Are You Ready for Some High-Stakes Gambling?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIt is a light economic calendar if measured by the number of reports but an important one given the focus on employment. We will get reports from ADP, the “official” BLS employment situation numbers, and the weekly early indicator from jobless claims. Whatever else happens in the economy, jobs take center stage.

Despite the interest in employment, markets are looking beyond the current horrible numbers. Everyone is paying attention to the reopening of the US economy and how things will look in the future. The nature and pace of the reopening has implications for your personal health, societal wellbeing, and financial markets. The question is:

Are you ready for a high-stakes gamble?

The gamble is especially interesting, partly because one’s ability to control personal risk is much lower than it would be in a casino!

Last Week Recap

In my last installment of WTWA, I warned about excessive emphasis on what was working in the current market, asking whether investors should behave like traders. Thanks to those of you who joined in with comments and examples. Especially when the market is making big moves in both directions, it certainly seems like there is opportunity.

This was not a subject picked up in financial media, which benefits from very active trading. As I noted at the start of 2020, I am emphasizing the issues that are most important for investors. I recognize that many of these will not become major themes – at least not right away.

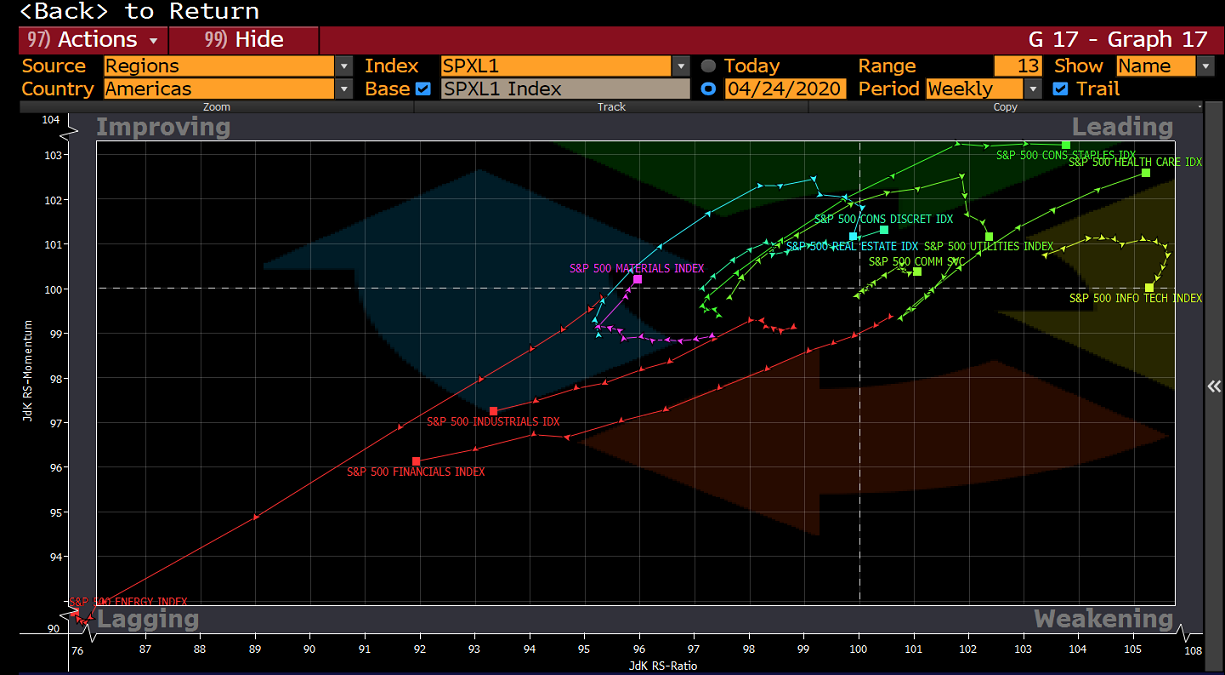

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, an excellent combination of the most important information.

As has been the case for several weeks, there are frequent opening gaps. This has been accompanied by much more active trading in the overnight futures markets (WSJ).

Here is an interesting chart from our research team showing what has been working. As I have recently written, this is not a road map for investors unless they want to imitate traders.

The market lost 0.2% on the week. The trading range was 4.7%, a continued reduction from a few weeks ago. You can monitor these along with historical comparisons in my weekly Indicator Snapshot (below).

Personal Note

I am finding myself with more good material on science, economics and the investment implications than I can use. I am trying to find a way of providing it on my site instead of leaving it on the cutting room floor. I am finding fewer investment ideas that I can really endorse.

I am still looking for some time off. Next week is a possibility.

Noteworthy

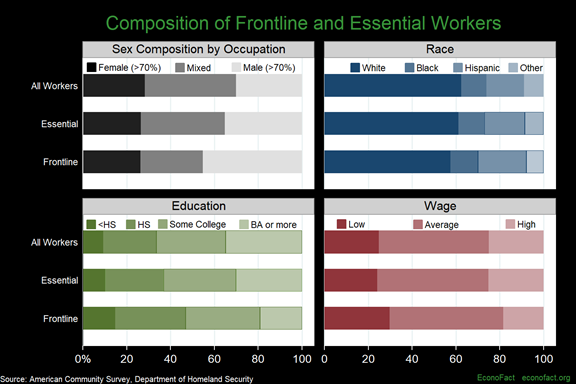

EconoFact analyzes who is an essential worker and who is on the front lines. The data show that the risks differ in recognizable patterns.

Read all of the evidence to see why they reach this conclusion:

Essential workers have been called on to meet our basic needs during the COVID-19 shutdown. A significant portion of these workers, frontline workers, cannot work remotely. Our analysis shows that, on average, frontline workers are disproportionately less educated and minority workers, earning below average wages and with a substantial share of workers in the bottom wage quartile. Thus, the provision of hazard pay to these workers may be merited both because of the risks they are taking by remaining on their jobs as well on equity grounds. Hazard pay could also help recruit workers into these jobs at a time when they are especially vital. This is especially the case given the generosity of the unemployment insurance benefit increase under the CARES Act which may leave some low-wage workers doing better collecting unemployment benefits than continuing their frontline employment. Other benefits should also be considered including support for the childcare needs of these workers, paid sick leave (where not otherwise mandated under the CARES Act), coverage of COVID-19 health expenses for those who lack health insurance, and death benefits to the families of those who have died of the virus.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators have always been a valuable part of my economic review. Over the next year we will watch for signs of the eventual economic rebound; NDD’s three time frames will be especially helpful. The overall picture, terrible now and on short indicators and mildly positive on long indicators continues. Some of the short-term indicators are slightly “less terrible.”

The Good

Until we have more relevant data, I will just hit the highlights and provide some interpretation. Some of the “good” news fits the less bad description, especially if beating expectations. I do not intend this to sugar coat the terrible economic situation. It is simply a technique for taking note of changes.

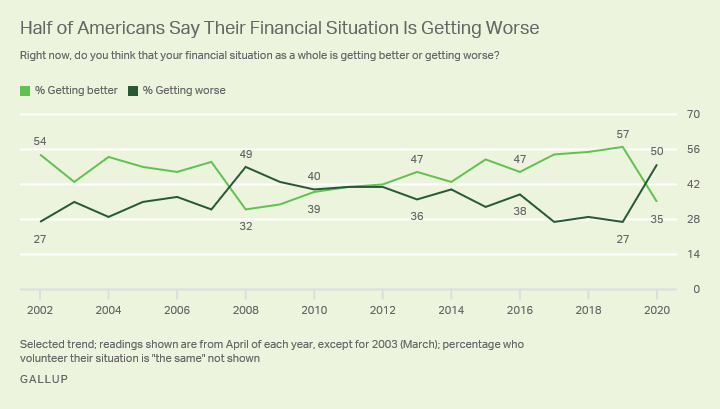

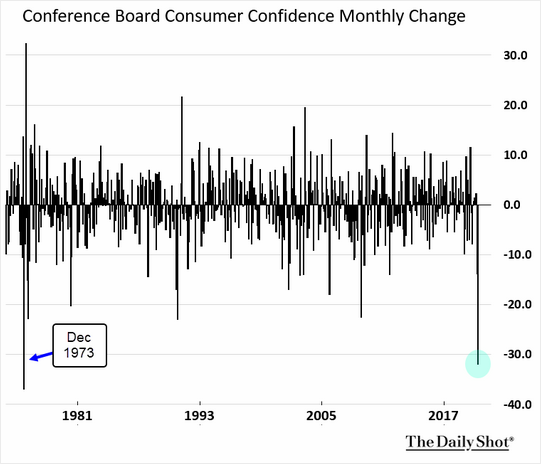

- Consumer confidence declined to 86.9 in April. This slightly beat expectations of 86.5 but was much worse than March’s 118.8. Gallup polling data was more bearish. Not only is the current situation poor, but expectations are weakening as well.

- The Fed, as expected, made no change in official policy but provided reassurance to investors.

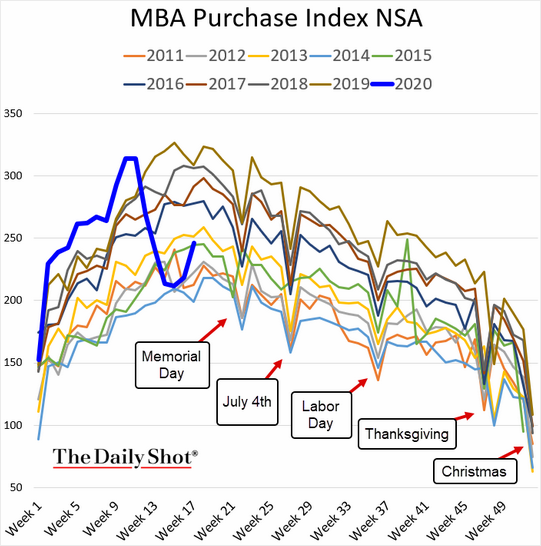

- Mortgage purchase applications continue to rebound.

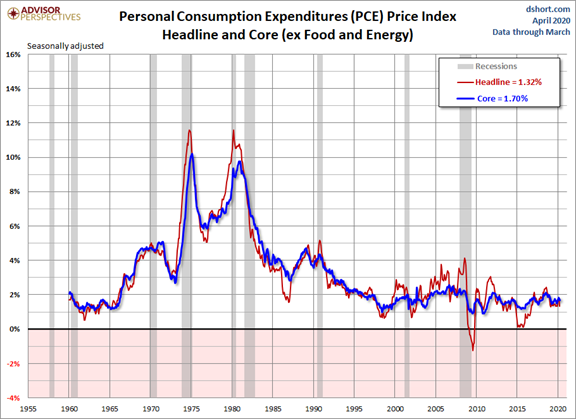

- Core PCE prices in March declined by 0.1% versus expectations of a 0.1% increase and February’s 0.2% gain. This is good news because it implies no pressure on the Fed to start fighting inflation. Here is a long-term view from Jill Mislinski.

- Construction spending in March increased 0.9%, much better than the expected decline of 3.5% and February’s (downwardly revised) -2.5%.

- ISM Manufacturing for April was 41.5, better than expectations of 39.0, but worse than March’s 49.1.

The Bad

Everything else declined significantly. Some of the March data still does not reflect the entire coronavirus effect.

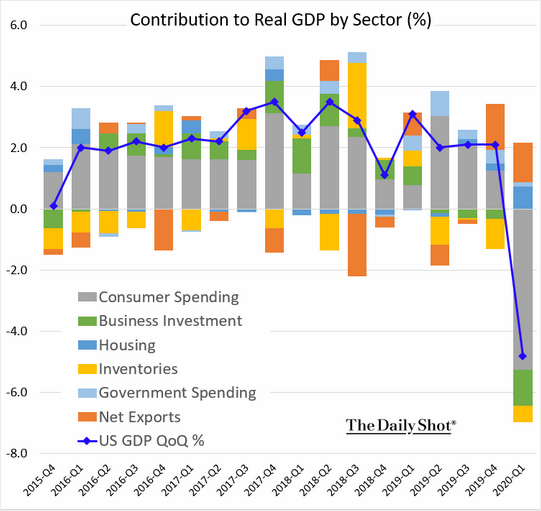

- GDP for Q1 2020 declined by 4.8% on this first estimate. This was worse than the estimated -4.3% and much worse than Q4 2019’s 2.3%.

- Pending home sales for March declined 20.8% versus February’s 2.3% gain. Calculated Risk.

- Unemployment benefits exceed paychecks for many workers. (Heritage Foundation).

- The Chemical Activity Barometer fell 5.5% in April, consistent with recession levels. (GEI).

- Personal income for March declined 2.0%, worse than the expected decline of 1.5% and much worse than February’s gain of 0.6%. We should expect much worse from the April report.

- Hotel occupancy is down 62.2% year over year (Calculated Risk).

- Personal spending for March declined by 7.5% worse than the expected -3.6% and much worse than the February increase of 0.2%. This will also get much worse in April.

- Initial jobless claims were 3.839M worse than the expected 3.050M, but an improvement over the prior 4.442M. I expect this decline to continue, but continuing claims to increase.

- Continuing jobless claims jumped to 17.992M from the prior week’s 15.818M. I once again remind everyone that this number is reported a week later than initial claims.

- Rail traffic continues to worsen. Steven Hansen (GEI) notes that the four-week rolling average is down 20.8% from one year ago.

The Ugly

China’s role in the origin of coronavirus. Evidence of original research and cover-up. Threats of retaliation?

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

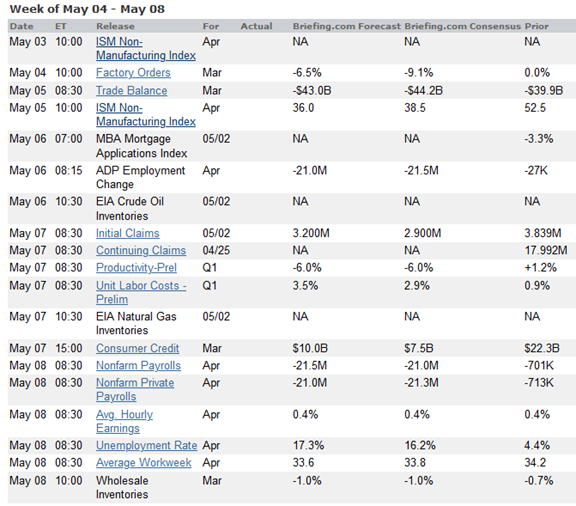

The Calendar

The economic calendar is light in the number of reports, but the focus on employment makes it an important week. We will see April data on both the ADP private employment change and the official employment situation report. ISM non-manufacturing will provide a read on the service sector, with a big decline expected. Jobless claims have become even more important than usual as the first read on employment changes.

Corporate earnings reports will provide continuing company-by-company descriptions of the shutdown effects and future prospects. The big story will once again be the pandemic and the prospects for reopening at least part of the economy.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The employment data will certainly attract attention, but most market watchers will focus on the gradually reopening US economy. There is an obvious willingness to look beyond the current horrible data, if there is some assurance that change is coming. The push for that change has created an issue that reaches far beyond the financial markets. It is a matter of personal and societal health. Strong and sharply differing opinions are voiced, but no one really knows what will happen.

Are you ready for this high-stakes gamble?

Background

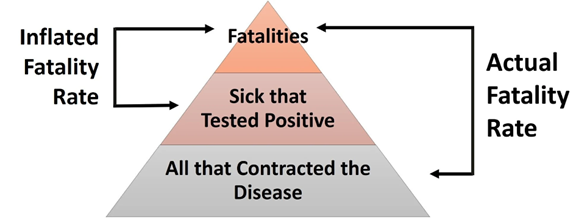

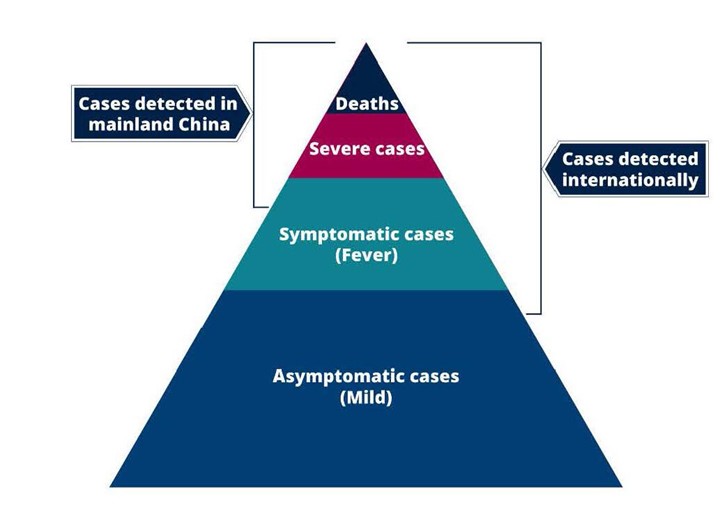

I have been writing for weeks that understanding models will prove to be essential in reaching logical policy and investment conclusions. I have also described the issues involved in finding the needed data. I am going to use just one of the simple modeling problems to highlight the intense and growing division over the issue of reopening US business. The key question is determining the case fatality rate.

While this seems simple enough, it is often confused with the mortality rate or loosely described (even by top journalists) as the “death rate.”

Challenge of the Basic Model

Here is how that goes wrong. First, the denominator. Suppose that you start with people who are sick. Calculating fatalities from that gives an inflated rate.

Even if you try to discover everyone, you will have a large number of asymptomatic cases that are not included.

How about the numerator of the equation? Surely, we know how many people died, don’t we?

Some think the deaths are overstated, including non-COVID19 victims or people who would have died anyway.

But several media figures who are sympathetic to the president have started to question the official death toll, claiming it is being distorted for political purposes, by including in the statistics people dying of other causes.

Fox News‘s Brit Hume, who has previously tweeted that New York’s “fatality numbers are inflated”, appeared on Tucker Carlson’s late-night show on Tuesday to claim that any person with the virus is being counted as a Covid-19 death “regardless of what else may be wrong”. Carlson responded by saying, “There may be reasons people seek an inaccurate death count,” adding: “When journalists work with numbers, there sometimes is an agenda.”

The rightwing radio host Rush Limbaugh, who received the presidential medal of freedom from Trump, previously dismissed Covid-19 as similar to the “common cold” but changed tack recently to claim: “It’s admittedly speculation, but … what if we are recording a bunch of deaths to coronavirus which really should not be chalked up to coronavirus?”

Most experts believe that the deaths are actually understated. Many who died in hospitals were not tested. Others died at home.

Since many reject science and models, they are free to reach any conclusion they wish.

Implications of the equation debate

Both of the principal sides agree that the case fatality rate is over-stated. One side says that this proves that the reaction has been overdone because of a false assumption of lethality. The other concludes that the higher denominator proves that the virus is more infectious than believed.

Economic reopening issues

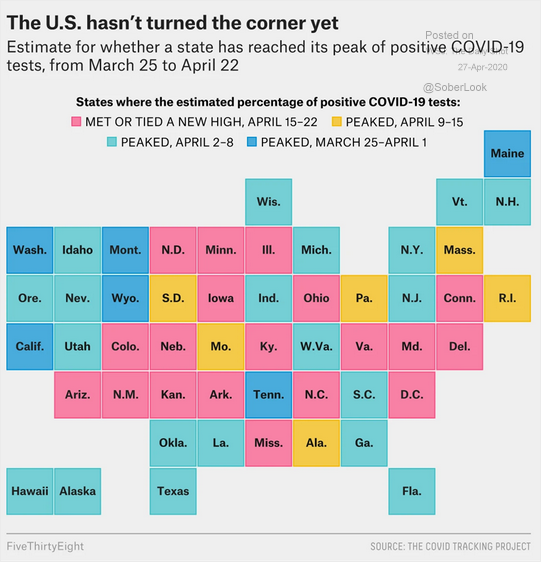

There is a patchwork of state decisions concerning reopening businesses. This chart shows the expected peak for each state.

Even within the states where reopening permission has been given, there are questions about what to expect about the actual pace. Business owners, workers, and consumers have a cautious attitude (Washington Post).

There are methods to reopen that do not require the end of the pandemic (WSJ). Hint: Schools will reopen, and young people will be the first to emerge from shelter-in-place. The OldProf and his demographic colleagues will get to read and watch more movies.

Reopening would be speeded by testing and tracing. Will people accept that loss of privacy?

Nearly 3 in 5 Americans say they are either unable or unwilling to use the infection-alert system under development by Google and Apple, suggesting that it will be difficult to persuade enough people to use the app to make it effective against the coronavirus pandemic, a Washington Post–University of Maryland poll finds.

As usual, I’ll suggest some conclusions of my own in today’s Final Thought.

Quant Corner and Risk Analysis

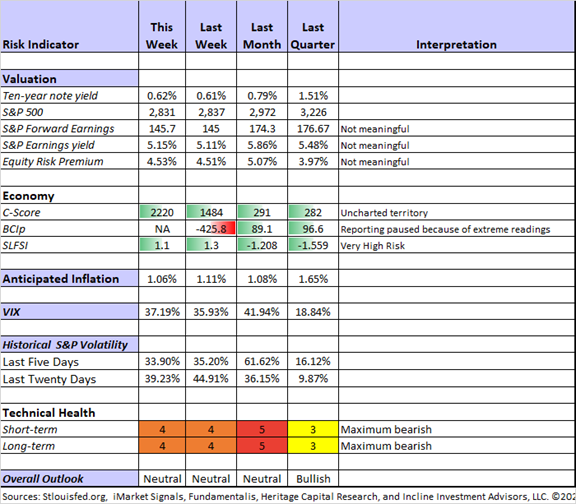

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

Welcome to David Moenning and his Indicator Wall. His approach has many parts, but I will attempt to summarize two time periods on our five-point scale. The C-Score spiked again. It is a dramatic change in underlying factors which normally provide important indications. This level is an outlier that cannot readily be interpreted. I’ll have more on this soon. Georg Vrba has paused the BCIp signal because of the extreme readings. It has done its job for now.

I am treating forward earnings and the resulting measures as not meaningful until we get more clarity.

I contine my rating of “Neutral” in the overall outlook for long-term investors, but it is close to becoming mildly bearish. I am not trying to guess what will happen in the next week or two. As an investor, I would be neither a buyer nor a seller at this point. I did a little buying for new accounts and for programs where our cash had built to more than 30%.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian suggests that one way of looking ahead might be to average 2020 and 2021 expected growth rates.

Georg Vrba: Business cycle indicator and market timing tools. Georg’s business cycle index continues its steep decline.

David Moenning: Developer and “keeper” of the Indicator Wall. His most recent update summarizes the key elements.

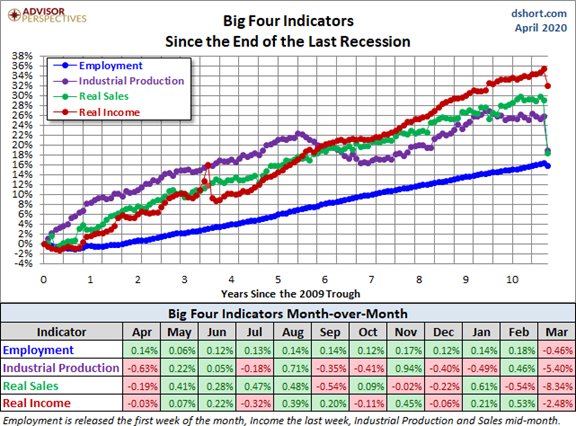

Doug Short and Jill Mislinski: Regular updating of an array of indicators, including the very helpful Big Four.

The sharp decline is apparent and broad. If it is sustained as everyone expects then the NBER might call March or April the month when the recession started. We’ll get that verdict in a year or so!

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I were to recommend a single must-read investment article this week, it would be Marc Gerstein’s Searching For Less-Known ETFs: Large-Cap Value. He shows a means for investors to be contrarian while also getting good stocks and good prices. He wonders first about why this is the right time to seek large-cap value. One answer is keeping down risk.

High P/E is dangerous, not in and of itself, but only if or when the market comes to realize that the growth expectations (or dreams) that support high ratios are not going to be achieved. We saw it in the 1960s with the once-beloved “Nifty Fifty.” We saw it in the early 2000s with then-new internet stock. But we’ve lately come through a very long business expansion, accompanied by a new generation of newly introduced businesses, that for a long time have made disappointment, or unfulfilled expectations seem like a thing of the past.

I like his discussion of “the usual suspects.” His ratings for big firms all looked alike and came up neutral in his ratings. Going beyond these, he tweaked some standard screening rules and came up with QARP (for quality at a reasonable price). Haven’t heard of it? Neither had Marc. The ETF is small ($84.4 M AUM) and rather thinly traded, but it is based upon Russell 1000 stocks. This means that the ETF process can liquidate underlying assets if necessary.

Marc goes on to discuss several better-known choices. As is the case with many of my “best of the week choices” he is combining solid ideas with a process that provides a lesson for investors.

Stock Ideas

Here are a very few ideas to consider, keeping in mind the companies and sectors that will be viable on “the other side.”

Chuck Carnevale is enjoying a menu with more attractive choices! This week he analyzed NetApp (NTAP), which combines dividend safety, attractive valuation resulting, and high yield. As always, Chuck’s analysis includes both positive and negative factors, and an educational video highlighting important valuation metrics.

How about sports? Barron’s explains that you can now buy Madison Square Garden Entertainment (MSGE) for the site and Madison Square Garden Sports (MSGS) for the teams. This is another good “other side” question. Mrs. OldProf adds that you can also buy stock in her Packers, but there is not much of a resale market!

There is a current focus on consumer staples, a group that is doing well right now. Be sure to consider how well they will do on “the other side.”

Mondelez: Great Execution, Stock Slow To React

PepsiCo: A Dividend Aristocrat With 47 Years Of Solid Growing Income

Income ideas

Blue Harbinger has an interesting idea that lets you benefit from the oil glut, including the low prices. Own those with storage. The corporate structure is a bit tricky and be sure to read the risk section carefully!

Lyn Alden Schwartzer discusses how to protect purchasing power when you purchase ostensibly risk-free Treasuries.

I have resumed my series on boosting your dividend yield by writing near-term covered calls. This week I discussed a trade in Cardinal Health (CAH) the day before we executed it for clients.

The Great Rotation – Now the Great Reset

Stone Fox Capital is looking beyond current performance to incipient changes. How will American Airlines Group (AAL) do as air travel rebounds? The author sees a rebound on this stock and the sector as a whole, “as the public increasingly returns to flying, even while the domestic economy is virtually locked down.” Check out the full post to review the supporting data, including a rebound in traffic through TSA checkpoints. He also has a post on Southwest Airlines (LUV).

I am intrigued by these ideas because my Great Rotation research team was working on LUV Friday afternoon. As I have recommended in recent posts, we are looking at three tests:

- Solvency

- Earnings impact

- Resumption of revenue growth and margins

I will not buy or hold any stock that does not meet these tests, and you should not either.

I welcome those who have already joined my Great Reset Project. There is no charge as you monitor our progress, including some stock ideas as they emerge. We hope that members will join in a few brief surveys assisting with our use of James Surowiecki’s Wisdom of Crowds approach. More members will improve my research results. The airlines provide one example. We need to know how deep the dip in air travel and for how long it will last. Bill Gates and Warren Buffett have offered opinions, but they are not regular customers. (In fact, they have been known to take the train to enjoy a few hours of bridge. They fly their favorite partners to the departure point and home after they arrive. It is a great idea for a peaceful and relaxing trip). Airlines have done passenger surveys. Analysts and industry experts opine. This is actually a perfect example of the Wisdom of Crowds approach. There are many other similar sectors to consider. I cannot describe the full method within the context of WTWA, so join us to learn more.

Watch out for

Inovio (INO). Paulo Santos looks at the vaccine potential and concludes that it is a “strong sell.”

Final Thought

The high-stake gamble is one that an individual can hedge – at least a bit.

- Be cautious in your own social interactions until there is better evidence that danger has reduced or passed.

- Do not feel compelled to make all-in or all-out investment decisions. Even though we are missing baseball season, drat it, think of yourself as a runner on first base. You do not want to be caught leaning the wrong way! You have an investment plan. If you have a strong conclusion, even a small tweak could have an important effect.

- Do not be too confident about a lack of cases in your local area. If parts of the country are moving too aggressively, it will ultimately reach everywhere.

For myself and my clients I am pretty cautious right now. That comes with my academic tradition and commitment to finding the best experts on each topic. If the easing of restrictions leads to a rebound in the virus, we will not have an indication for at least two weeks. We can afford to wait a bit longer.

One striking conclusion: Usually governments test the waters with a variety of policies. They do more of what is working and stop policies that fail. In this case, if policies reduced the number of cases, many will conclude that restrictions were unnecessary. People are not very good at imagining counterfactuals – what would have happened in the absence of action.

And finally, everything has become politically loaded. My personal conclusions flow from my lifetime methods (which have been quite effective). One recommendation has been to avoid mixing politics with your investing.

The challenge of putting politics aside has never been greater! Or more necessary.

We all want a quick end to this, but we need more evidence before taking major steps.

I’m more worried about

- The complication of another disaster with the coronavirus. The earthquake in Puerto Rico is an example. Our capacity to handle major problems is becoming stretched.

- Another round of tariff action against China or anyone else. The time is not right.

I’m less worried about

- Hmm. At least my AC is fixed after conking out for five days in an Arizona heat wave!

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits