Want to read more by Nasdaq Dorsey Wright? Visit their Featured Firm page here

As everyone in the financial services industry knows, the US equity market is open from 9:30 am – 4:00 pm EST. However, the US market now also has pre- and post-market trading from 7:00 am until open and from close until 8:00 pm. Meanwhile, equity index futures trade almost 24 hours per day from Sunday evening through Friday evening. Therefore, between pre- and post-market trading and futures, there are significantly more outside-of-market hours during which equities and equities derivatives trade than there are normal market hours.

During a recent afternoon market rally, a CNBC commentator joked that perhaps the market was trying to front-run the daily 1% futures move as futures had gained about 1% overnight during a few consecutive times during that week and the major indices had consequently opened about 1% above their prior close. By-and-large your average investor doesn’t do much buying or selling outside of normal market hours, nor do they invest in futures. This means that, for the most part, these investors simply “take” the portion of the market return that is generated outside of market hours. This made us wonder – how much of the market return is driven by trading that takes place outside of normal hours? If there are more total hours of trading when the market is closed than when it’s open, could the out-of-market-hours trading account for more of the market’s return than the hours the market is open? If we didn’t have to worry about taxes or transaction or costs would we theoretically be better off not leaving exposure open during the off-market hours?

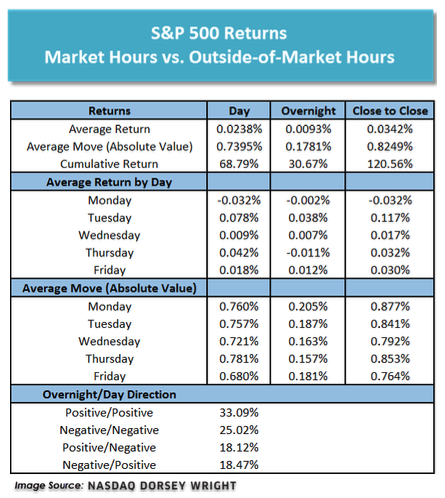

To answer these questions, we compared the returns of the S&P 500 Index (SPX) from 1/7/2008-6/17/2020 and segregated the returns from market close to market open the next day and the returns from market open to market close on the same day. We examined the time period since 2008 because although S&P futures started trading in 1982, the S&P price history on FactSet does not display a separate opening value before the beginning of 2008 and while other price sources do have opening values prior to this time, the differences between the opening values and closing values were negligible. The results of our study can be seen below. The figures labeled “Day” show the S&P’s return from open to close (Close Value/Open Value-1); the “Overnight” figures show the returns from the prior close to the open (Open Value/Prior Close Value-1). Overnight returns are grouped with the day of the opening value, i.e., the returns from Thursday close through Friday open are classified as “Friday” and Friday close through Monday open would fall under “Monday,” etc.

As you can see, both in terms of the simple average and the average absolute size of daily changes, regular market hours still account for most of the S&P 500’s return. The average return during market hours was about 0.024%, while the average return from close to open was just under 0.01%. We can see that since 2008, this resulted in a cumulative return of 68.79% generated during normal market hours, which is more than twice the 30.67% return attributable to the hours between close and open and gives a cumulative price return of 120.56% for the S&P 500. So, while regular market hours account for the bulk of the return, we clearly would have been worse off had we not held positions overnight. Prior to looking at the data, we speculated that we might see an outsized overnight move from Friday close to Monday open (labeled as Monday), as there is more time for market-moving news to break. However, while the absolute move was slightly larger than the other days it wasn’t dramatically so. The overnight move Friday (Thursday close – Friday open) was the largest of the overnight changes while Friday had the smallest change during market hours, which may be explained by traders closing out positions after Thursday’s close before taking a long weekend. Finally, in the bottom section of the table, we can see that the direction of overnight trading has been a fairly good predictor of the direction of trading during market hours – with the change overnight and the change during market hours was either both positive or both negative about 68% of the time. You may notice that these four percentages only add up to about 94% and the reason for this is that there were about 160 occurrences out of slightly more than 3,100 observations when there was no change from the close to the next session’s open.

Over the last 30 years, the amount of equity trading done electronically has increased significantly, which has allowed trading hours to be extended to the point that there are now more pre- and post-market trading hours than there are hours when the exchanges are officially open. However, as we’ve seen the majority of the market movement still takes place during the core market hours.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

Unless otherwise stated, the performance information included in this article does not include all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.