Want to read more by Nasdaq Dorsey Wright? Visit their Featured Firm page here

Over the years, we have illustrated the value of relative strength-based sector rotation in a variety of ways. Most of these studies have treated the sectors generically, i.e., they looked at the performance of the best performing sector without regard to which sector that happened to be at any given time. The sectors, however, are not homogenous. Some, like utilities and consumer staples, are viewed as defensive and, on a relative basis, often perform better when the market or the economy is weak. On the other hand, offensive sectors, like consumer discretionary, often exhibit superior relative strength when the overall market is strong. As a result, when offensive sectors are strongest on a relative strength basis, we might expect that their absolute performance would be better than that of defensive sectors, which tend to be relatively healthy when the overall market is weaker.

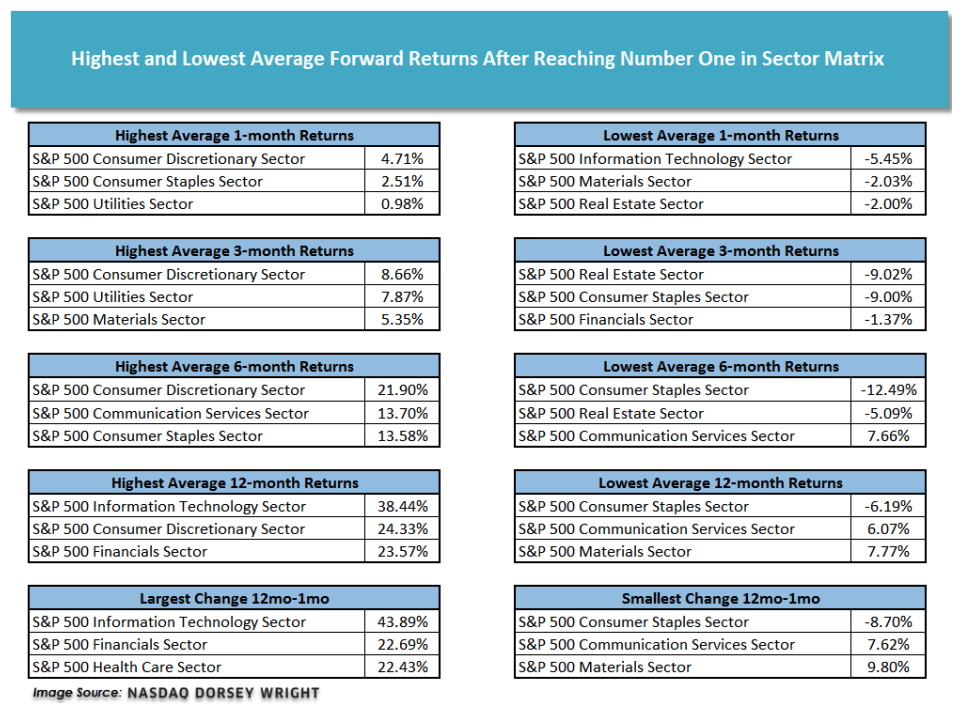

The table below shows the average total return performance for each sector after it has reached the top of a matrix that ranks S&P sector indices by relative strength. Each of the sectors reached number one in the matrix at least twice (includes backtested data of indexes that are not available for direct investment going back to 1996).

For the most part, the actual returns are in line with what we expected – the sectors with the best absolute performance were ones typically regarded as offensive or growth-oriented sectors. To be clear, this did not happen in every single period we examined, these were averages of performance over periods examined from multiple market cycles. In contrast, the lower absolute performances came from sectors we tend to think of as more defensive. Below we've broken out the highest and lowest average returns for each period examined.

A few observations:

- Every sector, except consumer staples, has positive average returns 12 months after reaching number one

- Consumer discretionary has the best one-, three-, and six-month forward returns after it reaches the top spot.

- At -5.45%, technology has the worst 1-month average return after being ranked number one. However, it also has the best 12-month average return at 38.44%.

- The consumer staples sector has the second-best one-month average at 2.51% but has the worst 12-month average at -6.19%.

- The industrials sector has reached the top spot the fewest times, occurring only twice.

- Utilities, technology, and financials have each reached the number one spot six times.

- Consumer discretionary was the only sector to generate an average six-month return greater than 20%

- Technology, consumer discretionary, healthcare, and financials each posted average gains of more than 20% one year after reaching number one.

Our previous studies have shown that owning the strongest sector can have tremendous performance benefits on a relative basis. The data we have examined today adds some useful context to that and demonstrates that there is relatively wide dispersion in absolute performance depending on which specific sector exhibits the highest relative strength.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The performance numbers within this article reflect dividends but do not reflect the potential transaction costs associated with investing in a particular market sector. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.