Executive Summary

Recent unprecedented action by central banks, notably the Federal Reserve on April 9th, has helped markets recover meaningfully. This has caused many investors to wonder, “What do we do next?” or, “Did we miss the rally?” While credit spreads have tightened ~300 bps from March levels, they are still very attractive today versus history and remain at levels not seen since the 2008 Global Financial Crisis. We believe that a nimble approach to credit selection can offer enhanced downside protection and structural seniority while potentially generating double-digit returns. Although many performing credit investors are now chasing Fed flows into the highest-quality high yield issuers and many traditional distressed investors believe that now is the time to focus on defaulted debt, we believe the most attractive investing opportunity set today is in a middle area that we like to call “stressed performing” credit. In particular, we have found that this area of the credit market has created a unique mispricing where we are able to acquire the debt of quality businesses facing short-term business complications at low dollar prices with equity-like total return potential, but without the long-term secular challenges faced by the current crop of defaulted debt. There will be a time to buy defaulted debt in size, but we believe stressed performing debt is the most attractive opportunity in the credit markets today.

Oh, the Places the Fed Will Go!

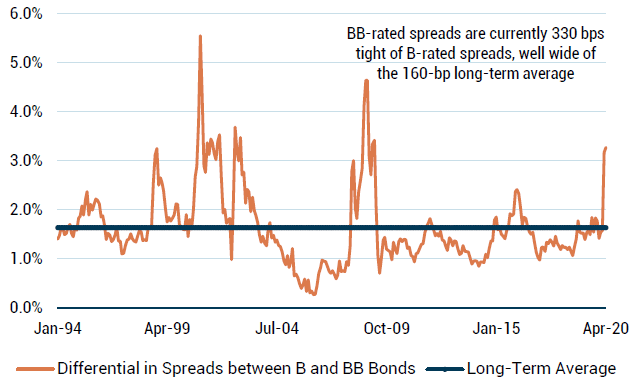

While Mr. Market moves in funny ways sometimes, many investors were scratching their heads over the moves of the Federal Reserve on April 9th, as the Fed’s “bondzooka” sent a tidal wave of bullishness through the markets. The most notable part of this Fed action was its commitment to purchase fallen angels and U.S.-listed ETFs with exposure to corporate bonds, which included certain high yield issuers and ETFs for the first time.1 This Fed action led to a rally in high-quality high yield and leveraged loan names, with the highest-rated BB credits leading the way. Since March lows, BB bonds have outperformed B-rated and CCC-rated bonds by 3% and 6%, respectively, and through April 2020, BB bonds are down only 7% YTD (versus -12% for single B and -15% for CCC-rated bonds).2 Per Exhibit 1, the difference between BB- and B-rated bond spreads is now 330 bps, which is well wide of its long-term average of 160 bps, reflecting the diminished opportunity available in BB bonds today versus the more stressed area of high yield.3

EXHIBIT 1: DIFFERENTIAL BETWEEN B AND BB SPREAD LEVELS

As of 5/1/20 | Source: J.P. Morgan High Yield Monitor

While BB bond spreads are historically very tight relative to B bond spreads, credit spreads overall remain wide and attractive even after a roaring April that saw high yield gain 3.6%:

-

High yield spreads today sit at 839 bps, versus their 30-year historical average of 566 bps and recent wides of 1139 bps on March 23, 2020.4

-

Leveraged loan spreads are 852 bps, versus their 30-year historical average of 574 bps and recent wides of 1325 bps on March 23, 2020.5

While we believe credit remains very attractive overall, we believe that BBs have rallied so much that it is not wise for investors to simply own the high quality, highest beta part of high yield at this time.6 Similarly, we believe that it is too early to be buying only defaulted or soon-to-be defaulted debt (often rated CCC and below), as our current pipeline indicates that the companies filing for bankruptcy now are low quality in nature with more risks than stressed performing debt.

Is it Time to Buy Defaulted Debt?

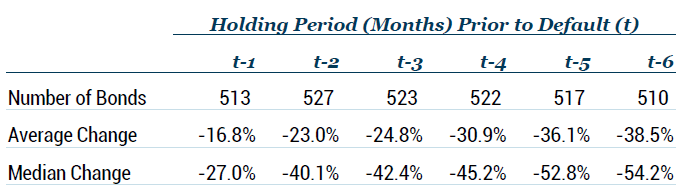

We believe that buying bankrupt debt is best when there is a wave of defaults that causes extreme forced selling and allows us to buy quality businesses at distressed prices. The time to pounce on defaulted debt is when there is an abundance of defaults after the default rate has spiked, but not before. As the Altman-Kuehne NYU Salomon Center Defaulted Bond Pricing Database has shown, price changes of defaulted corporate bonds immediately prior to a default event typically perform the worst and significantly underperform the overall credit markets. In Altman and Benhenni’s study7 of more than 500 bonds from 2002 to 2016, the average return for a bond 6 months prior to bankruptcy was -39%, 3 months prior to bankruptcy was -25%, and 1 month prior to bankruptcy was -17% (see Exhibit 2).

EXHIBIT 2: PRICE CHANGES ON DEFAULTED CORPORATE BONDS RETURN AND VOLATILITY PERFORMANCE PRIOR TO DEFAULT

Time period: 2002 – 2Q 2016 | Source: Altman-Kuehne NYU Salomon Center Defaulted Bond Pricing Database

Turning to the present, we are also observing this phenomenon in the current Coronavirus crisis with active and near-term bankruptcy candidates. While the default rate for bonds in April increased 140 bps to 4.7%, up from 3.3% in March, when we exclude Energy – which has been a large portion of defaults – from the list, the default rate today still sits at just 3.5%, a level barely above its long-term average of 3.4%.8 In April 2020, a record 19 companies filed for bankruptcy or missed an interest payment, and one company executed a complex distressed exchange. Ultimately, this affected $36 billion of bonds and loans, amounting to the fifth largest monthly default volume on record! This raises the common question, “Is now the time to dive in?” We believe the answer is, “Not yet.” While the April default data looks compelling, the month was driven largely by the default and missed interest payments of Frontier Communications and Intelsat, with $17.5 billion and $14.6 billion of affected debt, respectively. Both companies have faced significant industry and business challenges for years, with Frontier struggling as a legacy wireline telecom provider with an underinvested network and Intelsat facing industry secular pressure from the vast build-out of fiber around the world as well as significant price reductions for its services. These companies were expected to restructure regardless of the Coronavirus pandemic.

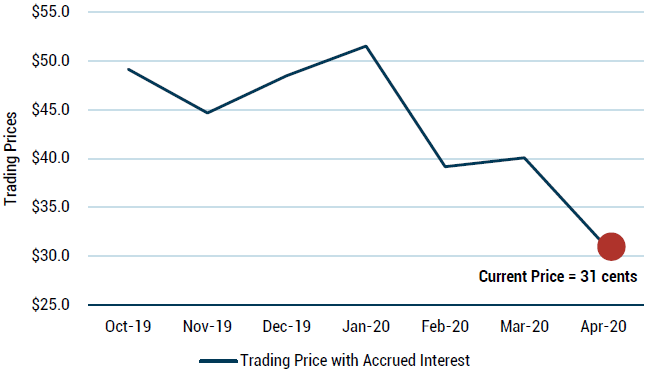

In Exhibit 3, we have plotted the trading prices of Frontier unsecured bonds – the majority of its outstanding debt – from 6 months ago all the way through April 30th, 15 days after Frontier officially filed bankruptcy. As we can see, the bonds traded down from close to 50 cents on the dollar in October 2019 to 31 cents on the dollar at the end of April. This resulted in a 37% decline in value during this 6-month period while high yield declined only 5% in the same period on a total return basis.9

EXHIBIT 3: FRONTIER UNSECURED BONDS PRE-DEFAULT

As of 4/30/20 | Source: Bloomberg

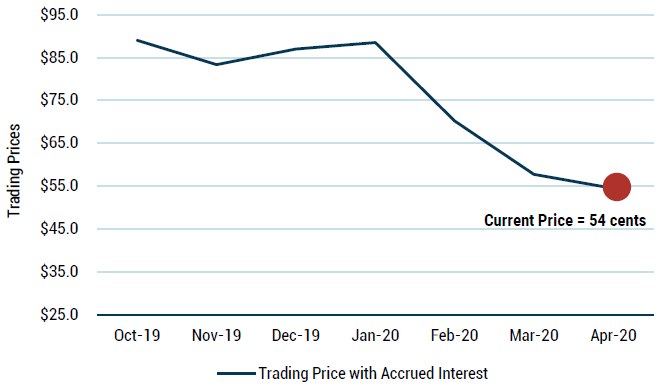

Similarly, in mid-April, Intelsat missed interest payments on its unsecured bonds and is currently in its grace period. At this point, most market participants expect Intelsat to file for bankruptcy in the near term. As we can see in Exhibit 4, as with Frontier, Intelsat’s unsecured bonds have also been a poor investment heading into an expected default period with these bonds returning -39% in the past ~6 months and a stunning -22% alone in the past 2 months through the end of April versus high yield at only -5% and -7.7% in each respective period.10

EXHIBIT 4: INTELSAT UNSECURED BONDS PRE-DEFAULT

As of 4/30/20 | Source: Bloomberg

While some may view this underperformance as a significant opportunity to buy defaulted paper, we believe that businesses like Frontier and Intelsat were bound to restructure as a result of major secular headwinds unrelated to the Coronavirus and are inferior to the opportunities that we currently see in higher-quality debt, while also possessing greater process risk. Frontier and Intelsat are representative of the current defaulted debt opportunity set, which along with other existing bankruptcies, largely comprises challenged businesses with uncertain long-term prospects. Our current pipeline has shown us that it is too early to rush into the first defaulted debt opportunities as the risk-reward remains poor relative to the opportunities in the stressed performing credit of higher-quality businesses.

So, Where’s the Opportunity?

While we believe that BB high yield credit has broadly rallied to levels that make it less attractive and the defaulted debt opportunity set has not yet become broadly attractive, where are we finding the best opportunities? Somewhere in the middle.

We have been focused on a variety of unique dislocations for high-quality businesses facing short-term (but not fatal) challenges from the Coronavirus that trade at attractive dollar prices with large public market equity value behind their debt. Our pipeline has never been larger for these stressed performing debt opportunities, and most of these opportunities trade at dollar prices ranging from 70-90 cents (down from well over par pre-virus) offering yields of 7-15% and total return potential of 25%+. We have invested in and continue to evaluate a number of these opportunities including:

-

First lien secured debt in a sports media company at a dollar price under 80 cents, with a double-digit yield and a market value of debt equal to ~30% of the total public enterprise value of the company, which includes its large public equity market cap.

-

Unsecured investment-grade debt of specialty finance companies at dollar prices of 75-85 cents, with 7-12% yields, and debt to equity levels ranging from 0.5-1.0x.

-

First lien secured debt in a leisure business at dollar prices in the low 80s, with a high single-digit/low double-digit yield with the market value of net debt roughly equal to its market cap and also equal to 28% of pre-virus enterprise value.

-

First lien secured debt in a diversified insurance brokerage business in the mid-high 80s with a low double-digit yield, with bond prices down from 105 cents pre-virus and liquidity lasting more than 3 years.

-

First lien senior secured debt of a healthcare company that manufactures and distributes personal protective equipment with its bonds down 10-15% on the year, despite a higher equity price, creating bonds at ~55% of enterprise value and

-

working capital.

These are just a handful of the opportunities we are seeing today. In each of these investments, we see attractive double-digit total return potential, with less process and valuation risk than defaulted debt. We believe this investment profile allows us the potential to generate stronger idiosyncratic return regardless of market direction. While we are distressed investors at heart, we currently see the most attractive opportunities in companies that will largely recover from near-term disruptions, while other credits continue to struggle and ultimately default, leading to a potentially more fertile distressed opportunity set down the road. As value investors, we cannot let our desires for a more robust defaulted debt landscape influence our decisions about how best to position the portfolio today.

In general, credit is highly attractive today but very idiosyncratic in nature, therefore requiring a keen focus on active fundamental analysis. While the Fed’s actions have caused a lot of questions among many investors wondering where to go next, we believe stressed performing credit presents the best risk-adjusted returns. While we hope there will be a time for us in the medium term to be aggressive on defaulted “distressed” debt, we are finding better value today in quality businesses that face short-term obstacles yet maintain the liquidity to withstand a severe stress recession scenario. We are confident that this is the best approach today to maximize return with the least amount of risk.

Download article here.

1Bloomberg

2J.P. Morgan High Yield Monitor, May 1, 2020.

3Op. cit.

4Op. cit.

5Leveraged Loan Spreads calculated versus 3-Year Treasuries; J.P. Morgan High Yield Monitor, May 1, 2020.

6We do believe that certain BB bonds remain very attractive now as there have been dislocations throughout the credit market. However, these opportunities are idiosyncratic and require deep fundamental analysis, rather than simply owning BBs, which we think no longer presents the best overall opportunity set in credit today.

7Edward I. Altman and Robert Benhenni, “The Anatomy of Distressed Debt Markets,” Annual Review of Financial Economics, Vol. 11, pp. 21-37, December 2019.

8J.P. Morgan High Yield Market Monitor.

9Bloomberg, using Frontier 11% Unsecured Notes as illustrative example; using IBoxx High Yield performance for high yield.

10Bloomberg, using Intelsat 5.5% Unsecured Bonds due 2023 as illustrative example; using IBoxx High Yield performance for high yield.

The views expressed are the views of Jeff Friedman through the period ending May 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2020 by GMO LLC. All rights reserved.

© GMO