Want to read more by Russell Investments? Visit their Featured Firm page here

In a recent blog post, my colleague Will Pearce discussed why we persevere with value exposures when the style has struggled versus growth for an extended period. I want to highlight two key points about growth stocks that I find particularly compelling:

- Growth stocks are now behaving like a carry trade, where a large group of investors believe owning only these stocks is a low risk, guaranteed way to make money. This leads to a false sense of security and a big, negative surprise when market leadership changes.

- The combination of interest rates falling to essentially zero and little to no inflation has had the effect of increasing the present value of long term, potential future earnings.

Consider a bond with a 30-year maturity

As interest rates drop to near zero, the value you would pay today for the bond’s future coupon payments rises substantially. The same thinking can be applied to long duration earnings prevalent in equities with high levels of anticipated future growth. Once at this level, there is a high risk that you are overpaying for future opportunities as interest rates normalize.

For today’s investor considering what to own for the next 10 years, let's crystalize how these points impact stock valuations using real world examples.

An exercise in what you must believe

In this exercise we take the current price of a stock and break down the assumptions investors are making about future earnings growth. This isn’t hard—after all, a stock price is ultimately the present value of its future earnings potential. Putting this into practice, we adopted the same model used by the respected investment firm, Research Affiliates, updating and extending it for additional analysis that follows.

Using the current earnings and market value of a stock, we can estimate the amount of earnings growth required over the next 10 years to support the current valuation. In other words, what must investors believe about a company’s prospects to justify purchasing its stock at today’s prices?

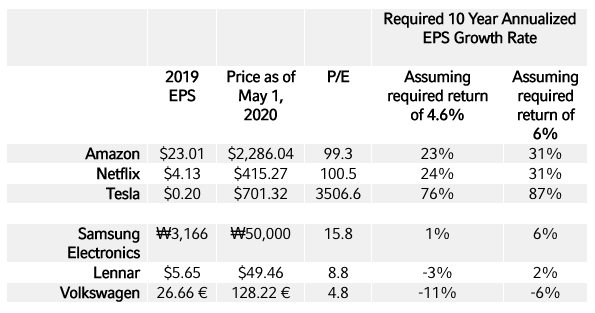

The table below summarizes the findings for three popular growth stocks and three stocks with significantly cheaper valuations. These stock examples are illustrative of the "valuation" gap and are not a recommendation.

What must the market believe to justify current prices?

Our growth stocks have some lofty assumptions embedded in their price. Assuming the market’s implied return requirement remains at 4.6%:

- Amazon and Netflix will have to post annualized earnings growth of well over 20% for the next 10 years.

- Tesla has much loftier expectations.

If we assume that the required return rises to 6% (a number we believe is generous given the amount of fiscal and monetary stimulus now making its way into the system), the required earnings growth rises even further.

To put this into perspective, Amazon is currently the third largest company in the S&P 500, Netflix is 24th and if Tesla was in the index, it would sit at number 43. If we look at the 50 largest U.S. companies 10 years ago, only one firm (Merck) was able to post 10-year annualized earnings growth of 30%. Only three were able to sustain earnings growth between 20% and 30%, and this includes Amazon.1

Do we really believe Amazon, Netflix and Tesla can accelerate growth even further for the next 10 years, given their current size? Maybe, but that is an incredibly high bar and would mean breaking all sorts of records for sustained earnings growth. More realistically, we expect competitive realities and a myriad of other forces, including regulation, economic developments and strategic missteps, to present substantial challenges to their continued dominance.

Any skilled stock picker will tell you that what matters most is the relative opportunity that lies ahead of you, and not to get locked into anchoring on the past. With that in mind, what must we believe about our three value stocks? One thing is for sure, the market has very low expectations for growth.

Looking at Samsung, do we really believe this electronics giant, a key supplier of OLED and 5G technology across the globe, is only capable of growing earnings at 3%? Do we believe a U.S. home builder like Lennar will shrink over the next 10 years as demographic shifts increase housing demand and low mortgage rates persist? And, at current prices, it appears the market thinks that in 10 years the only cars that will be sold are Teslas, and that other car companies like Volkswagen will have nothing left to offer!

It is exactly this sort of stretch in assumptions, driven by the current valuation dispersion, that excites us about the opportunity for value investing going forward. In our multi-manager funds, we hire what we believe to be best-in-class stock pickers, who scour the globe and look for opportunities of extreme dislocation in market price versus underlying company fundamentals.

Going back to Mr. Pearce’s blog post, we believe skilled active management means putting money to work in uncomfortable areas that offer attractive relative payoffs. We continue to follow our disciplined investment process that guides our decision-making and provides guardrails to ensure appropriate risk budgeting.

It is within this framework that we can tilt within the broad and diversified range of styles and return drivers that allow us to respond and take advantage of what the market gives us.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors, and size of companies preferred by the investment managers. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Please see a prospectus for further details.

The S&P 500® Index, or the Standard & Poor's 500, is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

Indexes are unmanaged and cannot be invested in directly.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2020. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

1 Source: FactSet