The field is set for the 2020 US presidential election, and markets are turning their focus to November’s contest. Historically, political transitions haven’t had much impact on the economy and markets. But with the political spectrum and breadth of potential policies widening, that will likely change.

That’s all the more true because of the circumstances in which we find ourselves. The ongoing COVID-19 crisis and resulting policy responses will likely make this election result more meaningful than normal.

Of course, we can’t predict the electoral result for the presidency or Congress, and even the market’s reaction is unclear. Four years ago, conventional wisdom said a Trump win would create policy uncertainty and be bad for equity markets—today, markets are at record highs. However, given the stakes of this election, investors would be well advised to track a few key themes.

Key Factors: Fiscal Stimulus and Tax Policy

In our view, the most important policy factor that will drive financial markets over the next several months is fiscal stimulus.

With the US economy still reeling from COVID-19, future growth rests heavily on government spending to replace lost household income. Financial markets are even more reliant: the equity market seems far above levels that the economic environment alone would justify. So, markets will be watching to see if the result makes stimulus more or less likely.

The second most important policy factor for financial markets will likely be tax policy. Equity markets have received a shot in the arm from the tax cuts passed in 2017, which bolstered corporate profits. The possible reversal of these corporate tax cuts will also be a meaningful influence on the market.

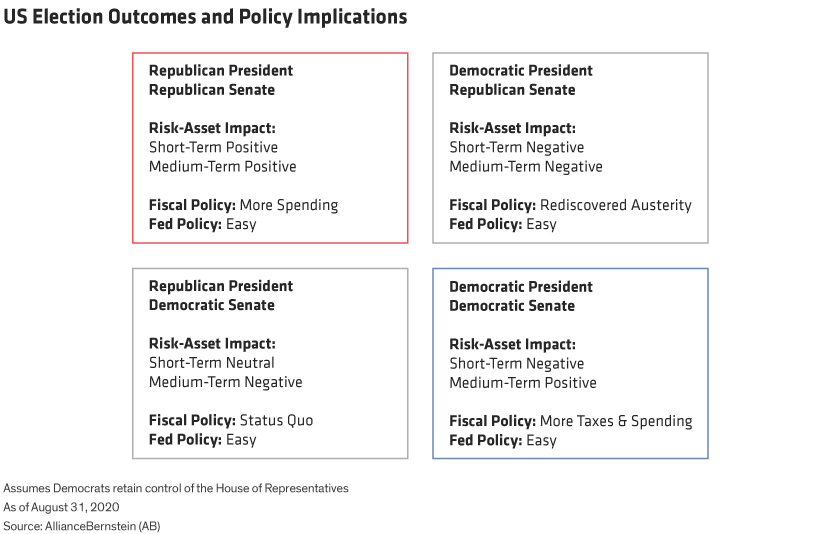

To assess the likely impact of the election on these issues, we’ve created a grid (Display) with the four potential outcomes (assuming Democrats keep control of the House of Representatives in any case). These include a red wave and a blue wave, in which one party controls both the Senate and presidency.

Red Wave, Blue Wave: Fiscal Spending as the Common Factor

A red wave (upper left), with Republicans controlling the Senate and White House, would probably represent more of the status quo, with current policies staying in place. The Trump administration cut taxes and boosted spending when the economy was strong, so there’s little reason to expect a change in a weak economy.

The president’s executive orders to push funds into the US economy despite resistance from Senate Republicans signals his policy priorities, and that resistance would likely fade in the wake of a successful electoral campaign. With more spending and possibly more tax cuts on tap, the red wave seems to be the most favorable electoral outcome for financial markets.

In the blue wave (lower right), Democrats would win the presidency and Senate (therefore controlling both houses of Congress). This outcome would be similar in some ways with the red wave in terms of fiscal policy, but corporate tax cuts would most likely be reversed. So, it seems reasonable to expect financial markets to struggle in the near-term aftermath of a blue wave.

But after a blue wave, fiscal policy is most likely to be expansive—House Democrats have already passed a $3.5 trillion stimulus bill that’s hung up in the Senate. And infrastructure spending is most likely to increase after a Democratic sweep. So, while tax policy could be a near-term market headwind, spending plans would probably benefit markets over the medium term.

Gridlock from Split Decisions: One Benign, One Not

The other two scenarios would be variations of gridlock. A Republican president and Democratic Senate (lower left) would be the more benign version, looking in many ways like the status quo in which the Senate resists White House priorities. Over time, we expect a spending agreement in this scenario but after a slow and painful process.

A Democratic president and Republican Senate (upper right) could be more problematic for markets. The Senate is already reluctant to roll out more stimulus—and would very likely prevent more stimulus spending altogether if the White House changes hands. Because the US economy and financial markets rely a lot on that spending, the risks of a double-dip recession would be very high, and financial markets very likely would suffer.

All of these scenarios, of course, depend on the election result being resolved on or fairly soon after election day. If the result isn’t clear-cut, all bets are off. Hopefully, that won’t be the case, and the US receives a clear election outcome that allows markets to process the outcome and move forward.

Eric Winograd is a Senior Economist at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein L.P.

© AllianceBernstein

Read more commentaries by AllianceBernstein