Economic Sunrise?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe have a big economic calendar with reports on inflation, small business optimism, retail sales, consumer confidence, and unemployment claims. I expect the data to continue occupation of the back seat. The election news is easy to write about, and financial media are taking the bait. Anything about the pandemic is newsworthy. Most important will be the fate of moves to extend economic assistance to the unemployed and others.

Many pundits have been unduly pessimistic about the economic rebound. That has also been my viewpoint. I am accepting a reader suggestion to think carefully about my conclusions. What would make me bullish? Put another way:

Are we witnessing an economic sunrise?

Last Week Recap

In my last installment of WTWA, I raised concerns about the accuracy of the upcoming payroll employment report. I described the problems more completely in a Wednesday preview and another post after the release. Employment was a big topic during the week, of course, but no one else has joined in about my specific concerns. The actual job count will be available in about six months.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version. Her chart combines much of what interests us in one picture.

Once again, there was little change in fundamental values or news during the week.

The market gained a strong 2.4% on the week with a trading range of only 2.1% (after Monday’s gap opening). My weekly indicator snapshot monitors the actual volatility as well as the VIX (see below).

The weekly sector chart shows the sources of the action.

The “recovery” trade is still leveling but remains in “improving” territory. Industrials, financials, energy and materials are all part of that group. Defensive sectors like utilities, consumer, and health, continue to improve. You can watch the progress of the rotation via this chart.

Noteworthy

Statista continues excellent coverage on important questions.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators have always been a valuable part of my economic review. They are especially important as we all try to monitor the economic recovery. His weekly report remains positive in the long leading and short leading indicators and has improved to neutral on the nowcast. He views the current rebound to be dependent on the continuation of emergency unemployment benefits.

The Good

- Light vehicle sales for July improved to 11.19 M (annualized) from June’s 9.58. “Davidson” via Todd Sullivan explains the importance and also why interpreting stats in this recession is a different challenge.

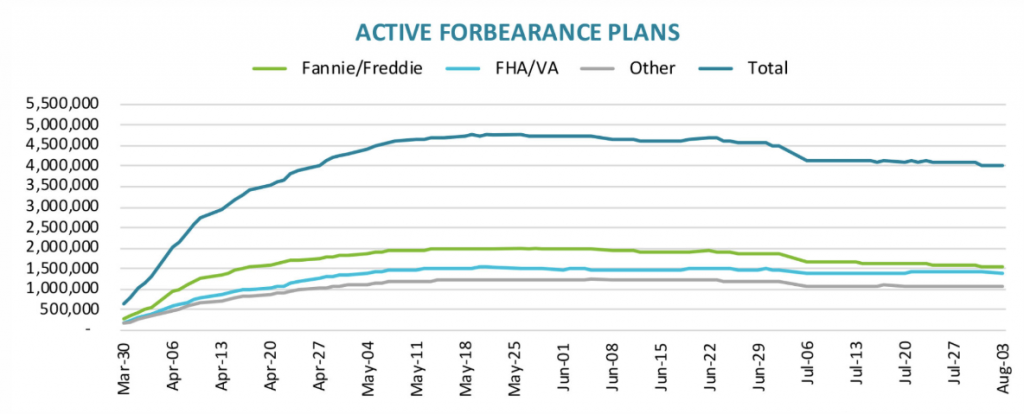

- Mortgage forbearance plans fell by 101,000. About 4 million homeowners remain in active forbearance, 7.5% of all mortgages. (Calculated Risk).

- ISM Manufacturing for July registered 54.2 beating expectations of 53.4 and June’s 52.6.

- Factory orders for June increased 6.2%, better than expectations of 5.2% but weaker than May’s (downwardly revised) 7.7% gain.

- ISM Non-Manufacturing for July was 58.1, much better than expectations of 55.2 and also ahead of June’s 57.1. (Jill Mislinski).

- Initial jobless claims declined to 1.186M, historically high, but significantly better than expectations of 1.4M and the prior 1.435M.

- Rail traffic is showing improvement. See Steven Hansen’s (GEI) innovative look at the economically intuitive sectors.

- Continuing jobless claims declined to 16.107M from the prior week’s 16.951M.

- Corporate earnings reports have soundly beaten lowered expectations. FactSet reports record high levels of earnings beats (83%) and the margin of outperformance (22.4%). Revenue is also beating the five-year average in both number and margin.

The Bad

- Construction spending for June declined -0.7%, worse than expectations of a 1.3% gain, but better than May’s 1.7% decline.

- MBA mortgage applications declined 5.1%, worse than the prior week’s -0.8%. As the regular chart from The Daily Shot shows, the purchase index remains at very high levels.

- ADP private employment grew 167K versus expectations of a gain of 1.6M. The June report, however, was revised from a gain of 2.639M to 4.314M. The massive revisions, induced by a desire to match and/or forecast the BLS result, are reducing the value of this information.

- Nonfarm Payrolls for July increased 1.763M, lower than expectations for 2.0M and June’s gain of 4.719M. Other aspects of the employment situation report (hourly earnings, hourly earnings, unemployment rate, etc.) were somewhat positive. This suggests a weak situation that is improving slightly.

-

Imminent end of COVID-19 relief as Congress and the President could not come to an agreement on extensions. The President, though an executive order, extended unemployment benefits (on different terms), delayed payroll tax requirement, and extended protection on mortgages and student loans. We can expect discussion on the legality of these orders.

- From Statista.

The Ugly

Lebanon – a toxic brew of political unrest, economic weakness aggravated by a COVID lockdown, spreading COVID cases, and a deadly explosive catalyst.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

We have a big calendar, featuring inflation data, small business optimism, consumer sentiment, retail sales, and jobless claims.

Earnings season has wound down, but we can expect even more political news along with pandemic updates.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

As has been the case for months, the economic specifics will be less important than the interplay of pandemic and the economy. My analysis of this has been extensive and timely, but my conclusions are not popular. The genesis of this week’s topic came from a reader comment. I described it to Mrs. OldProf as a loyal reader who felt I had spent too much time in the desert sun. Naturally, she challenged me and wanted details. I had to admit that it was actually an extremely courteous observation that my viewpoint might be influenced by living in a COVID_19 hot spot. Upon reading the comment to her, she translated it as a reasonable request to consider the other side. As usual our conversation moved to the Packers, our insulted QB, and whether we would actually have a season. But she had done her job.

I was convinced. Whenever you have a viewpoint, you should periodically ask yourself what would change your mind. This is not the exact request from my reader, but it sparked the idea.

Perhaps we need to ask:

Are we enjoying an economic sunrise?

Good things must start somewhere. Have recent stock moves confirmed the optimism on several important fronts?

Background

There is an intense search to explain current market prices, resulting in many theories. Here are a few.

Tom Lee, Fundstrat Global Advisors, has been bullish and right through the rally days. He sees a big breakout and is willing to make a forecast with a date: Next Week!

The Fundstrat team finds that it takes 20 days after the cases have peaked for the rally to begin. That would be August 14th.

Bill Miller, Miller ValuePartners’ founder and CIO.

Challenged with the data on “pandemic pivots” in an interview by Consuelo Mack, he cited the following bullish observations:

- The market’s fall in March of this year represented an excellent buying opportunity, according to Miller, who underscored his belief that people are underestimating values. Given the backdrop of low interest rates and no inflation, Miller says, “we can get valuations that go much higher, so buying now is a good thing.”

- His firm’s tech holdings (it owned Facebook and Amazon as of their IPO dates) do not fly in the face of his value investing philosophy, says Miller.

- Miller says the degree to which debt concerns him is dependent on a company’s cash flow and interest coverage. It worries him more in capital intensive, commodity businesses (like oil), he notes.

- Regarding the hit taken by the airline industry due to the pandemic, Miller contends, “if you had airlines and sold them, you were effectively betting against a vaccine or effective treatments.” He believes airline traffic will come back “faster than the current stock prices would indicate. Right now, I’m not betting in favor of a vaccine, but I’m not willing to bet against it.” He notes that only one case of Covd-19 could be traced to flying in an airplane and believes strongly that traffic will gradually come back as people become more comfortable. Airline holdings also offer diversification, he adds.

- Miller has no concern regarding financials and describes them as “among the most attractive areas of the market today” given their strong capital positions and profitability. Even with the stress of the pandemic, Miller claims that financials “aren’t getting worse, they’re getting better.”

- On a more macro level, Miller argues that the market is “taking too dire a view of perceived risk” relative to the real risks presented by the current environment. “When people are fearful,” he says, “their perception of risk changes dramatically”—which is what happened with the market went from an all-time high to a bear market in four weeks.

Howard Marks, Oaktree Capital Management provides many interesting ideas in his latest report to his investors. I urge you to read it all, which includes his account of recent events, policy reactions, and mistakes by all. Many of these echo the problems I have written about. There is a long list of continuing worries, but today’s mission is to ferret out the bright side. Here are his comments on that front:

The first is that many investors have underestimated the impact of low rates on valuations. In short, what should the stock market yield? Not its dividend yield, but its earnings yield: the ratio of earnings to price (that is, p/e inverted). Simplistically, when Treasurys yield less than 1% and you add in the traditional equity premium, perhaps the earnings yield should be 4%. That yield of 4/100 suggests a p/e ratio (the inverse) of 100/4, or 25. Thus the S&P 500 shouldn’t trade at its traditional 16 times earnings, but roughly 50% higher.

Even that, it’s said, understates the case, because it ignores the fact that companies’ earnings grow, while bond interest doesn’t. Thus the demanded return on stocks shouldn’t be (bond yield + equity premium) as suggested above, but rather (bond yield + equity premium – growth). If the earnings on the S&P 500 will grow to eternity at 2% per year, for example, the right earnings yield isn’t 4%, but 2% (for a p/e ratio of 50). And, mathematically, for a company whose growth rate exceeds the sum of the bond yield and the equity premium, the right p/e ratio is infinity. On that basis, stocks may have a long way to go.

Then he reviews arguments about the narrow leadership from tech companies.

Thus, it’s said, the skeptics seriously underestimate the ability of the technological leaders to grow, and to pull up the overall growth rate for the universe of common stocks. They grow every day, and so does their representation in the equity indices and in corporate America, creating a virtuous circle.

Thus, with these dominant large-cap tech companies making up a large and growing percentage of the stock market, to be bearish one has to have a thesis on why they should fall. Or else you would have to bet on the non-tech sectors to decline a great deal and pull down the averages – despite the fact that they’re already down a lot.

His final thoughts do not reach a clear conclusion – which seems about right!

Paul Schatz, Heritage Capital LLC.

The bulls have run hard this week although the window of opportunity for a decline has not closed yet. There are all kinds of cracks in the market’s foundation. So far, each and every time the market has just run over them. And before someone asks, the answer remains yes. I am still very concerned about the outperformance in the NASDAQ 100 and those 5 stocks in particular versus the rest of the market. No matter how you slice it, the fact that Apple, Amazon, Facebook, Microsoft and Netflix have been ubiquitous and dominate the various indices they are of is not a good thing.

I have no idea how this party ends. The fundamentals make perfect sense. The macro picture makes perfect sense. I only know from 32 years in the business that when everyone owns certain stocks and no one can find fault, it usually does not end well. And I am not talking about no earnings, no revenue stocks from the Dotcom Bubble. GE comes to mind as a stock that everyone owned and could no wrong. Wall Street fell over itself praising and upgrading it for years, right into its all-time high in August 2000. 8 years later it was almost insolvent.

Attempting to Meet the Challenge

I will review the key areas where I have worries. In each case I will identify both what bothers me and how I might be reassured. Please note that I am not looking for perfection on all fronts, but I am hoping for serious improvement.

Pandemic

Permanent improvement in the economy and higher stock prices depend on taming the pandemic. This can be done in various ways, but is it a requirement.

- Vaccine

- Adequate production – accelerated actions are helping with this.

- Poplar compliance – a problem at the moment, but improvement may come.

- More testing and tracing. (Bill Gates). Many do not understand the entire testing question. It has been muddled in politics. This is the best path to what I call a “balanced solution” where reopening is accelerated while the most vulnerable are protected.

In an interview with CNBC on Monday, Bill Gates had sharp criticism for the United State’s COVID-19 testing system, calling it a “complete waste” that requires a much shorter turnaround period to be truly effective.

“You should not reimburse somebody for getting a test that takes more than 48 hours to get a result back,” Gates said on CNBC’s “Squawk Box.” “That test is a complete waste. And to all these numbers about how much we test, the majority is just a complete waste. You need to get [a test] back as soon as possible so that somebody can change their behavior — so that they’re not infecting other people.”

Economy

Economic recovery will not be complete until business reopening or replacement is nearly complete and those who seek jobs can find them. Most observers are accepting the data at face value to determine where we stand. I am looking for more. We need a critical look at indicators to make sure that the violent moves have not destroyed their relevance. We should also put “diffusion” indicators aside for now.

- Business cycle (Econbrowser).

- Continued low inflation. “Davidson” (via Todd Sullivan) explains how this can justify valuation.

The 12mo Trimmed Mean PCE is reported 1.82%, down from last month’s 2% with the past 6mos revised lower. Lower inflation translates into higher Value Investor Index(VII) valuation to $2,583 for Aug 2020 with SP500 at $3,235, a 24.2% premium. The SP500 peaked in 2000 and 2007 at 100% and 65% premium levels respectively vs the VII. Those levels represent well over $5,000 in today’s low inflation environment.

Market prices represent investor perceptions of economic activity. As long as economic activity trends higher, equity prices trend higher. Coupled with falling regulations, tariff initiatives and lower taxes, the US remains in a strong economic trend implying that if conditions continue equity prices should trend significantly higher the next few years.

- Reliance on beating expectations, improvement over last month, and similar measures. We should have the standard of approaching old and/or potential levels.

Leadership

Leaders of all types must be better informed and more serious about the problems. This could apply to political actors in all branches and levels of government. I am astounded by the lack of knowledge about issues and methods. The idea of a coherent plan on any government level has been a challenge. If this were to improve, I would definitely be more bullish!

In order to avoid the sharp edges of the current political climate, let me suggest these examples.

- College football. Pac-12 Players Say Commissioner Was Dismissive of Their Virus Concerns. Yes, I know that players included assorted non-health demands.

- A promising and safe plan for education.

- College reopenings. College Reopening Plans Include How Many Coronavirus Cases Would Close Them Again

- Local school reopenings. Many people cannot resume work until schools reopen. Many students get their best meal of the day at school. This requires attention that respects the safety needs of everyone. And provides funding for it.

State and Local Government Finances

Corporate Earnings

Stock values depend upon earnings expectations. I monitor these closely and urge readers to do the same.

- So far, advance earnings have strengthened. Brian Gilmartin provides the best regular updates on this subject, so I watch his blog closely. The sell-side analysts have a good ear for corporate expectations. So far, these have been holding up.

- Acceptable market valuations depend upon the “forward earnings yield” versus alternatives. Confidence in the earnings expectations is a crucial element in what valuation is deemed to be appropriate.

Market Action

Broader strength in the market is essential. The punditry is struggling to provide excuses for the narrow market leadership. As Paul Schatz notes (above) this is a warning sign. Let us hope that Tom Lee (also above) is correct on the broadening of the market rally. I believe he will be correct on the “other side” of the recession but is too optimistic about when we will see that.

I have a few other conclusions in today’s Final Thought.

Ideas for Investors

I have switched the investor section to a separate post. I hope to run it nearly every week, calling it Investing for the Long Term. So far, I have failed in that aspiration, but I hope to do better. During the last week I wanted to write about the problem in the payroll employment report. My semi-retirement (ho ho) time is more limited, and I want to emphasize what I think is more important. Since I do not believe there is a rush to add investments, I want to emphasize the issues discussed in today’s post. I plan to do a new investment piece next week.

A Personal Favor

Please consider joining the Great Reset group. This is the key driver behind investment commentary. You will get updates about what is being studied and can join in the process. There is no charge and no obligation, but I hope you will join in my Wisdom of Crowds surveys. I need more wise participants! I have just beta-tested the new survey and it will go out on Monday. The results of our team effort will be published on a regular basis, so you will be joining me in contributing to a greater good.

We have already identified key sectors to avoid as well as those worth further examination. Articles in financial publications are only now catching up. Members have avoided some of the most dubious ideas, but there is still time for new members. I have created a resource page where you can join my Great Reset group.

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

Despite the improving technical indicators, I continue my rating of “Bearish” in the overall outlook for long-term investors. We should also keep watch on the increase in anticipated inflation. So far it has not affected bond prices (Thanks, Chairman Powell) but it eventually will.

The C-Score remains at levels never before seen. It is combining the sharp economic rebound with pandemic effects. When we are able to separate the two, a current mission of Dr. Dieli, it will provide more guidance on the timing and extent of the recovery.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian also takes note of the improvement in corporate credit spreads.

David Moenning: Developer and “keeper” of the Indicator Wall.

Doug Short and Jill Mislinski: Regular updating of an array of indicators, including the very helpful Big Four.

Georg Vrba: Business cycle indicator and market timing tools. Georg’s iM-Weekly Employment Monitor shows “no sign of a recovery.”

Guest Commentary

Conference Board data shows the recent increase in consumer inflation expectations.

James Picerno ponders the possibility for negative real yields.

Meantime, the demand for safety and an expectation for firmer inflation co-exist. If recent headlines are a guide, it’s not difficult to imagine that these two trends could persist for the foreseeable future. That may drive some observers batty, but Mr. Market answers only to himself in setting prices. The truly tough part is left to mere mortals: explaining the rationale.1

And based upon the last 34 years of data, the Fed is likely to be on hold for a long time.

Final Thought

This was a challenging exercise. I did my best, but there is plenty of room for criticism and commentary. I always welcome reader reactions, but especially on this post.

The biggest difference between me and the world?

Most managers and pundits need to sound smart by explaining what everyone already knows and implying that their actual positions captured recent moves. They are motivated by driving page views and getting on TV. I don’t need to do that.

I began writing because I thought I had a message. Even though I have been right (and for the right reasons) for many years, it has not been the best marketing plan. Stubbornly, I stick to my guns. I can see that much of the popular economic analysis is superficial. If I were still at a prestigious university, I could write about that with authority. In my semi-retirement I can analyze information that will help clients and readers, but I regret that I do not have more reach. It is ironical that knowing much more than I did as an Assistant Professor gives me less authority! If there is one troubling aspect of my current life, it is that I cannot help more investors do as well as I have. The key to this:

Be willing to challenge conclusions of the big names.

I’m more worried about

- The China challenges are somewhat under the radar, despite increasing small disputes.

- The train wreck of electoral politics in the face of needed action and coordination remains on my list of worries. Electoral motivations are supposed to be how democracy works, but this is painful to watch.

I’m less worried about

- The upcoming election. It is everyone’s hot topic and the cover story for Barron’s. I’ll write a post at some point, but for now I do not see it as important. Outcome not known, policies not known, ability to implement not known.

- Local conditions. Arizona cases seem to be improving, but I remain cautious on my rare excursions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All