China’s Economic Growth: Stronger Exports Support Recovery

Want to read more by VanEck? Visit their Featured Firm page here

China has been a major contributor to global growth, and its economic activity tends to have significant repercussions for the global economy. To understand where the Chinese economy is in its growth cycle, we highlight a few key charts below, which may also provide context for the impact of the coronavirus. China-related political and geopolitical headlines are grabbing the most attention lately. However, China remains an important economic bellwether for countries that have started to reopen following the COVID-19 epidemic.

Chinese Economy Health Check: PMIs

China’s latest official Purchasing Managers Indices (PMIs)1 confirmed that the rebound is gaining pace and that manufacturing—and large companies in particular—continues to drive the recovery. The manufacturing PMI surprised to the upside in July, rising to 51.1. The new orders PMI also edged higher to 51.7. Business activity expectations continued to improve both in manufacturing and services, with the latter showing strong overall results (the non-manufacturing PMI is at 54.2).

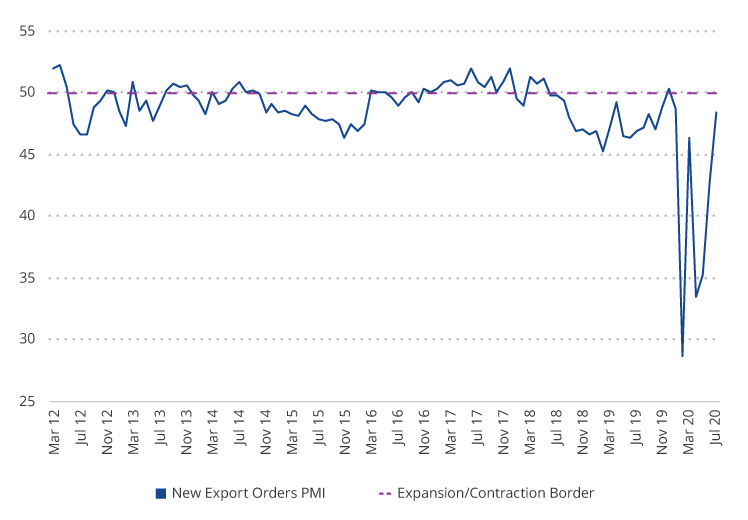

China New Exports Orders PMI

Source: Bloomberg. Data as of July 31, 2020. Past performance is no guarantee of future results. Chart is for illustrative purposes only.

A sharp improvement in new export orders suggests that global headwinds are subsiding as the unprecedented stimulus and pent-up demand are kicking in (we are still keeping an eye on a potential second wave of the virus though). However, the dichotomy between the large and small companies PMI persists, and it mirrors the divide between private and state-owned investments earlier this month. The large companies PMI remained firmly in expansion zone (52.0) in July, while small companies PMI slipped further down to 48.6.

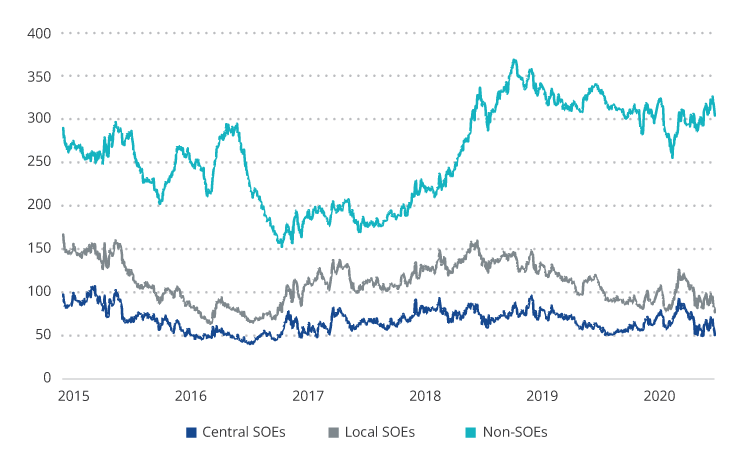

Understanding the Credit Cycle: Non-SOE Borrowing Costs

Source: UBS. Data as of July 28, 2020. Past performance is no guarantee of future results. Chart is for illustrative purposes only. Spreads are measured relative to average yield of 1, 3, 5, and 10 year bonds issued by the China Development Bank.

As with any economy, central bank policy is very important in China. In this chart, we can see that interest rates for the private sector fluctuate, whereas the interest rates paid by state-owned enterprises (SOEs) are pretty stable. Therefore, to understand the credit cycle, we point your attention to this private sector, or non-SOE, interest rate.

We think that the imperfect transmission mechanism is partly to blame for the slip in the small companies PMI. It keeps the financing costs for smaller and privately owned firms high, despite multiple pledges to lower them. However, it is also exceedingly clear that authorities learned from previous boom and bust episodes and are not too eager to create another one now. Recent communications from the central bank and this week’s Politburo meeting warned against monetary policy excesses and pointed to targeted (“drip”) stimulus as the preferred tool.

Finally, even though July’s PMIs pointed to improving external conditions, short-term and especially longer-term uncertainties abound. The Politburo’s emphasis on domestic demand—both in terms of consumption and more self-sufficiency—should not come as a surprise.

DEFINITIONS AND DISCLOSURES

Source for all PMI data: Bloomberg

1Purchasing managers index (PMI) is an economic indicator derived from monthly surveys of private sector companies. A reading above 50 indicates expansion, and a reading below 50 indicates contraction. We believe PMIs are a better indicator of the health of the Chinese economy than the gross domestic product (GDP) number, which is politicized and is a composite in any case. The manufacturing and non-manufacturing, or service, PMIs have been separated in order to understand the different sectors of the economy. These days, we believe the manufacturing PMI is the number to watch for cyclicality.

Please note that Van Eck Securities Corporation (an affiliated broker-dealer of Van Eck Associates Corporation) offer investment products that invest in the asset classes discussed in this commentary.

This is not an offer to buy or sell, or recommendation to buy or sell any of the securities mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

© VanEck