as a high-risk country.

Conclusion

We of course acknowledge the subjectivity inherent in risk assessment. However, we believe the above methodology is a logical way to analyze risk. After all, investing is all about probability, and these frameworks help us mitigate some of the risks by creating a well-diversified portfolio. In our Emerging Domestic Opportunities Strategy, we were already underweight countries in the “risky cluster,” but have increased this defensive positioning recently based on the results of this new framework. We will continue to keep a close eye on this constantly evolving situation.

Acknowledgement: The authors would like to thank Mehak Dua for her many contributions to this paper.

2 C. Wang, C. Ng, R. Brook, “Response to Covid-19 in Taiwan: Big Data Analytics, New Technology, and Proactive Testing,” JAMA, March 3, 2020.

3 Nomura estimates.

Disclaimer: The views expressed are the views of Amit Bhartia, Tiger Tong, and Uday Tharar through the period ending April 16, 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2020 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO