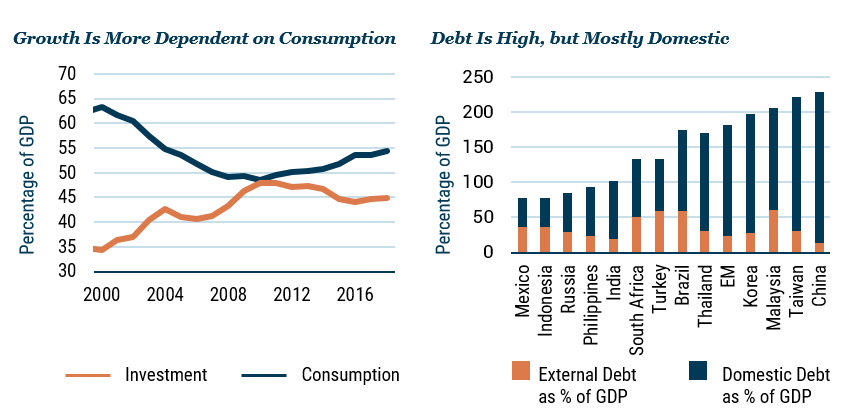

Five Reasons EM Are More Resilient Than in the Past

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Executive Summary

This paper highlights five reasons why Emerging Markets (EM) in aggregate are more resilient today than in prior periods. A “healthier” index composition in addition to four other reasons support our analysis that EM drawdowns will be significantly more muted than previous peak- to-trough drawdowns. The 30% rebound that the asset class has experienced since its trough in late March is in line with our thesis of a more robust index. In GMO’s recent Quarterly Letter, Ben Inker, Head of our Asset Allocation team, made the case for emerging stocks given their lower relative valuations.

We acknowledge the heterogeneity of the asset class but take comfort in China at 40% of the MSCI EM Index being resilient, with better growth prospects and plenty of residual dry powder. Not only has the weight of cyclical sectors like Energy and Materials shrunk (from 30% to 12%), there has also been a significant improvement in their balance sheets. Some domestic consumer-driven and growing sectors such as Information Technology and Internet/Media names are now nearly one-third of the index. In our April 2020 paper, “Covid-19: Risk and Resilience in Emerging Markets,” we provided a framework to assess the most vulnerable EM nations and those best placed to emerge less scathed than others from the pandemic. We identified only 9% of emerging countries as high risk vs. 66% as safe countries.

However, the EM asset class is innately characterized by risk – this paper discusses five such risks and cautions of other uncertainties that can morph into risk. While some traditional risks have abated, we discuss tensions from a renewed U.S.-China trade war, domestic power struggles in some of the larger EM countries like Brazil and India, constraints on the coffers of EM governments, and both currency and concentration risk. As we construct our EM portfolios today, we strive to take advantage of the lower volatility of the asset class while maintaining a defensive stance to mitigate the heightened risks in today’s environment. Net/net, however, we believe many of the EM-specific risks are navigable.

EM Performance Through Previous Crises

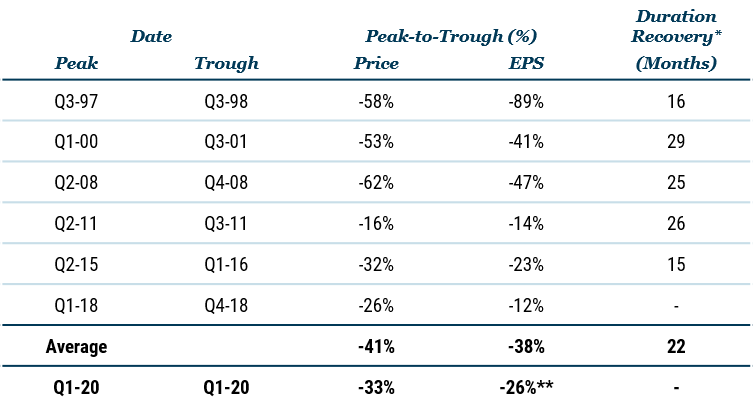

Table 1 highlights peak-to-trough drawdowns in previous periods of market uncertainty and the time taken to recover. Despite the impact of the current crisis on GDP likely being the worst in decades, EM fell peak-to-trough by 33%. This time, however, not only is the drawdown lower, but the recovery has been faster than in previous crises – a 30% rebound from the trough in less than 3 months.

TABLE 1: EM HISTORICAL PRICE AND EPS DRAWDOWNS

As of 5/31/2020 | Source: Bloomberg, GMO

* Months it took prices to return to previous peak from the trough

** Change in NTM earning estimates from peak

We believe there are five reasons that explain this less painful drawdown and suggest why “this time is different.”

#1: THE WEIGHT OF VULNERABLE COUNTRIES IN THE MSCI EM INDEX HAS BEEN SIGNIFICANTLY REDUCED

At approximately 40% of the index today, China has displaced the weights of vulnerable economies in the EM index. We identify “vulnerable” economies as those that are highly dependent on foreign savings and, therefore, more exposed to external outflows. In 2012, over 30% of the index was made up of 9 vulnerable economies including countries like Brazil, Turkey, and South Africa. Today, the impact of these vulnerable countries has waned because the weight of China has increased and macroeconomic fundamentals in some of these countries have improved.

Exhibit 1 shows the index weights of these vulnerable countries and China across time. The dominance of the “vulnerable” country bucket has historically led to higher volatility and risk contagion across EM.

EXHIBIT 1: VULNERABLE* ECONOMIES DISPLACED BY CHINA IN THE MSCI EM INDEX

![]()

As of 5/31/2020 | Source: Bloomberg, GMO

* Vulnerable economies are defined as countries with poor external balances and reliant on foreign savings. Vulnerable countries are South Africa, Chile, Colombia, Argentina, Egypt, and Pakistan.

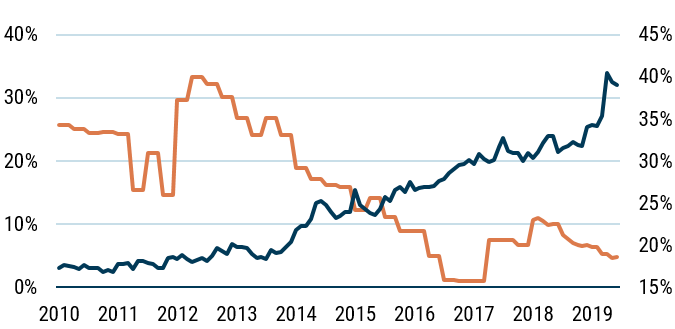

#2: CHINA, WHICH CONSTITUTES 40% OF THE MSCI EM INDEX, IS SAFER AND STILL HAS DRY POWDER FOR STIMULUS

Despite commonly predicted China hard-landing scenarios, we are less worried than most analysts. For the last three decades, China has shown that it has the fiscal and monetary wherewithal to rebound from temporary economic setbacks. In the last few years, China has transformed itself from an externally dependent economy to one in which the domestic consumer has begun to pick up much of the responsibility for stimulating the economy (see Exhibit 2). To contextualize China's growth with some numbers, let's look at the China Internet sector. At $1.4 trillion market cap, today the China Internet sector alone accounts for nearly half the EM aggregate market cap of a decade ago. Today, China's Internet sector is 17% of the MSCI EM Index while the BRICs countries (ex-China) are only 20% of the index.

EXHIBIT 2: CHINA’S TRANSFORMATION FROM EXTERNALLY DEPENDENT TO DOMESTIC CONSUMPTION DRIVEN

As of 12/31/2019 | Source: BIS, CEIC, Bloomberg, GMO

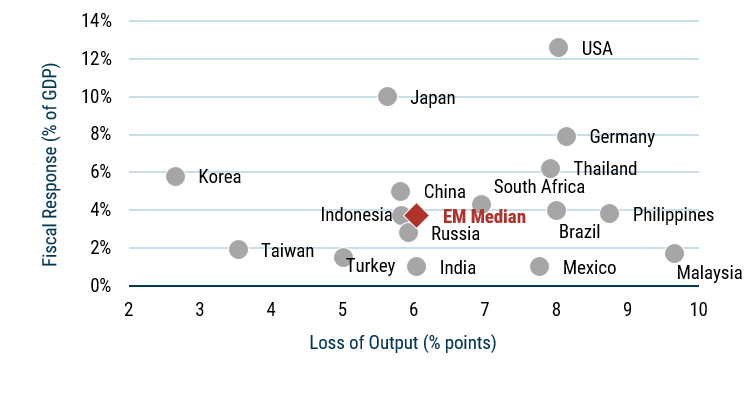

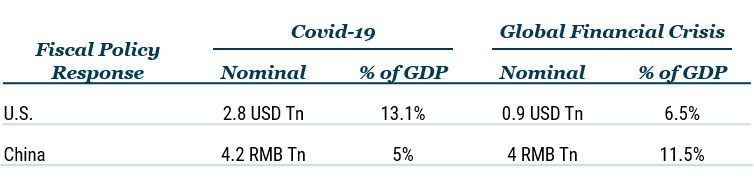

We should not mistake the lack of China’s headline-grabbing stimulus plans to date as a signal of the State’s reluctance to use its resources. Exhibit 3 and Table 2 show that China still has the fiscal might to bail out its businesses and enterprise should it be necessary. It is likely, though, that a future stimulus will fall well short of the whopping 4 trillion RMB (>10% GDP) China announced during the GFC – a sum adequate to offer a lease not only to China, but also to much of the rest of the world. To date, China has spent only 5% of its GDP on fiscal stimulus compared to 11.5% spent during the GFC. For comparison, the U.S. has spent 13% of its GDP to date in response to Covid-19 compared to 6.5% spent during the GFC.

EXHIBIT 3: CHINA HAS PLENTY OF DRY POWDER TO INCREASE STIMULUS

As of 5/31/2020 | Source: CEIC, GMO

TABLE 2: CHINA HAS PLENTY OF DRY POWDER TO INCREASE STIMULUS

As of 5/31/2020 | Source: NDR, GMO

#3: SECTOR COMPOSITION HAS MOVED FROM CYCLICAL SECTORS TO INFORMATION TECHNOLOGY AND CONSUMER SECTORS

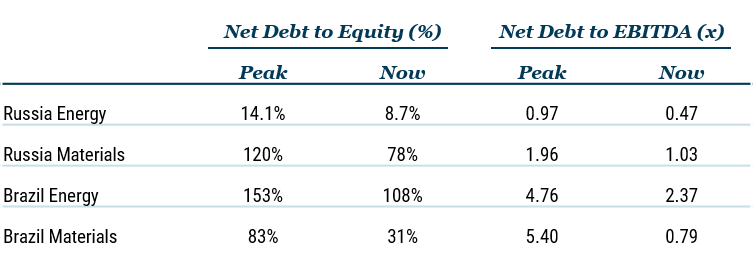

In 2010, 30% of the index was in cyclical sectors such as Energy and Materials. Today, the weight of these sectors has dropped to less than 15% with significant improvement in balance sheets. Table 3 highlights the improvement in balance sheets over the last decade of the four traditionally levered country sector groups in Russia and Brazil.

TABLE 3: SIGNIFICANT DELEVERAGING IN LARGE CYCLICAL COUNTRY SECTORS

As of 12/31/2019 | Source: Bloomberg, GMO

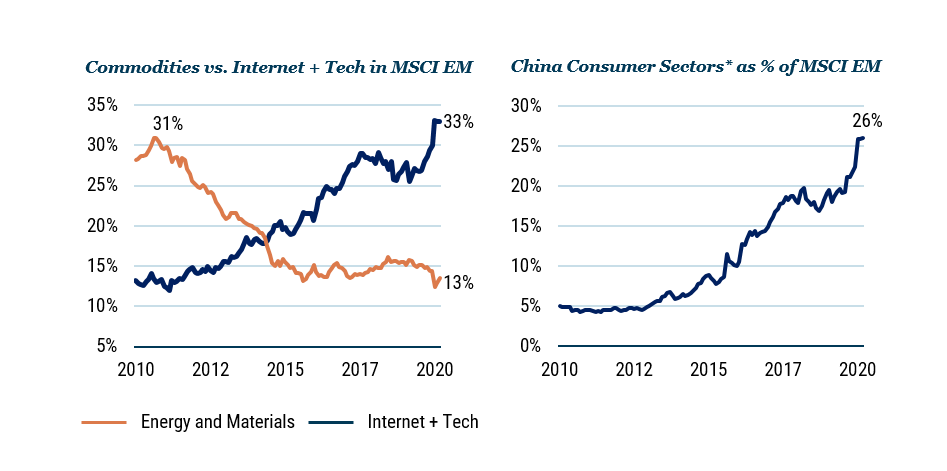

At the same time, as Exhibit 4 shows, the weight of Internet and Technology has steadily increased over the last decade and today accounts for one-third of the index.

EXHIBIT 4: FROM CYCLICAL TO TECH/CONSUMER SECTORS

As of 5/31/20 | Source: Bloomberg, GMO

* China consumer sectors include Discretionary, Staples, IT, Healthcare, Insurance, Media and Entertainment.

#4: WHILE FINANCIALS REMAIN A SIGNIFICANT CONSTITUENT OF THE INDEX, THEIR “QUALITY” HAS IMPROVED WITH CHINA FINANCIALS ACCOUNTING FOR 36% OF THE FINANCIALS INDEX

With a market cap above USD 5.0 trillion and total assets of USD 67 trillion, Financials comprise the largest sector in the MSCI EM Index. Given the leverage endemic to these banks, it is critical to understand the innate risks of this group to better assess the asset class. While Financials have historically made up about a quarter of the index, their composition has changed over time as shown in Exhibit 5. One key change has been that the weight of banks in the “vulnerable” country group as described previously has reduced from 46% to 10% of MSCI EM Financials.

EXHIBIT 5: COMPOSITION OF MSCI EM FINANCIALS INDEX

As of 5/31/2020 | Source: Bloomberg, GMO

As of May 31, 2020, Chinese banks accounted for 36% of the Financials sector weight. We believe these banks are significantly less risky due to our more favorable macro-assessment of China as discussed above in addition to a number of other reasons (per UOB Kay Hian):

- The provision coverage ratio of these banks is 183.2% versus E.U. banks’ range of 50-60%; the provisions/pre-provision operating profit (PPOP) is high at 30-60% because Chinese banks started implementing IFRS9 in 2018 (most U.S. and E.U. banks have delayed IFRS9).

- The Capital Adequacy Ratio is 14.53% (Basel Accords requirement is 10.5%); CET1 is 11.94% (Basel Accords requirement is 7.5%).

- Chinese banks own 70% of all bonds; in turn, bonds represent 25% of total banking assets, thus Chinese banks inject liquidity into buying bonds without PBOC getting involved. (For contrast, in the U.S. the Fed currently mops up

every type of bond such as municipal, high yield, or money market to help asset prices recover.) - Chinese banks underwent a shadow banking crackdown from 4Q 2016-4Q 2018, with banking asset growth dropping from +17% to +6%, and thus have room to resume growth without risking the return of shadow banking.

- Chinese banks offer dividend yields of 5-6%, payout ratios of 30%, and they are not cutting dividends; retained earnings growth was strong in 1Q 2020,

averaging 6-10%.

While there is an argument that banking systems across a broad set of geographies inherently represent some stress, we believe this is a diversified group and dominance of the Chinese banks mitigates much of this risk.

#5: ABILITY TO RESPOND TO COVID-19 AND HIGHER GROWTH PROSPECTS

In our April paper,1 we argued that the EM asset class is more resilient to the impacts of Covid-19 given the composition of the index today. Using several factors, we gave each country a Covid-19 “Risk Score” as well as a ranking for its “Ability to Respond” and rebound from the current crisis. Per Exhibit 6, our analysis revealed that today only 9% of EM countries are in the high-risk category.

EXHIBIT 6: IMPROVED INDEX COMPOSITION RESULTED IN BEING MORE RESILIENT TO COVID-19

Significant Divergence among EM Countries' Ability to Recover from Covid-19

As of 5/31/2020 | Source: GMO

Percentages in parentheses are country weights in the MSCI EM Index.

The conclusions from this analysis lead us to believe that the countries in the “Safe” cluster will withstand the crisis better while the recovery and reopening of the economies in the “Risky” cluster will be more challenging (see Exhibit 7).

EXHIBIT 7: 66% OF EM TO HAVE HIGHER GDP GROWTH THAN DEVELOPED MARKETS

- As of 5/31/2020 | Source: Bloomberg, GMO

EM: Born This Way (Certain Risks Will Always Remain!)

By virtue of a healthier index today, we believe certain innate risks that have previously characterized EM have dissipated. However, the asset class is inherently home to a number of unforecastable events that we must acknowledge.

- With great weight comes great responsibility (and magnified risk). With China comprising nearly 40%of the index, we need to be prepared for hitherto atypical risks such as the trade war with the U.S. returning to the forefront of political and economic rhetoric. In an election year for the U.S. – and in light of recent comments coming from the White House – it is likely that the trade war re-emerges with a net-net impact on the EM asset class (there will be both winners and losers within the asset class). However, China has had some time to prepare itself since 2018 and we believe it has both the fiscal and the monetary might to take on what the U.S. and other nations may throw its way (see, for example, Exhibits 2 and 3). We also believe “extreme” actions by either the U.S. or China are unlikely. Rather, political and economic attention will rightly be focused inward so as to get jobs, small enterprises, and other constituents most affected by Covid-19 on their feet again.

- Beyond China, several of the larger EM economies are also witnessing their own power struggles and rising nationalism. There is increasing evidence of this in India (with socio-religious issues in Kashmir), Brazil, and with the Beijing/Hong Kong dialogue gathering momentum. History has shown that in prior periods of economic distress, nuances of authoritarian regimes can also be seen. While in some cases, the political and religious risks have been tied to their respective lands for decades, in other cases, there are newer risks that can arise.

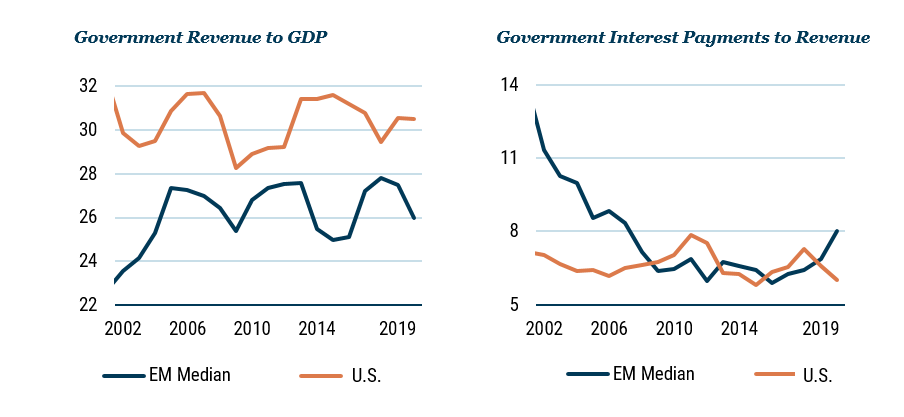

- Limited wallet size of EM governments. EM governments today have limited revenue streams with much higher borrowing costs (see Exhibit 8) and do not have the luxury of a reserve currency. The public coffers of EM are not as plentiful when compared to the U.S., for example. Many EM leaders find themselves more reliant on the kitty of the U.S. Fed and its willingness to continue to stimulate, irrespective of the knock-on effects such stimulus will have on trade and market sentiment. Brazil and India (combined 13.5% of MSCI EM Index) are expected to be running fiscal deficits of 13% and 11%, respectively (Central and State debt).

EXHIBIT 8: EM GOVERNMENTS HAVE LIMITED REVENUE STREAMS AND HIGHER BORROWING COSTS

As of 3/31/2020 | Source: CEIC, GMO

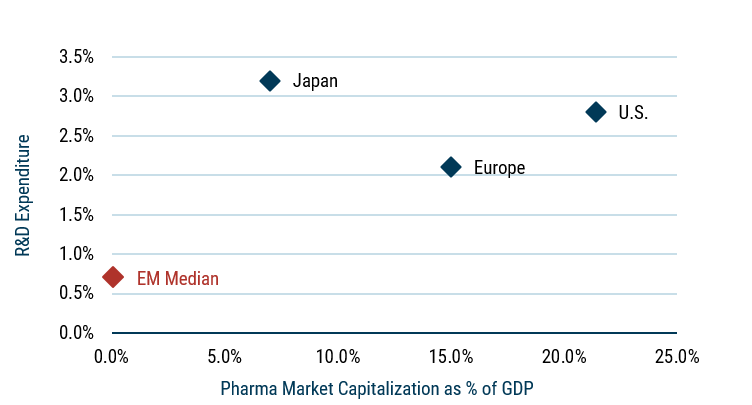

- Poor healthcare infrastructure and “trimming” of other essential services. It should come as no surprise that pharma companies, R&D, and the sheer number of beds and accident and emergency facilities in EM fall well below the standards of developed nations (see Exhibit 9). For example, while the U.S. and E.U. have 3 and 6 hospital beds per 1000 people, respectively, India has only 0.5 beds. Similarly, the E.U. (5x) and U.S. (3x) have more physicians per capita than India. Further, EM lack a social security net to offer fiscal support like income guarantees and small business grants as seen in Britain and the United States. With resources in EM countries being limited and finite, other areas like public education or security spending (as in the case of Thailand) may suffer. Some impacts may only become evident in the medium term.

EXHIBIT 9: EM HEALTHCARE — LIMITED RESOURCES AND LACK OF INNOVATION

As of 3/31/2020 | Source: Bloomberg, World Bank, GMO

- Higher currency risk. Unlike some of their developed counterparts, central banks in emerging countries will need to toe a fine line between managing investor sentiment, prompting capital flight, and currency depreciation. Typically, the U.S. dollar has a negative impact on EM. We take comfort in the fact that EM currencies are cheaper and the dollar has already appreciated over 30% in the last 9 years (per Bloomberg DXY Index). We see significant adjustments in current account deficits on the horizon after the currency depreciation witnessed this year. For example, Brazil, which has been the worst performing currency this year, is likely to see a current account surplus next year.

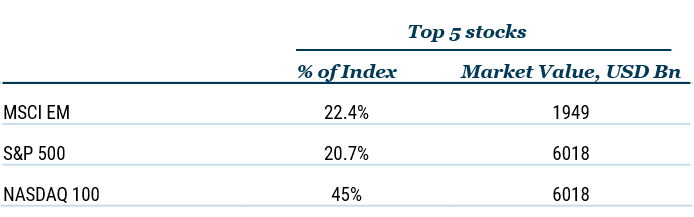

- Concentration and spill-over risks. Similar to the U.S., where the top 5 stocks represent 20% of the S&P 500, Table 4 shows the top 5 stocks in EM represent 22.5% of the MSCI EM Index. However, in EM this risk is mitigated by the companies having strong domestic franchises, high quality, and strong moats around them. (The average ROE in the last 5 years for these companies was 23%.) A large part of the EM earning stream is tied to businesses related to technology and the internet. There is therefore an ironic “symbiotic” relationship between the U.S. (S&P 500 and NASDAQ) and Chinese stock markets.

TABLE 4: CONCENTRATION RISK — TOP 5 STOCKS AS PERCENT OF INDEX

As of 5/31/2020 | Source: Bloomberg, GMO

Conclusion

The data clearly indicates that the quality of EM earnings has improved significantly, resulting in a more resilient asset class.

At 40% of the index, we believe China is resilient and capable of long-term growth and capital appreciation. The index is more stable in its composition as sectors like Information Technology and Consumer Discretionary have become “core” and the weights of more cyclical sectors have shrunk. While Financials account for nearly a quarter of the index, the majority are “safer” Chinese institutions that have demonstrated their ability to preserve capital. Based on our research, we characterize only 9% of emerging market countries as high-risk while a majority (66%) of the index is in the “safe” cluster. However, given our analysis of the risks within the asset class, it is evident that some nations are better placed to withstand the current crisis. Today, despite the risks, our dedicated EM portfolios reflect the improved resilience of the asset class.

Download article here.

1A. Bhartia, T. Tong, U. Tharar, “Covid-19: Risk and Resilience in Emerging Markets,” April 2020. This GMO white paper is available at www.gmo.com.

The views expressed are the views of Amit Bhartia, Mehak Dua, and Alvaro Pascual through the period ending July 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2020 by GMO LLC.All rights reserved.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits