TWO BROAD SHIFTS INCREASING INCOME DEMAND

Globally, there are two fundamental shifts happening in the current environment that are increasing the need for income-producing products. First, as baby boomers continue to retire from their work lives, the demand for investment income is likely to grow. According to the 2019 BlackRock Defined Contribution Pulse Survey, “plan participants are sharpening focus on how to secure crucial, ongoing retirement income.”

Second, interest rates have been in a downward trend and most recently have hit record lows. This means that total return from fixed-income assets will not help bridge the $1 trillion funding gap¹ that 76 million baby boomers² are likely to face in pensions, health care and other benefits.

STOCKS COULD OFFER A COMPETITIVE INCOME SOURCE (%)

Source: Evercore ISI (Data 01/31/1995 through 03/31/2020). Past performance is not a guarantee of future results.

MID-CAP STOCKS MAY PROVIDE OPPORTUNITY FOR CAPITAL APPRECIATION, INCOME

In an environment where bond yields are at a record lows, we believe that stocks in the mid-cap universe may be well positioned to fill the income gap and provide an opportunity for capital appreciation. Generally, investors think that dividend-paying companies mostly exist in the large-cap universe. However, as shown below, there are numerous companies in the mid-cap universe that pay dividends.

Many mid-cap companies pay dividends

The Fund was created to achieve a dual mandate of investing in companies that have the potential to grow their dividends and provide an opportunity for capital appreciation across all market cycles. Focused on companies in the mid-cap space, we invest in core growers at a stage in their lifecycles where they have enough earnings growth and are generating cash in excess of what is needed to grow organically that they can offer return of capital to shareholders. Since the Fund’s inception in October 2014, portfolio investments have provided nearly a 3% gross yield and have generated high single-digit income growth annually.

Source: FactSet and Ivy Investments.

AN ACTIVE APPROACH TO INCOME GROWTH, CAPITAL APPRECIATION

In today’s environment where stocks are supported by expansionary monetary policy and cheap money³, we believe investing in an actively managed dividend portfolio with the potential to generate income and provide attractive growth characteristics is a sound approach. This is where the Ivy Mid Cap Income Opportunities Fund can fit into an investor’s portfolio.

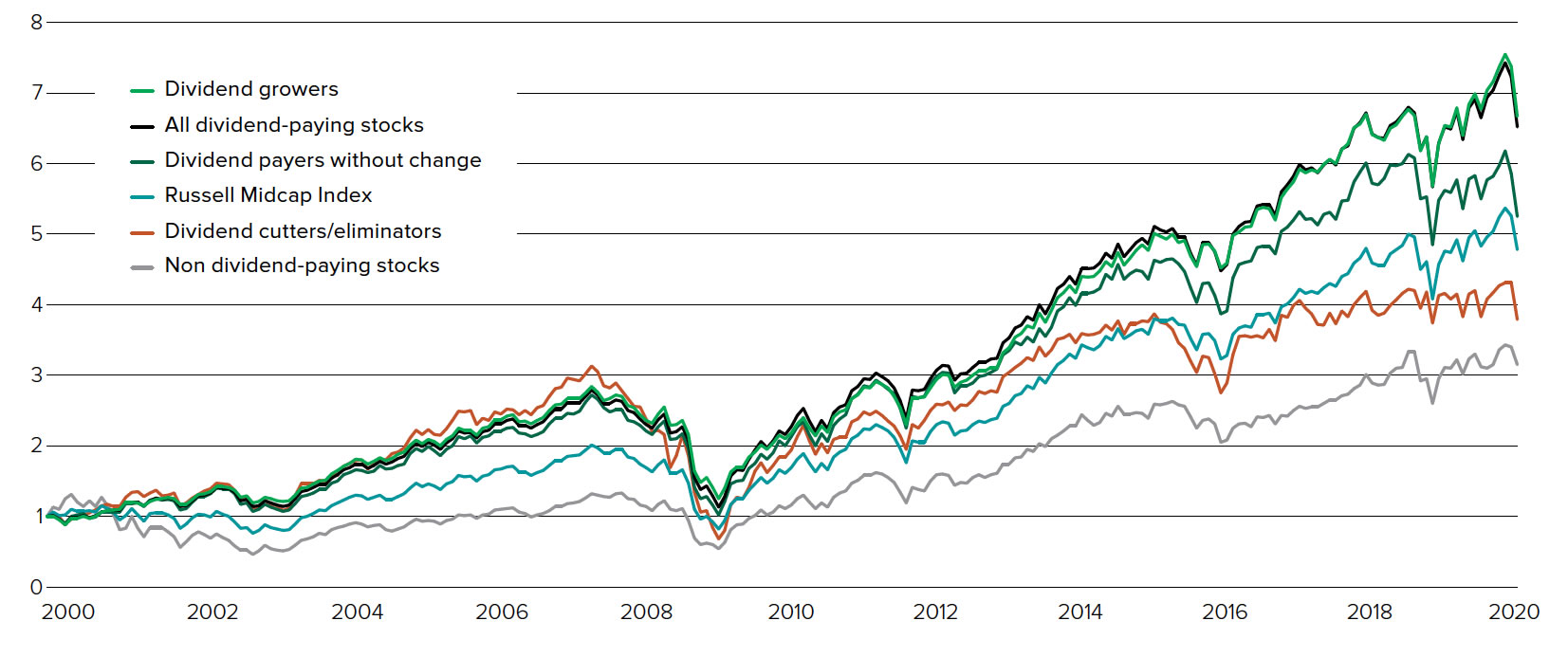

DIVIDEND GROWERS IN THE PAST, FUTURE

As shown in the chart below, dividend growers have generally been rewarded by the markets. Historically,within the Russell Midcap Index, the Fund’s benchmark, divided payers have tended to perform better than the index. This chart also shows the importance of avoiding those companies that don’t pay or eliminate dividends.

Overall, as interest rates remain low, investor demand for yield and income have become elevated and should remain so. In such an environment, we expect dividend- paying companies to become increasingly valuable. In our view, companies with strong cash f lows, low payout ratios, and durable business models are in a favorable position to increase dividends and grow over time.

DIVIDEND STOCK RETURNS ACCORDING TO DIVIDEND PAYMENT TRENDS (%)

Source: Evercore ISI (Data: 12/31/1999 through 03/31/2020). Past performance is not a guarantee of future results.

AN ACTIVE APPROACH PROVIDING DIVERSIFICATION INTO DIVIDEND-YIELDING STOCKS WITH GROWTH CHARACTERISTICS

We think the foundation of a successful actively managed strategy within the mid-cap universe is a focus on companies that offer capital appreciation and have as history of dividend increases. Yields are an unappreciated aspect of the universe.

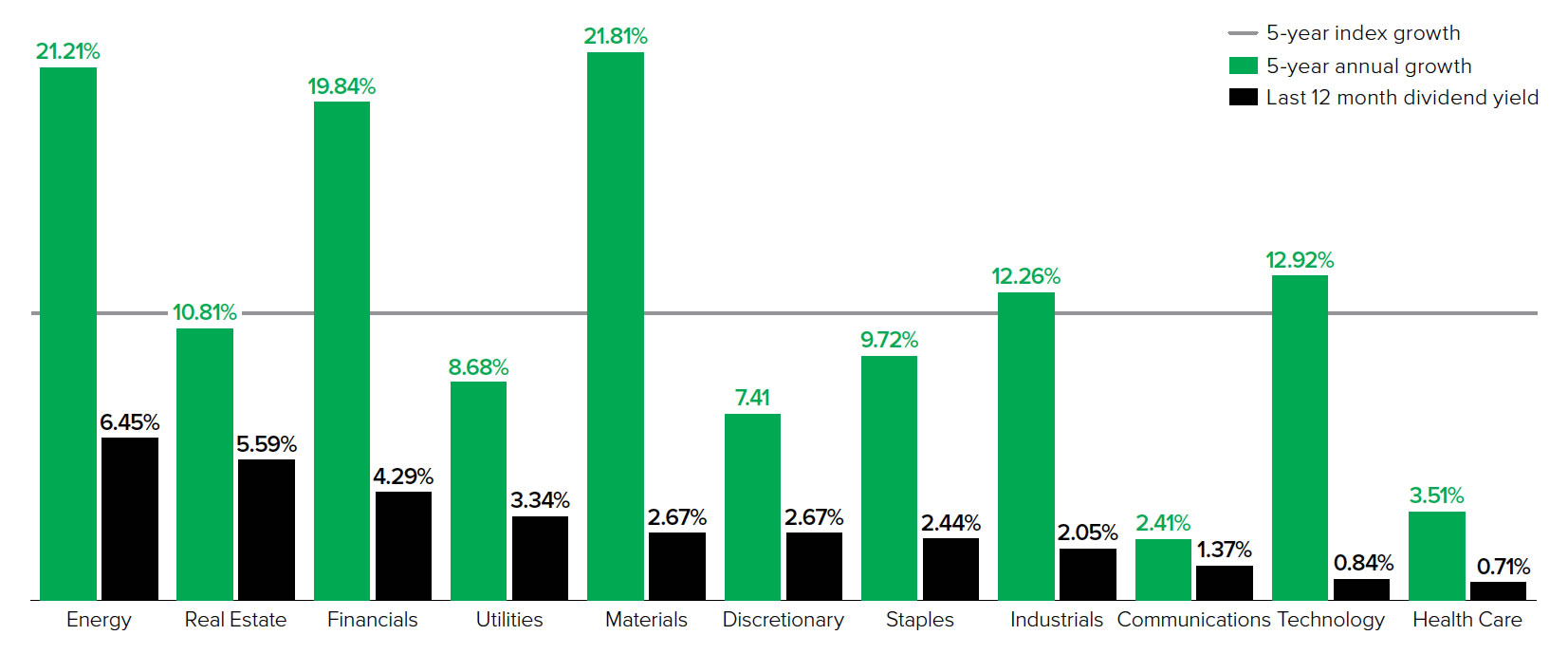

Through the Fund’s bottom-up investment process, we seek companies that have a current yield above 0.5% (as of 03/31/2020 — the lowest yielding security in the Fund is at 1.6%) and a track record of yield growth and earnings growth that can allow for upside potential in stock prices. As of 03/31/2020, the Fund’s largest overweight positions were in materials and consumer discretionary because these sectors offered a combination of competitive yield and income growth supported by underlying earnings growth. In the generally low-yielding consumer discretionary sector, Fund holdings as of 03/31/2020 had an average yield of 4.4% versus the lower yield in the sector in the index (see chart below).

FUND OFFERS INCOME GROWTH, STOCK PRICE APPRECIATION

With interest rates at record lows, stocks appear well positioned to fill the income gap. While investors generally believe income-generating stocks are found within large caps, data shows that the mid-cap universe not only has a competitive stream of income payers and potential for growth, but it is also considerably underutilized.⁴ With such a backdrop, we believe the Ivy Mid Cap Income Opportunities Fund’s bottom-up active approach and dual mandate of income growth and capital appreciation may fill the income gap created by record low interest rates and the income needs of an aging population.

RUSSELL MIDCAP INDEX: DIVIDEND YIELD AND GROWTH BY SECTOR (%)

Source: Evercore ISI; Data as of 03/31/2020. Past performance is not a guarantee of future results.

Portfolio Management

Ivy Investment Management Co.

Nathan A. Brown, CFA

Kimberly A Scott, CFA

¹ https://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2019/06/the-state-pension-funding-gap-2017

² https://www.prb.org/justhowmanybabyboomersarethere/

³To support economic growth impacted by the coronavirus outbreak, the U.S. Federal Reserve re-started quantitative easing on 03/15/2020.

⁴Source: FTSE Russell and Strategic Insight Simfund as of 12/31/2019. Mid-cap stocks make up 25% of the U.S. equity space. This indicates that some value is being left on the table. Equity mutual fund assets represent open end mutual funds, domestic mid-cap categories vs. all domestic equity categories. The Russell Midcap Index measures the performance of the mid-cap segment of the U.S. equity universe. The Russell 3000

© Ivy Investment Management Co.

Read more commentaries by Ivy Investments