Diving into the Pronounced Size and Style Bias within the Current US Equity Market

Want to read more by Nasdaq Dorsey Wright? Visit their Featured Firm page here

Thus far in 2020 and throughout the COVID-19-induced sell-off and partial recovery, there has been a pronounced size and style bias within the US equity market in favor of growth over value and large-cap over small-cap. Large-cap growth sits atop the Dorsey Wright asset class size and style rankings, as it has for more than a year, with that relative strength advantage having been clearly demonstrated through the performance dispersion this year.

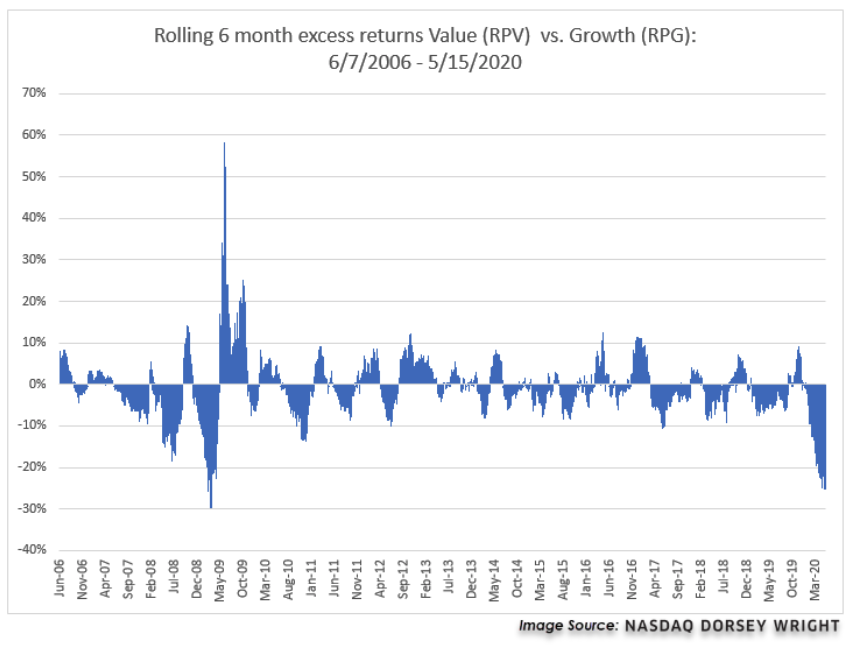

Year-to-date (through 5/18), the Invesco S&P 500 Pure Growth ETF (RPG) has generated a price return of -4.35%, putting it ahead of the S&P 500 Index (SPX) by just over 4.2%, as the Index has returned -8.57%. Meanwhile, the S&P 500 Pure Value ETF (RPV) has produced a return of -35.01% over the same period, a whopping differential of almost 31%. Dispersion at this level is something one might expect to see between the best- and worst-performing individual stocks in the S&P 500, but not between two style funds derived from the same index, each of which contains more than 100 holdings. On average since 2009, RPV and RPG have had a performance differential of 4.39% in any given calendar year. In 2016 RPV returned 17.05% while RPG returned 3.56%, making it the only year during this time that produced a performance difference in the double digits. So needless to say, the disparity we've seen this year is not typical. One way to view this relationship is through a rolling six-month return comparison of RPV against RPG from mid-2006 through last Friday (5/15). This picture represents how the relationship between these two funds typically rotates in favorability, with RPV being favored in certain times and RPG favored in others. When viewing the historical comparison we see that there has not been this level of dispersion favoring RPG since the early-2009 timeframe.

The stark contrast between growth and value is also readily apparent when we look at the technical pictures of RPG and RPV. RPG currently has a robust 4.86 fund score and a positive 1.15 fund score direction. After bottoming at $85 on its default chart in March, RPG has rebounded to give three consecutive buy signals, and with movement on Tuesday broke out to give a fourth consecutive buy signal at $121. Throughout the volatility of 2020, RPG has maintained its positive trend, which has been intact since 2015. RPV, by comparison, has a dismal 0.49 fund score and -3.70 score direction. On its default chart, RPV is currently on a sell signal after breaking a triple bottom in last week's trading. While the fund has rebounded from its March low, it has largely traded sideways in April and May and remains in a negative overall trend after violating its bullish support line in February.

The dispersion between growth and value has not been limited to large-cap – the iShares Russell 2000 Growth ETF (IWO) has posted a year-to-date return of -10.22%, which while weaker than its large-cap counterpart, is significantly better than that of the iShares Russell 2000 Value ETF (IWN) which is down -25.18%.

As mentioned at the onset, the second major size & style trend in the US equity market has been the dominance of large over small, which is evident in the relative performance of the SPX and the Russell 2000 (RUT) as RUT's year-to-date return of -20.07% lags the S&P's by 11.5%. What is less-readily apparent is that this size bias exists not only across, but within capitalization categories. While SPX is down -8.57% year-to-date, the S&P Equal Weighted Index is down nearly twice as much at -16.72%. Further illustrating this phenomenon, the Invesco S&P 500 Top 50 ETF (XLG), which holds the 50 largest companies in the S&P 500, has returned -3.08%, besting SPX by more than 5%. So, while demand for large-cap stocks has held up better than demand for small caps, it has been mega-cap stocks that investors have favored most.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Year-to-date returns are through 5/18/2020. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.