Q2 2020 Fixed Income Survey: The Quarter of Quarters. a COVID-19 Special.

Want to read more by Russell Investments? Visit their Featured Firm page here

In this latest survey, 68 leading bond and currency managers considered valuations, expectations and outlooks for the coming months.

In our February survey, which now seems like a lifetime ago, managers recognized some positive market developments despite the backdrop of a slowing global economy: improving Sino/U.S. trade relations, moderating Brexit uncertainties and an end to impeachment proceedings against U.S. President Trump (in his favor).

At the time however, managers were concerned about potential geopolitical risks and whether markets perhaps relied too much on the Federal Reserve (the Fed) and its mid-cycle adjustment of last year to prop markets.

What a difference a quarter makes. In January, a dangerous conflict between the U.S. and Iran was overshadowed by the coronavirus pandemic. Governments across the globe decided to enforce lockdowns, which immediately impacted livelihoods and national economies. In a concerted effort, central banks, alongside respective governments, have been unleashing unprecedented levels of stimulus measures as a direct response. Oil prices also slumped, owing to a price war between Russia and Saudi Arabia.

In spite of the painful economic fallout, the severe risk-off market environment in the first quarter largely reversed in April and May. There seems to be a divergence in economic and financial market performance. The concerted support of monetary policy and an opening of the fiscal taps has driven a rapid recovery in credit spreads, even with corroding credit fundamentals. The market has also latched onto positive news regarding potential vaccines and treatments for COVID-19, which have improved sentiment among investors.

We therefore ask, will we see a swift recovery from the first-half economic downturn to market conditions as of December 2019? Are inflation expectations still largely muted? Has the wrath of the coronavirus truly passed?

How steady are the markets?

Views from interest rate managers

- The consensus view from managers is that the Fed will not move interest rates into negative territory. 74% of managers don't expect the next rate hike before 2023. This was effectively confirmed in the latest Fed news conference, where Chairman Jerome Powell stated that rates would remain in the current levels until at least the end of 2022.

- 70% of managers expect the Fed to engage with yield curve control, starting as soon as the second quarter of 2020. 50% of them expect yield curve control for at least three years.

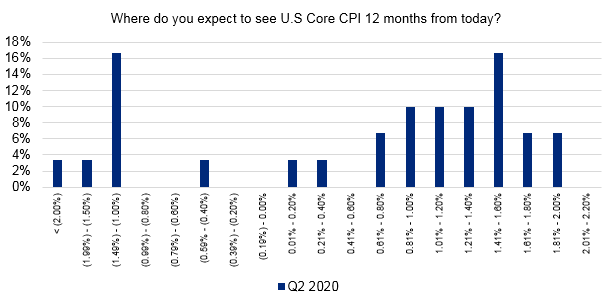

- With little consensus, the weighted average for the core consumer price index (CPI) in the U.S. stands at 0.53% for the next 12-months—the lowest level since we started the survey. In addition, for the first time since we started the survey, 27% of managers expect to see a disinflationary U.S. economy in the next 12 months.

- It is clear that participants believe that the Fed must continue to support markets but are unclear whether there will be ramifications for inflation, with deflationary forces seeming to be the focus, although a minority of respondents are looking toward inflation.

Views from investment-grade (IG) credit managers (generally bullish)

- 73% of managers expect spreads to tighten in the next 12 months—the highest rate since we started the survey. We already saw most of this rally over the course of April and May. In terms of regional preference, most of the managers favor the U.S. followed by Europe (excluding the UK). In regard to sectors, financials and non-cyclical industrials are expected to post the best returns over the next year.

- 87% of managers expect leverage of lower quality U.S. IG to increase—also the highest rate since we started the survey.

- When asked about energy allocation, considering recent tumultuous oil prices, 45% of managers seem to be comfortable with maintaining risk exposures in this sector. If considering any changes to exposure, the focus is on the credit quality of the names and their liquidity levels.

Global leveraged credit (generally bullish)

- 70% of managers expect tighter spreads over the next 12 months—the highest amount since the start of the survey. The risk-on environment in April and May already gave rise to a meaningful rally.

- In regard to corporate fundamentals (leverage, interest coverage, cash flows), 100% of respondents consider they will deteriorate in the short term. This is also the highest amount since the beginning of the survey.

- 64% of managers believe that U.S. high-yield bonds should deliver the best risk-adjusted return in the next 12 months.

- The main risk concern for managers is the slowdown in global growth. Energy, retail and auto are the areas where managers consider credit risk not to be correctly priced in.

Risk across the globe

Europe and UK

- Regarding sovereign bond yields, 70% of respondents expect periphery spreads vs. German bunds to tighten over the next 12 months.

- 75% of managers expect the euro to be in the wide 0.96 to 1.10 range. In the last survey, 50% of managers expected the euro to move in the 1.06 to 1.10 range. Since these results, the euro has strengthened on the back of more unified European Union stimulus plans.

- About 60% of managers expect the British pound (GBP) in the 1.16 to 1.25 range in the next 12 months. This range is lower than in the previous survey as Brexit uncertainties began to rise again. However, reports that the UK government might be willing to make some important compromises to reach a final Brexit deal paved the way for a higher GBP.

Emerging markets (EM)

- 100% of the managers expect spreads in the hard currency emerging market debt (HC EMD) index to tighten in the next 12 months, the most bullish stance since the survey started. Spreads for the EMBI Global Diversified have retraced approximately 60% from the peak registered on March 23.

- In the HC EMD space, managers expressed their preference for Ukraine and Mexico as the countries with the highest expected return, followed by Indonesia and Brazil. China and the Philippines are the top two underweight countries. Default expectations remain low for EM countries where managers expect less than 10 countries to default in the next 12 months. The most concerning point among managers is unexpected changes in Fed policy.

- While 75% of the managers consider HC EMD to offer the most compelling opportunities over the next year, they still favoured local currency EMD (LC EMD) in the long term.

- 32% of LC EMD managers expect foreign exchange (FX) to be a detractor in the next 12 months—the highest number since we started the survey. Only in November 2016 did managers express such a negative view on FX.

- Managers' expectations about return for the J.P. Morgan Global Bond Index-Emerging Markets Global Diversified over the next 12 months stands at about 5.5%.

- In the LC EMD space, managers expressed their preference for the Russian ruble as the most attractive currency in the next 12 months, followed by the Mexican peso. They consider that the Turkish lira will post the worst performance during this period.

Securitized sectors under COVID-19 conditions

Securitized credit suffered some of the most significant spread widening in fixed income markets during the market turmoil in March. The market faced technical pressures from levered players like hybrid mortgage REITs and hedge funds, as well as significant fundamental challenges from broad economic concerns and social distancing.

On the fundamental side, unemployment concerns and high levels of borrowers entering forbearance challenged residential real estate markets. Meanwhile, business closures from social distancing initiatives, particularly in the retail and lodging segments, hurt commercial real estate markets. These markets were also less supported by government stimulus programs. Hence, spreads have remained wide and the segment has been slow to recover.

As a result, the relative value of securitized credit looks attractive compared to corporate credit and other risk assets. These markets are seeing fundamental green shoots, with housing data coming in stronger than expected, employment showing signs of improvement and local economies reopening around the nation. Should the U.S. economy continue to progress in reopening and recovering from COVID-19, securitized credit looks attractive relative to other risk assets at this point.

- 50% of managers expressed that they will be adding risk in their return-oriented securitized portfolios in the next 12 months—the highest amount since the start of the survey.

- When asked about taking a meaningful beta position, 50% of managers expressed already having a long position in their respective portfolios, whilst 36% of them expect to add a short position.

- Regarding long/short positions on CMBX.6.BBB-1, 73% of managers would take a long position (sell protection) and 27% would take a short position (buy protection).

Conclusion

Our interest rate managers have clearly indicated that they believe monetary support will be substantial and prolonged, in spite of the extraordinary budget deficits expected over the coming years, driven by the large expansion of fiscal spending. On balance, the credit specialists are expecting this will drive tighter credit spreads, even in the face of weaker fundamentals and higher degrees of leverage.

It is clear that spread markets continue to be addicted to policy support and policy makers are obliging. Yet this policy support has been extraordinary, and we have yet to learn what longer term consequences we will face from such changes. There are signs in the survey that some managers wonder about the chances of inflation, which seems like a remote possibility in the depths of one of the worst recessions on record.

Managers' top concern currently was the speed of the recovery. 46% of managers expect the global economy to revert to December 2019 levels by the second half of 2021, while 43% believe it will not revert before 2022.

The key question remains: What is the level of sustainable growth an economy can deliver when it is dependent on monetary stimulus? With more sovereign and corporate leverage needed for each unit of real GDP (gross domestic product) growth, productivity is deteriorating. While it is clear that policy is forcing a recovery in credit assets, the quality of the cash flows supporting those assets are deteriorating in the face of weaker productivity and structurally higher leverage. Given that risk-free assets offer no real returns, options for investors are becoming higher stakes.

1 The CMBX are indices that track the prices of a basket of tranches (e.g. BBB-) in commercial rather than residential mortgage-backed securities.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Indexes are unmanaged and cannot be invested in directly.

The J.P. Morgan Government Bond Index-Emerging Markets Global Diversified Index is one of a series of comprehensive emerging market debt benchmarks that track local currency bonds issued by emerging market governments.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2020. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-11692