“None of us has the luxury of choosing our challenges; fate and history provide them for us. Our job is to meet the tests we are presented. At the Fed, we are doing all we can to help shepherd the economy through this difficult time.” -Jerome Powell Chairman of the Federal Reserve

Before we begin our quarterly investment commentary, we are pleased to announce an expansion: Kurt Beimfohr, Jeff Vieth CFP, and Erica Berger will be joining our team. While our investment strategy will not change, the addition of these team members adds depth to our current capabilities, as well as helpful expertise in financial planning and fixed income management. Some of our long-time clients may recognize Kurt’s last name, as he is the son of Knightsbridge co-founder, Al Beimfohr. Thus, the addition of Kurt, who for years has been a successful financial executive in his own right, represents a special homecoming of sorts to the Knightsbridge family. His associate, Jeff, has the Certified Financial Planner designation, and will strengthen our offering in this area. The friendly new voice you may hear on the phone if you call our main line, will belong to Erica, who will be available to assist clients. Given our expanded services we are now doing business as Knightsbridge Wealth Management. To accommodate our larger team, in September we are moving across the street to 450 Newport Center Drive, Suite 630. We look forward to offering you deeper client service from our new location.

Imagine for a moment that you pick up your morning paper and read that your state government has established a new agency with the stated intent to spend one hundred million dollars a month buying duplexes all across the state. It just so happens you own several duplexes yourself, which you rent out to tenants for some extra income. Is this good news?

Well of course it is... you naturally expect the price of duplexes to go up! You had planned to sell one of your buildings for $200,000 to fund your living expenses... and immediately tell the interested party that your price is now $250,000. The buyer agrees.

Before long, the State Agency comes around and wants to buy one of your units for $300,000. You hadn’t intended to sell, but it seems like a good price, so you do so. But now you’re sitting on some extra cash. You’re an investor, so you want to put that extra money to work, buying another property you’ve had your eye on. You fix it up, sell it for more than you dreamed possible, but now can’t find any more reasonably priced duplexes to buy. They’re too darn expensive! You’ve always specialized in duplexes, but single-family home rentals and apartment buildings now look significantly cheaper versus the rents they generate. Thus, every time you sell a duplex, you buy a small apartment complex instead. In no time, prices for apartment buildings are rising as well, even though the State Agency has made no apartment purchases.1

Thinking through this vignette is one of the best ways to understand what is going on with the stock market. The Federal Reserve has come into town to buy a Trillion dollars’ worth of bonds2 (with money printed out of thin air) and, thus, the price of bonds has unsurprisingly skyrocketed. In July 2019 a 10-year Treasury Bond sold for 50 times the annual interest it produced. In July 2020 that same bond sells for 57 times its annual interest stream.

Just as a duplex is reasonably similar to an apartment building, a bond is reasonably similar to a stock. Thus, even though the Federal Reserve hasn’t been buying stocks, stock prices are going up anyway. Bond investors, flush with this cash, are bidding up stocks as soon as they sell their bonds to the Fed. Accordingly, in the second quarter, the S&P 500 rose 20 percent, its biggest quarterly gain since 1998.

It is said that a rising tide lifts all boats, and that goes for monetary tides as well (see cover image of this letter). Watching the market every day, this is exactly what it has felt like; stocks just want to go up... fundamentals be damned. On June 8th, the height of the Q2 market rebound, every single stock in the S&P 500 was up over the prior 10 weeks, an incredibly rare occurrence. To take a specific recent example, June 25th was the day that it became very clear that the U.S. was in a second COVID wave, as Texas halted its reopening. Stocks rose that day.

When you’re not sure what’s going to happen, often it is best to listen to the market. Thus, despite being bearish, when the tide started rising, we didn’t stand against it, but started to swim with it. It can feel crazy, but at some level it also makes sense depending on how you look at it. If you own a 10-year Treasury Bond, you are rewarded with a 0.6% annual yield. If you own the S&P 500, your dividend yield is 1.9%. In June, the gap between these measures was the largest in 30 years, meaning that by this measure, compared to Treasury Bonds, stocks were the cheapest they had been in 30 years (beyond even the March 2009 nadir of the Global Financial Crisis)3. In our story, apartment buildings are expensive compared to their old prices... but they still look very cheap compared to duplexes. In today’s markets, stocks are very expensive compared to the stocks of yesteryear, but they appear cheap relative to bonds.

Money printing is not only a reason stocks rose, but also a reason they did not fall further. It’s not so much that stocks fall during recessions because investors suddenly think they are worth so much less. Stocks fall because people need the money and they sell. Investors need to sell regardless of price to get cash. This time around, investors are flush with cash and no longer need to sell everything that isn’t tied down.

To summarize, the story of the market in the second quarter was the unmovable object of economic recession trying to withstand the unstoppable force of money printing. The unstoppable force emerged as the clear victor4.

Although, to be fair, the unmovable object was facing another foe besides money printing by the Fed: various stabilization programs run by the government. (While there are some connections, it is best to think of the government response separate from the Federal Reserve response discussed above.)

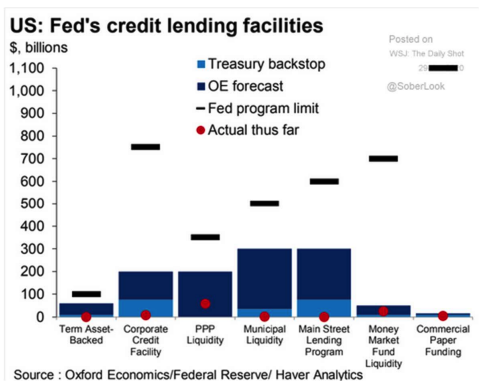

The unstoppable force of money printing won round one... but will it keep winning? The Fed indeed has the ammo to keep fighting. It recently committed to keeping interest rates at zero through 2022, and the chart at right shows it has printed and spent a fraction of that available through its programs (and they can always do more when their programs run dry).

In fact, with all the Fed has done (which will not be reversed soon, if ever), we expect stocks to emerge from this recession more expensive than when they went in (as they did after the Great Recession). Just like with our opening vignette, apartment prices would remain expensive long after the State Agency stopped buying duplexes. However, as everyone knows, we have not eliminated the virus. Maybe at some point the market will start to care?

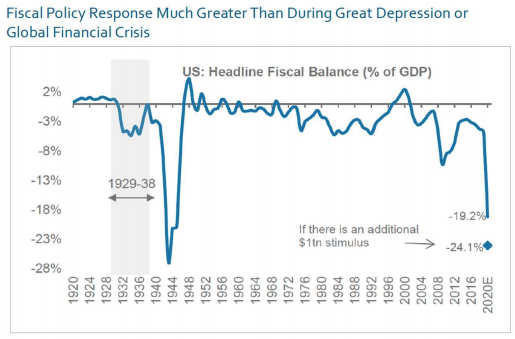

Last quarter we wrote about the economic devastation that the Coronavirus would wreak on our economy. That has happened. Second quarter earnings for the S&P 500 are forecasted to decline 44%. Unemployment, which was a historically low 3.5% before the pandemic, hit a staggering 16% in May, though it has since subsided to 11%. 11% is certainly better than 16%, but that’s still worse than the darkest days of the Great Recession. As bad as the economy has been, things would have been vastly worse without an incredibly robust government response. This response, which encompassed numerous programs, was the largest peacetime intervention in the economy by the government ever. Its size is approximated by the “U.S. Headline Fiscal Balance” in the graph above. The only thing larger was World War II. See if you can locate the Great Depression or Great Recession.

We have learned a lot about the Coronavirus and COVID-19 in the last quarter. Let us quickly cover some of the most important aspects, even if they’re not all directly related to the stock market.

- Transmission is most likely to occur from sustained indoor contact. Outdoor activities are much safer. This is perhaps best illustrated by the absence of a surge in cases in New York after massive protests5. Other states have had surges, but those occurred during re-opening.

- The virus itself is not seasonal... but we are. The more we are cooped up inside with each other, the more we spread the virus. It should be no surprise then that the worst spread this summer is being seen in Florida, Houston, Arizona, and Imperial County, CA; areas where people flee the unbearably hot outdoors for indoor air conditioning. Colder locales should conversely beware the winter when everyone will be indoors.

- The wearing of simple cloth masks dramatically reduces the risk of transmission. The number of studies with this conclusion vastly outweighs those with the opposite conclusion. It is unfortunate that in the early stages of the pandemic the WHO, to limit hoarding, said masks were ineffective.

- COVID-19 is now believed to be a vascular disease, not a respiratory disease as earlier thought. This means it affects blood vessels. And since blood vessels go pretty much everywhere in your body, damage can result anywhere, from the kidney to the liver to the brain. This damage to blood vessels can result in thousands of tiny blood clots, and strokes. Thus, even for patients who recover from the disease, there is the potential for long-term damage.

- Two-thirds of people who became infected do not fall ill with respiratory symptoms or fever according to new studies from Italy. Only one-quarter of the infected under age 60 showed respiratory symptoms or fever.

- Unfortunately, the high frequency of asymptomatic cases is only a mixed blessing. Despite the comments from one WHO official, we do know asymptomatic spread represents an important pathway of spread, with recent estimates blaming it for almost half of infections.

- Unlike with the flu, children, especially young ones, do not appear to be an important vector for the virus spreading. The implication of this growing consensus is that schools are likely to open in some form in the fall.

- Though there are exceptions, the vast majority of fatalities consist of the elderly and those with pre-existing conditions. Current estimates are just that, estimates. But those estimates indicate only about half of one percent of people who become infected ultimately die6. This can change as treatments and conditions change.

- Herd immunity – the point at which the virus has infected so many people that it just burns itself out – appears a long way away. Even in the hardest hit areas like New York, Northern Italy, or Sweden, somewhere between 3 and 14 times more people would need to be infected for herd immunity to be achieved.

- Interestingly, people with Type A blood are at significantly higher risk of developing a severe case than are people with other blood types. Type O appears to be the most resistant.

While we have no miracle cure and a vaccine appears at least a half a year away7, an important but underappreciated aspect of our fight with the virus is that important advances in treatment have been made. The following is a quick rundown of some of the more important advances in treatment of which we are aware:

- The treatment of intubated patients (on a ventilator) with currently available anti-coagulants has been shown to double the survival rate.

- The treatment of intubated patients with the cheap and available steroid Dexamethasone has been shown to increase the survival rate by a third.

- Unlike the above examples, the new (and expensive) drug Remdesivir can be used to treat patients who are not yet severely ill to shorten the duration of the disease and reduce the risk of death by up to 62% in one recent study.

- Other drugs such as the Hepititus C drugs Sofobuvir and Daclatasvir are showing promise in reducing mortality as well.

- Infusing patients with the blood of recovered persons is also an emerging treatment.

- There have also been important non-drug changes in treatment, that can prevent patients from going on ventilators in the first place. Two of these are giving patients oxygen first and placing them on their sides in a prone position instead of leaving them flat on their backs.

Put all these developments together and you get one of our key predictions going forward: the disease will start to be less deadly. Case and infection fatality rates have not only to do with disease, but also with treatment, and we’ve had time to get better at that. This means the above stated “Infection Fatality Rate” will decline, and though cases may continue to spike, deaths, while rising, will lag far behind.

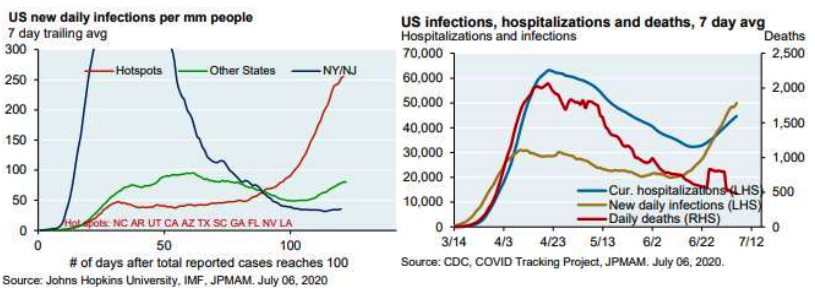

The good news is that while cases are spiking in the U.S. right now, deaths are still low. This is due to a lot of factors such as increased testing, more young people getting sick (who are less at risk of death), and, we suspect, the above-mentioned treatments. However, probably the most important factor is the two to five week lag between getting infected and dying, and thus, we believe we are about to experience a multi-week spike in deaths, since it was only last week that people started to become more cautious again. In the meantime, we know that the picture is not completely distorted due to increased testing, because hospitalizations are going up (graph at right on next page).

Despite this, we do not think we are headed toward another tight national lockdown, even if cases rise sharply (which they have). People just don’t have the appetite for another preventative lockdown. We believe we will only go into full lockdown again if hospitals are at risk of getting overwhelmed. This is a possible outcome, even though hospitals have had time to prepare surge capacity, order more PPE, and train ventilator technicians. Getting a handle on hospital capacity is difficult because there are many different types of surge capacity that can be put into use (including shipping people to other nearby facilities). Headlines can sometimes be misleading, but there are indications capacity has become a problem in Houston and areas of Florida. Any improvement in the Case Fatality Rate or Infection Fatality Rate due to improved treatment could be offset by people not being able to get that treatment.

Just because we don’t think we’re in for another strict lockdown, doesn’t mean we’re in the economic clear. We are particularly worried about the end of forbearance and roll-off of government programs that have prevented the worst of the economic damage:

- So far, the consumer spending that drives the economy has been pretty good given how many unemployed people there are. A huge driver of this is the excess unemployment benefit, which had some 70 percent of people earning more on unemployment than when they were working. However, this $600 a week benefit is due to expire at the end of July.

- The requirement that recipients of PPP loans not lay off employees in order to have their loans forgiven (i.e. turned into grants) has already rolled off for many firms. In other words, many PPP recipients can now lay off employees and they are starting to do so.

- Many creditors voluntarily agreed to suspend payments during the shutdown, but many of those agreements are coming to an end as well. Twenty states have lifted their bans on evictions and foreclosure proceedings, and nine more states are scheduled to end their bans in July.

In short, many Americans are not at all in good shape, but up to now different temporary programs have shielded them from the worst consequences. We worry about what happens if these programs are not extended and this starts to change.

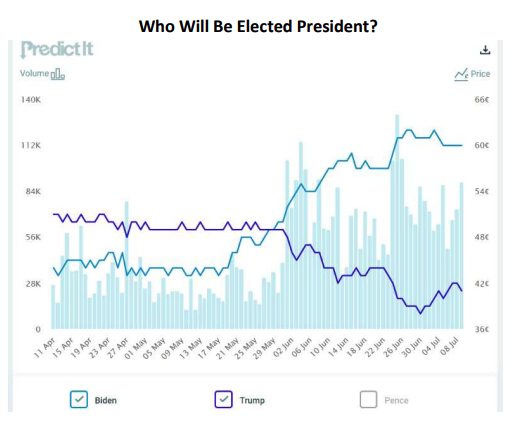

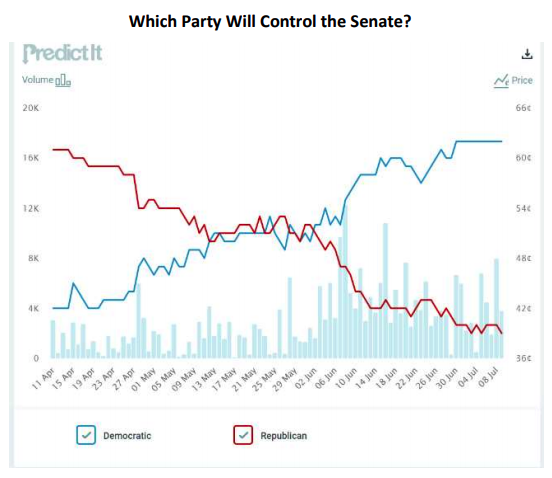

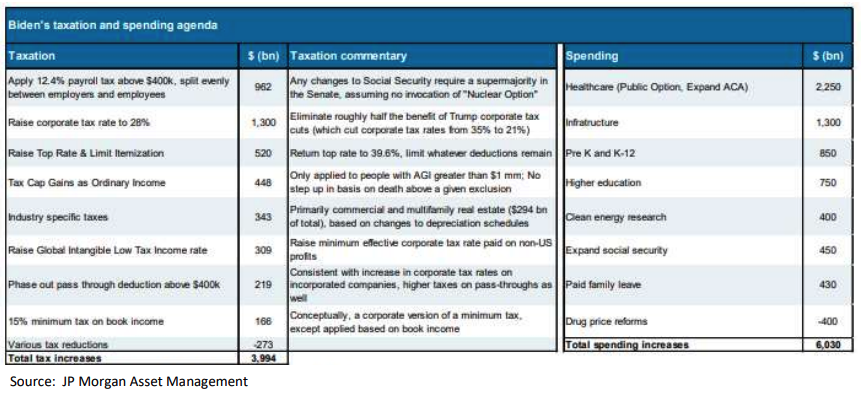

Another potential negative catalyst for the stock market is politics. Betting odds show Joe Biden is increasingly the favorite to be elected. These odds are even starting to suggest a Democratic sweep of both houses of congress and the presidency is likely (56% on www.predictit.org). Just like with Vegas odds on sporting events, sometimes the underdog wins, but the odds still mean something.

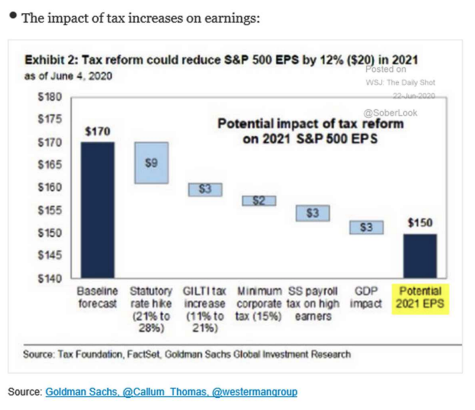

We believe political events are usually over emphasized when it comes to the stock market in aggregate. Historically, both the stock market and economy show very similar growth rates under both parties. However, this year is different in that candidate Biden proposes raising the corporate tax rate to 28% from the current 21%. This would reduce corporate earnings and affect the stock market in a very direct fashion. Just like the market went up a quick 15% on the Trump tax cut, we could see a quick correction on a Biden tax increase.

Despite the potential fallout from the virus and politics, it is important to remember that the stock market usually goes up over time. There is more uncertainty than usual in the world today, but to own stocks is to own a piece of American productivity, and America will one day emerge strong from this crisis.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 Does this activity by the State Agency cause inflation? Well, that depends on what you and the other sellers of the duplexes do. When they sell their investment properties, do they go and spend the proceeds out on the town (raising prices in general), or do they plow the money back into investments? What would you do? If the answer is the latter, or mostly the latter, then the inflation impact may be more on assets than on general everyday goods. Money printing obviously has the potential to cause inflation. But what is done with the money, once it is printed, matters. Think about our story. If the State Agency was instead buying pickup trucks and hamburgers, the impact would be different. Food and transportation prices would rise.

2 The Fed is buying corporate bonds through a $750 billion program and bond ETFs through a $250 billion program.

3 Of course, relative to their earnings, stocks today are very expensive when compared to stocks in previous years. We wrote about this dilemma in our Q4 2019 letter, available on our website.

4 This is an oversimplification, as all explanations of market activity must necessarily be.

5 There is substantial evidence besides that from the protests that outdoor activities do not regularly result in substantial transmission, especially if some distance is maintained.

6 This “Infection Mortality Rate” is inherently an estimate because we rarely know for certain everyone who is infected. The “Case Fatality Rate, which is deaths as a percentage of confirmed cases, is less meaningful, but more easily known, and is around 5% in the U.S.

7 Any vaccine proving successful is definitely not guaranteed, and even if one is proven safe and effective, it will take additional time to manufacture.

© Knightsbridge Asset Management, LLC

Read more commentaries by Knightsbridge Asset Management