Unsurprisingly, trying to plug the holes of a leaking $23 trillion economy with government money resembles a rudderless adventure right now. The economic repercussions of COVID-19 are almost too vast to fully appreciate. In just five weeks, 26.5 million people filed for unemployment benefits in the U.S. And just wait until Q2 GDP numbers start coming out. The good news is that the government can—and will—keep printing money during this massive crisis. While an oft-cited risk is that such spending could cause runaway inflation, we remind that policies only become inflationary if stimulus extends beyond the required period of need and lending increases.

In the near term, we expect the opposite, deflation, with wages being eliminated, energy prices in free fall due to lack of demand and too much supply. Further out, the question for the short to medium-term is, how exactly could prices go up? Aside from essentials (see personal protective equipment and, of course, toilet paper), demand has collapsed, critically for big-ticket expenditures like entertainment, travel and real estate. As for the longer-term, we lean on several recent examples of whatever-it-takes fiscal and monetary policy not leading to anything close to inflation.

Current State: Deflationary Limbo

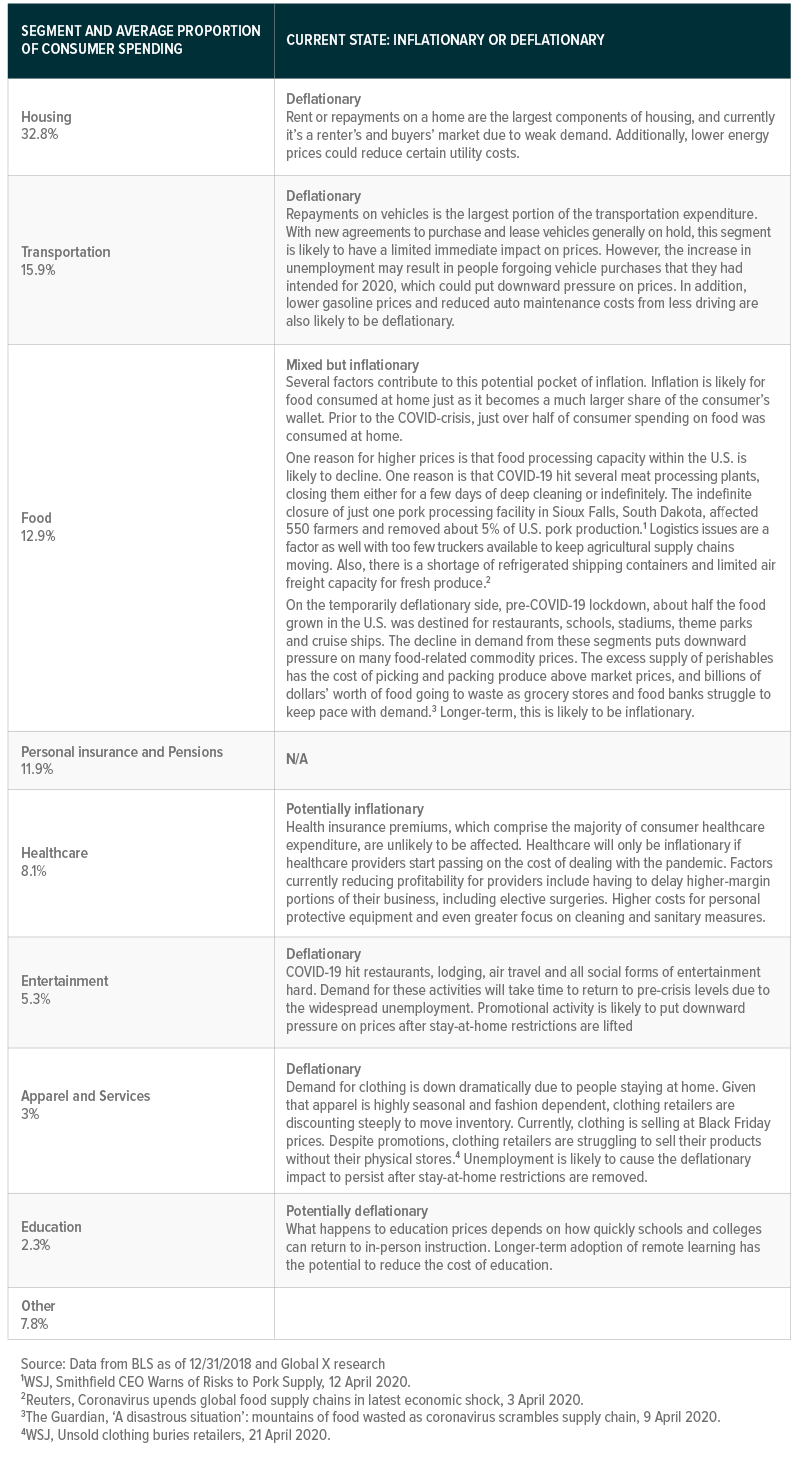

Over the last five weeks, 16.7% of U.S. workers employed in February applied for unemployment benefits. Given the current labor force participation rate, this implies that the current unemployment rate likely jumped from 3.5% to around 14% during these five weeks.i This exceptionally large increase in joblessness is likely deflationary, as people have less ability to spend. Additionally, for those who’s financial means have not been impacted by COVID-19, spending has also been curtailed due to impacts on spending habits. While it’s good for a household’s budget to reduce spending, when we see this activity occur on a national (or global) scale, it adversely impacts GDP growth and puts downward pressure on prices. To generate revenue and most importantly, cashflow, companies need to discount prices.

Compounding this deflationary pressure is the sharp decline in energy prices. WTI crude prices are down approximately 76% since the market peaked on February 19.ii Normally, lower oil prices benefit consumers, but stay-at-home orders make it harder for consumers to take advantage of these low prices. Still, energy prices filter through into most production and transportation processes, so this deflationary development will have a large impact on the economy.

COVID-19 does have inflationary components for producers, though. Due to social distancing, many companies are unable to run their production lines at full capacity. Companies providing essential services also need to spend substantially more on cleaning and protective measures to reduce the risk of infections at grocery stores, warehouses and production plants, among other areas. Within select areas of the economy, higher labor costs – including danger pay and bonuses to compensate workers – is another factor that could increase producer prices. However, given the current weakness in consumer demand, there is greater potential for margin contraction rather than passing on the higher prices to consumers.

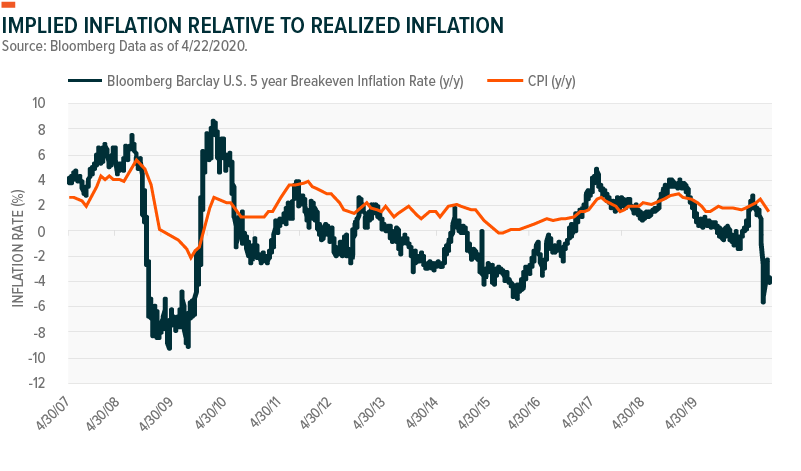

Given all of the inputs, it is fair to say that our current environment is likely to be at least somewhat deflationary. The implied inflation rate has declined sharply since the recent market peak on February 19th. Typically, there is a reasonably strong relationship between changes in the implied inflation rate and what is later reflected in the reported consumer price inflation (CPI) numbers. Referring to the chart below, due to the recent drop in the implied inflation rate, we expect the reported CPI rate to decline sharply in the coming months.

Near Future State: China’s Experience

Reopening the U.S. economy will likely occur slowly and with consumers nervous about their physical and financial health. We expect behavioral change to persist long after the U.S. returns to business as usual. In that sense, China’s restart provides some valuable insight into the U.S.’ path forward, despite vast differences in the two economies’ guiding principles and consumer spending. Early returns from China show a resurgence in supply and languished demand with Chinese consumers reticent about leaving their homes and discretionary purchases. Demand is at about half of pre-crisis levels.iii

Morgan Stanley’s AlphaWise China Consumer Survey for the week of April 13 shows that while 94% of respondents left their homes for work, only 25% planned to go out in the following week for social contact or discretionary purchases.iii Willingness to buy non-essential goods remained stable since the survey began, showing only minor increases over the last six weeks despite government “all clears.”

We believe the mismatch between supply and demand forces support the case for price deflation over the near term. The supply side of the Chinese economy looks like it rebounded. By the end of March, between 85% and 95% of industrial capacity came back online, while 75% to 85% of services returned to operation.iii This trend is pervasive, with only the construction, tourism, cinema, and education industries lagging. Full revival is expected by the summer, barring complications from secondary outbreaks. Should consumption bounce to the same degree, China’s economy will return to full operation.

However, spending habits continue to shift in China, with consumers planning to increase purchases of groceries, apparel, and alcohol, while shirking spending on luxury products, consumer electronics, and home appliances over the next month.iii Delayed current spending in categories such as home appliances will likely create pent-up demand, but in the short term prices for lower-demand goods are expected to drop in the hopes of encouraging sales. At the same time, a more home-focused consumer base shows increased demand for essentials, supply shortages and production complications could cause the prices of these staples to increase.

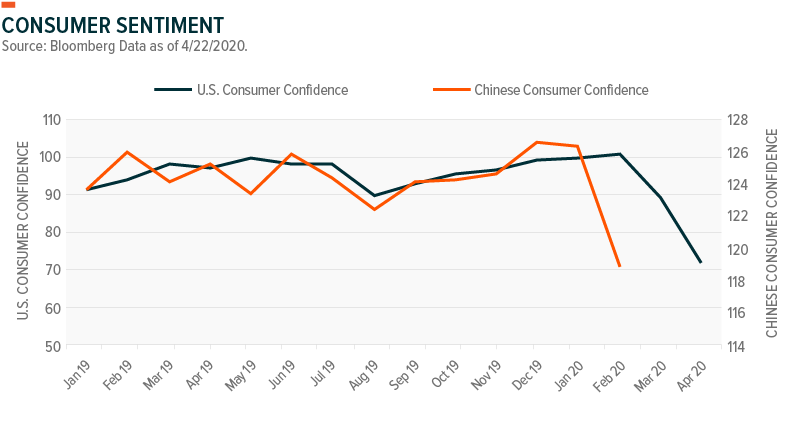

The current dichotomy between staple and discretionary goods in China will likely continue until the crisis is resolved. Its persistence is concerning, given what it suggests about a more consumer-centric economy like the U.S. Unlike China, the consumer is king in the U.S., where roughly 70% of U.S. GDP comes from consumption. And current data is less than desirable. The University of Michigan’s Consumer Sentiment for April fell to 71.8, its lowest reading in almost 10 years. U.S. Consumer Sentiment seems to mirror the China’s trend with a slight lag. Some deductive reasoning applied to our day-to-day lives reinforces these numbers. As people shelter in place at home, purchasing behaviors shifts towards essentials and away from non-essential goods.

Social distancing will be with us until we reach herd immunity or a vaccine is readily available. Effects of these behaviors, combined with economic damage sustained via job losses and salary cuts, will weaken demand for goods and pricing power of suppliers. These dynamics may pressure inflation down, possibly to the point of notable deflation.

Further out Future State: Risk Overstated

The dramatic increase in money supply has some concerned about rampant inflation over the long term. But when the dust settles from this crisis, in our view, that risk is highly unlikely. We can point to several recent several examples of a higher money supply having no meaningful impact on inflation in the U.S. and abroad, namely the Global Financial Crisis. Additionally, prior to that episode, Japan increased its money supply without affecting inflation. We can look to credit for an answer as to why.

When interest rates are effectively zero, increasing money supply no longer impacts the incentives for households and businesses to take out additional credit.iv Without substantial credit expansion, rampant inflation is unlikely during the COVID-19 recovery.

This is not to say that slightly higher inflation isn’t possible as economies adapt to post-pandemic life. Globalization and efficiency were dominant themes over the last few decades. And prior to 2018, global supply chains with stock levels optimized for efficiency generally worked well. China’s lockdown showed the extent to which supply chains still relied on China. While companies diversified elsewhere in Asia and across eastern Europe, China remained a key provider of inputs for factories.v

As companies emerge from the crisis, they are likely to think about how to diversify their supply chains away from China. The process is likely to lead to choices between greater global diversification or deglobalization and localization. Greater diversification globally may include more duplications in existing manufacturing partnerships. Conversely, advancement in robotics and automation could encourage deglobalization and localization. In prior decades, better technology enabled supply chains to spread globally. Now, technology could provide avenues for companies to bring them back home.vi

Regardless of which approach companies choose, there is new focus on ensuring supply rather than efficiency. With this shift, some margin compression is likely, and potentially some price increases may be passed onto consumers. Despite this risk, technology appears ready to minimize the inflation risks over time.

Conclusion

The word unprecedented gets thrown around a lot these days, to the point of exhaustion. From an economic perspective, it’s important to remember that the government’s current spending habits aren’t completely novel. We only have to go back to 2008 to see what unlimited government spending looks like. Admittedly, this pales in comparison to the fiscal and monetary policy stimulus that we are currently seeing during the COVID-19 crisis. When there are dislocations within financial markets, monetary policy has proven highly effective at restoring functioning markets. Similarly, fiscal policy is best utilized countercyclically in conjunction with monetary policy. This is in line with the current stimulus spending.

Importantly, in years following the Global Financial Crisis, we learned that stimulus spending sprees don’t necessarily lead to troublesome inflation. In fact, historically low inflation is one of the most persistent themes over the last decade-plus. Inflation requires increased demand. Within the current environment, lack of demand is a persistent issue despite increased government spending. Due to the sizable impact on employment and consumption patterns, demand is unlikely to bounce back once the restrictions are eased. As a result, inflation is likely to remain subdued. Debt always comes due, and traditional political dependencies will likely want to inflate it away at some point. But for the foreseeable future, inflation is one COVID-19-related risk that we probably don’t have to worry too much about.

i As of 4/23/2020

ii As of 4/27/2020

iii Morgan Stanley, China Activity Tracker: Income and COVID-19 Concerns Capped the Return of Shoppers, 4/21/2020

iv MasterClass, Paul Krugman IS-LM Model, 9 October 2019.

v The Economist, The changes Covid-19 is forcing on business, 11 April 2020.

vi The Economist, The changes Covid-19 is forcing on business, 11 April 2020.

Definitions:

Inflation: Inflation is the general increase in prices. This can be applied to consumer price or producer prices. Inflation is typically discussed in reference to the Consumer Price Index (CPI) or the Producer Price Index (PPI).

Deflation: Deflation is the general decline in prices. This is potentially harmful for economic activity as the expectation of lower future prices can put downward pressure on demand currently. This helps to perpetuate lower prices.

Bloomberg West Texas Intermediate (WTI) Cushing Crude Oil Spot Price Index: Designed to track the spot price of WTI.

SEI Investments Distribution Co. (1 Freedom Valley Drive, Oaks, PA, 19456) is the distributor for the Global X Funds.

Check the background of SIDCO and Global X’s Registered Representatives on FINRA’s BrokerCheck

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit or guarantee against a loss. This information is not intended to be individual or personalized investment or tax advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation.

Information provided by Global X Management Company LLC (Global X) and SEI Investments Distribution Co. (SIDCO). Global X and SIDCO are not affiliated.

© Global X ETFs

More ETF Topics >