Domestic equity markets have certainly shown a significant amount of movement thus far through 2020, with the S&P 500 Index SPX undergoing its swiftest decline from all-time highs in March, only to rally over the next few months to print new all-time highs at the beginning of September. Almost immediately after these fresh-highs earlier this month, major domestic equity indexes each saw major pullbacks from overbought territory at the end of last week, which have been largely continued based on intraday trading Tuesday. Perhaps unsurprisingly, this movement has also come with enhanced levels of volatility across major domestic equity indices. There are a variety of ways to measure volatility across broad domestic equities, with the most frequently referenced volatility barometer being the CBOE Volatility Index VIX, which provides the expected volatility of the broader market based on S&P 500 Index options. Another way we measure volatility is through the number of extreme daily moves for SPX, as classified by a gain or loss of 1% or greater. Today, we will examine an update to this SPX volatility study, in addition to reviewing how many days this year have seen daily moves exceeding 2% given the pick-up in volatility.

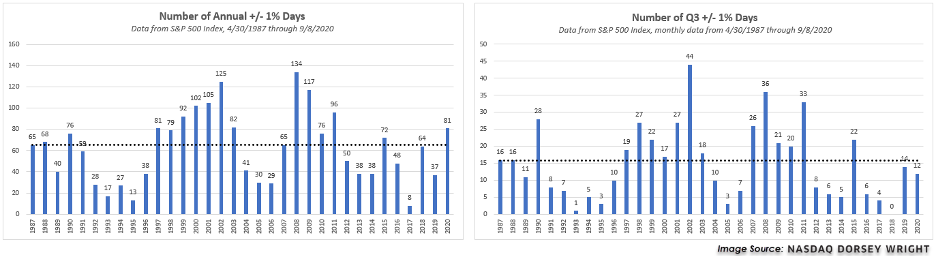

For the first part of our study, we examine the number of daily moves in which SPX shows a gain or loss of 1% or greater from April 30, 1987, through September 4, 2020. Over this timeframe, there is an average of just over 65 days a year that see an extreme up or down move for the benchmark index. However, there have been significantly more extreme days in 2020, a total of 80 days have seen SPX move +/- 1% or more. Most of these days came earlier in the year, as Q1 saw 31 extreme days, which is tied with 2008 and 2003 for the second most extreme days in the first quarter of any year, behind the 40 extreme days seen in 2009. There were 38 extreme days in Q2 this year, which is the most in Q2 of any year dating back to 1987. However, this volatility lightened thus far through the third quarter, with there being 12 days of extreme moves including the decline on Tuesday. This is below the average of extreme moves in Q3, which sits at just under 16 days. It should be noted that we still have a few weeks left until we hit the fourth quarter, and SPX has already seen 3 out of the 5 trading days in September show a move exceeding 1%, including Tuesday. With that said, we also see that September typically has the least amount of extreme days of any month, at 4.73 days on average. This is quite different than the next month of the year, as we typically see October display the most amount of extreme days at an average of almost 7 days.

The returns above are price returns, not inclusive of dividends or all transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

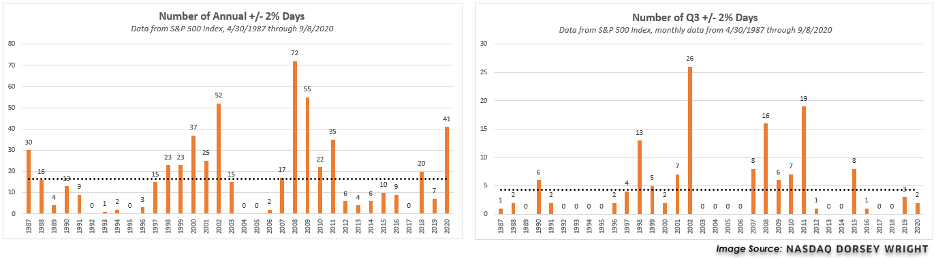

If we take a step back on our study and review the number of days where SPX has a gain or loss of 2% or more, we see a similar story. There are typically just over 16 days each year on average that see such a move, and there have been 41 days thus far through Tuesday. Out of these more extreme daily returns, 22 came in Q1 while 17 came in Q2, which are each significantly higher than their quarterly averages of about 4 and 3 days, respectively. Furthermore, the third quarter had not seen any daily moves greater than 2% until last Thursday, and there have now been 2 in the last three days. This still sits below the average of +/- 2% days in Q3, which is just over 4 days.

The returns above are price returns, not inclusive of dividends or all transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The Dorsey Wright Sector Indexes are non-investable, equal weighted baskets of stocks including the largest and most liquid names from within each sector. The indexes are rebalanced daily and do not include the reinvestment of dividends. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.