Review the latest Weekly Headings from CIO Larry Adam.

Key Takeaways

- US Economic Recovery Has ‘Many Miles To Go’

- Not All Sectors Of Spending Are On The ‘Right Route’ Just Yet

- Specific Counties May Need To ‘Hit The Breaks’ On Reopening

Tomorrow is the summer solstice, the longest day of the year and the official start to summer! For those who are still fortunate enough to travel with friends and family this year, the trip may look a little different than usual given ongoing restrictions and social distancing guidelines still in effect. Many travelers are planning to replace their flights with road trips, and I bet most are bound to hear the infamous words “Are We There Yet?” from their travel companions. Oddly enough, these are the same words we have been asked regarding when the US economy will fully recover the recent economic contraction. Given the recent rally in the equity market that temporarily got the S&P 500 back into positive territory last week, it is hard not to hope for the same sharp rebound in the economy. But the economy is not the equity market and we believe there are still ‘many miles to go,’ likely not until after next summer, for the economy to return to its pre-COVID-19 growth levels.

-

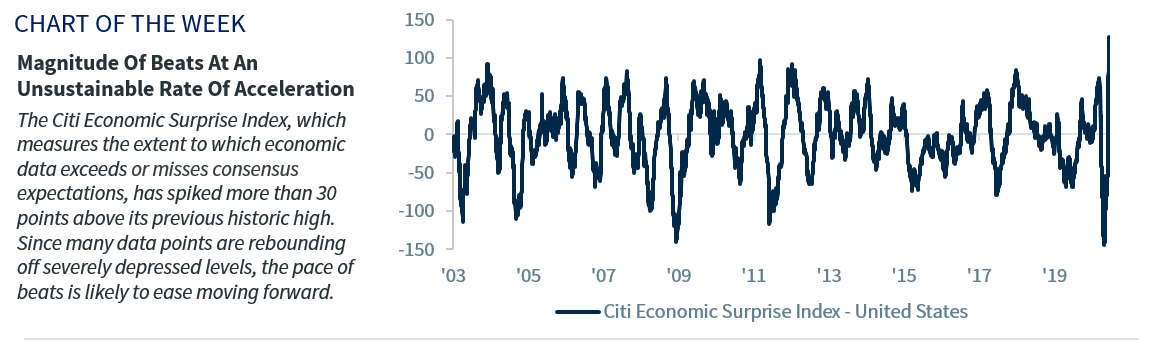

US Economy Turns The Corner | Optimism surrounding the eventual US economic rebound has led to the recent market rally. As we’ve mentioned in prior publications, real-time activity metrics signaled that the ‘bottom’ likely occurred in April and that the recovery process started in May. Since then, economic data points have not only confirmed but have significantly exceeded the consensus expectations of the bounce back in activity. In fact, the Citi Economic Surprise Index, which measures the extent to which data is coming in versus expectations, spiked ~30 points above its previous record high in 2011. However, it is important to realize that this rate of acceleration from the bottom and the magnitude of beats is likely not sustainable, it is more of a reflection of a quicker than expected bounce off of severely depressed levels. Due to the suddenness and rigidness of the shutdowns, the full recovery from the significant virus-induced decline in economic activity (~12%) is not likely to arrive until the end of 2021.

- Labor Market – Some May Need Roadside Assistance | The recent jobs report (June 5) delivered a shock to the financial markets as it reported the US economy gained just over 2.5 million jobs rather than losing the expected 8 million. However, this single jobs report needs to be put in perspective, as it alone does not erase the 45.7 million unemployment claims that have been filed since mid-March. With the gradual reopening of the economy, we hope these workers will be rehired once their employers reopen their doors, but some may still need assistance over the near term. The additional unemployment benefit is set to expire at the end of July, and all eyes are on Congress as it continues to negotiate an extension of these benefits or a possible return to work bonus. While employment conditions are expected to slowly improve, the unemployment rate will likely not return to the pre-COVID levels for years, ending this year near 9%, more than double the beginning of the year.

- Consumer Spending – Coming Round The Mountain | This week, May retail sales more than doubled the consensus estimate of 8.1%, growing 17.7% MoM. However, on a YOY basis they remain down 6.1%. While spending is likely to rebound (especially on-line sales), it will probably take us well into next year to fully recover consumer spending. Consumer confidence, a harbinger of future spending, remains near multi-year lows and the percentage of people who expect to see an increase in income over the next six months declined to the lowest level since 2013. This uncertainty is evident in ‘big ticket items’ such as motor vehicles as sales are down 30% YoY and unlikely to rebound to pre-COVID levels until the unemployment rate meaningfully falls.