Time for A Look Under the Hood of the Economic Engine

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe face an important economic calendar and earnings reports from 192 companies in the S&P 500. We will get important data on sentiment, personal income and spending, housing, employment claims, inflation, manufacturing. The first estimate of Q2 GDP is expected to be bad, very bad. And by the way, the FOMC meets and announces a rate decision on Wednesday.

The punditry will seek any hints about the state of the recovery as well as commentary about the COVID-19 impact. Earnings reports and the Fed press conference will be the basis for clues.

The difficulty with this search for evidence is confirmation bias. In a world where the data is suspect, unsupported opinion may sound profound.

In the days before the check engine light, a car owner might hear an odd noise and do their own checking, just like these boys working on a first car.

Investors are not compelled to take opinion at face value, of course. We can ask whether we hear a knock in the economic engine.

It is time to look under the hood.

This may not seem very exciting but give it a chance. I think you will be surprised at what you learn.

Last Week Recap

In my last installment of WTWA, I called attention to some hidden risk faced by investors – the concentration of a few stocks. This was indeed a popular topic in financial reporting last week, especially with some stumbles from the big five. It was an almost daily topic on CNBC and here is an example from print.

If the ‘Big Five’ Tech Stocks Falter, They’ll Take the Rest of the Stock Market Down With Them

And from Jesse Felder, who is always on the watch for problems, we have this chart and comment:

Just three stocks, Apple, Amazon and Microsoft, make up more than 16% of the S&P 500 Index and over a third of the Nasdaq 100 Index. Together they are now valued at nearly $5 trillion. That’s larger than the entire economy of Germany and roughly the size of the Japanese economy.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version. Her chart combines much of what interests us in one picture.

Once again, there was little change in fundamental values or news during the week.

The market lost 0.3% with a trading range of only 2.5%. My weekly indicator snapshot monitors the actual volatility as well as the VIX (see below).

The weekly sector chart shows the sources of the action.

The “recovery” trade is leveling off even more but remains in “improving” territory. Industrials, financials energy and materials are all part of that group. Defensive sectors like utilities, consumer, and health, continue to improve.

Personal Note

My plan, barring a major market event, is to take off next weekend. (This naturally increases the odds of a major market event!)

Noteworthy

There are many skilled and experienced people working to bring clarity to the COVID-19 data. I have mentioned several sources in the past. I follow several of them and calculate some of my own indicators. The positive test rate for the U.S., for example, is hovering at about 9% after a dip two months ago. At one point, eleven states were ready to test and trace. That has fallen to zero.

I especially like the ability to interact with data, asking my own questions. Prof. Wade Fagen-Ulmschneider (who goes by Prof. Wade) of the University of Illinois has done a beautiful job of providing this opportunity. Visit his site to try the different visualizations and animated features. Here is a static shot which only hints at what you will find. (HT to NDD for suggesting this!)

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators have always been a valuable part of my economic review. They are especially important as we all try to monitor the economic recovery. His weekly report shows little change. NDD warns that the “nowcast” data is most important to watch, and it remains negative. He concludes:

As to the US, I encourage anyone who doubts that deaths have started increasing again to click over to 91-divoc.com and check out their graphs of cases, hospitalizations, and deaths. Further, and most importantly, federal emergency unemployment benefits have terminated this week, and while the House passed an extension several months ago, the Senate has not even debuted a plan. I anticipate a poor market reaction to this on the order of that which greeted the federal government shutdown at the end of 2018 through January 2019.

The Good

- Mortgage applications showed continued strength.

- Existing home sales for June registered 4.72M (SAAR), in line with expectations of 4.70M but beating May’s 3.91M.

- New home sales for June reached 776K (SAAR) beating both expectations of 680K and May’s 682K. Calculated Risk analyzes the results – the best since 2007. He expects continued strength in July. Is this a good sign for the economy? Maybe not, he writes:

Important: No one should get too excited. Many years ago, I wrote several article about how new home sales and housing starts (especially single family starts) were some of the best leading indicators for the economy. However, I’ve noted that there are times when this isn’t true. NOW is one of those times.

Currently the course of the economy will be determined by the course of the virus, and New Home Sales tell us nothing about the future of the pandemic. Without the pandemic, I’d be very positive about this report.

The longer the pandemic lasts, the more long term damage to the economy – and, if the pandemic worsens and persists – that will eventually negatively impact housing. The outlook for housing depends on the outlook for the pandemic.

- Continuing jobless claims were 16.197M, down from a downwardly adjusted 17.304M. This report trails initial claims by one week and remains very high.

The Bad

- Leading economic indicators for June gained 2.0%, slightly missing expectations of 2.1% and much lower than May’s upwardly revised 3.2%.

- Initial jobless claims increased to 1.416M, higher than expectations of 1.285M and the prior week’s 1.307M.

- Homeowners in mortgage forbearance plans increased, but just slightly. (Black Knight via Calculated Risk). And serious delinquencies surged to a 9-year high.

The Ugly

Policy inaction in the face of key economic issues, especially these two.

- State and local government finances – both for services and economic impact.

- Expiration of unemployment benefits.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

We have a big economic calendar. The ISM Manufacturing Index is a widely followed read on current conditions. Jobless claims remain the timeliest employment indicator. Sentiment reports from both the Conference Board and the University of Michigan will tell us something about the state of the consumer, which will also be reflected in personal income (seen as lower) and personal spending (expected to be higher). Durable goods orders are a factor in the GDP calculation. PCE prices are the Fed’s favorite inflation measure, which makes them worth watching. Rounding out the big week we will have several housing reports and the first estimate of Q2 GDP. Think bad, very bad.

And while no one expects a policy change from Wednesday FOMC announcement, all will be looking for any hints of the next policy step.

Corporate earnings reports gear up, with 192 S&P 500 stocks on the calendar. Everyone is watching for outlook and COVID-19 effects more than current results.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

There is something troubling about the economic data. There are small reversals in many indicators. These are often better than economic forecasts.

The problem is that none of this represents a convincing picture of the return of real economic strength. The numbers just do not “add up.” Since there might be something wrong with the economic engine,

It is time for a look under the hood.

Background

Prof. Menzie Chinn makes a key point in his look at the upcoming GDP report and the several revisions that will follow. In general, this is a normal process with modest effects. He writes:

In other words, not only is potential GDP an estimate; so too, to varying degrees, are all the GDP figures associated with each release (advance, 2nd, 3rd). It’s just that usually, the revisions are expected to be relatively small. This is not the case as the recession deepened after Lehman Brothers collapsed, and not the case for 2020Q2.

So many take the reported data at face value. This includes highly paid economists at big firms and policymakers who consume their work. A skilled data analyst learns that you cannot just look at equations and indicators. You need to get your hands around the data. You need to see it.

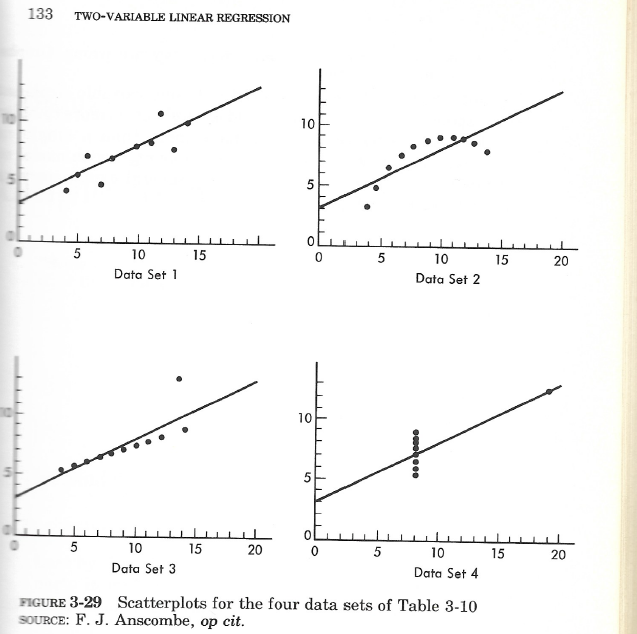

In one of my classes teaching data analysis I used a wonderful book by Edward R. Tufte, Data Analysis for Politics and Policy. It is so good that it survived the major reduction in my library before our move west. In one example he provides a great teaching example. He provides four data sets that are very similar on most material numerical measures, including a regression analysis. Then he shows the folly of relying on the numbers and computer output alone.

In presenting this lesson my key point was to make sure that your conclusions were firmly based upon available data. Inference can be especially dangerous when there are extreme outliers. If the outlier is part of the prior data, you could choose to leave it out. But what if the outlier is the current problem?

I have written about economic indicators for more than fifteen years in WTWA and studied them before that. Usually there is some value in each. Not now. Very few are helpful in identifying the economic turn and prospects.

Indicator Analysis

I will summarize the indicator, how it is interpreted, the current implication, and my own comment.

| Indicator | Interpretation | Current | Jeff Comment |

| Monthly Employment Reports | Survey based methods of determining the number of payroll jobs and the extent of unemployment. The official report. | A brisk rebound in jobs and a reduction in unemployment. The data have been good enough to influence current policy decisions. | I have little confidence in this report – at least right now. Like most economic observers, the May report was an outlier. I will soon publish a more detailed explanation. |

| Jobless Claims | The most current read on employment, using data from local employment offices. There is noise in the national report when some states have trouble collecting data. | Early on, the increase in jobless claims was consistent with the economic shutdown. Some rebound was expected as parts of the country reopened. The series has become flat. | Analysts are reaching for explanations about why claims have not declined further. Maybe the jobless claims are right, and the monthly report is wrong. |

| CNBC “Markets in Turmoil” | Shows up whenever the DJIA has made a big move lower, formerly a “triple digit” move, but now higher. Sometimes volatility itself qualifies. | Not in evidence in the evening hours in recent days, although various versions appear during the day. | The main implication is that you won’t get to watch Jay Leno or Shark Tank that night. |

| Vaccine Stories | A COVID-19 vaccine is the ultimate assurance that the end of the recession is coming. | Vaccine development has progressed well. Products have moved into late trial stages and production facilities are already under construction. | The most optimistic estimates are for early candidates to have some availability by the end of 2020 or early 2021. Most underestimate the distribution problems and the need to meet a minimum number of participants. |

| Interest Rates, Yield Curve | The level of rates indicates inflation expectations. The yield curve is an indicator of economic strength or weakness. | Interest rates remain at record lows. The yield curve has regained some slope. | Current rates contain very little information. The Fed controls the short end and is now more involved in the longer maturities. European bond rates have also pushed down the ten-year note. |

| Debt | An objective measure of the fiscal policy of countries and the financial strength of companies. | Rising rapidly, it is seen by many as an imminent danger sign. | My take is a little more nuanced. Austerity at all levels reduces revenue and can make the problem worse. Reducing debt will be easier when we have improved the economy. |

| Inflation | Measured in various ways, it describes how a basket of goods is changing in price. | Inflation remains very low – the 1 – 2% range with little change in sight. Very few average people believe this. | Regardless of your personal feelings about the cost of living, official numbers govern many types of payments, including Social Security increases. Watch the PCE price level, which captures elements important to Fed policy. |

| Corporate Earnings | The reason to buy stocks. If there were no earnings, why invest? | Earnings are down dramatically, about 40% year over year. | Trailing earnings are known – safe for pundits and fund managers who want to “demonstrate objectivity.” The current market is looking past current earnings for the first time in many years. The 2020 effects will also linger in the CAPE ratio for another decade. |

| Corporate Forward Earnings | More important than trailing earnings, since there is a basis for estimating future cash flows. | Currently following the trailing earnings, which companies and analysts use as the basis for prediction. Brian Gilmartin’s valuable work provides regular updates on this key indicator. | I am skeptical about current estimates leading to $163 for the S&P 500 in 2021. I expect the recession to last longer than expected and many more companies to fail. |

| Correction Indicators | You analyze a chart in an effort to find trading ranges, breakouts, support levels and the like. | Pick your analyst. | I make some limited use of simple technical indicators, but they are of little current help. If there is a big change on the recession front, we can forget about the technical predictions. |

| Volatility | Historical volatility is measured by past stock price data. Expected volatility is determined by a formula based upon option trading in particular products. | Volatility is perceived as dangerous for the investor. I monitor both historical and implied volatility each week in the indicator snapshot. | Volatility is not dangerous per se. It reflects moves both higher and lower. There are better risk measures. Investors who know how to value their holdings can use volatility to their advantage. |

| Consumer Sentiment | Sentiment is measured by several different firms using survey questions. Some of the surveys are very well done and based on long experience. | Nearly all survey measures have shown a rebound from the shut down days. The surveys are pretty good at measuring current feelings and actions, but perhaps not as good at whether plans will be executed. | From my experience I have more confidence in surveys than many other analysts. I see them as confirmation of current behavior rather than a solid look forward. |

| Diffusion Indexes | These include the ISM, PMI, and regional Fed measures. You ask whether things are better or worse (including a range of topics). You subtract the worse number from the better number to get the index. | The surveys are now showing a brisk rebound from the initial recession lows with some showing significant expansion. | The problem with this basic approach is that it counts the number reporting a change, not the size or significance. If everyone finds that things are a little better, the index is much higher. That explains the recent wild movement in these measures. There is also a question of who is included in the sample, but that is currently less important. |

| Business Sentiment | Indicators like the NFIB provide a sense of how small businesses see things. The NAHB tells us about homebuilder sentiment. North Carolina does an annual survey of CFO’s. | Small businesses like the President and the reduction in regulations. Homebuilders are enjoying great times. The CFO’s are not so enthusiastic. | I see these as concurrent indicators, confirming business conditions. While some of the questions are forward looking, we need some data to demonstrate a relationship. CFO’s are a dour lot, always lower on optimism than anyone else. [Mrs. OldProf rejected my proposal to insert an accountant joke at this point]. |

| Smart Money | An indicator defining “smart money” as big traders, late in the day traders, or some similar idea. | The smart money is currently described as bearish. | The average investor has been beating the smart money, which probably does not prove anything. I ignore this indicator. |

| Housing | Home sales, especially new ones, new permits, home prices and several others. | Housing has been a bright spot for a long time for reasons I have frequently described. Things look good. | While I have enjoyed large gains in this sector and maintain those positions, I do not see it as an important economic indicator. See Bill McBride’s comment above. |

| Movement Toward Balanced Reopening | No specific indicators. Pundits either talk about the virus or the economy, not how joint progress can be made. | The prospects are not very good. Many are in denial about the rebound in virus cases, which reduces the chances for progress on testing and tracing. | A balanced solution will have more tests, immediate and effective tracing, and protection for all parts of the population. It will encourage a return to work by improving the safety and finding those whose risk is lower. |

I have a few other conclusions in today’s Final Thought.

Ideas for Investors

I have switched the investor section to a separate post. I hope to run it nearly every week, calling it Investing for the Long Term. In the latest edition I show how to interpret the advice of “experts” using my matrix approach. In each case I added a comment about how I might use the idea and also related it to our Great Reset Wisdom of Crowds surveys. I hope readers will find this valuable and that my colleagues will consider the Great Reset Matrix as part of their selection process.

A Personal Favor

Please consider joining the Great Reset group. You will get updates about what is being studied and can join in the process. There is no charge and no obligation, but I hope you will join in my Wisdom of Crowds surveys. I need more wise participants! The latest survey results are part of my most recent report. The results of our team effort will be published on a regular basis, so you will be joining me in contributing to a greater good.

We have already identified key sectors to avoid as well as those worth further examination. Articles in financial publications are only now catching up. In the next stage of our research (leading to specific stock ideas) we will go inside the cells of the Matrix to build a watch list. There will also soon be another Wisdom of Crowds survey, helping to gauge the length of the pandemic. I have created a resource page where you can join my Great Reset group.

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

Despite the improving technical indicators, I continue my rating of “Bearish” in the overall outlook for long-term investors. We should also keep watch on the increase in anticipated inflation. So far it has not affected bond prices (Thanks, Chairman Powell) but it eventually will.

The C-Score remains at levels never before seen. It is combining the sharp economic rebound with pandemic effects. When we are able to separate the two, a current mission of Dr. Dieli, it will provide more guidance on the timing and extent of the recovery.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian also takes note of the improvement in corporate credit spreads.

David Moenning: Developer and “keeper” of the Indicator Wall.

Georg Vrba: Business cycle indicator and market timing tools.

Doug Short and Jill Mislinski: Regular updating of an array of indicators, including the very helpful Big Four.

Guest Commentary

If we are looking under the hood, it helps to consider the composition of key market indices. My colleague Todd Hurlbut does this very nicely for the DJIA and the S&P 500. He discusses the history, how the competition changes, and the shortcomings. His conclusion:

While stock indices play an important role in understanding markets and their current trajectory, it pays to look a little deeper to determine what is really happening. On the surface, things can look rosy while market internals may in fact be painting a very different picture. Historically, sustained bull markets in stocks require broad participation, a characteristic which is absent from the current advance. Next time the newscaster reports on the Dow Jones Industrial Average, take it with a grain of salt.

This chart shows a longer-term history of a key element in my indicators snapshot.

Supply chain problems are often mentioned, but these second order economic effects are difficult to measure. CNN Business explains the shortage of aluminum cans – and perhaps your favorite beverage!

Final Thought

If your conclusion is that I am discouraged about the relevance of current data, you are correct. We should not be impressed by small rebounds in specific measures. Data will eventually regain importance.

Many months ago, I wrote that understanding this problem required combining expertise with modeling, epidemiology, economics, public policymaking, and investments. Many are happy to state opinions without any knowledge of the relevant fields.

Those who offer advice to decision makers have an important obligation: Be aware of when you have nothing to say!

Politicians want to speed up reopening, but it will not happen until people feel safe. From Alan Murray’s CEO Daily:

Are Americans ready to reopen? A survey by Fortune Analytics, done in conjunction with SurveyMonkey, makes it pretty clear most are not. The survey found:

–Only 43% of Americans are comfortable to return to dine-in restaurants;

–Only 27% of frequent flyers are ready to board a flight again;

–Only 26% are willing to return to bars;

–And only 20% would feel comfortable attending a large public gathering.

If Alan were a member of the Great Reset project, he would have known about this two months ago.

The Brookings Institution continues research on Reopening America: The value of testing and modeling. Here is the key theme:

Decision-makers must balance the imperatives for reopening to restore economic activity, education, and social life against the epidemiological risks of renewed transmission. Reopening too soon, or without the right epidemic control measures in place, is likely to produce additional waves of infection. Experience from other epidemics suggests these waves could produce surges of infection as high or worse than what the country has experienced so far. The science of epidemics tells us clearly that until a large fraction of the U.S. population has immunity—whether via a widespread vaccine or recovery from previous infection—the risk of resurgent infection will not go away. Given that a successful vaccination effort is likely many months into the future, and that we are currently far from widespread immunity, can the risks of reopening be mitigated or managed? Is there a “middle path” between indefinite shutdown and a freely spreading virus with inevitable high tolls of disease?

Until we see tangible progress toward this “middle path” the investment climate will be unattractive.

I’m more worried about

- The latest tit-for-tat with China concerning consulate closures. This might seem unimportant, but it is another indicator of growing tension in the relationship.

- The train wreck of electoral politics in the face of needed action and coordination.

- Tropical storms threatening parts of the country already hard hit by the coronavirus.

I’m less worried about

- Attitudes toward mask-wearing. The percentage has moved a little higher but is still only about 67%.

- Isolation. The return of some sports TV will help many.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All