2Q 2020 GMO Quarterly Letter

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGOVERNMENT BONDS HAVE GIVEN US SO MUCH

Do they have anything left to give?

By Ben Inker

Executive Summary

The recent fall in cash and bond yields for those developed countries that still had positive yields has left government bonds in a position where they cannot provide two of the basic investment services they have traditionally provided in portfolios – meaningful income and a hedge against an economic disaster. This leaves almost all investment portfolios with both a lower expected return and more risk in the event of a depression-like event than they used to have. There is no obvious simple replacement for government bonds that provides those valuable investment services. As a result, investors would be well advised to think critically about not only what their fixed income portfolios can feasibly achieve going forward but also what the implications are for the amount of risk they can afford to take across the rest of their portfolios.

A ROADMAP FOR NAVIGATING TODAY’S LOW INTEREST RATES

By Matt Kadnar

Executive Summary

Today’s low bond yields, which are without precedent in U.S. history, create several challenges for investors. Three crucial ones for investors to contemplate are: how can we replace the income that bonds used to supply; how can we adapt portfolios for the loss of depression protection that comes from bond yields having little or no room to fall; and how can we protect our portfolios from the risk of rising inflation and rising interest rates? Each of these challenges is unique and requires a different playbook than what we have used over the last 30 years. They will also require more dynamic allocation between the opportunity sets. We will take you through each of these issues and propose portfolio solutions to help adapt portfolios to today’s anemic interest rate environment.

GOVERNMENT BONDS HAVE GIVEN US SO MUCH

Do they have anything left to give?

By Ben Inker

When I was a student studying finance, I was taught that government bonds served two basic functions in investment portfolios. They were there to generate income and provide a hedge in the event of a depression-like event.1 For the first 20 years or so of my career, they did exactly that. While other fixed income instruments may have provided even more income, government bonds gave higher income than equities and generated strong capital gains at those times when economically risky assets fell. For the last 10 years or so, the issue of their income became iffier. In the U.S., the income from a 10-Year Treasury Note spent the last decade bouncing around levels similar to dividend yields from equities, and in most of the rest of the developed world government bond yields fell well below equity dividend yields. The falling levels of income caused us to question what had become an implicit article of faith for many investors – that a balanced portfolio could generate 5% returns over inflation in the long run. But while the income side of the equation for bonds was clearly not what it once was, until very recently we have continued to assume that bonds could accomplish their other important task, providing capital gains in the event of an economic disaster. This winter, U.S. Treasuries once again did their hedging job admirably, providing substantial positive returns when riskier assets fell in the early stages of the Covid-19 crisis. But that success has come at a cost. At today’s yields, U.S. Treasuries not only fail to provide a useful amount of yield to investors but also have likely lost their ability to hedge in the event of further economic trouble.

While developed government bonds do provide other useful services to investors – they continue to be one of the most reliably liquid assets investors can own, and for investors with long duration liabilities their duration itself is a risk-reducer – the loss of those two critical services demands that investors rethink the role of government bonds in their portfolios. The bad news is the loss of these services means that traditional portfolios are both riskier and lower-returning than they used to be. Non-traditional portfolios have some ability to sidestep the trouble, but frankly it is hard to envision a diversified portfolio that is not worse for these changes in the characteristics of government bonds. Our belief in this shift owes nothing to assumptions of mean reversion in interest rates. Whether or not bond rates rise in the future, from today’s levels government bonds cannot provide the depression hedge they did in previous cycles. That isn’t to say that whether rates rise in the future is irrelevant. If rates stay where they are, bonds give little income but do at least outperform cash, given the positive slope to the yield curve. Only a mild increase in rates would destroy that outperformance as the yield cushion of bonds over cash is overwhelmed by capital losses in even a minor upward move in bond yields. On the other hand, rising bond rates would give hope to buyers of tomorrow’s bonds, because those bonds might be able to do their traditional jobs. But any future rate rise does not help investors who need to build their portfolios today.

Given that there is no single asset that can obviously fill the roles government bonds formerly played, we believe that fixed income still has an important place in investor portfolios. But investors would be well advised to think more critically about what investment services they truly need from their fixed income portfolios and how the rest of their portfolios will have to change given a realistic assessment of what the fixed income portion of their portfolios can deliver.

So Much for Income

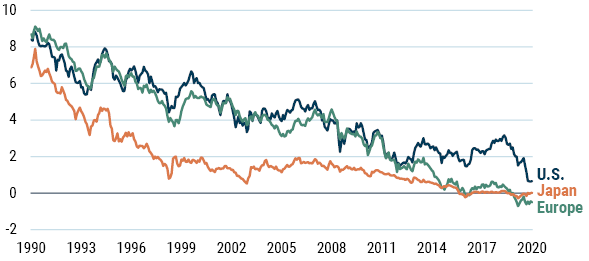

The income aspect of fixed income is certainly a straightforward and measurable concept. Exhibit 1 shows the yield on bonds in Europe,2 Japan, and the U.S. over the last 30 years.

EXHIBIT 1: 10-YEAR GOVERNMENT BOND YIELD

As of 6/30/2020 | Source: Datastream

I can well remember complaining about the desultory 2% yields prevailing in the Japanese bond market 20 years ago. Little did I realize that in another two decades I’d find myself thinking wistfully about getting a 2% yield on a government bond and wondering when and if it would ever happen again!

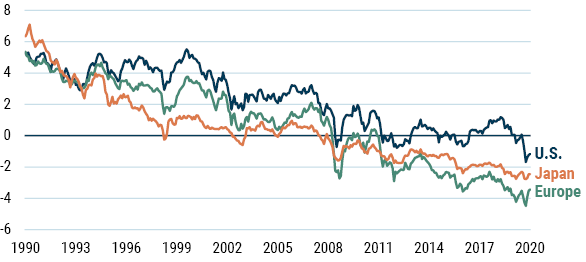

As Exhibit 1 shows, the absence of yield from government bonds isn’t exactly news in Europe or Japan. It is news in the U.S., even if yields over the last 10 years have been only a fraction of their yields of earlier decades. Comparing bond yields to equity yields – equities, after all, are another place in the portfolio where income is available – doesn’t make the case for government bonds look any better, as we can see in Exhibit 2.

EXHIBIT 2: 10-YEAR GOVERNMENT BOND YIELD LESS STOCK MARKET YIELD

As of 6/30/2020 | Source: Datastream, MSCI

In both Europe and Japan, equities have offered higher income than government bonds for 10 or so years. The U.S. was treading water with similar yields for stocks and bonds over that period, but the recent jag down has left those bonds joining the others with a sub-equity yield.

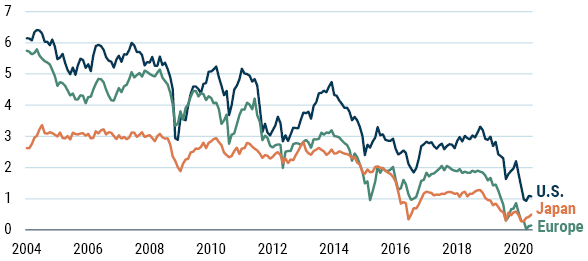

Now, 10 years is a pretty long time in investing, but the fall in bond yields is not simply a statement that the markets are making about the difficulty in emerging from the Covid-19 crisis. Even if we look at very long bond rates, the markets are saying things will stay unprecedentedly low for an unprecedentedly long time. Exhibit 3 shows the implied rate of a 20-year interest rate starting in 10 years’ time across the three markets.

EXHIBIT 3: 10-YEAR FORWARD 20-YEAR INTEREST SWAP RATE

As of 6/30/2020 | Source: Datastream

Possibly surprisingly given the huge drop in short-term interest rates driven by the Global Financial Crisis, very long rates weren’t very different in 2010 than they had been in early 2008. This time, however, long rates began to fall sharply even before the Covid-19 crisis and are now decisively at all-time lows. While rate markets have been far from unerring predictors of the distant future, they are saying this low-income environment will persist out as far as they are capable of stating an opinion.

Bye, Bye Depression Hedge

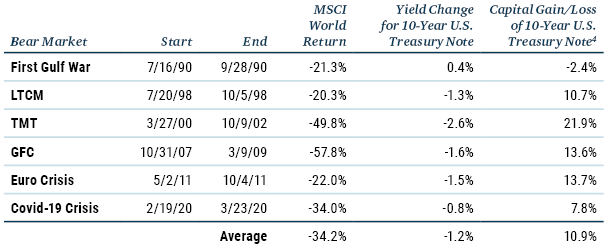

But income is only a piece of the puzzle. The inimitable charm of government bonds over the last 30 years or so has been their wonderful tendency to give capital gains when the world starts to fall apart. Table 1 shows all six bear markets3 for MSCI World in the last 30 years and the capital gain or loss of a 10-Year U.S. Treasury Note in each of them.

Source: Datastream, MSCI, GMO

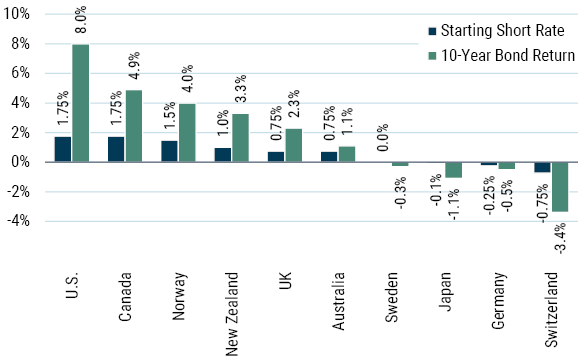

Five times out of six, the 10-Year Note did a wonderful job of cushioning the pain of the bear market, and across all six bear markets it averaged a double-digit capital gain. To put it in overall portfolio terms, a portfolio with 30% of its weight in U.S. Treasuries reduced its effective equity position in those drawdowns by 9.6 percentage points. What’s not to like about that? The fly in the ointment is that those capital gains came from an expectation that the Federal Reserve would reduce interest rates to combat any economic weakness. In each of the above events, such a reduction was possible. Today that is probably no longer true.5 And while you can argue as to whether I’m merely speculating about a hypothetical future problem, let’s look at what happened to the 10-year bonds in each of the G-10 markets during the Covid-19 crisis this winter. Exhibit 4 shows the return of the 10-year bond in each G-10 market in the Covid-19 crisis crash, sorted by the official short rate in that country as of the end of January 2020.6

EXHIBIT 4: COVID-19 CRISIS BOND RETURNS AND STARTING SHORT RATES

Source: Datastream, GMO

Note: Short rates are levels as of 1/31/2020 and bond returns are the returns from 2/19/2020 to 3/23/2020.

As you can see, those markets where short rates were meaningfully above zero saw significant gains in their 10-year bond, even if none were quite as impressive as we saw in the U.S. Those markets where the short rate was already around zero or lower, though, told a very different story. The average bond return in those markets was -1.3% and none of them had a positive return in the period. So much for hedging the losses in the rest of the portfolio!

And today, the group of countries where short rates are already around zero or lower consists of every member of the G-10, the U.S. included. As a result, it seems to me unlikely that any government bond in the G-10 would provide meaningful positive returns if the global economy should encounter further problems associated with the Covid-19 outbreak or for any other reason in the near future.7 If short rates and bond yields rise meaningfully between now and that future downturn, that might no longer be the case. But if you are counting on such a rise occurring before the next downturn, you are also counting on bonds delivering a negative return in the interim.8

There is another potential problem that this inability to reduce interest rates creates beyond what this does to bonds and cash. Central bank measures to reduce interest rates can also be a boost to equity markets directly. While it is often unclear exactly what causes equity markets to move as they do, a reduction in the risk-free rate theoretically increases the present value of the cash flow streams for equities and other risk assets, and by dropping rates in bad economic times, central banks have arguably done much to put a floor under equity markets during these difficult times. If we have indeed hit the limit on their ability to reduce rates, equities themselves are arguably riskier than they were in the prior regime. This makes the loss of potential capital gain for government bonds even more unfortunate.

What You Need, and What You Can Get

So, what does this shift in circumstances for government bonds mean for investor portfolios today? All portfolios that include government bonds have both lower expected returns and higher risk than anyone had a right to expect them to have previously. What investors should do about it depends on why they held their portfolio in the first place. Was their portfolio the riskiest portfolio that they could reasonably stand in the long run? If so, they will need to reduce risk in the rest of their portfolio, which means reducing the expected return of the portfolio even further. Was it the least risky portfolio that met their return requirements? If so, they need to increase the risk in their portfolio in the hopes of counteracting the fall in expected returns on fixed income.

The reality is that the investment problems we are all trying to solve are generally more complex than either of those representations. There is usually not a level of volatility or economic risk that is either the “right” level or even the “maximum allowable” level. Nor should there be a particular expected return that is viewed as absolutely required, regardless of the risk that would be required to achieve it. All investing is about trade-offs. For almost all portfolios, those trade-offs have suddenly gotten worse because of what has happened to the yields on cash and government bonds. At some level, this has been true for several years. The Purgatory versus Hell9 scenario analysis we have talked about for a number of years was driven by the fact that return expectations should have dropped given what had happened to bond and cash yields since the middle of the last decade.10 But our concerns back then were really with the expected return part of the equation. While the yields on cash and bonds had fallen, they had not yet fallen by so much that they were incapable of providing protection in a depression scenario.11 Today, there is certainly a quantitative change to bond expected returns. The math of bonds is unforgiving and expected bond returns must be lower given what has happened to their yields. But beyond this expected return change, investors also need to recognize the important qualitative change in any rational expectation for future bond behavior, because there is no longer meaningful room for yields to fall in the event of an economic crisis. For those who build their portfolios using a historical covariance matrix, that covariance matrix is no longer a decent guide to what the future behavior of bonds will be. For those who build their portfolios in a less quantitative fashion, I think the most reasonable way to think about the challenge for portfolio constructors is that the investment services that bonds can deliver to a portfolio have changed. Investors in need of the investment services that bonds once provided will probably have to look beyond their bond portfolios to get some of those services.

To turn that into a more concrete example, a 60% stock/40% government bond portfolio has historically “acted” as if it had only around 50% of the portfolio in stocks in the bear markets of the last 30 years. We cannot expect that kind of behavior from a 60/40 portfolio going forward, but we can build a portfolio that has that risk characteristic in expectation if desired. One simple way to do it would be to reduce the equity weight to 50% from 60%. The downside, of course, is that will reduce expected returns considerably. It also feels somewhat counterintuitive to be increasing the weight of an asset (government bonds) in your portfolio when it has just gotten worse in both its expected return and risk characteristics. Expanding the opportunity set beyond stocks and traditional government bonds is very likely to make for a better trade-off.

Perhaps the first stop one might make outside of traditional government bonds is less traditional government bonds. Inflation-linked (IL) bonds have been issued for decades now and have some interesting features relative to traditional bonds. First, because they offer a “real” (inflation-indexed) yield, their rates do not have a particular bound at or around zero. In a world where nominal yields stay low and inflation rises, IL bonds can move to materially negative yields, and we have seen such yields in the UK for years. This means that zero or negative yielding IL bonds can still offer a potential capital gain. The circumstance in which they would do so is not depression (depressions are usually disinflationary) but stagflation.12 Stagflation is a big problem for most portfolios because both stocks and traditional bonds tend to lose money in weak, inflationary economies. This leads to large losses in investment portfolios, potentially larger than in a depression scenario where bonds at least are spared pain. But while stagflation is a bad event for portfolios, depression is a significantly worse event for most problems that a portfolio exists to help solve, as I have written about in the past.13 IL bonds are not as good a depression hedge as traditional bonds, nor would they help from an income perspective today. For those who use their government bonds as a liquidity source, IL bonds also have the downside of being significantly less liquid than traditional government bonds. All in all, IL bonds seem as if they may be a superior choice to nominal government bonds today (at least they do hedge in an event that is nasty for portfolios, even if it is not the very worst event that could befall you), but they are far from a panacea.14

But how about a way to get some income and some depression protection for your portfolio? Somewhat paradoxically, risky bonds might help on both fronts. Today, high yield corporate bonds and emerging country debt are both trading at wider than normal spreads over U.S. Treasuries. Both asset classes clearly have plenty of downside risk in the kind of environment when equities are likely to fall, but they are almost certain to fall significantly less than equities in really bad economic scenarios. Taking 10% out of stocks and moving it into risky debt won’t reduce portfolio downside by that full increment, but if we were to assume the downside for those risky debt assets in the bad scenarios was going to be half as bad as for equities, it is very plausible that a 45% stock/10% risky debt/45% government debt combination would be a better blend than 50% stocks/50% government bonds,15 providing more income and no worse expected returns in a depression scenario.

And going beyond traditional fixed income entirely, other assets or strategies beyond fixed income and equities may be able to help. Besides credit, plenty of other liquid alternative strategies can provide expected returns above cash and bonds while having less economic risk than equities. They usually don’t provide an explicit depression hedge. As we saw with risky debt, that isn’t necessarily a problem if you adjust the risk level of the rest of your portfolio to compensate. But if you really want to find an effective depression hedge, there are strategies that can fill that need. Put options on stocks or a long position in volatility or any of a variety of tail hedge strategies can deliver a fairly reliable depression hedge. What had made government bonds so valuable in the past, however, is the fact that they provided their depression hedging service while still giving a return materially higher than that of cash. In contrast to that pleasant combination, almost all tail insurance has a negative long-term expected return. In fact, a negative expected return is generally the case for pretty much anything with “insurance” in the name. We don’t buy auto insurance or health insurance or life insurance because we believe the expected return to the policy will be positive, but because we think the risk reduction of having the insurance is worth the reduction in expected wealth we get from taking on the contract. Depending on how wedded an investor is to the non-bond portion of his or her portfolio, tail insurance might make sense for an analogous reason. But given that portfolios are a lot easier to change than other aspects of one’s life, in the majority of cases the right call is probably taking less risk in the rest of the portfolio instead of adding a negative expected return hedge to a portfolio that is otherwise unacceptably risky.16

So, what should a thoughtful investor do? First, I think it would be an excellent idea to sit down with your fixed income portfolio managers and make sure you and they are on the same page as to what the portfolios they are managing on your behalf are trying to achieve given the new environment and what a realistic return expectation for the portfolio is. Broadening that discussion beyond what your current strategy does to what services a different fixed income portfolio might be capable of providing and what a reasonable expected return to such a strategy is would be important as well, because it may well be that your current portfolio is no longer a good fit for your needs. Armed with that knowledge, you can then try to determine what adjustments in the rest of the portfolio can help deliver an acceptable risk/reward trade-off overall. My colleague, Matt Kadnar, has written a companion piece to this letter (“A Roadmap for Navigating Today’s Low Interest Rates”) detailing some of the strategies we are using in our asset allocation portfolios to deal with this new reality.

The task of investing has unquestionably just gotten harder. Investors will need to think more creatively than they have had to historically in order to get the services they used to get from bonds or to build a portfolio that doesn’t require those services in the first place. That task is by no means impossible, but in a world where historical performance is much less relevant for forward-looking expectations, it will require more thought and creativity than it once did.

A ROADMAP FOR NAVIGATING TODAY’S LOW INTEREST RATES

Matt Kadnar

Filling the Income Void

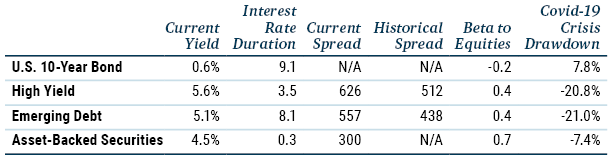

Moving past government bonds into the wider spectrum of credit provides several ways to add income above government bond yields. While credit spreads have come in from their Covid-19 crisis wides, they generally remain elevated from those recorded at the beginning of the year, providing investors with greater return potential. Bankruptcy risk has increased through the crisis, making the return-to-risk of owning high yield more difficult to assess, but having the ability to add to high yield if spreads widen and taking advantage of security allocation each represent return potential. We would also argue that this is likely to be a long bankruptcy cycle as this economic crisis plays out and allocating to distressed debt – particularly employing more nimble managers – has great potential. Likewise, spreads in emerging market debt remain elevated and the potential for security selection alpha remains high given the liquidity of the asset class and the macro uncertainty in the many different countries comprising the emerging debt universe.

Asset-backed securities have always comprised an intriguing asset class to us, in part, because they are often overlooked and unloved. These are generally complex instruments, which we believe means there are opportunities to add significant alpha after thorough analysis. Interestingly, asset-backed strategies can often take more idiosyncratic and less macro-oriented risk, thereby lowering their overall contribution to the riskiness of a portfolio than is typical of traditional credit. Asset-backed securities are also primarily floating rate instruments that help in a rising interest rate environment.

While we can find several sources to help fill the income void from lower-yielding government bonds, credit is vulnerable to deflationary shocks (see Table 1) and is also prone to increased illiquidity during times of stress. In a portfolio, the benefit of the additional income and total return from credit must be balanced off against the increased depression risk and illiquidity that comes with it.

TABLE 1: EVALUATING INCOME REPLACEMENT

As of 7/31/2020, Drawdown data: 2/29/2020 – 3/23/2020 | Source: Bloomberg

Note: The proxy for asset-backed securities in the absence of an index is the GMO Opportunistic Income Strategy.

Through our analysis and based on the opportunity set and alpha potential, in our Asset Allocation portfolios we have allocated to the following GMO strategies: High Yield, Emerging Country Debt, Credit Opportunities (distressed debt), Opportunistic Income (asset-backed).

Depression Protection and Tail Hedging – the Need for Discipline

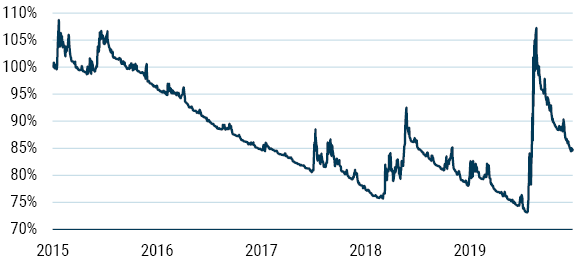

Over the last 30 years, bonds provided both income and depression protection, or a tail hedge, for investors. It was a phenomenal combination and unique for almost all tail insurance. As Ben Inker points out, insurance is generally a negative-expected-return endeavor and bonds have defied this expectation quite well. Today as we look at other tail hedges, we do not find that holy grail of both positive expected return and negative correlation to risky assets. This means that for depression protection, investors must turn to tail hedges that bring with them the very likely prospect of negative expected returns over a number of years before the potential payoff. For some investors, this may be a reasonable trade-off. However, there are reasonable caveats to consider before embracing this approach.

Investing in tail hedge strategies requires substantial discipline. Properly structured tail hedges pay off in the scariest of times – either extreme economic duress or some period of extreme geopolitical uncertainty. Like any good rebalancing strategy, investors should be moving out of strongly performing tail hedges and into beaten-down risk assets. This requires selling those tail hedges at the point of maximum uncertainty, which is difficult to do to say the least. Having a firm plan in place before the extreme event occurs is critical to using tail hedges to maximum effectiveness. To illustrate, we constructed a simple put-buying strategy1 and plotted its returns over a 5-year period (see Exhibit 1). It is evident that this form of insurance had some significant benefits in the spring of this year. Of course, enduring a drawdown of more than 25% of the original capital before receiving the payoff would have been unnerving. And failing to rebalance in the spring would have caused a substantial loss over the succeeding several months. Rebalancing from tail hedges in times of crisis really matters. The negative carry peculiar to most tail hedges prevents them from being a “set it and forget it” type of strategy.2 The depression hedge that has provided the best success for GMO (excluding government bonds) has been our Tactical Opportunities Strategy, which is long high quality stocks (which tend to do well in bad economic times; these companies are well insulated from bankruptcy) and short low quality stocks (or, at times, the market). Again, rebalancing can be critical.

EXHIBIT 1: CUMULATIVE LOG RETURNS OF PUT-BUYING STRATEGY

As of 7/31/2020 | Source: GMO

Rising Inflation and Interest Rates – an Underappreciated Risk?

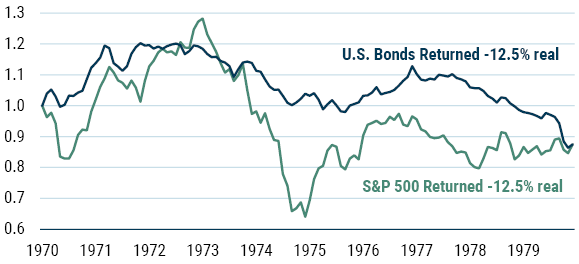

One of the biggest risks investors face today is one they have not had to worry much about over the last 30 years: rising interest rates. Rising interest rates negatively impact all assets with duration, namely stocks and bonds, with stocks actually faring worse because of their longer duration.3 The 1970s and early 1980s was the last period of rising rates, and it is easy to see the havoc this caused on both stocks and bonds, with each asset type delivering an annualized 1.3% real return (see Exhibit 2).

EXHIBIT 2: IMPACT OF RISING RATES ON STOCKS AND BONDS IN THE 1970S

Source: GMO, Federal Reserve, Bloomberg

The culprit behind those rising rates? Unanticipated inflation. While the prospect of unanticipated inflation may seem quite far removed today given the deflationary shock caused by the Covid-19 crisis, we believe inflationary seeds are being sown. We are experiencing unprecedented monetary and fiscal stimulus on a global scale. The growing support of Modern Monetary Theory and its insouciance to risks associated with increasing government deficits increases the potential for inflation. Traditional economics suggests this is likely to be inflationary. While the track record of economics on inflation leaves something to be desired, the combination of massive money creation and fiscal stimulus, a supply shock coming from a retreat from globalization, and the potential failure of many small and midsized companies means the potential for inflation simply cannot be ignored by investors.4

We are still a bit skeptical on the return of 1970s’ style inflation, which can truly wreak havoc on an economy. Inflation averaged over 7% annually during the 1970s5 as the spike from the 1973 OPEC-led oil embargo fed through to wages, inducing a wage-price spiral. Potential higher structural unemployment due to the lasting impact of Covid-19 makes it less clear we will get the type of wage pressure that would cause an extended period of truly scary inflation rates like those of the 1970s.

A rising trend level of inflation or elevated, cyclical bouts of inflation due to fiscal stimulus or supply factors could have significant impact on the psyche of investors, resulting in important implications for portfolios. Inflation rates of 3% or 4%, somewhat tame by historical standards, could feel significantly worse to investors or consumers given the very low rate of inflation we have seen the past couple of decades. Bonds are highly vulnerable to increased inflationary concerns given today’s lower yield and higher duration.6 Equities, with their long duration, would not fare well with increased inflation as the associated uncertainty generally results in investors demanding a higher margin of safety, i.e., lower P/E to own equities.

Even if you do not believe there is a material risk of rising interest rates, there still appears to be limited reward for holding duration in your portfolio. Below we assess potential solutions for lowering your interest rate risk (duration) while still generating return through Liquid Alternatives, Value and Resource stocks, and Inflation-linked bonds.

Reducing Your Duration Sensitivity by Adding Liquid Alternatives7

Cash is the ultimate liquid asset and has approximately zero correlation with other assets. However, owning cash while yields are at 13 basis points feels a bit like chewing glass. We have allocated more recently to Liquid Alternatives (Liquid Alts) strategies to generate a return over cash but with relatively lower beta and shorter duration.8 The long/short nature of most Liquid Alts removes the duration associated with both stocks and bonds.9 While Liquid Alts generally do have a small amount of beta, they will not be the equity hedge that bonds have been in another deflationary bust. However, in terms of generating overall returns for a portfolio and serving as a lower-duration substitute for bonds, Liquid Alts are an important tool.

For our Liquid Alts positions, we have allocated to pure alpha strategies (for example, GMO Systematic Global Macro and GMO Fixed Income Absolute Return) and the more diversified Alternative Allocation Strategy, which combines our long-tenured alpha strategies and insurance-like activities in put-selling (GMO Risk Premium) and merger arbitrage (GMO Event Driven). We like this combination of alpha and insurance-selling activities to provide a more durable pattern of returns over time.

Many investors have been disappointed with returns more recently for Liquid Alts, particularly Alternative Risk Premia (ARP) strategies. We have seen a proliferation of ARP strategies and view many as being commoditized. They can also be more highly correlated in times of stress as they anchor to common, underlying risk factors. Understanding the sources of return for a Liquid Alts portfolio, the inefficiencies being exploited, how the portfolio will behave in times of stress, the fees per unit of expected return, and the prudent use of leverage in a portfolio are all important factors in analyzing Liquid Alts strategies.

Value Equities – Exceptionally Cheap and Lower Duration

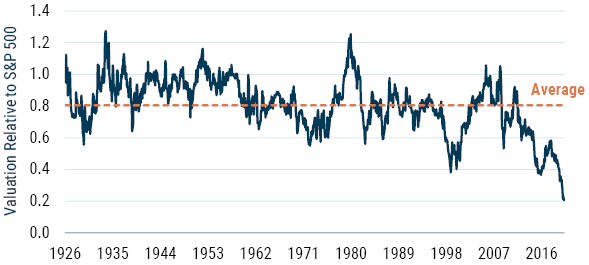

Rotating into Value stocks offers substantial upside in terms of return versus the broad market10 and has the favorable portfolio characteristic of lowering overall duration. We have written extensively over the last several years about Value11 and our view continues to be that Value stocks may be bruised, but they are not broken. However, in the marketplace, investors have been voting with their feet, selling Value stocks and propping up the return and subsequent valuation of Growth stocks (see Exhibit 3).

EXHIBIT 3: GROWTH OUTPERFORMANCE EXCEEDS FUNDAMENTALS

MSCI Growth / Value relative price and relative forward earnings indexes

As of 7/31/2020 | Source: GMO, Minack Advisors, IBES

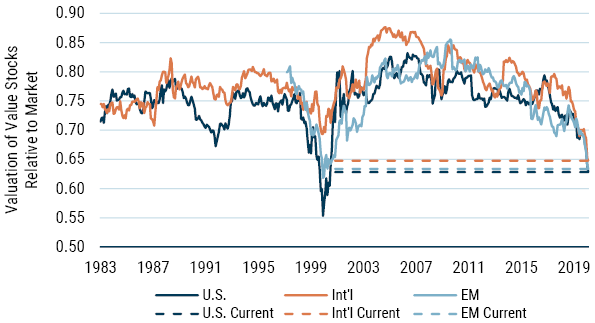

The result of this activity is that there is opportunity within Value stocks, which are in the top decile of attractiveness around the world (see Exhibit 4).

EXHIBIT 4: SPREAD OF VALUE FOR MSCI REGIONAL VALUE FACTORS

As of 6/30/2020 | Source: MSCI, Worldscope, GMO

In addition to currently being very cheap relative to the market, allocating to Value stocks also helps lower the duration of your portfolio. Value tends to have a higher dividend yield, so you get more of your return earlier than with Growth stocks, where you are more dependent on cash flows further into the future. How much Value lowers your effective duration is a more complicated issue because you also need to make assumptions on the changes in the discount rate, the return rates on invested capital (as the discount rate changes), changes in payout rates, etc. As you can see in Table 2, the duration difference between Value and Growth can be quite significant.

TABLE 2: THE SENSITIVITY OF EQUITY TO CHANGING DISCOUNT RATES

As of 7/31/2020 | Source: GMO, Bloomberg

Value provides more current income, a cheaper and therefore more resilient asset, and lowers the duration of your equity portfolio. This sounds pretty good to us, but given Value’s performance, we clearly stand in the minority. There is an aura of invulnerability for Growth stocks and a revulsion for Value stocks today that rivals 1999, but there are some important differences between today’s Growth and Value environment and what we saw then. There are portions of Growth, specifically large cap Technology, that are vastly more profitable than what we saw during the TMT Bubble.13 But there remains a sizeable portion of the Growth universe that is very expensive, low quality, and, in many instances, quite levered. There are also considerable risks to parts of Tech that are vulnerable to increased regulation relating to their dominant positioning within their markets and increasing media content.

Value is also more complicated than it was in 1999. Traditional value tools such as Price/Book and ROE have been distorted by the growth of intangibles on the balance sheet and capital-light businesses. We have made significant adjustments to our valuation framework to keep pace with these changes. The simple Value factor has more “value traps” than it did 20 years ago, requiring investors to be more discerning as to what true fundamental “value” for a company is today. This is something our Global Equity and Emerging Equity teams have spent years researching, and we have made significant changes to how we define book value and ROE today versus the recent past.

Resource Equities as a Value Opportunity and Inflation Hedge

Resource-based equities14 provide an interesting mix between a significant opportunity within Value equities today (thus lowering overall duration) and a hedge against future inflation. From a Value perspective, Resource equities, particularly Energy and Metals stocks, appear to be trading at the cheapest levels they have ever been relative to the S&P 500 (see Exhibit 5).

EXHIBIT 5: VALUATIONS ARE AT HISTORIC LOWS

As of 6/30/2020 | Source: S&P, MSCI, Moody’s, GMO

Valuation metric is a combination of P/E (Normalized Historical Earnings), Price to Book Value, and Dividend Yield.

Metal producers are also an interesting subset because they are in a secular growth mode as the world transitions to more clean energy. This cannot be done without metals such as copper, lithium, nickel, vanadium, etc.15

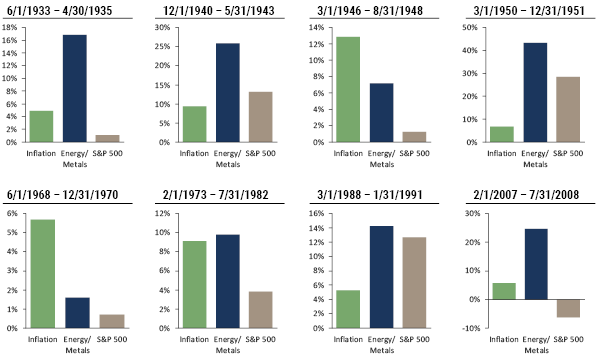

Resource stocks have also been a very useful tool in inflationary times. Exhibit 6 shows the return of Energy and Metals stocks during the more significant (CPI greater than 5% for a year or more) bouts of inflation we have seen in the U.S.

EXHIBIT 6: DURING INFLATIONARY PERIODS, RESOURCE EQUITIES HAVE PROTECTED PURCHASING POWER BETTER THAN THE BROAD EQUITY MARKET

Source: S&P, CRSP, Global Financial Data, MSCI, GMO

Annualized data. Inflationary periods have been identified as periods where inflation, as measured by CPI, was greater than 5% per annum for a period longer than one year.

During these inflationary periods, Energy and Metals stocks kept up with or beat inflation in six of the eight periods and outperformed the broad market in all eight periods.

Replacing Nominal Government Bonds with Inflation-Linked Bonds

If you must own bonds in a portfolio, Inflation-linked (IL) bonds should provide some shelter from the potential inflationary storm. Receiving inflation plus a coupon indexed to inflation helps offset the rise in interest rates that can afflict nominal bonds.16 This unfortunately is not a cure-all because there is a significant risk that IL bonds would still be vulnerable to a rise in real interest rates as investors potentially demand an additional margin of safety for the inflation uncertainty. They would almost certainly outperform nominal bonds in such a scenario.

Current yields on IL bonds in much of the developed world are negative. In July of 2020, the U.S. 10-Year TIPS reached a historic low of -1.0% real yield. Investors are locking in a negative real return on their money for 10 years. We cannot dismiss the possibility that an inflation scare would increase the demand for inflation-protected bonds, further lowering rates. It is hard to bet on an expensive asset (and we would argue that a real yield of -1.0% for 10 years is an expensive asset) becoming more expensive.

Inflation-linked securities do tend to be much less liquid than nominal bonds. We have seen violent fluctuations in the TIPS market this past spring where yields rose more than 100 bps in less than 2 weeks (an enormous move in the bond market). We saw moves of similar magnitude but over a longer duration in 2008 during the height of the GFC and during the Taper Tantrum in 2013. A large participant in this market is risk-parity strategies that will often lever TIPS as part of their investment strategy. Levering less liquid assets can add fuel to the fire during times of crisis, which helps explain these types of extraordinary moves.

A Word or Two About Gold

No discussion of the investment implications of inflation would be complete without addressing gold. For a valuation-based investor, gold presents some real difficulties. There is no yield or cash flow from the asset, making any type of valuation all but impossible. The most compelling case for gold is one based on opportunity cost. Gold has delivered an approximate zero percent real return over the last several millennia (quite impressive for an asset that produces no cash flow). If you assume the real return for gold is going to be zero, you can own gold rather than other negative real yielding bonds. In our traditional portfolios, we would prefer owning higher-returning Liquid Alts and Value strategies.

Conclusion: The Need to Be More Dynamic

Today’s very low yields on high-grade government bonds is making life difficult for most investors. It is hard to achieve 5% real or 7% nominal return rates for institutions and savers alike with government bonds yielding far less than 1%. Add in the inflation uncertainty brought about by previously unimaginable levels of fiscal and monetary support and Covid-19-based supply disruptions and owning government bonds becomes doubly difficult. Questioning the role of bonds and exploring alternatives are critical to meeting return objectives. Fortunately, there are some significant opportunities within asset classes that align themselves with these macro uncertainties. We believe taking advantage of higher-returning opportunities in Liquid Alts, the extraordinary cheapness in Value and Resource stocks, and floating-rate asset-backed securities while simultaneously lowering your overall portfolio duration provides the ability to still generate returns despite very challenging bond valuations. These opportunities also require investors to be more dynamic in thinking about portfolios. There are times where asset classes like Value or Credit may look more attractive and other times substantially less so. Thinking more dynamically about these opportunities will help increase your ability to continue to generate the returns you need.

Footnotes for: Government Bonds Have Given Us So Much

1 There are a couple of other services that investors prize from government bonds – liquidity and duration. I honestly can’t remember the liquidity benefit coming up much in any of my classes or textbooks. In those ancient days before the rise of private equity and hedge funds, people seemed to take it for granted that their portfolios would be acceptably liquid even at those times when portfolio returns were bad. Certainly, my finance professors seemed to take it for granted. The idea that asset duration had an intrinsic benefit for investors with long duration liabilities was also notably absent in the discussions we had in the late 1980s and early 1990s. I can remember our head of quantitative equities at the time, Chris Darnell, making the point in the early 1990s that corporate pension plans investing in equities was an oddly tax-inefficient way for companies to lever themselves on behalf of investors, but the idea that long duration bonds were a better match for the liabilities of a pension fund seems to have taken another decade or two and some accounting changes before it came to the attention of investors.

2 Europe is proxied by Germany for Exhibits 1, 2, and 3.

3 I’ve used the traditional definition of a bear market as a 20% peak-to-trough fall.

4 Strictly speaking, this is the capital gain or loss of a bond of precisely 10 years’ maturity at the start of the bear market with a coupon of the yield of the Datastream U.S. 10-Year Government Bond Index on that date that instantaneously had its yield change to the yield at the end of the bear market. I’m using capital gains rather than total returns because in a bear market of longer duration the income return to bonds would be naturally much greater. The capital gain aspect is much more comparable across time periods of different lengths.

5 Clearly, the moves by the ECB and a few other central banks have shown that it is possible to bring short rates down below zero. I’d argue the subsequent performance of the economies where this has been done suggests that there was no obvious benefit to the economy from having done so. Furthermore, the Federal Reserve has stated a strong reluctance to make such a move, and the structure of U.S. finance and the central role played by money market funds would probably make a move to negative rates significantly more disruptive than it was in Europe.

6 You’ll have to forgive me for making slightly arbitrary choices on the official short rate in some markets. In the Eurozone, for example, there are several rates that could be described as the official short rate. The -0.25% rate I'm using is neither the highest nor lowest that one could plausibly claim as the official short rate in the Eurozone, but none of the other plausible candidates would change the picture in any meaningful way.

7 If true, this means the calculus for liability-driven investors may have changed. If the “risk” of rates falling meaningfully from here is low, it is less obvious that the first priority of investors with long-dated liabilities should be to find assets with similarly long durations. While I admit that may seem cold comfort for pension funds that have seen the value of their liabilities swell yet again with an unexpected fall in their discount rates, it really does seem plausible to believe this may be the last time this will happen.

8 This is certainly true of all the bonds with negative current yields. For those markets with positive current yields it is possible that if the next downturn takes long enough to occur, we could see a rise in bond yields between now and then that didn’t require a negative return along the way, but it would imply a very gentle increase in yields persisting over a lot of years to “recharge” the depression hedge, and any positive returns would be insignificant even in that case.

9 We also refer to this as mean reversion versus partial mean reversion.

10 The difference between Purgatory and Hell (or mean reversion and partial mean reversion) comes down to whether the drop in return expectations is a temporary phenomenon (yields will eventually rise back up) or a permanent phenomenon (average yields have permanently fallen).

11 Strictly speaking, cash rates were already around zero across several markets at the time, including the U.S. But bond yields assumed that those cash rates were low temporarily. It was therefore plausible to expect that in bad economic times those expectations for future cash rates would fall further and bonds would deliver meaningful capital gains.

12 Stagflation is a circumstance in which economic growth is weak and inflation is high.

13 See GMO 1Q 2019 Letter, “Stop Worrying About Your Portfolio,” and GMO 3Q 2017 Letter, “What Happened to Inflation? And What Happens if it Comes Back?” Each paper is available at www.gmo.com.

14 A lot of what I said about IL bonds could also be said about gold. It provides no income, but over hundreds of years it has been a reasonably reliable inflation hedge. Gold might significantly outperform IL bonds in an inflationary period that is not associated with economic weakness, because real rates tend to rise in inflationary booms. Gold does suffer from the downside that it is both fairly volatile and has little “value” anchor given the limited industrial uses for gold could be met with current stocks more or less forever, requiring no further production for decades or longer. As hard as it can be to determine the fair value for most traditional commodities, for a commodity where the primary uses are ornamental and speculative it can be close to impossible.

15 That certainly seems to be true today given GMO’s asset class forecasts as of 6/30/2020. Given the high valuations of U.S. equities and their very large weight in a global equity index, a blend of high yield and emerging debt today has both a higher expected return and lower depression risk than a traditional global equity portfolio on our data. Given the extraordinary spread of valuations in equity markets today, though, that is not true if we are comparing risky debt to a value-oriented equity portfolio, because value stocks around the world are much more reasonably priced.

16 An alternative to buying homeowners insurance, for example, might be to live in a home whose value is low enough that if it burned down or got burglarized it wouldn’t be a financial disaster for you to have to rebuild it or refill it with stuff. But this will have the downside of forcing you to live in an area you wouldn’t otherwise choose and in a house that doesn’t provide a lot of housing “services.” You might be financially better off, but your quality of life would almost certainly be worse. For most of us, our investment portfolio doesn’t provide a lot of other services beyond the investment ones, so having a portfolio where you can handle the risks of bad events doesn’t reduce your aggregate quality of life. As a result, you need to have a pretty specific set of expectations about the future to believe that owning a combination of risky assets and negative expected return tail hedges is better than having your investment portfolio have less risk in the first place.

Footnotes for: A Roadmap for Navigating Today’s Low Interest Rates

1 This is an unlevered strategy that buys 1-month at-the-money puts on the S&P 500.

2 A simple put-buying strategy starting with $100 in 1986 would have resulted in remaining capital today of about $5. Ouch.

3 Approximately half the value of equities is derived from cash flows 30 years into the future.

4 Additionally, inflating away high levels of government debt is also much more palatable to politicians (the Fed included) than paying the debt back through austerity or defaulting on the debt.

5 Inflation in the 1960s averaged 2.5% versus 7% in the 1970s - a significant shock to any economic system. Inflation in 1974 and 1979 was greater than 11%!

6 The duration of a 10-year bond today is 9.5. In 1981, when interest rates peaked, the duration of a 10-year bond was 4.9.

7 We would include most hedge funds in the “Liquid Alternatives” category, but for purposes of this paper, we are referring to those that are available in mutual fund, UCITS, or ETF form.

8 John Thorndike, “Liquid Alts: Rising to the Occasion,” GMO Quarterly Letter, Q4 2018.

9 Other Liquid Alts are also inherently short duration, e.g., merger arbitrage where deals close on average in 180 days.

10 As the U.S. and EAFE are broadly expensive in our view, owning U.S. Value and EAFE Value offers strong relative return opportunities but more muted absolute return opportunities. Within emerging equities, we believe Value offers both strong absolute and relative returns.

11 Ben Inker, et al., “It’s Always Darkest Before the Dawn,” April 2020; John Pease, “Risk and Premium: A Tale of Value,” July 2019; Rick Friedman, “Value Investing: Bruised by 1,000 Cuts,” May 2019. Each of these papers is available at www.gmo.com.

12 This may seem like an oddly wide range of duration estimates for stocks, particularly for Growth stocks. The difficulty in coming up with an effective duration for types of stocks comes down to what assumptions one makes about the correlation between future growth and the discount rate. If discount rates do not impact growth or return on capital at all, the duration is at the high end of this range – in a dividend discount model framework, one can reduce (or increase) the denominator without impacting the numerator at all. But it is far from obvious that changing discount rates are truly uncorrelated with future growth, and if the numerator of a stream of discounted cash flows falls while the denominator is falling, the effective duration is much less. The circumstances in which discount rates fall are generally ones in which expectations for future economic growth fall as well. A slowing economy should generally slow the growth of even fast-growing companies.

13 The Tech sector is the largest sector weighting in the GMO Quality portfolio as of 6/30/2020.

14 We define “Resource-based equities” for the GMO Resources Strategy as Energy, Industrial Metals, Agriculture, and Water sectors and industries.

15 See Lucas White, “An Investment Only a Mother Could Love: The Tactical Case,” April 2020. This white paper is available at www.gmo.com.

16 For U.S. Treasury Inflation Protected Securities, the coupon remains fixed but the value of the interest payment increases as the coupon is paid on the inflation-adjusted value of the bond. Inflation-linked bonds are contractually linked to domestic inflationary measures such as the U.S. and Canadian CPI indexes, UK Retail Price Index, or the European Harmonised Index of Consumer Prices.

Disclaimer: The views expressed are the views of Ben Inker and Matt Kadnar through the period ending August 2020, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

© GMO LLC.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits