Roadblocks to Recovery

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is a normal one and is beginning to include data from after the start of the crisis. This week includes small business and consumer sentiment surveys, as well as April data for retail sales and industrial production. I will also be watching jobless claims, both new and continuing. As I have noted for weeks, none of this will matter. The stock rally on a day with a terrible jobs number makes clear the actual market focus. I expect market participants to be monitoring the economic reopening and asking,

What are the roadblocks to the rebound?

Last Week Recap

In my last installment of WTWA, I described the high-stakes gamble involved in the economic reopening. That was a good (but perhaps easy) guess about the topic of the week. Financial news made it the lead story throughout the week.

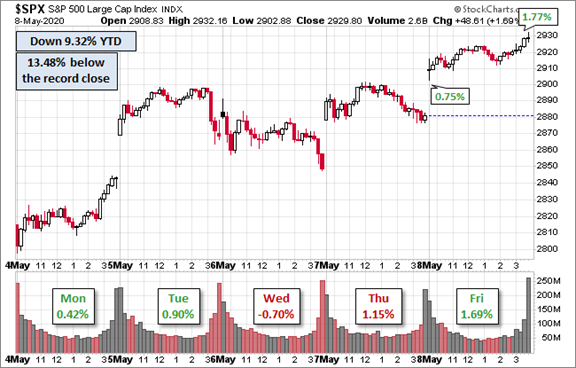

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, an excellent combination of the most important information.

As has been the case for several weeks, there are frequent opening gaps. This has been accompanied by much more active trading in the overnight futures markets (WSJ).

The market gained 3.5% on the week. The trading range was 4.8%, in line with the last several weeks. You can monitor these along with historical comparisons in my weekly Indicator Snapshot (below).

Personal Note

I am finding myself with more good material on science, economics and the investment implications than I can use. I am trying to find a way of providing it outside of the regular WTWA series instead of leaving it on the cutting room floor. I am finding fewer investment ideas that I can really endorse, but some that are worth investigation.

I am still looking for some time off. I’ll try again next week.

Noteworthy

The Visual Capitalist describes 11 Cognitive Biases That Influence Political Outcomes. Why should investors care? These principles are at the root of important current decisions about health, safety, the economy, and investments.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators have always been a valuable part of my economic review. Over the next year we will watch for signs of the eventual economic rebound; NDD’s three time frames will be especially helpful. The overall picture, terrible now and on short indicators and mildly positive on long indicators continues. NDD expects that meaningful changes, one way or the other, will begin to show up at the end of May.

The Good

Until we have more relevant data, I will just hit the highlights and provide some interpretation. Some of the “good” news fits the less bad description, especially if beating expectations. I do not intend this to sugar coat the terrible economic situation. It is simply a technique for taking note of changes.

- ISM Services for April showed contraction with a reading of 41.8, much lower than March’s 52.5. I am scoring this as “less bad” since it beat expectations of 38.5. Even that is a bit questionable, since the price component may have artificially inflated (!?) the result.

- Investor sentiment a contrary indicator, is close to the maximum bearish sentiment level. (David Templeton).

- Hotel Occupancy showed a slight uptick but remains down 58.5% y-o-y (Calculated Risk).

- Mortgage applications increased by 0.1%, better than last week’s decline of 3.3%.

The Bad

Everything else declined significantly. Some of the March data still does not reflect the entire coronavirus effect.

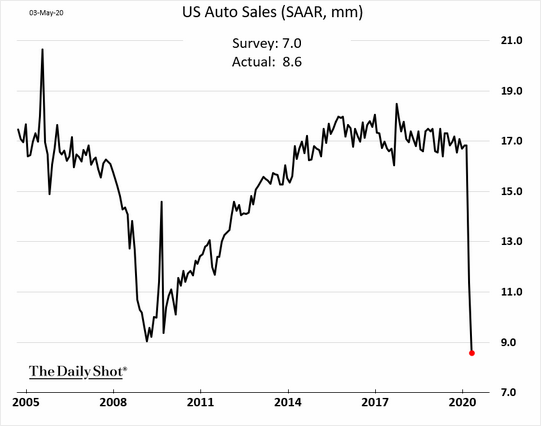

- Auto and truck sales plunged to a total of less than 7 million.

- Factory orders for March declined by 10.3%, worse than expectations of a 9.1% decline and much worse than February’s flat report.

- Mortgage Forbearance related to COVID19 has now surpassed four million homeowners, about 7.7% of mortgages (Calculated Risk).

- Initial jobless claims of 3.169M were better than the prior 3.846M but worse than expectations of 2.900M. It is a challenge to make any reasonable forecast of employment in this environment.

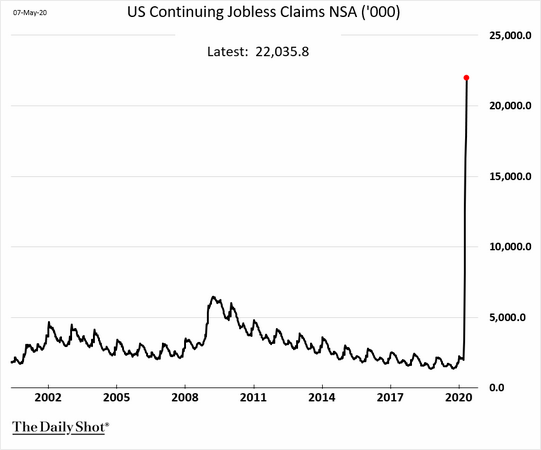

- Continuing jobless claims, now the more important read, increased to 22.647M, up from 18.011M the week before. And remember, this week’s 3 million will be added to that next week.

-

- ADP private employment declined 20.236M in April versus 149K in March.

- The payroll employment report showed a net loss of over 20 Million jobs.

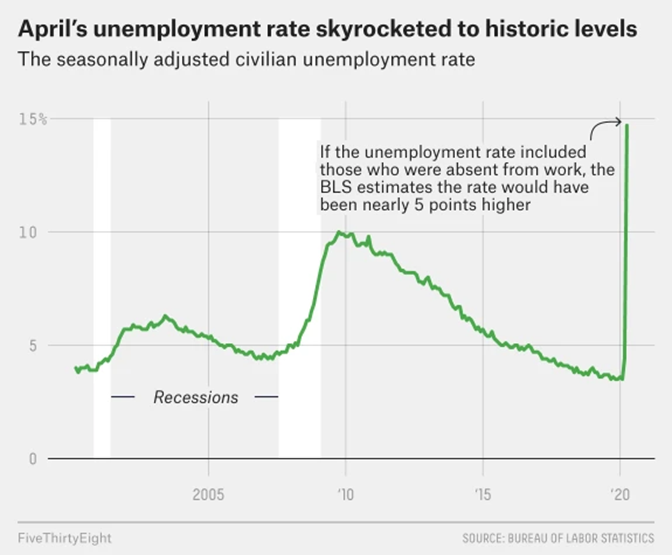

- The household survey showed unemployment reaching 14.7%. FiveThirtyEight says that it is even worse than that. The situation worsened after the survey time of mid-April. There was some questionable calculation based on whether people were “absent” or laid off. There is also a requirement that you be “actively looking for work” to be part of the labor force.

I have written extensively about employment and the jobs report methodology. I was afraid that the method of adjusting for non-respondents in the payroll survey would dramatically understate the loss of jobs. I studied the report and the technical notes. There are problems in adjusting on the fly in the face of massive changes, but the BLS team made a good and honest effort to do so.

The Ugly

U.S.-China relations, where the “pandemic has brought relations between the two to a modern-day nadir as they try to outmaneuver one another to shape the world order” reports the WSJ. Despite a news release of new trade talks during the week, the potential for China to meet the import goals seems remote.

This is happening at a time when people are more concerned about the extra costs they face.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

The economic calendar has many reports and is starting to include meaningful information. Small business optimism and Michigan sentiment will be important. Retail sales and industrial production for April will provide the missing pieces in the “Big Four” (see Quant Corner below). Jobless claims, especially continuing claims, provide the most recent take on the employment news. I am not very interested in the regional Fed indexes or the March JOLTs report, but others will try to squeeze some information from them.

The pandemic story and the economic reopening will continue to lead the news.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Background

Ready or not, the reopening of the economy has begun and is proceeding swiftly. Few are following my suggestion to analyze with a causal model including these factors:

- Science

- Government responses

- Economic effects

- Corporate earnings

And only then the implications for stocks.

My suggestions that we look to scientists for science, avoid politics in analyzing policy, recognize that economists are not epidemiologists, and seek a company-by-company analysis of effects? No luck with that either. Experts cannot resist the temptation to swing outside their “happy zone.”

With that in mind, I will hit the high spots of current developments. These are things that are important to an investor wanting to make intelligent, fact-based decisions.

Scientific Progress

Faster communication of scientific findings – “peer review to Twitter” (Bloomberg).

Moderna Speeds Up Timeline for Covid-19 Vaccine, Gets All-Clear for Phase 2 Trial

But even possible solutions raise issues if the rules are not clear. Doctors lambaste federal process for distributing Covid-19 drug remdesivir

And finally, Mounting promises on Covid-19 vaccines are fueling false expectations, experts say

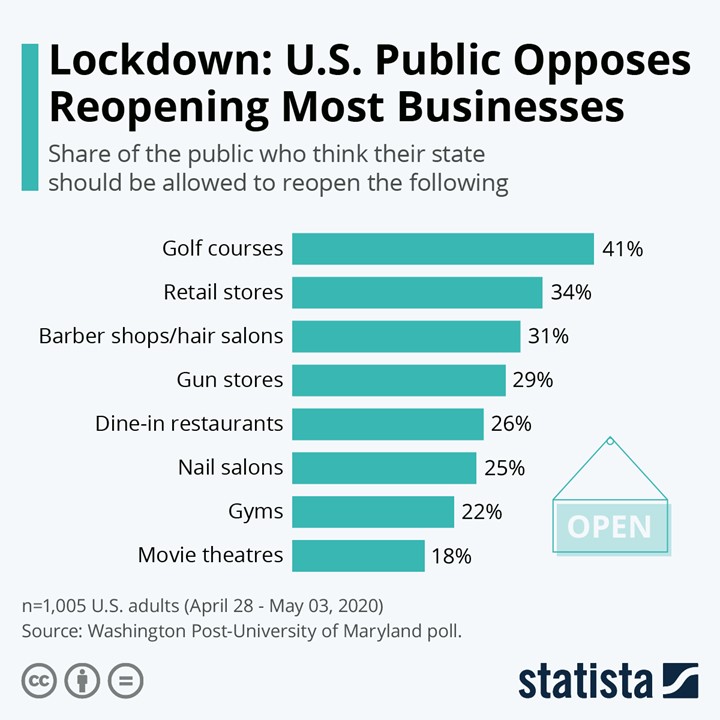

Public Attitudes

Even if businesses reopen, most of the public is not ready to return.

Results from FiveThirtyEight’s weekly roundup show similar results.

Testing Progress

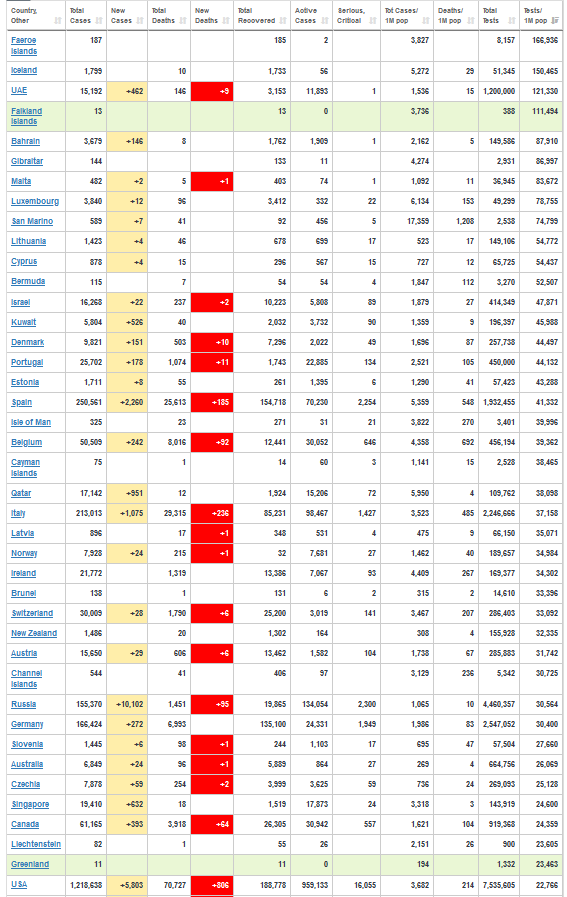

Suppose we ranked countries by number of COVID19 tests per million of population. Where do you think the US ranks? (Answer in today’s Final Thought.)

The current pace is 250K per day. Is that enough? (The Hill)

But as states prepare to reopen, the Harvard Global Health Institute sees a need for more than 900,000 tests a day, an increase from previous estimates because of projections for more infections as people begin interacting again in reopened states.

Ideally, the U.S. would be able to test everyone with symptoms and their close contacts through a process called contact tracing in addition to testing individuals who aren’t showing symptoms but could still be spreading the virus.

However, the country is far from setting up the kind of medical surveillance needed to fully reopen the economy. That shortcoming will become acute in the fall, when doctors will need to distinguish the flu from COVID-19, experts say.

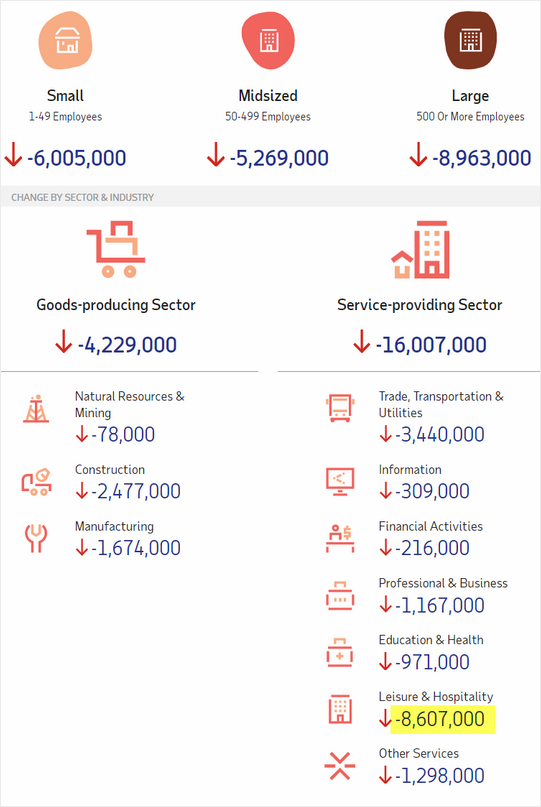

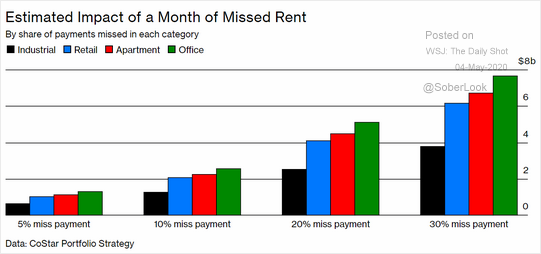

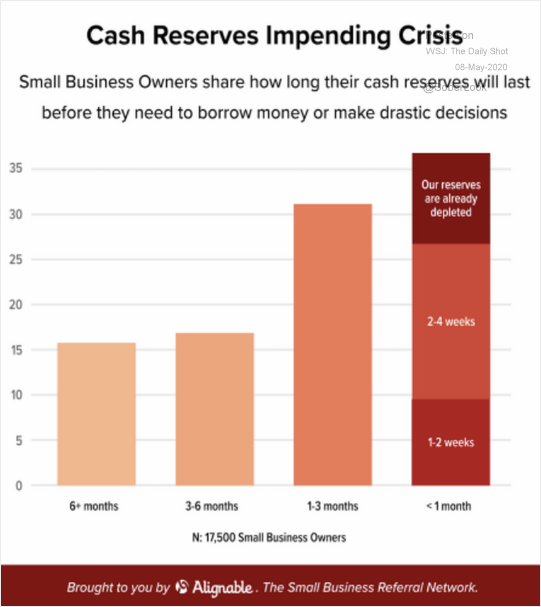

Economic Effects

There are some indicators that go beyond the regular reported data. The two charts below show the significance of the crisis for individuals, landlords, and small business. The duration of the decline matters – a lot!

Corporate Earnings Effects

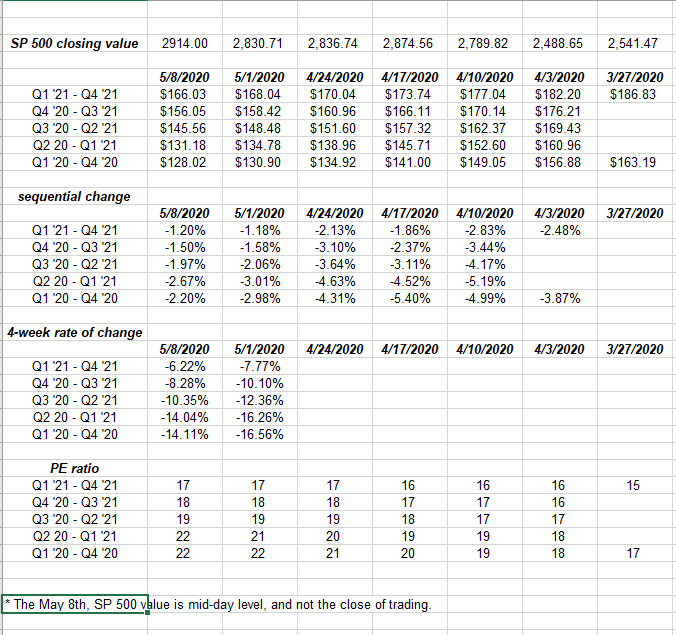

With 86% of the S&P 500 reporting, Q1 earnings have once again beaten the greatly reduced expectations – just not as much as in the past five years. The blended average growth rate is 0.6% (FactSet).

More important for investors is what lies ahead. Brian Gilmartin’s regular reports on this topic included two important updates last week. First, he described the significance of “the forward earnings curve.” Instead of looking at periods defined by the calendar, you have a rolling look ahead. This post describes the updating process. He also provides data on the rate of change in the estimates.

In the second post, he describes the “sequential improvements in the rate of decline.” This is yet another example of the challenge for investors during this crisis. We know that things are bad, but we need indicators to see when they are “less bad.” This article includes several interesting facts which you probably didn’t know. Fiscal response has raised household income to a level that is 30% higher than before the crisis? Should one consider an eighteen-month horizon for forward earnings? Here is a key table of the most recent data.

Market Outlook

Opinions about the economic and financial outlook cover a wide spectrum. Here are a few examples from some of my regular sources.

Scott Grannis is applauding the reopening and emphasizing the cost of the “most expensive self-inflicted injury in the history of mankind.”

It’s worth pointing out that cash yields almost nothing in nominal terms and is thus a wasting asset in regards to purchasing power. Faced with the strong likelihood of an ongoing recovery (however weak or strong it might be), plus an extended period of low interest rates directed by the Fed, a decision to hold on to cash is equivalent to taking an extremely expensive anxiolytic.

Paul Schatz sees a trading range.

Kirk Spano is worried about a depression.

As usual, I’ll suggest some conclusions of my own in today’s Final Thought.

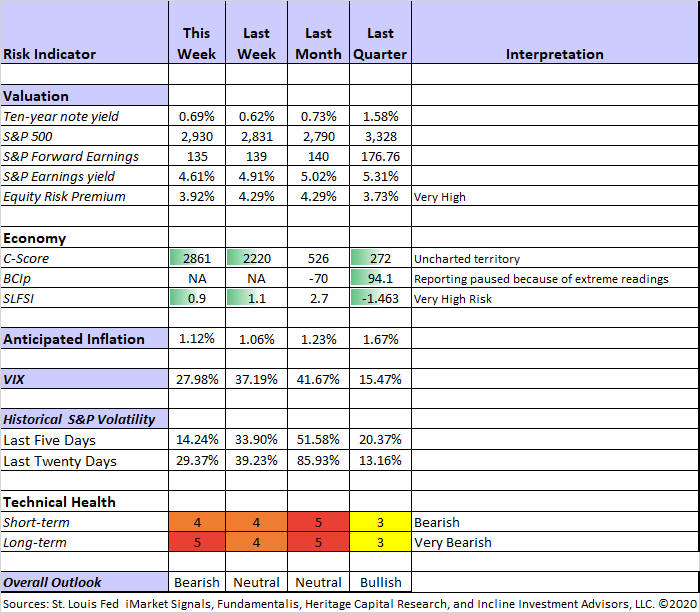

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

The C-Score spiked again. It is a dramatic change in underlying factors which normally provide important indications. This level is an extreme outlier that cannot readily be interpreted. Georg Vrba has paused the BCIp signal because of the extreme readings. It has done its job for now.

I have moved to a rating of “Bearish” in the overall outlook for long-term investors. I did some selling last week and plan to do more. I expect to replace positions with stocks that will do extremely well in an economic rebound.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. Georg’s business cycle index continues its steep decline.

David Moenning: Developer and “keeper” of the Indicator Wall. His most recent update summarizes the key elements.

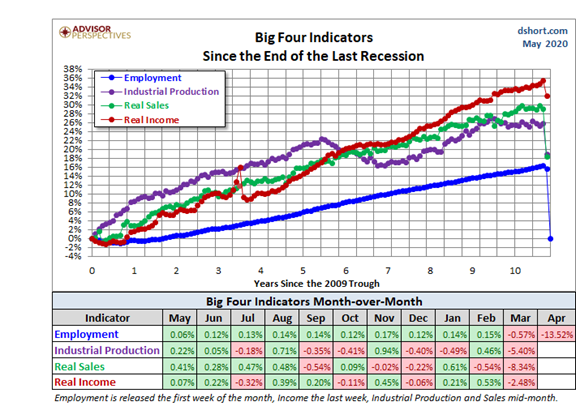

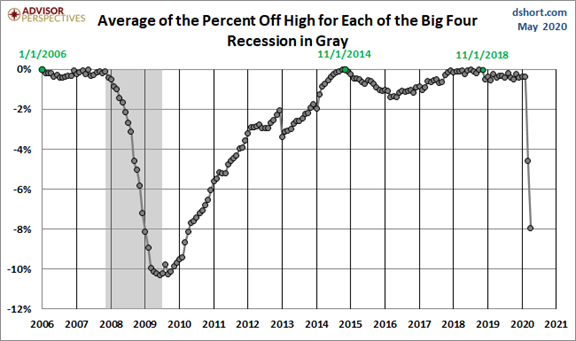

Doug Short and Jill Mislinski: Regular updating of an array of indicators, including the very helpful Big Four.

We can finally see what the start of a recession looks like. The sharp decline is apparent and broad. If it is sustained as everyone expects then the NBER might call March or April the month when the recession started. We will not get that verdict for a year or so, but it is not the job of the NBER to forecast. That is why we have other models. This chart shows how much more rapidly the indicators got to recession territory than in the Great Recession.

Guest Commentary

From Timothy Taylor, the Conversable Economist. (See the post for the list of papers).

Want to keep up to speed on what economists have to say about the pandemic? The Centre for Economic Policy Research has started a new journal, Covid Economics: Vetted and Real-Time Papers, with VERY short publication lag-times. The first issue of the journal, with six papers, appeared April 5. The 14th issue (not a typo) of the journal appeared today, May 6, with these eight papers:

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I were to recommend a single must-read investment article this week, it would be Tim Duy’s analysis of whether and how the economic downturn could become a depression. He emphasizes the duration, doing better than almost all economists by acknowledging, “We can’t accurately forecast the duration of the downturn because it depends on the course of the virus.”

Still, any rebound will not be akin to simply flipping a light switch back to the “on” position. It will be more like turning the dial on a dimmer switch, maybe quickly at first but more slowly thereafter. How much we can turn the dial at first, and how quickly thereafter, will determine the recovery’s duration.

He then does a careful analysis of the post-crisis effects, emphasizing changes that will persist for a long time.

And he cites the need for another massive fiscal package.

This article pulls together many important threads for investors.

Stock Ideas

Here are a very few ideas to consider, keeping in mind the companies and sectors that will be viable after the Great Reset.

Beth Kindig updates her analysis of Roku (ROKU). Her take is always valuable and especially so on this company. Key question: Should the company go for the top or bottom line? And a corollary, will investors misunderstand (again).

Qualcomm: Ignore Weakness

opines Stone Fox Capital which likes the resilience.

Or how about PayPal (PYPL). D.J. Martins Research says the “crisis was just a bump in the road” as business improved in April.

Alphabet (GOOG) – high quality with meaningful capital appreciation upside reports Valuentum.

Housing stocks. Ace analyst Ivy Zelman explains why this will continue to be a strong market. She describes her top homebuilders, some related stocks, and some names to avoid. This sector is a focus of my Great Reset research. In interview fashion, she responds to several great questions about mortgage rates, regional variation, and new homes as a share of the market.

Over the past several years, new homes have been taking market share from resales, as builders have increasingly been adding affordable supply to the inventory-starved entry-level segment. In 2019, new homes represented 13% of total home sales in the U.S., up from a trough of just 7% in 2011. In the near term, we believe new homes will continue to take share, as homeowners pull listings from the market due to health concerns over having strangers visiting their homes. After the pandemic ends, we expect consumers to increasingly favor new homes for the reasons they have for several years—innovative floor plans and technological advancements, including home automation.

I’m always interested in articles about value stocks, and Barron’s suggests nine of them from three different managers. There are some ideas (and I own two of them), but I sense some reaching going on.

Income ideas

Dividend aristocrats have been lagging during the market decline (David Templeton).

Renter Strikes? Colorado Wealth Management considers the implications for REITs, finding many choices with attractive entry points.

The Great Reset

Chuck Carnevale emphasizes the wide variation in the COVID19 impact on stocks in a recession like no other he has seen is a five-decade career. Where does it leave investors?

…(B)ecause valuations were so extended on so many companies, even the severity of this correction did not bring them into prudent valuation levels. I do not think I have ever seen a recession where so many stocks remain as highly valued as they do today.

In closing, what we have today is clearly a market of stocks and not a stock market. Furthermore, it is also a stock picker’s market. There is a lot of value to be found, however, as previously stated, this is a different kind of value. The best kind of value is when fundamentals remain strong, and only price falls. In this case, perhaps the most opportunistic value will be found where both price and fundamentals have fallen in tandem. Consequently, most of today’s value represents turnaround situations.

His conclusion is an emphasis on stock-picking, one of the elements of The Great Reset approach.

Investors Turn to Stock Picking at the Expense of S&P 500 Funds

The most closely-watched earnings season in history, now winding to a close, has thrown the difference between companies thriving from economic shutdowns and those decimated by it into sharper focus. While almost every sector ETF saw inflows in April, health-care and technology funds led the intake.

It is not enough to be a passive investor in active methods (Alpha Architect). The academic research cites five factors.

In sum, we identify five pitfalls when active investing is approached with passive investing techniques. First, the split in responsibilities between index provider and index replicator means that there is no more accountability for overall performance. Second, trading big on just a handful of days each year according to a preset schedule is inefficient and involves opportunity costs. Third, factor index strategies are active strategies focused on asset gathering and without the intention, or the means, to control capacity. Fourth, the preannouncement of index reconstitutions makes indices vulnerable to predatory trading by hedge funds, and to gaming by passive managers who can influence the prices against which they will be benchmarked. Fifth and finally, whereas active strategies can evolve based on new insights and research, index strategies tend to be set in stone, based on the knowledge at the time of their development.

Watch out for

American Brands That Might Not Survive the Coronavirus. These are just ideas, but useful for those of us analyzing the Great Reset.

The Stanford Chemist identifies three overvalued closed-end funds.

Boeing (BA). The beleaguered company now faces problems from suppliers.

High-Yield Bond Funds. If these are part of your portfolio, you should read this article. The “fallen angels” losing investment grade ratings have added apparent quality and duration to the funds, but historically, such changes do not last.

Final Thought

As I always try to do, I am writing this week as if the reader were here with me for a conversation. (Mrs. Oldprof says that it must be a long conversation with me doing most of the talking!) Perhaps so. I am describing the challenging logical process required to make good investments in this market. It is more difficult than ever because even small matters, like whether you wear a mask, have become inflammatory political signals.

My local newspaper quoted a maskless woman as saying that if she were going to get the virus, she’d have it by now. Why bother?

The challenge of putting aside our politics is greater when our leaders are so sharply divided. We all want so much for things to return to normal. This plays upon all the cognitive biases. Even clear-cut data may not be convincing for some.

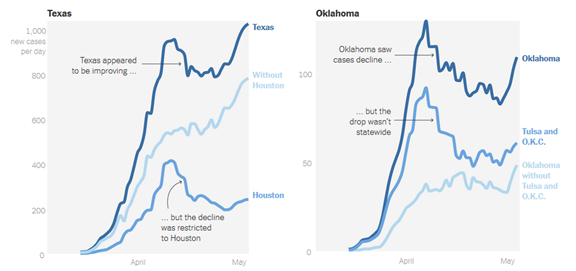

- Areas which loosened restrictions early. There is an opinion piece in the New York Times from their graphics reporter. Feel free to reach your own conclusions, but please look at the interactive chart first. It gives a clear picture of how national data are affected by the worst, but now improving, areas. Here are two examples from early-easing states.

-

Yahoo Finance

“It’s exactly the kind of effect we’ve been worried about,” Maegan Fitzpatrick, who studies infectious diseases at the University, told the Washington Post. “This is not an unpredictable outcome with businesses opening in one location and people going to seek services there.”

In some ways, the slow opening of business in Georgia, Texas, and several other states is a litmus test for the United States as a whole. If protocols are lifted too early, it could lead to thousands of preventable deaths, epidemiological models show.

“If you lift the restriction too soon, a second wave will come, and the damage will be substantial both medically and economically. We don’t want to throw away the sacrifices we have made for weeks now,” Turgay Ayer, a research director for healthcare analytics at Georgia Institute of Technology, told The Daily Beast.

- The opening of specific locations will also attract attention. Will new rules work? Fortune covers Shanghai Disneyland.

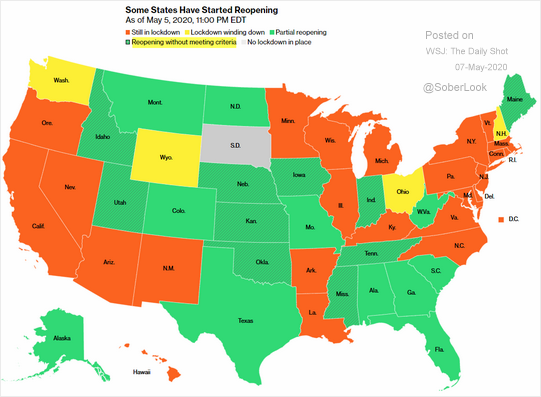

The pressure to reopen, ready or not. Bloomberg reports on the pressures faced by states and which meet the federal criteria.

Arizona is opening soon, so I could get a haircut if I wished.

Earnings. I especially appreciated Brian Gilmartin’s work. Investors need an anchor for their analysis. While making earnings estimates is always a challenge, I prefer the efforts of the bottoms-up analysts, especially right now. They are in touch with the covered companies, so we have a better chance of seeing the economic effects on earnings. The work illustrates the decline in the attractiveness of the overall market and the need to focus on individual stocks.

Here is the list of testing by country promised above. I stopped with the US (sorry Belarus), but there are obviously many more.

Be wise in your personal choices and very careful with your investments.

A Personal Request

One of my personal 2020 resolutions was even more emphasis on investor education – not just recommending stocks but learning how to find suitable choices. I have created a resource page where you can join my Great Reset group. You will get updates about what is being studied and can join in the process. There is no charge and no obligation, but I hope you will join in my Wisdom of Crowds surveys. I need more wise participants!

The results of our team effort will be published on a regular basis, so you will be joining me in contributing to a greater good.

I’m more worried about

- The complication of another disaster with the coronavirus. It is past time to put a stop to wars.

- The ability to conduct a normal election process, including conventions and actual voting.

I’m less worried about

- Scientific discovery and industrial innovation. I was pretty optimistic in my expectations for progress, but it is even better than I hoped.

© NewArc Investments, Inc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits