A Is for Annual Rebalancing. and It's Never Been More Vital.

Want to read more by Russell Investments? Visit their Featured Firm page here

I’m trying to think of a year when rebalancing has been more important. None come to mind.

At Russell Investments, we believe in the value of an advisor. And this year, we believe in advisors more than ever. The more difficult markets become, the more advisors matter. That’s why we’ll be sharing five deeper dive blog posts, digging into the details of our annual study on this topic. This is our first of the five, and the topic is annual rebalancing.

Right now is the right time to dig deeper. We’re in the middle of a market, economic and societal event like none of us have ever experienced. We’ve all been impacted by it—if not directly to our health, then by changes to the way we work, the way we connect to each other and certainly by the way we think about financial security.

As an advisor, you know how stressed your clients are. They want to know how certain their financial plan still is. They want to know what the future holds for their investments. They want to know what to do. Most of all, they want to know that they and their family will be ok. When markets are rising calmly, I suppose it can be easy to underestimate the importance of disciplined rebalancing. But when volatility strikes—and it’s never struck as hard as it has this year—this annual process should get the attention it deserves.

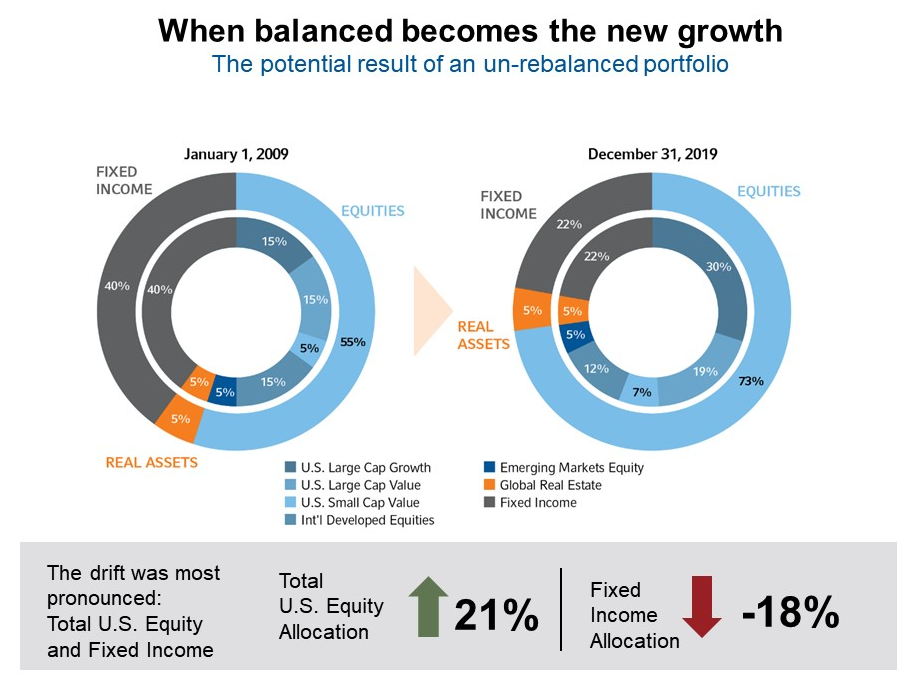

Minimize the drift

As the chart below demonstrates, a hypothetical balanced index portfolio that has not been rebalanced would look more like a growth portfolio and expose the investor to risk they may not have agreed to. And the data used here ended at the end of December 2019. Imagine how far off track a portfolio could get this year without rebalancing.

Click image to enlarge

Source: Hypothetical analysis provided in the chart & table above for illustrative purposes only. Source for both chart & table: U.S. Large Cap Growth: Russell 1000 Growth, U.S. Large Cap Value: Russell 1000 Value, U.S. Small Cap: Russell 2000, International Developed Equities: MSCI World ex USA, Emerging Markets Equity: MSCI EM, Global Real Estate: FTSE EPRA NAREIT Developed, and Fixed Income: Bloomberg Barclays U.S. Aggregate Bond.

Is now the right time to rebalance?

This year, as my colleagues, Sam Pittman and Natalie Miller explain, it’s likely that recent large market drops have pushed your clients’ asset allocations away from their policy allocations to something more conservative. Consider, for example, a 60/40 balanced portfolio of 60% MSCI ACWI Index and 40% U.S. Bloomberg Barclays Aggregate Bond Index. Between Dec. 31, 2019 and March 20, 2020, the MSCI ACWI Index was down 30% while the Bloomberg Barclays Aggregate Bond Index was flat. From Dec. 31, 2019 to March 20, 2020, that portfolio would have shifted from 60/40 to 51/49, with an allocation of 51% MSCI ACWI Index and 49% Bloomberg Barclays Aggregate Bond Index. Should this portfolio be rebalanced back to target and what implications does rebalancing have on returns? I encourage you to read Sam and Natalie’s piece on the topic for deeper guidance. But the impact of that consideration shows just how vital your role as an advisor is. Assuming you’re doing the work, providing the guidance and helping your clients navigate these troubling times, it’s also important that they understand the value of that work.

The value communication gap

Do your clients recognize the value of what you do? Establishing the value of all the good things that advisors do is completely dependent on good communication. This communication should cross styles. It should not just include what you write—via client emails, your online presence, or via traditional mail—but should also include what you say when you are face-to-face, phone-to-phone, or on video chat with investor clients. And my guess is that you’ve been making your Zoom or WebEx account work overtime lately.

We consistently find that there continues to be a disconnect between what advisors do and what their clients think they do. In other words, there is a value communication gap between advisors and their clients. Advisors don’t always know what their clients really value. They don’t always know what their reference clients say about them. And they don’t always understand what they should do less of and what they should do more of.

We believe that rebalancing is one of the most vital functions advisors provide. But the value of it is often downplayed. And when it comes to devaluing this vital service, advisors may be the main culprit. Why? Because it’s something they do every single day. It’s like breathing for advisors, and most of their clients don’t think about the impact of doing it or not doing it.

Unless you clearly communicate the value of rebalancing, don’t expect your clients to appreciate it. They should, because we think clients practice reverse rebalancing much of the time. We believe that without the help of advisors, clients are more likely to make fatal mistakes, such as buying high, selling low, or running to cash at precisely the wrong time.

How to tell the rebalancing story

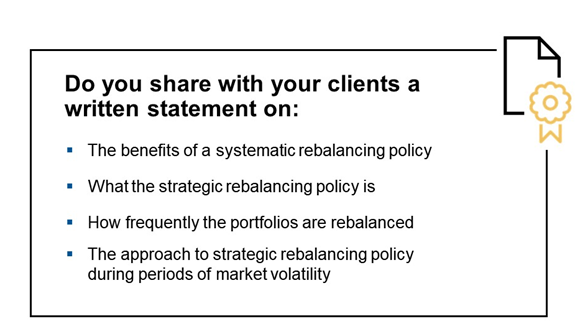

Do your clients recognize the value of annual rebalancing and how it’s a vital part of wealth management? If advisors don’t talk about rebalancing, don’t name it and don’t have conversations about it, then we can’t expect investors to understand its importance. We recommend four simple touchpoints to make the communication both easy for you and meaningful for your investor clients.

Click image to enlarge

- The benefits of a systematic rebalancing policy—Explain what can happen if rebalancing doesn’t happen and how annual rebalancing helps keep their portfolios on track with their goals and their risk profiles.

- What the strategic rebalancing policy is—Let your clients know the basics of the policy, how it works to be both efficient and oriented toward their desired outcomes.

- How frequently the portfolios are rebalanced—Explain how often strategic rebalancing happens and why you believe that frequency makes sense for them.

- The approach to strategic rebalancing policy during periods of market volatility—Let your clients know how sticking to a long-term, disciplined rebalancing policy can help them avoid costly mistakes, such as following the herd, buying high and selling low, and leaving the market at the worst times.

A blatant pitch for model strategies

Rebalancing takes time. And as valuable as it is, there may be other aspects of your job that provide even more value. The good news is that many advisors are increasingly using model strategies and communicating the model’s strategic philosophy and policies. Models hand the rebalancing role over to the expertise of asset managers. Adding models to your inventory helps take care of both the rebalancing policy and helps to free up your time for efforts that may deliver even more value (which we will dive into in our upcoming blog posts in this series. Stay tuned!)

Choose the solution that matches your outcome.

The bottom line

Rebalancing likely has more obvious value in 2020 than in any year in memory. But just because you recognize its importance, don’t assume your clients do the same. For them to understand the value of strategic rebalancing, you need to talk about it. This doesn’t have to be a complicated conversation—in fact, we suggest steering clear of the jargon. But we believe it needs to happen, because rebalancing is a key part of helping your investors achieve the financial security that matters so much to them.

To learn more about the 2020 Value of an Advisor Study, click here.

Disclosures

Bloomberg Barclays U.S. Aggregate Bond Index: An index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities, and mortgage-backed securities. (specifically: Barclays Government/Corporate Bond Index, the Asset-Backed Securities Index, and the Mortgage-Backed Securities Index).

FTSE EPRA/NAREIT Developed Index: A global market capitalization weighted index composed of listed real estate securities in the North American, European and Asian real estate markets.

MSCI ACWI is a market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. The MSCI ACWI is maintained by Morgan Stanley Capital International (MSCI) and is comprised of stocks from 23 developed countries and 24 emerging markets.

MSCI Emerging Markets Index: A float-adjusted market capitalization index that consists of indices in 21 emerging economies: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

MSCI World ex-USA Index: The MSCI All Country (AC) World ex U.S. Index tracks global stock market performance that includes developed and emerging markets but excludes the U.S.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values.

The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.

The Russell 3000® Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market.

Indices and benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Index return information is provided by vendors and although deemed reliable, is not guaranteed by Russell Investments or its affiliates. Due to timing of information, indices may be adjusted after the publication of this report.

ZOOM is a trademark of Zoom Video Communications, Inc.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

Copyright © Russell Investments Group, LLC 2020. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

Russell Investments Financial Services, LLC, member FINRA (www.finra.org), part of Russell Investments.

RIFIS: 22807