Join us and Calamos Investments for our upcoming webinar: Adding Convertible Strategies to Your Playbook on May 7th at 2 pm ET. Register now.

In a turbulent period for the markets, Calamos has been hosting a Calamos CIO Conference Call series for investment professionals.

Below are notes from a call Wednesday, April 29, with Eli Pars, CFA, Co-CIO, Head of Alternative Strategies and Co-Head of Convertible Strategies, Senior Co-Portfolio Manager, and Jason Hill, Senior Vice President, Co-Portfolio Manager. To listen to the call in its entirety, go to https://www.calamos.com/CIOmarketneutral-4-29

For highlights on last month's calls, see this post.

The dual strategies of convertible arbitrage and hedged equity helped Calamos Market Neutral Income Fund (CMNIX) weather the recent drawdown while being positioned for future opportunities.

“We’re never happy with a negative number, but the fund held up quite well, given the magnitude of the drawdown. And,” Pars noted, “it’s participated in the recovery and rally back.”

During the drawdown, convert arb behaved largely as it has in previous drawdowns, although Pars noted that forced selling didn’t occur to the extent it has previously. However, there was some price discovery, which the fund was able to take advantage of. While convert arb was flat to slightly down, that created significant embedded value, which the fund began to realize as the market recovered.

Pars also commented on the issuance market, where issuance is 60% higher year over year. Convertibles are being issued by more household names than have been seen recently, including Carnival, Booking.com, Priceline, Southwest Airlines and well known retailers.

The hedged equity book has also added value by participating in the market’s bounce back. The focus there, according to Pars, is to keep the risk profile in line. Selling calls has been more lucrative but puts continue to be expensive. During the market’s rally, the team continues to add puts, whose objective is potential downside risk mitigation.

Within the Beta Range

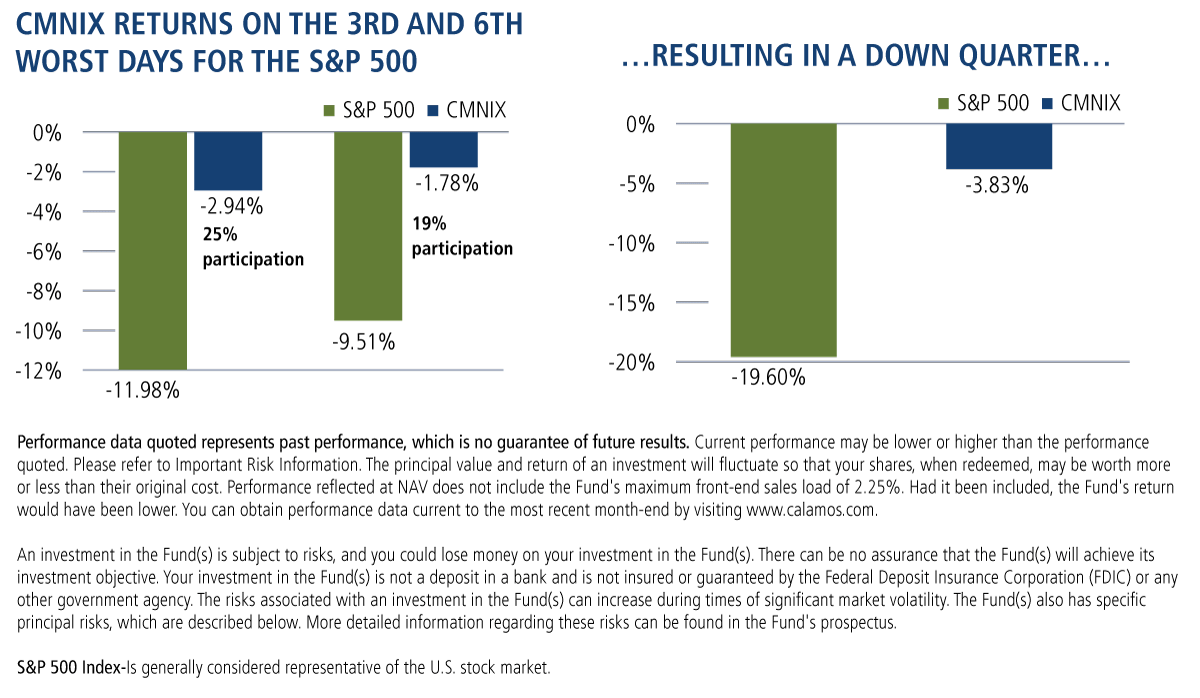

The PMs acknowledged the challenges of the unprecedented volatility, which included the VIX peaking above 80 on March 16. Even so, the participation in the drawdown on those days was still in range with the fund’s longer term beta range of 10 to 30.

March 16 and March 12 were the worst days of the drawdown, and they were the third and sixth worst days, on a percentage basis, in the history of the S&P 500. They led to a rare down quarter for CMNIX.

“With one-day moves of this magnitude, we’re just not going to have as many levers to change our potential returns in the short term,” said Hill. “With convertible arbitrage, for example, a lot of that strategy is about accruing and capturing value over time, so you won’t see that flow through immediately.”

Convert arb was selling off as the market declined, and rallying as it climbed—what Hill called a short-term phenomenon that isn’t sustainable, which may result in reduced beta longer term.

Most important, the team was able to stay opportunistic in each strategy in order to shape the portfolio going forward.

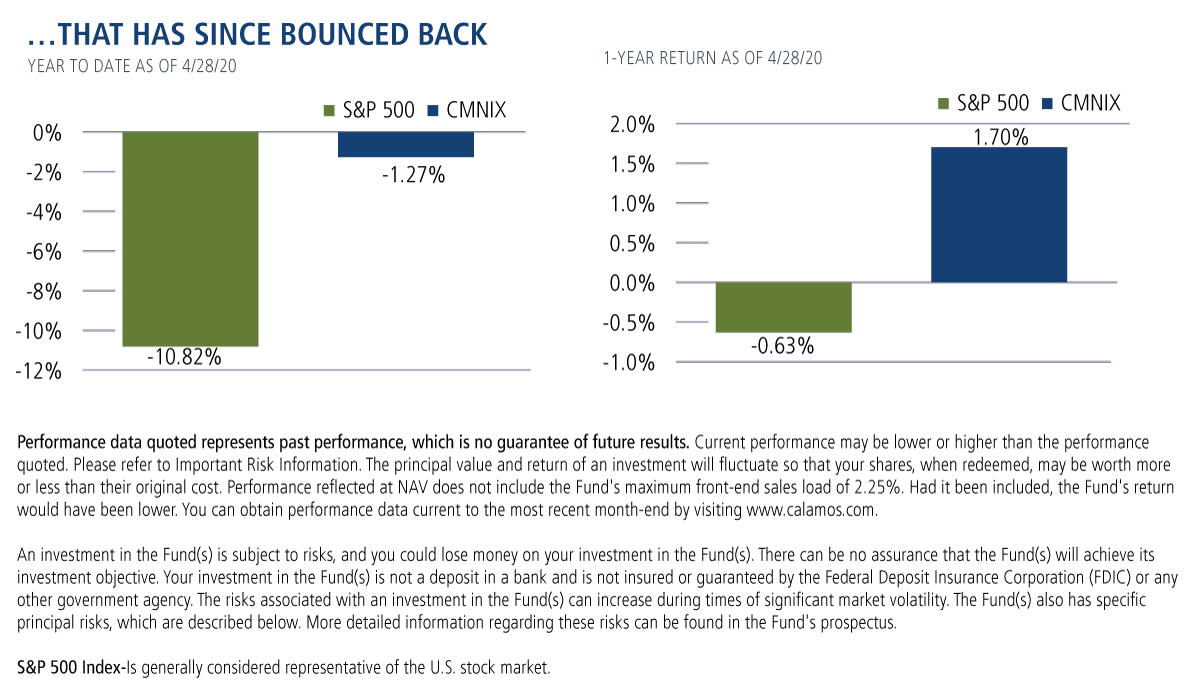

“Over time you’re able to see this vet out in the returns, even by looking at a little bit longer time horizon—such as the year-to-date performance. We’re very happy with that amount of downside when being compared to the equity markets and how much risk we are taking/not taking,” said Hill.

Less than a month after the quarter end, the fund had a -1.27% return year-to-date and its one-year return as of April 28 is 1.70%.

Fixed Income Alternatives May Be More Compelling

Asked for his view on the current level of interest rates, Pars said, “We don’t have a whole lot of rate risk or rate opportunity. We have earned a return that looks sort of like fixed income but we go about it a different way.”

Reduced interest rates detract from what can be earned on convert arb. But, Pars said, “The cheapness we see in the new issuance and secondary markets gives us a tailwind that offsets the rate move, at least for 2020.”

Pars acknowledged the challenge facing the Treasury investor.

“With the 10-year Treasury at 60 basis points, you’re going to get a 6% total return in the next 10 years. Now you may get that quickly if rates continue to rally but that’s all you’re going to get, in 10 years. That’s not particularly compelling, and that’s why we think alternatives are an interesting part of the conversation right now,” he said.

Investment professionals, for more information about CMNIX, please contact your Calamos Investment Consultant at 888-571-2567 or [email protected].

Before investing carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-800-582-6959. Read it carefully before investing.

Opinions are subject to change due to changes in the market, economic conditions or changes in the legal and/or regulatory environment and may not necessarily come to pass. This information is provided for informational purposes only and should not be considered tax, legal, or investment advice. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund's prospectus.

The principal risks of investing in Calamos Market Neutral Income Fund include: equity securities risk consisting of market prices declining in general, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, convertible hedging risk, covered call writing risk, options risk, short sale risk, interest rate risk, credit risk, high yield risk, liquidity risk, portfolio selection risk, and portfolio turnover risk.

Options Risk—the Fund's ability to close out its position as a purchaser or seller of an over-the-counter or exchange-listed put of call option is dependent, in part, upon the liquidity of the options market. There are significant differences between the securities and options markets that could result in an imperfect correlation among these markets, causing a given transaction not to achieve its objectives. The Fund's ability to utilize options successfully will depend on the ability of the Fund's investment advisor to predict pertinent market movements, which cannot be assured.

Convertible Arbitrage Risk: If the market price of the underlying common stock increases above the conversion price on a convertible security, the price of the convertible security will increase. The fund’s increased liability on any outstanding short position would, in whole or in part, reduce this gain.

Beta is a measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole.

802008 0420

© Calamos Investments

© Calamos Investments

More Alternative Investments Topics >