Is The Market Overbought?

The S&P 500 SPX and Nasdaq NASD have recently hit a series of fresh all-time highs and the Dow DJIA now sits less than 2% off of its all-time high which has many people wondering if the market is overbought and due for a correction. There are reasons to believe that the current market is overvalued – the July unemployment rate stood at 10.2%, second quarter GDP decreased at an annual rate of 31.7%, and there were 13.25 million continuing jobless claims this week – which is not the kind of environment in which you expect the major US indices to be hitting record highs. However, while the equity market and the economy are often discussed together, the market is a leading indicator of the economy, i.e. it reflects expectations about the future direction of the economy. Today we wanted to take a deeper dive into whether the market is actually overbought.

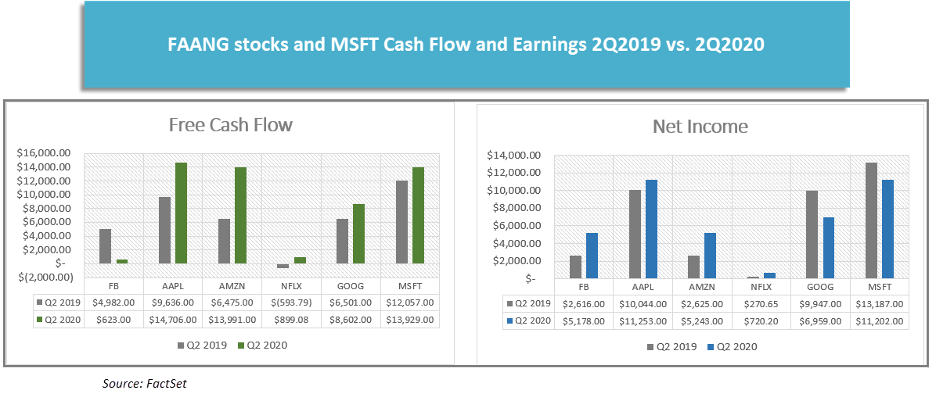

Net Income/Cash Flows

The basic model of fundamental equity valuation is a discounted cash flow model which takes the projected future earnings of a firm and discounts them backward through time to arrive at a present value for the stock. Thus, if a firm’s earnings or its expected earnings growth rate increase, then its stock price should increase. While many firms saw their earnings and cash flow decrease due to COVID-19, some firms, especially technology companies, saw their net incomes and/or cash flows rise as consumers relied more on services that could be accessed remotely. Included in these companies are the largest technology companies in the world which have large weightings in the S&P and the Nasdaq and their performance has been a major force driving the indices to their record levels.

As the graphs above show, most of the FAANG stocks and Microsoft MSFT had higher 2Q20 net income and/or cash flow than in the prior year; so by this metric, a higher valuation is justified for these companies and by extension helps to justify higher levels for the indices they are part of. It is worth noting that this is just a quick, rudimentary analysis. A true valuation would require looking into the financial statements in much greater detail, making adjustments to the stated earnings and cash flows, and making adjustments for changes in growth projections etc. However, it does show that some firms have had better earnings results since the coronavirus pandemic begin, with some of the largest companies in the market among them.

Discount Rate

One of the key parts of a discounted cash flow model is the discount rate and the level at which it is set can have dramatic impact on the overall valuation. A higher discount rate results in a lower valuation and vice versa. Many methods for constructing a discount rate begin with a risk-free rate of return and then add an equity risk premium. US Treasury yields are the most-often-used proxy for the risk-free rate and they have declined significantly since the beginning of year; the US Treasury 10 YR Yield Index TNX has fallen from around 1.9% in January to around 0.625% today. Therefore, the discount cash flow models used to value companies are using a lower discount rate, which all else equal, produce higher equity valuations.

US Dollar

Since peaking in March, the US dollar index DX/Y has fallen approximately 10%. For companies with international operations, the weaker US dollar provides a revenue boost as the foreign currency they receive is worth more in USD terms. Goldman Sachs recently estimate that a 10% decline in the US dollar increased the S&P 500’s earnings per share by about 3%. As a result, the weaker US dollar would be supportive of increased equity values.

It’s also worth noting that a weaker dollar tends to increase foreign investor’s demand for U.S. stocks as the purchasing power of their currency is higher in terms of USD. In the same article, Goldman says it expects foreign investors to buy $300 billion of U.S. equities this year, which would outstrip corporate buybacks as the largest source of purchases.

Technical Perspective

From a technical perspective, there is some evidence that the market is overbought. Prior to Thursday’s (9/3) pullback, SPX had a weekly overbought/oversold (OBOS) reading of 143%, placing it in heavily overbought territory. Even with Thursday’s move, the index had an intraday reading of 88.58% which would still put it in overbought territory. On the weekly distribution 0% is neutral, levels over 70% are considered heavily overbought and levels below -70% are considered heavily oversold. However, this does not mean that a crash is imminent or even that the outlook is negative. The table below contains all the times that the S&P has hit an OBOS level of 100% since 1957 and shows that in the vast majority of these instances the index’s returns were positive, especially over the longer time horizons.

The returns above are not inclusive of transaction costs. Investors cannot invest directly in an index or a model portfolio. Indexes and models have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. The relative strength strategy is not a guarantee.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The Dorsey Wright Sector Indexes are non-investable, equal weighted baskets of stocks including the largest and most liquid names from within each sector. The indexes are rebalanced daily and do not include the reinvestment of dividends. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.