Want to read more by Guggenheim Investments? Visit their Featured Firm page here

The Federal Reserve (Fed) will face numerous challenges in the months and years ahead. Economic output will remain below potential for years to come as we deal with the pandemic and its long-term scarring effects. An additional challenge will be a U.S. federal government budget deficit that will exceed $3 trillion this year with significant likelihood that it could be larger. Absent further action by the Fed, this deluge of Treasury securities will likely start pushing interest rates higher, threatening the overall economic expansion. The Fed cannot allow this to happen. As I gaze into my crystal ball, the Fed’s roadmap is likely to include the following progression of policy tools as the economy remains mired in a protracted downturn:

Extended forward guidance: The first and most likely policy option will be to announce a lengthy period of forward guidance. Forward guidance is nothing more than the Fed saying it does not expect to raise interest rates for a period of time. Given the current situation, forward guidance will have to be aggressive. With the market already pricing rates staying very close to the zero bound for the next five years, there is not going to be very much shock and awe if the Fed announces that it will keep interest rates at zero for two or three years. Currently the two-year Treasury note is yielding 21 basis points (and got as low as 11 points on May 8), and the five-year note is at 46 basis points. Pegging the overnight rate at zero would have a limited effect on reducing rates at the front end of the yield curve.

To make sure that longer-term interest rates stay in a range that provides greater support to the U.S. economy and financing the U.S. Treasury, the Fed will have to provide forward guidance that zero interest rates will be necessary for a protracted period. Extended forward guidance will keep a substantial part of the yield curve well-anchored, so the prospect of long-term rates rising dramatically will be limited even as the economy strengthens and inflation picks up.

The Fed is going to want to establish the shortest minimum time it thinks it can get away with, yet still have the impact of shocking the market. The minimum period of time for keeping rates at the zero bound would be something like five years, but a longer time period may be necessary. The Fed will most likely establish a second condition of an inflation rate target. In this scenario, the Fed could commit to maintaining rates at the zero bound for at least five years, and possibly longer, subject to the average inflation rate needing to exceed 2 percent on average over a five-year period. Only upon meeting the inflation target condition would the Fed begin a lift off in rates. Such an approach would have the benefit of automatically extending the expected period at the zero lower bound if economic conditions worsen or the recovery falters.

Swap Market is Beginning to Price in Higher Rates Within 5 Years

Source: Guggenheim Investments, Bloomberg. Data as of 6.5.2020.

Formal QE Program: The likelihood that the Fed will have to continue to engage in sizable purchases of Treasury securities is very high. The ability to attract enough capital to finance a multi trillion-dollar deficit at current interest rates is limited.

The dirty little secret about quantitative easing during the financial crisis is that it was used to finance the U.S. Treasury and keep interest rates from skyrocketing and crowding out the private sector. The Fed wants to make sure credit is available at attractive rates, which means a formal quantitative easing (QE) program, or large-scale asset purchases, must be on the horizon.

Currently the pace of the Fed’s purchases is determined weekly based on market functioning metrics monitored by the Open Market Desk. In the next QE program, the FOMC will outline the composition, size, frequency, and duration of its asset purchases. Given the government’s financing needs, I expect that the next QE program will be larger than any previous rounds of QE in terms of monthly purchases. The current pace of Fed purchases ($6 billion per day, or roughly $125 billion per month) is insufficient to absorb the $170 billion in net monthly Treasury coupon issuance we forecast for the rest of the year, let alone the hundreds of billions of monthly net T-bill issuance we expect. The duration of the next QE program could also be tied to achieving specific dual mandate outcomes, given the high amount of uncertainty around how long the purchases will be needed.

It will likely take at least $2 trillion in asset purchases per year just to fund the Treasury. The commitment to large-scale asset purchases should allow the Fed to at least take a first step in trying to contain any increase in long-term rates. The trade-off here is that committing to the zero bound for a period of time through forward guidance could raise inflationary expectations, which means that longer-term rates could rise. The rate sensitivity of the mortgage market, and the importance of the housing sector to the overall economy, means the Fed is not going to want to see long-term rates skyrocket. The announcement of a QE program would let the market know that the Fed is prepared to absorb some of the supply that is driven by federal deficits, while increasing the money supply to support nominal economic growth.

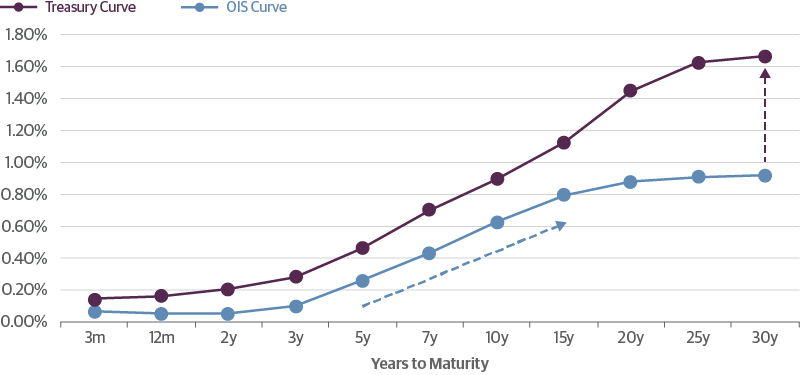

Yield Curves Show the Need for Fed Forward Guidance to Extend Beyond 5 Years and for QE to Support Treasury Securities

Source: Guggenheim Investments, Bloomberg. Data as of 6.5.2020.

Yield Curve Control: The first two items I’ve mentioned—extended forward guidance and a formal QE program—are very likely to occur within the next several months, perhaps in part as early as this Wednesday. If these programs fail to adequately support markets and the economy, the Fed will do more to support the economy and maintain satisfactory conditions for financing the government and corporations. The next option would be yield curve control. Very simply, yield curve control would require the central bank to announce that it will not allow interest rates across a portion of the curve to rise above a certain rate. For example, the Fed would announce a rate—say 50 basis points—and state that it stands ready to purchase all Treasury bonds of a certain tenor that trade above this level.

There is precedent for this policy tool. The Japanese government is currently engaged in yield curve control, and we did it here in the United States in the 1940s to help finance the war. The experience of yield curve control here and in Japan demonstrates that once the Fed announces that there is a put to the central bank at a certain interest rate level, it will not buy many securities. This has been the case with the Bank of Japan over the last year or so during their exercise in yield curve control and was the case for the Fed in the 1940s and early 1950s. It may not deliver as much incremental stimulus as outright QE, but it’s been used before, and it would effectively limit the rise in long-term rates and help ensure the effective transmission of forward guidance. The associated reduction in interest rate volatility would also help to lower mortgage rates and corporate bond yields.

It is worth noting that establishing a policy for yield curve control is fundamentally at odds with setting a quantitative target for QE purchases. Once the Fed transitions to yield curve control, the quantitative purchase target becomes somewhat meaningless. This has been the experience of the Bank of Japan which, after implementing yield curve control, continued to have a purchase target of 80 trillion yen per annum. But in reality, it has bought much less, totaling just 18 trillion yen in the past year.

Yield curve control could prove an interesting tool to limit money supply growth while keeping interest rates low in the event of a sudden surge of inflation.

Negative Interest Rates: The fourth option—and now we are getting into the land of more remote possibilities—is a negative interest rate policy (NIRP). Fed Chairman Jay Powell has gone out of his way to dispel any notion that negative interest rates are under consideration, but the one thing he does not do is affirmatively close the door to using them. He raises doubts about their efficacy and says they would not be appropriate in the U.S. economy. NIRP could also wreak havoc with the banking sector and money market funds. Nevertheless, if all other tools fail up to this point, negative interest rates have to be left on the table.

The Fed and virtually everybody else in the market thinks that negative interest rates are something that will be decided by the Fed, but it’s not like the Fed provides a permit in order to allow bonds to trade at negative yields. The reality is that the market can do it. In Europe the ECB policy rate is -50 basis points and German bunds have traded below -80basis points, meaning the bund yield curve has been inverted. Even if the Fed keeps the fed funds rate trading at 5 basis points, the bund relationship shows that the U.S. Treasury yield curve could invert and trade at negative rates.

Negative market rates can happen in the U.S., and most likely will happen at some point. The only question is whether the Fed endorses a negative interest rate policy. The central bankers would be loath to do it, but they cannot rule it out if the market forces their hand and other policy tools prove inadequate.

Equity Purchases: And then there are what I’ll call the more exotic destinations on the Fed’s roadmap. Equity market purchases might not necessarily follow negative interest rates, but they might come instead of NIRP if it is just too unpalatable. Either of these two policies would be highly politically charged.

There is a strong correlation between stock prices and corporate credit spreads. If stock prices were to begin to slide, this would mean that corporate credit spreads could widen. If that began to happen in a disorderly manner, the Fed would become more actively involved in purchasing corporate bonds. Ultimately the scale of the bond-buying program would probably not be large enough to contain a dramatic spread widening of the type that would come about from a slide in stocks of 30 percent or more.

Equities and Credit Spreads Are Highly Correlated

Source: Guggenheim Investments, Bloomberg. Data as of 6.5.2020.

If the Fed needs to tame a severe credit crisis, it will have to find a way to prop up stocks and thereby maintain access to capital in a market other than the bond market. The Federal Reserve charter does not allow for the purchase of stocks, but the U.S. Treasury could establish a special purpose vehicle to buy stocks that the Federal Reserve could fund. That artifice would be similar to that which is used for the purchase of corporate bonds and ETFs. If credit spreads should start to widen significantly again, perhaps if we see a second spike in COVID activity as the lockdowns are unwound, the Fed would not rule out a program to prop up equity prices and provide financing to the Treasury to do it.

Break the Glass: As long as we are looking at the possible roadmap for the Fed, we cannot avoid discussing one other tool. Central banks around the world, including the Fed, hold almost 35 thousand tonnes of gold reserves. A central bank owns gold to buttress its reserves with an asset that becomes increasingly valuable in a severe crisis. There are no signs the world is questioning the value of the U.S. dollar, but it is clear that it has been slowly losing market share as the world’s reserve currency. With the Fed going all-in on financing the government deficit, the U.S. dollar could be at risk to negative speculation of its status as the dominant global reserve currency. Investing in gold may help offset this trend. The accumulation of gold as a reserve asset historically has been seen as a responsible policy response in periods of crisis. This may very well become the policy option of choice in the future.

Shifting Market Share of Global FX Reserves

Currency Composition of Official Foreign Exchange Reserves (COFER)

Source: Guggenheim Investments, Haver. Data as of 12.31.2019.

A decade ago, I spoke about unorthodox monetary policies such as QE and forward guidance. Today, these have become acceptable and permanent policy tools of the Fed. To conceive that these policies are now considered sound monetary orthodoxy would have been practically unthinkable. Fast-forward a decade into the future and I foresee that we may be shocked at what is considered sound central bank policy.

Important Notices and Disclosures

One basis point is equal to 0.01%.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Investing involves risk, including the possible loss of principal.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

©2020, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.