Chief Economist Scott Brown discusses current economic conditions.

The broad range of economic data signal that a recession began in March. Real Gross Domestic Product (GDP, the total of final goods and services produced in our economy) is expected to have fallen in the advance estimate for 1Q20. The 2Q20 figures will show an unprecedented decline in activity. Weekly claims for unemployment benefits suggest that the pace of job losses has slowed in the last few weeks, but the pace has remained exceptionally high. One in seven U.S. workers has filed a claim in the last five weeks. Meanwhile, lawmakers in Washington approved another $484 billion in fiscal aid, bringing the total so far to about $3 trillion.

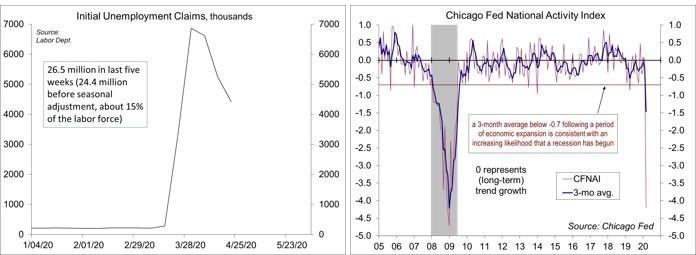

Some 26.5 million workers filed a claim for unemployment benefits in the last five weeks. That figure is inflated a bit by the seasonal adjustment (unadjusted claims normally trend low in the spring). However, we know that not every laid-off worker can file a claim. Still, the magnitude here is gut-wrenching. Prior to seasonal adjustment, 24.4 million people filed in the last 12 weeks. That’s nearly 15% of the labor force or one in every seven workers. The government will provide extended unemployment benefits and expand eligibility, but the loss of income will, in turn, reduce spending – and that spending is someone else’s income. Second- and third-round effects will add to economic weakness in the near term and hinder the recovery process. However, fiscal stimulus will help to counter those effects.

Weakness in retail sales and industrial production in March was severe enough to generate declines in quarterly figures. The Chicago Fed’s National Activity Index, a composite of 85 economic indicators fell sharply, and the three-month average, at -1.47, was well below -0.70, the level associated with an increased chance that a recession has begun. The National Bureau of Economic Research’s Business Cycle Dating Committee (BCDC) defines a recession as “a significant decline in economic activity spreads across the economy, lasting from a few months to more than a year.” There is no set definition of “economic activity,” but the BCDC takes that to mean various measures of broad activity, such as GDP, nonfarm payrolls, and inflation-adjusted personal income. To pinpoint starting and ending dates for a recession, the committee also looks at two indicators that don’t cover the broad economy, inflation-adjusted business sales and industrial production. Payrolls and industrial production have declined. Other indicators are likely to echo that when they are released. Still, while confirmation of a recession should be no surprise, the main concern is how rapidly this downturn has taken place. Moreover, there is no sign of a bottom.