What is Your Personal Downside Risk?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is light with a focus on home sales. Unemployment claims data remains an especially important indicator. Second quarter earnings reports will be more important than the economic data, but I do not expect much fresh information on COVID-19 and earnings outlook. The average investor gets little help from any of these reports and certainly not from the punditry. They are on their own with the key question:

What is my personal downside risk?

My goal is to provide some ideas for that analysis.

Last Week Recap

In my last installment of WTWA, I suggested that investors might want to study methods of hedging. On reflection, I should have discussed today’s topic first. Readers who find today’s post helpful should also review last week’s.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version. Her chart combines much of what interests us in one picture.

Most of the trading did not seem news driven, although reporters provided a reason each day. The image below is one I have been saving to illustrate this phenomenon. The inference of causality based on proximity in time is a tried and true basis for a story! Post hoc ergo propter hoc.

The market gained 1.3% with a trading range of only 3.5%. My weekly indicator snapshot monitors the actual volatility as well as the VIX (see below).

The weekly sector chart shows the source of the gains.

The “recovery” trade is leveling off a bit, but still reinforcing the market verdict on the coronavirus threat. Industrials, financials energy and materials are all part of that group. Defensive sectors like utilities, consumer, and health are perking up a bit.

Noteworthy

The Visual Capitalist calls attention to the “massive scale of the digital cloud.” Everyone has heard about the cloud, but do you really know how it works? Spend a few minutes with this post.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators have always been a valuable part of my economic review. They are especially important as we all try to monitor the economic recovery. His long-term indicators are very positive mostly from low interest rates. The short-term indicators are positive, and the nowcast remains negative. NDD continues to expect deterioration in the near term from increased COVID-19 effects.

The Good

NFIB Small Business Optimism for June registered 100.6 compared to May’s 94.4. Some of the enthusiasm is reflected in hiring and expansion plans. David Templeton (HORAN) sees this as a good sign for a “V” shaped recovery.

- MBA Mortgage Applications increased 5.1%. The increases generally signal a jump in new and existing home sales.

- Industrial Production for June increased 5.4%, better than the expected 4.6% and much better than May’s 1.4%.

- Corporate earnings reports are beating (lowered) expectations. With 9% of the S&P 500 reporting, FactSet reports that earnings and revenues are above expectations, beating the five-year average on both frequency and magnitude. Brian Gilmartin’s data show that forward earnings also continue higher. There has not been much specific outlook so far.

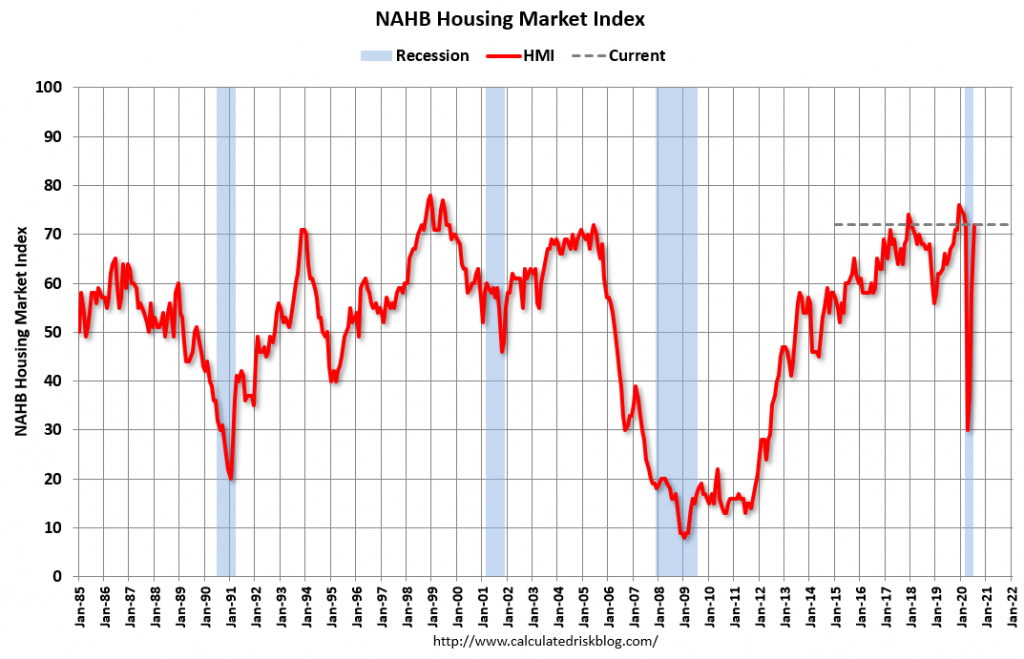

- The NAHB Housing market index for July registered 72, besting expectations and the June reading of 58. (Calculated Risk). Bill also comments on housing starts, which were in line with expectations.

- Retail sales for June were up 7.5%, better than the expected 5.2%. May’s blowout numbers were revised upward to a gain of 18.2%. The combination brings sales back nearly to the pre-pandemic levels. (“Davidson,” via Todd Sullivan). Also noteworthy is the distribution of the sales. When I mentioned the reduction in clothing sales, Mrs. OldProf opined that we should be glad it was not worse, saying, “The trend to ‘Zoom tops’ and optional bottoms might represent a 50% reduction.”

The Bad

- CPI for June increased 0.6%, slightly above expectations for 0.5% and much more than May’s 0.1% decline.

- Core CPI increased 0.2% versus expectations of 0.1%.

- Sea container counts for June remain in deep contraction. Steven Hansen (GEI) emphasizes the importance of looking at year-over-year data rather than monthly changes. Some readers have suggested that the Panama Canal widening may have altered these results. Steven has also published an interesting analysis on that topic, concluding that there has been little effect from the widening.

- Initial jobless claims were 1.300M, higher than expectations of 1.260M, but down slightly from the prior week’s 1.31M. There are still many initial claims even as the shutdown has ended in many states. Continuing claims are holding at over 17 Million. The numbers of initial claims are higher when one adds the Federal program (PUA) to normal state claims. These charts provide a good picture of the “sticky” weekly claims numbers and the overall unemployment situation.

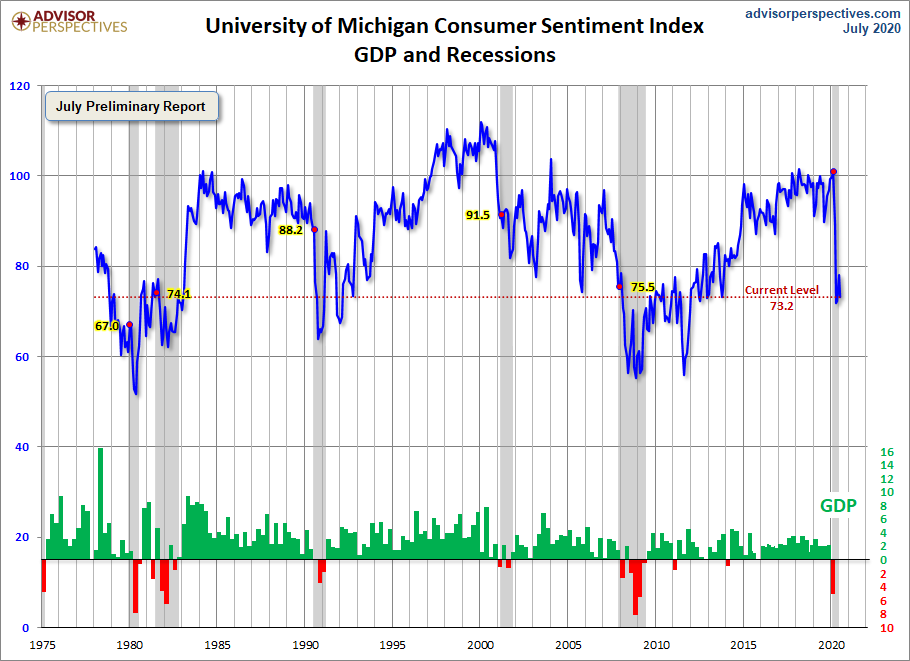

- Michigan consumer sentiment for July’s preliminary reading was only 73.2 (Jill Mislinski).

- The Federal Budget is setting new deficit records.

The Ugly

The latest state-by-state COVID-19 results. The data from the Johns Hopkins University of Medicine shows the worst and best states, and the chance to check the entire list. I have personally been monitoring the data on the entire U.S. My most recent readings were 8.7% positive, much worse than the recommended rate of 5% or below.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

There is a light calendar. Home sales data provide a good read on current conditions. Jobless claims data remain the fastest read we get about the employment situation. Leading Indicators are not very relevant at this point.

Corporate earnings reports gear up, with 92 S&P 500 stocks on the calendar. Everyone is watching for outlook and COVID-19 effects more than current results.

And of course, the political stories will also be louder and more frequent.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The economic news, yet again, got better, and pandemic news, once again, got worse. More of the punditry is expressing concern about an “elevated” market. This is especially difficult to do while claiming not to have “missed” the rally. There is some discussion about overall market valuation and narrow leadership, but little help for the average investor. The real question should be:

What is your personal downside risk?

I’ll try to show how to evaluate that in this post.

Background

There are many sources discussing the market cap concentration of a few stocks. Here are three of the best.

Taking note of the NASDAQ versus the S&P 500, the normally upbeat Paul Schatz writes:

I am recognizing that risk has increased in the stock market, especially in the NASDAQ. In other words, the window is opening for a potential stock market decline of some magnitude more than just a quick pullback. I don’t think this is a September or October story. I think that if a decline is going materialize, it should happen over the coming weeks. We now have to be on the lookout for signs of confirmation, like the tech sector rolling over and the other stock market indices unable to surge.

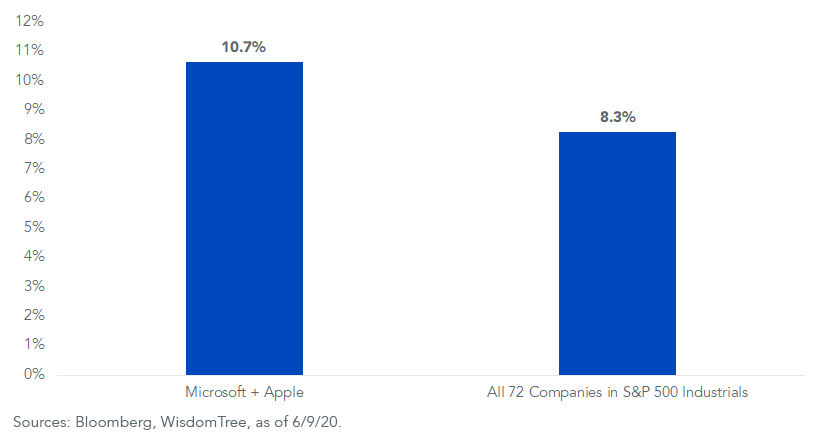

Or try this analysis from Wisdom Tree.

Dr. Ed Yardeni focuses on a few key stocks in The Magnificent Six Stocks That Are Gobbling Up Market Share. He makes several great points along with recommending MAGFAN as a more pronounceable acronym than FAANGM. Here is part of his list.

- All six are beneficiaries of the Great Virus Crisis and are expected to benefit from the aftershocks.

- They are major index components, divided among three sectors. 44.4% of the S&P 500 Information Technology sector, 66.4% of the Communication Services sector, and 50.8% of the Consumer Discretionary sector.

- All six are in the S&P 500 Growth index, representing 40.7% of the market cap.

- All have rapidly rising forward revenues and earnings, about doubling in the last five years.

- In eight years their market cap is up 467% versus 70.5% for the rest of the S&P 500.

Analyzing the Downside

My approach will be to make a few assumptions, creating a plausible scenario. Then, based mostly on experience, I will draw some conclusions about how the market would react. Wow! This is certainly dangerous. It is not a forecast. It is designed to help you think about what might happen. I encourage comments on this approach as well as the conclusions.

Overall market valuation

Many are fond of repeating that valuation is not a good timing method – especially those who have been citing over-valuation for the last decade. Nevertheless, it does get attention, so I will discuss it briefly.

- The most common method of market valuation looks at trailing earnings – either for the past year or through a model like the CAPE ratio. Analysts feel they are on safe ground when discussing data that is already in the books. We know that 2020 earnings will be terrible for the first two quarters. Many are optimistic about the rest of the year, but that depends on the speed of the rebound. The current trailing P/E (Ed Yardeni) is 22.1 and the long-term average is 15.1. My experience is that most of the talking heads use 16.5. The first case represents a market decline of 25% and the second is almost 32%. And remember, both assume the current expected rebound in earnings for the rest of the year. If there is another COVID wave or some other problem, all bets are off.

- I prefer forward earnings. Looking backwards does not really help if you are going to make some projection from it. At least the forward earnings have the benefit of hundreds of analysts talking with the companies. The current forward estimate, published weekly in my Indicator Snapshot, is 145. This implies a decline of about 17%, once again assuming that the estimates hold up.

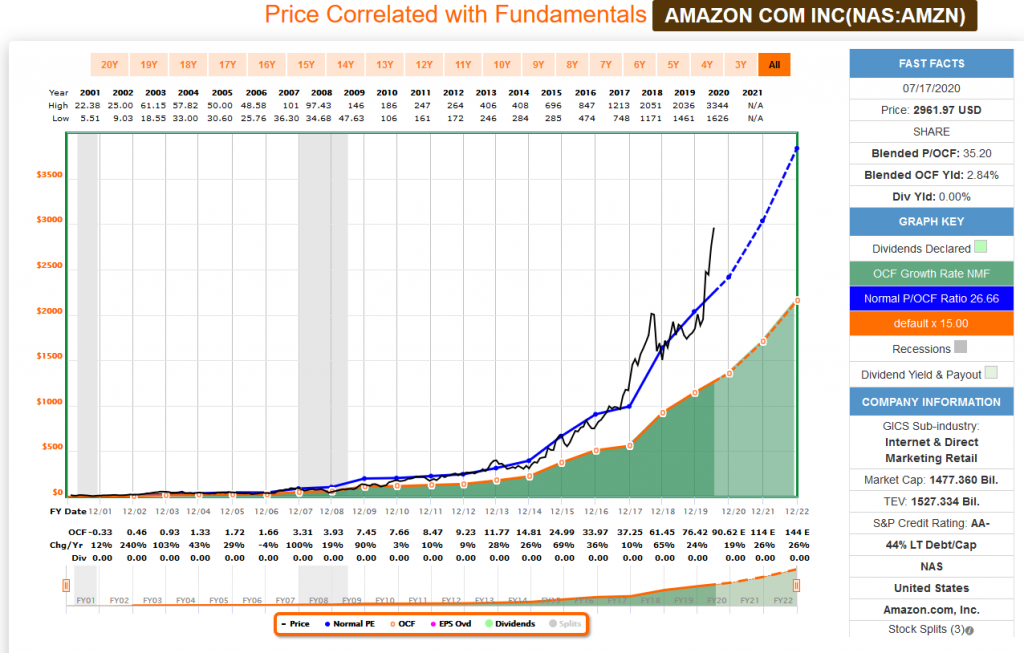

- A FAANGM analysis. Years ago, when I was writing at Real Money, the Pundit in Chief would post an annual article. He would look at each of the DJIA stocks and consider what might happen in the coming year. This involved looking at the company specifics and then applying the typical market multiples. It was both interesting and informative, but not a specific prediction. It seems to fit well with our current purpose, so I will give it a try. Here is the summary table, showing the effect of a return to a growth justified or normal P/E multiple. This is not assuming any earnings miss or decline, which would change the growth rate and the multiple.

The individual stock charts show that these names are generally priced for more than perfection. There is a story behind each. The stories explain why we should ignore traditional metrics.

I also checked the valuations using cash flow. It helped Facebook, but not the other stocks.

I have a few other conclusions in today’s Final Thought.

Ideas for Investors

I have switched the investor section to a separate post. I hope to run it nearly every week, calling it Investing for the Long Term. In the latest edition I show how to interpret the advice of “experts” using my matrix approach. In each case I added a comment about how I might use the idea and also related it to our Great Reset Wisdom of Crowds surveys. I hope readers will find this valuable and that my colleagues will consider the Great Reset Matrix as part of their selection process.

One of my personal 2020 resolutions was even more emphasis on investor education – not just recommending stocks but learning how to find suitable choices. I have created a resource page where you can join my Great Reset group. You will get updates about what is being studied and can join in the process. There is no charge and no obligation, but I hope you will join in my Wisdom of Crowds surveys. I need more wise participants! The latest survey results are part of my most recent report. The results of our team effort will be published on a regular basis, so you will be joining me in contributing to a greater good.

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

Despite the improving technical indicators, I continue my rating of “Bearish” in the overall outlook for long-term investors. We should also keep watch an inflation antcipation. So far it has not affected bond prices.

The C-Score remains at levels never before seen. It is combining the sharp economic rebound with pandemic effects. When we are able to separate the two, a current mission of Dr. Dieli, it will provide more guidance on the timing and extent of the recovery.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian also takes note of the improvement in corporate credit spreads.

David Moenning: Developer and “keeper” of the Indicator Wall.

Georg Vrba: Business cycle indicator and market timing tools.

Doug Short and Jill Mislinski: Regular updating of an array of indicators, including the very helpful Big Four.

Final Thought

Here are a few ideas that deserve further discussion.

- For those who think the crisis is ending soon, they may face a contradiction. These stocks are not the best in that scenario.

- An earnings miss is especially painful for a high P/E stock. There is a reduction in current earnings but also a revised path for earnings growth. The result is a reduction in both earnings and the multiple.

- Do not uses paying taxes as a reason to hold dangerous stocks. Do you know how much of a decline it would take to equal your taxes? There is always a breakeven point. If you do not know it, you are just guessing about the tax decision. I have seen people lose most of their wealth by refusing to realize gains on their most successful picks.

- ETFs do not provide needed diversification and may contribute to the current risk. Howard Marks puts it well in this interview:

When you see the way the markets have been going. It’s estimated for example that over 95% of all transactions on the New York Stock Exchange are made by machines nowadays, or at least investors who don’t make value judgements.

We’ve had a huge increase in index and other forms of passive investing but when money comes in to an S&P Index fund there’s nobody sitting at the fund who says – the markets too high I’m not going to put the money to work or who says there are 500 stocks I’m supposed to buy but these 50 are too expensive I’m only going to put money in the other 450. They have no choice but to continue putting money in everything in the index for example.

Sit back, relax, and think carefully about these three questions:

- What is your financial risk based upon your current holdings?

- Do your holdings provide diversity rather than emphasis on the most expensive stocks? (Check out your fund or ETF to find the top holdings).

- Forget about “risk tolerance” questionnaires. What type of market decline would you find acceptable? (Hint: It matters how quickly your holdings are likely to rebound).

I’m more worried about

- Continued lack of progress among leaders. The timing of this crisis, in the homestretch of the election season, is a special challenge. This is a repeat worry, but sadly it is not changing.

- State and local finances. These governments pay many of our essential workers and lack the ability to do so in times of stress.

- Conflict with China over Hong Kong.

I’m less worried about

- The Chinese economy. Here is some granular evidence from The Transcript:

China has bounced back

“So, our hotels in China all have already come back to some degree of business. Those that are within driving distance of a major metropolitan centre have recovered fully. ” – Banyan Tree Holdings (SGX: B58) Executive Chairman Ho Kwon Ping

“What we saw in Hong Kong is there’s a quick bounce back and Hong Kong is back to pre-COVID or very close to pre-COVID levels essentially positive volumes in many circumstances as well. So, this is something that frankly is not unexpected” – Uber Technologies (UBER) CEO Dara Khosrowshahi

- Vaccine progress. There are more competitors and the time frames have been accelerated.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All