Want to read more by Nasdaq Dorsey Wright? Visit their Featured Firm page here

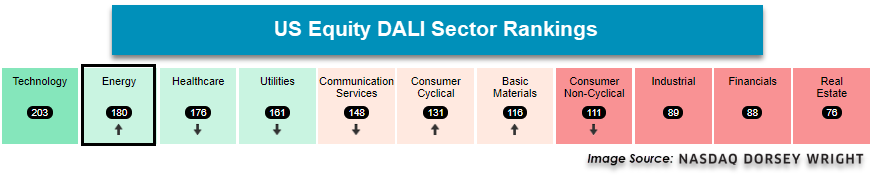

April was a strong month for the market with the S&P500 returning more than 12%. This came on the heels of an extremely volatile month that was March 2020 where the S&P 500 corrected 12.50% when all was said and done. However, there was a ton of volatility to get there. Underneath the surface, the carnage of March saw major changes within the Nasdaq Dorsey Wright Dynamic Asset Level Investing (DALI), most notably seeing US equity drop to the number four spot after holding the top spot for nearly four years! US equity has recovered a bit. At the lows, US equity was the fourth ranked asset class out of six and has recently moved back up to the number three ranked asset class with cash and fixed income still in the number one and two spots, respectively. All that being said, the past week has been fairly quiet in terms of new signals gained or lost on the asset class level, but the activity on the sector level has been dramatic for one sector in particular – energy.

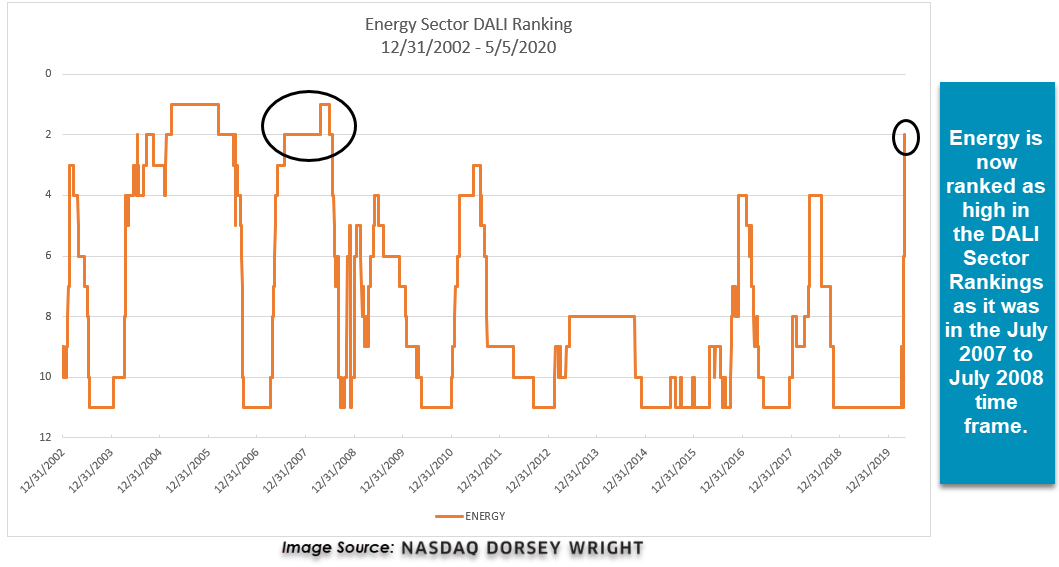

The energy sector was at the bottom of the US sector ranking coming into April; however, the energy sector has seen notable improvement recently and energy has moved up into the number two spot. That’s right, number two! Only the technology sector is ranked higher at this time. The last time that energy was ranked this high in the sector rankings of DALI was from July 2007 to July 2008.

Energy prices back then were very different than they are today. In July 2007, crude oil was changing hands for somewhere in the neighborhood of $70/bbl, which one year later would have been considered cheap! By July 2008, crude oil had reached its all-time high of $147. From July 25th, 2007, to July 23rd, 2008, the energy sector was ranked two or higher in the DALI sector rankings and crude oil surged more than 64% while energy stocks managed to post positive returns in an environment where stocks, in general, were down. Over that time period, the S&P 500 (SPX) was down 15.54% and the S&P 500 Equal Weighted Index (SPXEWI) was down 16.87%. On the other hand, the Energy Select Sector SPDR (XLE) was up 0.67% and the Invesco S&P Equal Weighted Energy Sector ETF (RYE) was up 4.5%.

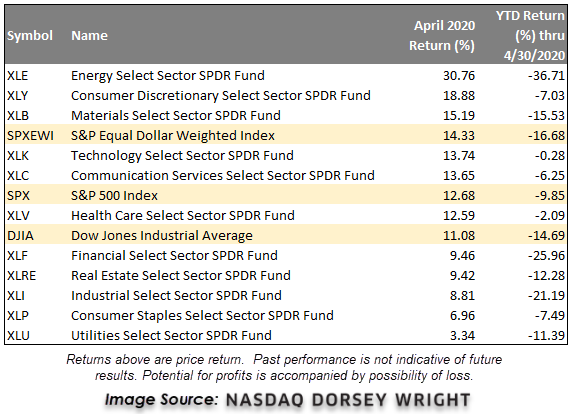

As it stands now, energy has just recently moved to number two so we don’t know how this will play out; however, what we do know is that energy has seen notable improvement from a relative and absolute basis. As well as the broad market did in April, energy was the best performing sector as XLE was up more than 30%. On a year to date basis, energy is still the worst-performing with a return of -36.71% while the S&P 500 is down about 10% and the SPXEWI is down almost 17% through the end of April. Energy is a sector that has seen short-lived rallies peter out pretty quickly over the years like in 2016 and even early 2017, but it has been over 12 years since the sector has been ranked this high. Further, we have seen energy rotate into a number of sector models All that being said, while energy is still one of the “least important” sectors in the S&P 500 with just a 3% weighting in the index, it is a sector that is worth taking note of in this market environment.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value.